Based on the December 23rd, 2011 Premium Update. Visit our archives for more gold & silver articles.

If youre looking for a post-Christmas read, take a look at a book called The Great Stagnation by Tyler Cowen of George Mason University whose theme is laid out in its subtitle: How America ate all the low-hanging fruit of modern history, got sick and will (eventually) feel better.

The interesting aspect of this book is Prof Cowens explanation on how the US got into its predicament.

The American economy has enjoyed ... low-hanging fruit since at least the 17th century, whether it be free land, ... immigrant labor, or powerful new technologies. Yet during the last 40 years, that low-hanging fruit started disappearing, and we started pretending it was still there. We have failed to recognize that we are at a technological plateau and the trees are more bare than we would like to think. Thats it. That is what has gone wrong.

Sustained economic growth requires new ideas and unfortunately, rates of invention and innovation have slowed. The high point, according to Cowen, was the late 19th and early 20th centuries, which produced: modern chemicals and so artificial fertilizers; electricity and so the electric motor, light, refrigerator, vacuum cleaner, air conditioner, radio, phonograph and television; the internal combustion engine and so the automobile; the airplane; pharmaceuticals; and mass production. These are inventions that transformed lives and caused paradigm shifts.

Today, in contrast, argues Cowen, apart from the seemingly magical Internet, life in broad material terms isnt so different from what it was in 1953.

He concludes that politics is very difficult in an America without much low-hanging fruit. Also he says in explaining the financial crisis that we thought we were richer than we were. Americans have made demands, both collectively and individually, that they could not afford, borrowing too much and resisting both higher taxes and lower spending.

Let's begin the technical part with the analysis of currencies. We will start with the euro chart (charts courtesy by http://stockcharts.com.)

We begin with a look at the long-term Euro Index chart. We see that the index has moved lower past the level of the previous low and slightly below the 61.8% Fibonacci retracement level. The uncertainty in Europe is undoubtedly contributing to the lack of clear focus here.

However, the breakdown has not been verified yet. The index moved back above this support level and is now right at it. This means that the outlook is considerably less bearish than when it was below its final retracement level. If the index rallies and the breakdown is indeed invalidated, a significant move to the upside could very well follow.

At this time, it seems that the odds favor a rally in the Euro Index. The situation has improved in Europe and although it is still not good, it is better. The outlook for the euro therefore has improved, and the very negative publicity which has been handed out by the popular media outlets is no longer current.

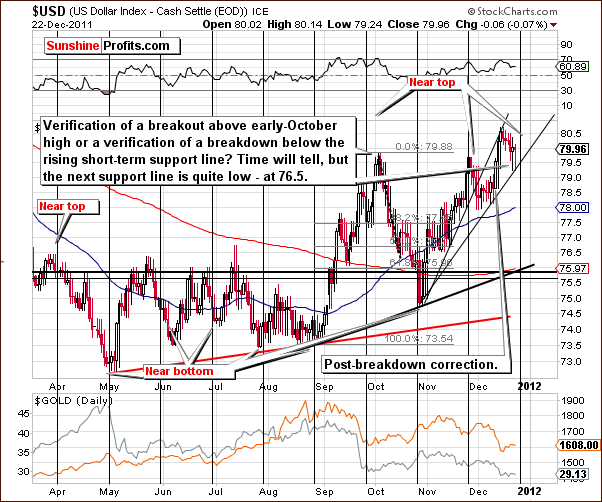

Concerning the very long-term USD Index chart, we would like to stress that the dollar has not truly broken above the declining long-term resistance line, and it has not moved above the 2011 high. Consequently, one should not be overly bullish on the USD Index just yet.

The short-term USD Index chart shows us that we are coming upon a cyclical turning point here. This suggests that perhaps a sharp decline is just around the corner. Two important points worth noting are seen in the chart. First the index is currently above the level of the October high but below the early 2011 high. Secondly, it is currently below a rising support line (the upper one) which it previously broke.

Since the index is currently between two important highs from the current year, the situation is quite mixed. The index is below the rising resistance line and the cyclical turning point is just around the corner, so the overall picture is somewhat bearish.

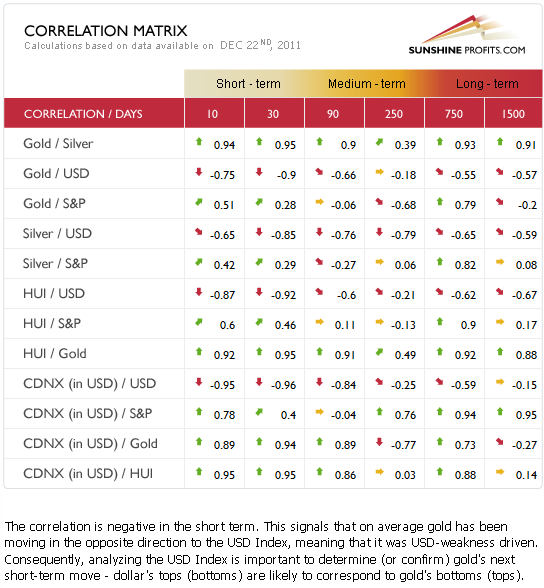

The Correlation Matrixis a tool which we have developed to analyze the influence in the coming weeks of the currency markets and the general stock market upon the precious metals sector. Gold is negatively correlated with the USD Index in the short and medium term. The coefficients are very low and thus significantly negative. With the outlook rather bearish for the dollar at this time and its correlation significantly negative with gold, the implications are somewhat bullish for gold and the entire precious metals sector.

This is consistent with our previous remarks on the developments for the yellow metal made in our essay on a possible move up in gold:

( ) although recent declines have been sharp, multiple signs suggest that the local bottom is in and higher gold prices are now expected. The precise target levels and their probabilities are a more delicate matter and require further consideration based on the full spectrum of our analysis.

Summing up, based on the situation in the currency markets, a move up in gold is currently more probable than not.

To make sure that you are notified once the new features are implemented, and get immediate access to my free thoughts on the market, including information not available publicly, we urge you to sign up for our free e-mail list. Sign up for our gold & silver mailing list today and you'll also get free, 7-day access to the Premium Sections on my website, including valuable tools and charts dedicated to serious PM Investors and Speculators. It's free and you may unsubscribe at any time.

Thank you for reading. Have a great weekend and profitable week!

P. Radomski

--

The full version of today's essay includes (in addition to the above): gold to bonds ratio, gold priced in currencies other than the US dollar, GDX:SPY ratio and the Gold Miners Bullish Percent Index. We cover both: major tendencies and short-term moves.

Additionally, we discuss if investors' perceptions have changed based on the fact that gold did not protect those who bought it as a hedge against euro problems and we comment on increased GLD inflows, their link to investors' sentiment and impact on future gold prices.

Moreover, we comment on 2 recent signals from our proprietary indicators. We encourage you to Subscribe to the Premium Service today and read the full version of this week's analysis right away.