This essay is based on the Premium Update posted on July 9th, 2010. Visit our archives for more silver articles.

You read a lot recently about "double dip" and it does not refer to two scoops of ice cream, or to the Jerry Seinfeld episode when George takes a large tortilla chip, dips it into a bowl of dip, bites into it and dips it into the bowl again, much to the utter disgust of the person standing next to him.

Yes, the financial meltdown has brought all kinds of new words into our lexicon.

The double dipping you have been reading about refers to recession -- a double-dip recession, with a W shape on the chart. It is a recession followed by a short-lived recovery, followed by another recession.

We are half way into the year and it is a good time to ask ourselves if we are in fact facing another "double-dip" recession? And if so, what are the implications for precious metals?

There is certainly enough fear and angst on the subject if you read the financial pages. The word "fear" led the front-page headlines of The Wall Street Journal at least twice last week.

The London Financial Times reported this week that optimism among finance directors of the UK's largest companies about their business's prospects has dropped to a 12-month low.

Some of the world's leading hedge fund managers are positioning their funds for a double dip recession, saying there has been a dramatic shift in the macro-economic environment over the last month.

Legendary investor George Soros recently told a banking conference in Vienna that the risk of a double-dip recession due to current European public finances woes can't be ruled out, as credit problems are forcing European countries to accelerate fiscal consolidation.

And then there is Robert Prechter of Elliot Wave International, who in a recent New York Times piece said we're headed for an even bigger crash than that of 2008 and 2009. He says the Dow could fall as low as 1,000 in the biggest bear market in 300 years. Here is his advice to investors:

I'm saying: ‘Winter is coming. Buy a coat.' Other people are advising people to stay naked. If I'm wrong, you're not hurt. If they're wrong, you're dead.

Double Dip of Dismal News

It is understandable when you consider that stocks registered their worst quarter since the financial meltdown in the fourth quarter of 2008. The economy is weak and this is after trillions of dollars have already been pumped into it. Hiring is weak, consumers have lost confidence, stimulus dollars are running out and debt is spreading across Europe. Commercial real estate is in trouble and no new buyers are coming into the housing market. Banks are still reluctant to lend and businesses are loath to expand. Automakers say they see no sign of recovery. Ten-year US Treasury notes are selling at the lowest yields in 14 months.

That's a lot of bad news to take it. But there's more.

Consider that Bush tax cuts are set to expire on January 1, 2011. Bush cut taxes in 2001 and again in 2003 in the face of a weak economy. Unless something changes, America is going to enact the largest tax increase in US history that will be matched by equally large tax increases and spending cuts by state and local jurisdictions. Unless Congress acts to make those cuts permanent, massive tax spikes will hit hard and could tip the U.S. back into recession. Research has shown that tax cuts or tax increases have as much as a 3-times multiplier effect on the economy. If you cut taxes by 1% of GDP then you get as much as a 3% boost in the economy. The reverse is also true.

Another New Term-"Option ARMs"

Here is another new term for us to learn-"Option ARMS." These are Adjustable Rate Mortgages and are considered one of the riskiest kinds of loans made during the housing boom; they have left many borrowers owing much more than their homes are worth.

ARMs generally permit borrowers to lower their initial down payments if they are willing to assume the risk of interest rate changes. Many ARMs have "teaser periods" when the ARM bears an interest rate substantially below the fully indexed rate.

Billions in Option ARM resets are scheduled to take place in 2010, which might make the subprime crisis look like a cakewalk. These are the loans that made it easy for consumers to buy houses they couldn't afford. About $750 billion-worth of Option ARMs were issued between 2004 and 2007 and they will all begin resetting shortly.

Does the government have the money to bail out the next batch of banks that will fail as a result of these Option ARMs? We should brace ourselves for more bank failures, job losses, foreclosures, delinquencies, and economic adversity.

To make matters even more unsettling, let's not forget that the world's governments met recently in Canada and pledged to reduce their countercyclical spending. If they follow through, it could result in the private sector and the public sector de-leveraging at the same time, which means another crisis. When governments begin to tighten at the same time that the private sector is tightening, the effect could push the world into a sharper, deeper recession. On the face of it, cutting back on spending seems like the prudent thing to do. But the move may not be enough to reduce sovereign debt levels, but still might have enough kick in it to tip several national economies into depression.

Having frittered away trillions in bailouts and confidence-building exercises, it will be nearly impossible for those same maneuvers to work again if the economy turns lower and defaults pick up again.

The likely scenario is that there will be wave of bankruptcies at first with inflation to follow.

Fascinating Crossroad in Modern Financial History

Albert D. Friedberg, of Friedberg Mercantile in Toronto, is one of the most respected hedge fund managers in Canada. In a private quarterly report he just sent to his investors Friedberg said: "In my view, we stand at a fascinating crossroad in modern financial history."

We would like to quote directly from his newsletter:

Massive quantitative easing for the past 18 months, at least in the U.S. and the U.K., has not led to an explosion of money as one would have expected. In effect, the money multiplies has shrunk dramatically; banks have build up record excess reserves and the asset side of their balance sheets has experienced a slight shrinkage, as loans have declined at a precipitous rate and Treasury holdings have only partially offset this decline. Clearly, banks are nervous about extending new credit...

If banks continue to hang on to their excess reserves, money supply will begin to drop in accelerated form and bring down with it asset prices and the economy. As it is, MZM (money of zero maturity, a proxy for transaction type money) has contracted at an annual rate of 6.9% over the past 13 weeks, while broader money (M2) has contracted at a 0.4% rate over the same span. The money contraction is puzzling in that they have occurred during a time when the Fed has made every conceivable effort to expand money to avoid the consequences of the 1930s. Recall that monetarists like Milton Friedman charged that the 30% contraction of money during the 30s was the principal cause of the depression. At the same time, fiscal profligacy in the U.S., Europe and Japan, is forcing the Treasuries of these countries to retrench in a massive way, implying rising taxes and a freeze on spending for years to come. The monetary drama in play at this time puts the continuation of the upswing in doubt.

The U.S. U.K., Eurozone and Japan are delicately poised between two very serious dangers; a once in a generation deflation and an accelerating inflation rate. Either a lack of oxygen or too much of it will kill the patient. The deflationary, the more likely scenario, would be deadly almost right way. The inflationary scenario on the other hand, on the other hand, would take a huge toll on the developed economies, but it would be likely to take some time.

Friedberg, a prudent investor, says he placed a modest amount of chips on the deflation table and fair sized short positions in stock indices. A gold bull, he also placed a "fair sized" long position in gold, which he says is becoming a safer international asset by the day.

We obviously agree that going long the gold market is the right move for investors to prepare themselves for the coming storm. Remember that the first goal always is not to lose money while waiting for the next opportunity train to leave the station. Gold is the ultimate money. We wrote in last week's Premium Update that there is only one reason not to invest in gold. You should not invest in gold or silver if you believe that Somewhere Over the Rainbow skies are blue, sovereign debt problems will disappear and economic recovery is just around the corner.

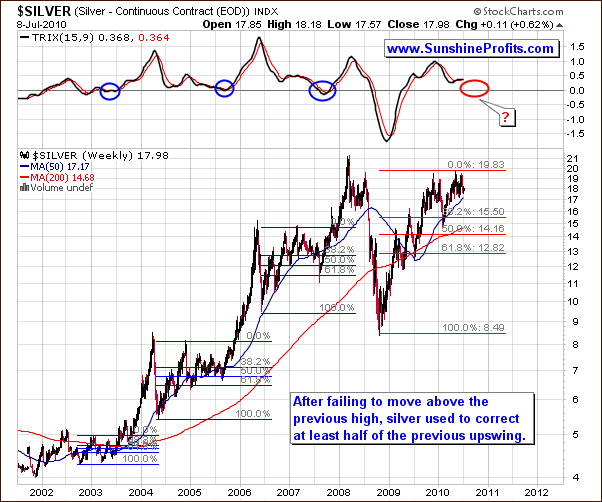

This week, however, we will turn to silver as this market provides us with particularly interesting long-term calls. Consequently, let's begin with the very-long-term chart (charts courtesy by http://stockcharts.com.)

The above chart has been featured in our updates several months ago when we discussed long-term targets for silver and gold.

Just like it was the case back then, it seems that silver prices would need to correct previous upswing twice before moving to new highs. Please note that once a new high is reached after a rally, there is a typical correction and then a move close to the previous high that does not take silver higher. It seems that this is what we have just seen.

Once this second trial fails, price corrects once again - at least 50% of the preceding upswing (as marked on the chart above) before moving much higher.

This means that if we have seen the second top for silver now (which is likely the case) then silver might need to move down to $14 - $15 level before it ignites a rally that takes it to new highs.

We realize that this is very discouraging news to silver and gold investors but it is our obligation to report what our analysis determines. Gold and mining stocks may also go substantially lower but confirmation from other techniques or signals is needed before validating this option as highly probable.

The upper section in this first chart for silver provides conclusive calls long-term. The Trix indicator normally does not imply a final bottom until a downward move has been followed by a correction and then an addition decline. This would be near the zero level for the Trix indicator. Above we see that we are beginning the second part of a corrective phase. This precedes our next rally and we expect to see a zero eventually. This would correspond to a final bottom possibly along with a possible decline to the $14 - $15 level.

This discussion has not been provided to scare you out of the precious metal sector. We do wish however to emphasize that the situation is quite serious. It is most important now to monitor all developments daily and react accordingly. Sunshine Profits has the tools and the expertise to keep our Subscribers informed. This is always our first priority.

The above chart indicates that we might be close to a local bottom, as the price of silver is right at the 200-day moving average. The Stochastic Indicator points towards the bottom possibly being in. The RSI however does not confirm this. So what does all this mean? The signals are presently mixed and unclear and we do not feel this benefits entering with speculative capital at this time.

This final chart for silver points to the bottom being in and a technical turning point also at hand. The Stochastic Indicator also identifies the bottom and a probable move upwards to follow.

Summing up, even though precious metals will likely move upwards slightly in the coming days, this may be the beginning of a bigger downswing in silver, gold and mining stocks. We caution that these moves higher may only be temporary (particular caution is necessary if one wishes to trade this move), as they are driven to a great extent by possibility of a consolidation in the Euro Index. Please note that this is not the end of the bull market for silver; in fact. In this week's Premium Update we provide a target for silver at the end of 2011, which is much higher than the 2008 high.

To make sure that you are notified once the new features are implemented, and get immediate access to my free thoughts on the market, including information not available publicly, I urge you to sign up for my free e-mail list. Sign up today and you'll also get free, 7-day access to the Premium Sections on my website, including valuable tools and charts dedicated to serious PM Investors and Speculators. It's free and you may unsubscribe at any time.

Thank you for reading. Have a great weekend and profitable week!

P. Radomski

--

This week's Premium Update is dedicated to both short- and long-term implications of the recent move lower in gold, silver, and mining stocks. The analysis of two very-long-term silver charts provides us with details regarding next major bottom and top in the white metal, and we speculate on where gold could bottom at the end of this decline. Additionally, we explain what signals we are particularly looking for to determine if the next major move in the precious metals is going to be down.

We analyze the Euro Index, USD Index, the general stock market, the correlations between these two markets and the precious metals market, gold, silver, HUI Index, and GDX ETF. We also comment on the very recent signal from one of our unique indicators, and provide trading thoughts for experienced Traders. We encourage you to Subscribe to the Premium Service today and read the full version of this week's analysis right away.