The U.S. yield curve has inverted again, and it has done so to the widest level since 2007. How much of a reason to worry is that actually? A sky-is-falling moment lurking ahead? If so, what chance of saving us does gold have?

Another Yield Curve Inversion Occurs

It's really getting more serious. Another yield curve inversion... And a much deeper one - that's frightening!

As you probably remember, the yield curve inverted for the first time in the post-crisis era in March 2019. The inversion was mild and short-lived. And it occurred after the Fed sent a dovish signal, not a hawkish one, as it announced a longer pause in further tightening of monetary policy and the end of shrinking its balance sheet as early as this September.

Hence, we concluded in the Gold News Monitor (here and here) that the March inversion did not fit the classical story when the Fed raises the short-term interest rates to combat inflation, so it did not signal the upcoming recession, especially that the unemployment rate (and other indicators, as well) did not confirm the warning. We were right, the sky did not fall, and the gold prices did not start to rally.

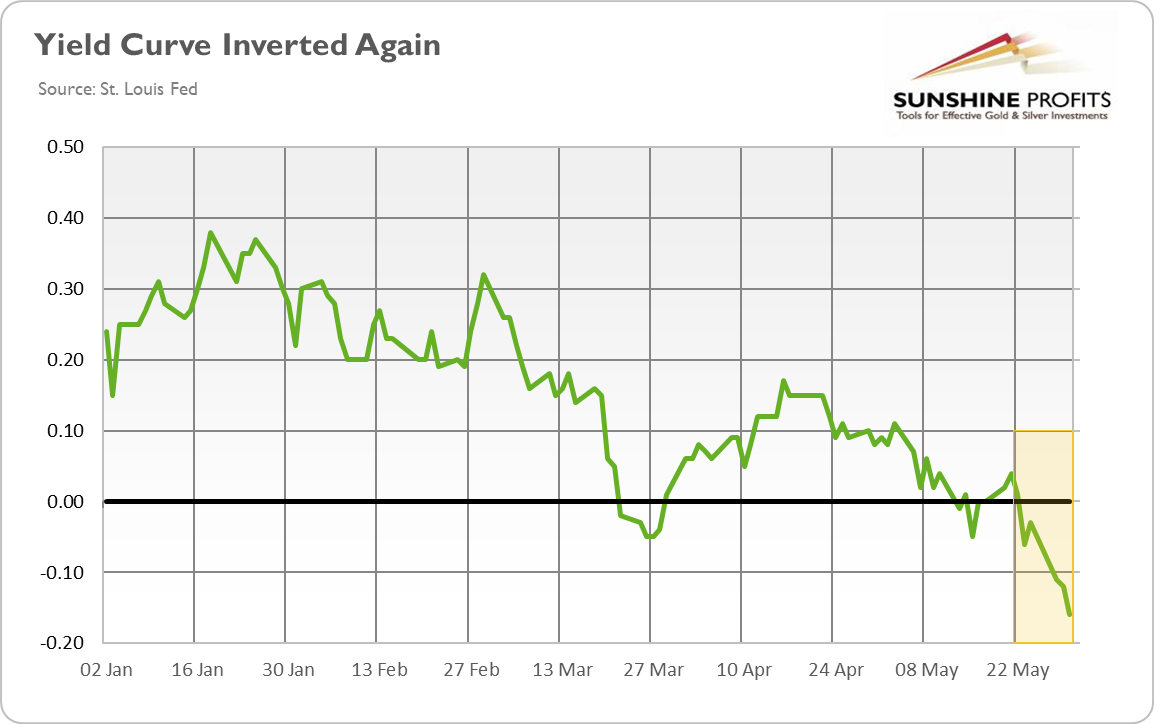

But maybe we will have to change our minds. You can blame the chart below, which is really worrisome. It shows the difference between 10-year and 3-month Treasuries. Just take a look!

Chart 1: Spread between 10-Year Treasuries and 3-Month Treasuries from January 2019 to May 2019.

As one can see, after short inversion in March, the yield curve returned to the positive zone and stayed there for the whole April. However, in the mid-May, the yield curve found itself again in the negative territory. On May 13, the spread fell to -0.01, but the inversion ended the next day. On May 15, however, the yield curve inverted again, to -0.05, but it terminated the next day. But since May 23, the yield curve has been inverted once more. And this time, the inversion is much deeper, as the spread dropped to -0.16.

So, this is the fourth inversion since March, which indicates that the negative spreads might be not so short-lived after all. And not so mild either. Previously, the spreads did not fall below -0.05, while the current difference plunged below -0.15. Hence, the situation might be more serious than we previously though, despite the fact that economic data seems to be solid overall as other recession warning signs simply are not there.

Indeed, the alarm bells are ringing louder not only in the US bond market, but around the world. Germany's 10-year rates plunged to a new record low well below zero. The UK yield curve is around its flattest level since the Great Recession, while Canada's yield curve has already reached 2007's level of inversion.

Implications for Gold

The bottom line is that the yield curve has inverted again. It should add to the fears of recession, which be a tailwind for the yellow metal in the near future. Indeed, as the chart below shows, the gold prices rose on Monday to their highest in more than two months. It seems that worries about a global recession - fueled partially by the trade wars - pushed investors into the safe-haven assets such as gold.

Chart 2: Gold prices from May 31 to June 3, 2019.

Should we press the panic button? On the one hand, an inverted yield curve has preceded every U.S. recession since WWII, so we should not assume that this time will be different. On the other hand, the quantitative easing and other central banks' interventions in the bond markets could really diminish somewhat the predictive power of the yield curve. Other recession indicators (including differently measured yield curves) do not blink red, at least not yet. And the inversion is caused by the 10-year yield falling rather than the 3-month yield rising.

So we do not send a Red Alert yet. We will examine thoroughly the newest inversion of the yield curve in the next edition of the Market Overview and let you know our verdict on the issue! As for now, the precious metals investors should become more cautious, that's for sure (but they should not panic!). If the yield curve is still an indicator to be trusted in our age of expanded monetary policy toolbox, we are likely about four - six quarters from the US recession. If we are on that gloomy path, that helps explain gold's increasing appeal. The important word here is - if...

If you enjoyed the above analysis, we invite you to check out our other services. We provide detailed fundamental analyses of the gold market in our monthly Market Overview reports and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. If you're not ready to subscribe yet and are not on our gold mailing list yet, we urge you to sign up. It's free and if you don't like it, you can easily unsubscribe. Sign up today!

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts.

Thank you.

Arkadiusz Sieron

Sunshine Profits' Gold News Monitor and Market Overview Editor