-

Gold Can’t Rise on Weak Payrolls

October 12, 2021, 9:26 AMThe US economy added only 194,000 jobs in September, falling short of expectations, but the Fed can still taper soon — and gold knows it.

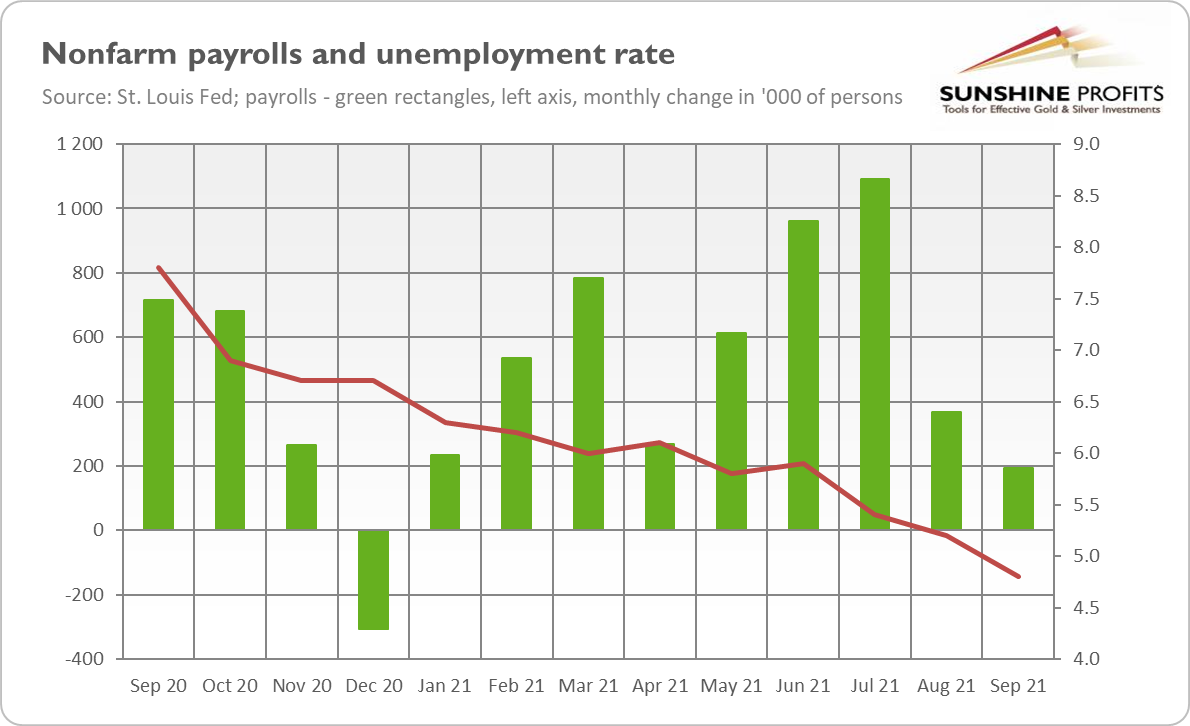

Another disappointment from the economy! The September nonfarm payrolls came surprisingly weak. As the chart below shows, the US labor market added only 194,000 jobs last month, much below the expectations (analysts forecasted about half a million added jobs). The disappointing numbers followed the additions of 1,091,000 in July and 366,000 in August (after an upward revision). The most recent job gains were the weakest since December 2020.

However, the overall report was generally more positive than the headline. First of all, the unemployment rate declined from 5.2% to 4.8%, as the chart above shows. It’s a positive surprise, as economists expected a drop to only 5.1%. In absolute terms, the number of unemployed people fell by 710,000 - to 7.7 million. It’s a considerably lower level compared to the recessionary peak, but still significantly higher than before the pandemic (5.7 million and unemployment rate of 3.5%).

Second, taking revisions into account, the employment in July and August combined is 169,000 higher than previously reported. It means that the monthly job growth has averaged 561,000 so far this year and about 550,000 over the last three months.

Third, the main reason for the very weak nonfarm payrolls was a decline in local and state government education - by 161,000. Most back-to-school-hiring typically occurs in September, but the recruitment last month was lower than usual, which some analysts attribute to early retirement of some teachers, mask-wearing mandates and vaccination requirements. Another issue is that the report is based on data that was collected when the Delta variant of the coronavirus was reaching its peak, and now the situation looks better.

Implications for Gold

What does the recent employment report imply for the Fed’s monetary policy and the gold market? Well, Fed Chair Jerome Powell told reporters during his press conference in September that he would like to see a “reasonably good” or “decent” employment report before deciding that the Fed’s threshold for reducing its asset purchasing program has been met.

So, you know, for me, it wouldn’t take a knockout, great, super strong employment report. It would take a reasonably good employment report for me to feel like that test is met. And others on the Committee, many on the Committee feel that the test is already met. Others want to see more progress. And, you know, we’ll work it out as we go. But I would say that, in my own thinking, the test is all but met. So I don’t personally need to see a very strong employment report, but I’d like it see a decent employment report.

Now, the question is whether 194,000 job gains are decent enough to taper the quantitative easing. Interpreting words of an oracle is never an easy task. The September payrolls are neither strong nor a catastrophe. However, given the level of expectations and the fact that job gains were weaker than in August (commonly considered a great disappointment) I wouldn’t describe the latest payrolls as “decent”.

However, we have to remember that the overall report was much better than the payrolls analyzed in isolation. Given the significant decline in the unemployment rate, the September employment report can be defended as “decent”. So, the Fed can still taper in November, or announce it at least, especially that some members of the FOMC were ready to tighten US monetary policy already in September.

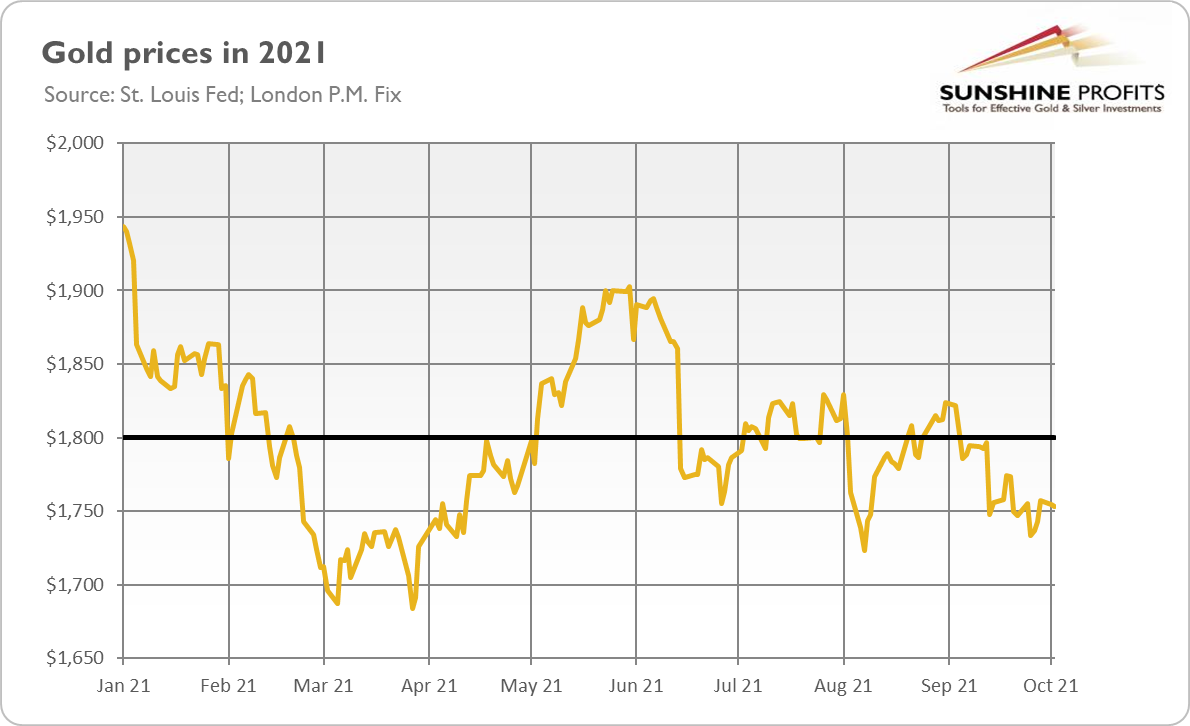

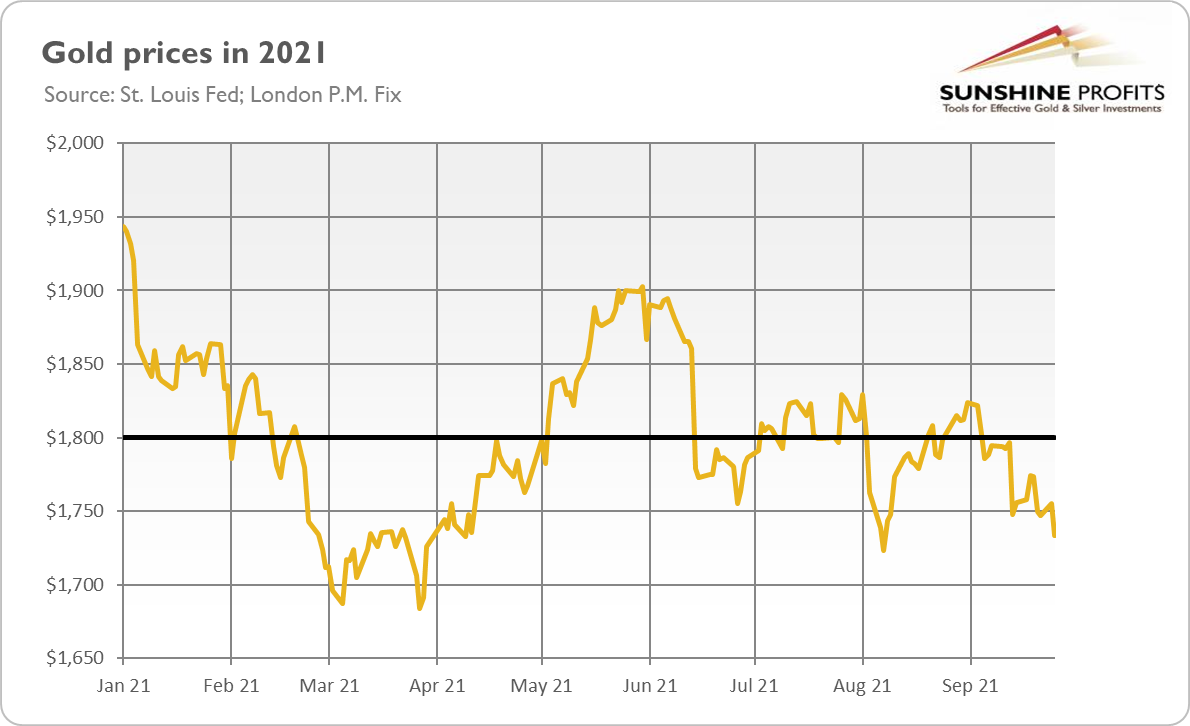

It seems that my line of thinking is in line with the market’s interpretation of the Fed’s likely course of action. The price of gold jumped briefly on Friday above $1,780, but it could not break the resistance or hold this position and returned quickly to its recent comfort zone of $1,750-1,760. The rather shy reaction of the yellow metal can be seen on the chart below.

Gold’s inability to shine in response to the second weak nonfarm payrolls in a row or to the inflation worries is quite disappointing. Well, Mr. Market decided that the September employment report wouldn’t restrain the Fed from tapering. The focus on the upcoming tightening cycle creates downward pressure on gold prices, which counterweighs worries about the labor market or inflation.

However, it might be the case that the price of the yellow metal will bottom somewhere around the actual start of tapering, and, without all that pressure around the tapering announcement, it could be free to move upward again.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Inflation Finally Meets Wall Street’s Ears! Is Gold Next?

October 7, 2021, 9:13 AMAt last, something is happening! Rising oil and gas prices sparked inflation worries among investors. However, gold hasn’t benefited so far…

It took Wall Street a while to find out about inflation above 5%, but it seems that investors have finally noticed that we live now in a world of elevated inflation. I have always known that only the smartest minds work on Wall Street! So, right after they finally learned how to operate a computer and found the BLS website, they got scared and started selling equities. As a consequence, the U.S. stock index futures declined yesterday morning.

All right, I was a bit mean to the Wall Street traders. They panicked not because of the CPI rates but because of soaring oil prices. As the chart below shows, the WTI crude oil has recently approached $80 per barrel, while the price of natural gas has more than doubled in recent weeks (left axis). A propos, if you want to know more about oil, gas and the energy sector, as well as keep track of all price moves happening there (and possibly profit from them!), I can recommend a great place to do so - Oil Trading Alerts.

The rising oil prices triggered inflation worries, as higher energy prices could translate into higher consumer inflation, and higher consumer inflation could trigger a more hawkish Fed’s action than previously anticipated. In particular, the US central bank could taper its quantitative easing faster than expected, especially if September nonfarm payrolls turn out to be decent. After all, good news is right now bad news for stocks, not to mention gold.

I’ve been warning for a long time now that inflation could be more lasting than the pundits claim. And here we are, the high inflation readings couldn’t be downplayed any longer, so the IMF admitted yesterday in its flagship report World Economic Outlook that elevated inflation could last by mid-2022:

Headline inflation is projected to peak in the final months of 2021, with inflation expected back to pre-pandemic levels by mid-2022 for both advanced economies and emerging markets country groups, and with risks tilted to the upside.

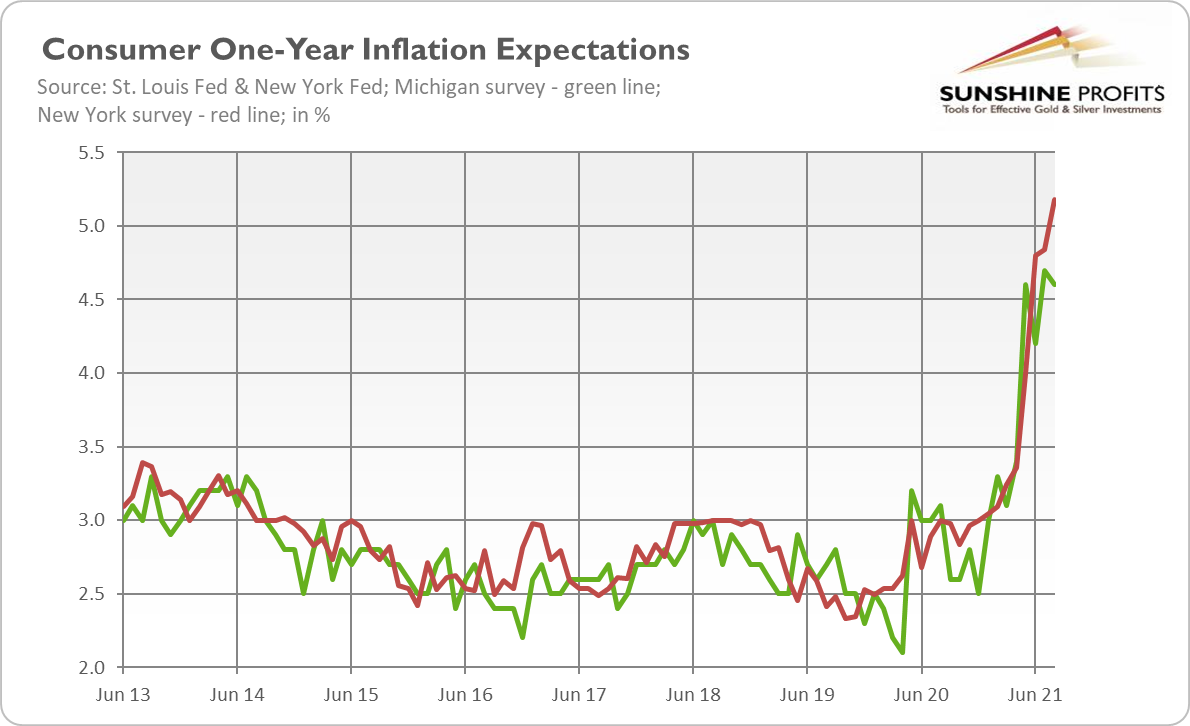

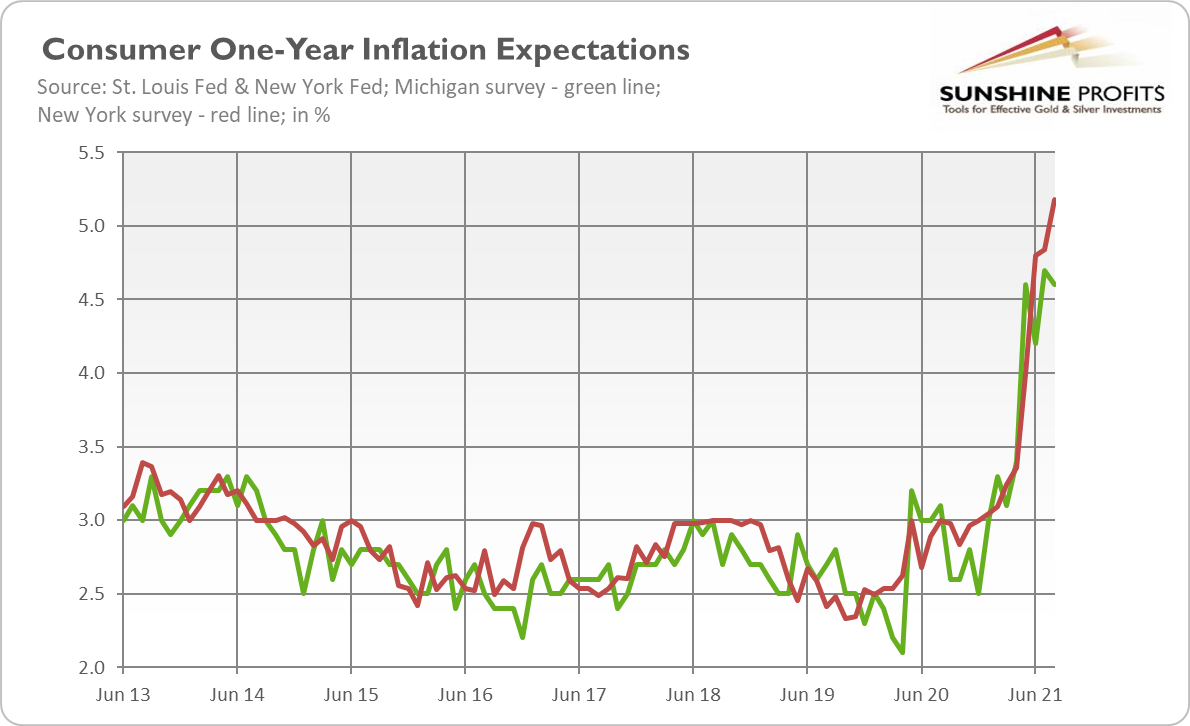

However, the baseline scenario assumes that inflation expectations remain anchored. And although the IMF is right that market-based measures of long-term inflation expectations have stayed relatively anchored so far, the measures based on surveys of consumers have clearly de-anchored recently, as the chart below shows.

I don’t know on which planet IMF economists live, but in my world such a graph shows anything but well-anchored inflation expectations. So, I would say that upside risks to the IMF’s baseline scenario are more probable than the authors are willing to admit. In fact, even they acknowledge that risks remain tilted slightly to the upside over the medium term:

Sharply rising housing prices and prolonged input supply shortages in both advanced economies and emerging market and developing economies, and continued food price pressures and currency depreciations in the latter group could keep inflation elevated for longer.

Implications for Gold

What does it all imply for the gold market? Well, as usual, I’m obliged to say that, theoretically, higher inflation should be positive for gold, which is considered to be an inflation hedge. However, theoretical links, which we can analyze in isolation, in reality work together with other forces, as economy is a complex system. In our case, gold is not getting much benefit from strengthening inflation worries as bond yields are rising in tandem, supporting the real interest rates. Gold’s disappointing performance in the inflationary environment (see the chart below) is also caused by the prospects of the Fed’s tightening cycle.

So, it seems that gold could remain in the downward trend in the near future, especially if the Employment Situation Report, which is scheduled to be released on Friday, doesn’t disappoint. However, the Fed will have to reverse its course at some point –they will not hesitate whether they should fight with the overheating or stimulate the economy during a crisis. And this will allow gold to shine again.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Will Q4 2021 Be Better for Gold?

October 5, 2021, 10:24 AMThe third quarter of 2021 was bad for gold, with a particularly awful September. Could the remainder of the year be any better for the yellow metal?

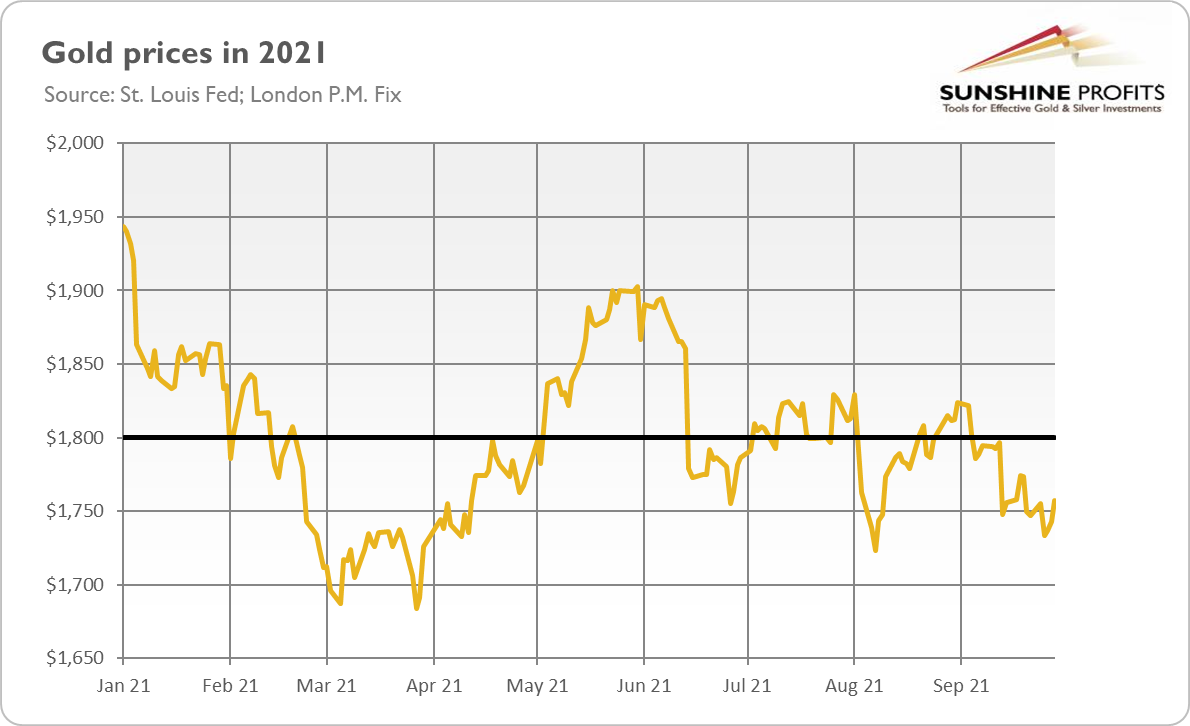

September is believed to be, from the historical point of view, one of the best months for gold. Well, September 2021 definitely wasn’t very good for the yellow metal. As the chart below shows, the price of gold declined almost 4% in that month (from $1,814.85 at the end of August to $1,742.80 at the end of September).

Actually, the whole third quarter was rather disappointing for the yellow metal, which lost 1.15% over the last three months. However, it was still much better than the disastrous first quarter of the year in which gold plunged more than 10%. So far, the yellow metal is 7.67% down year-to-date.

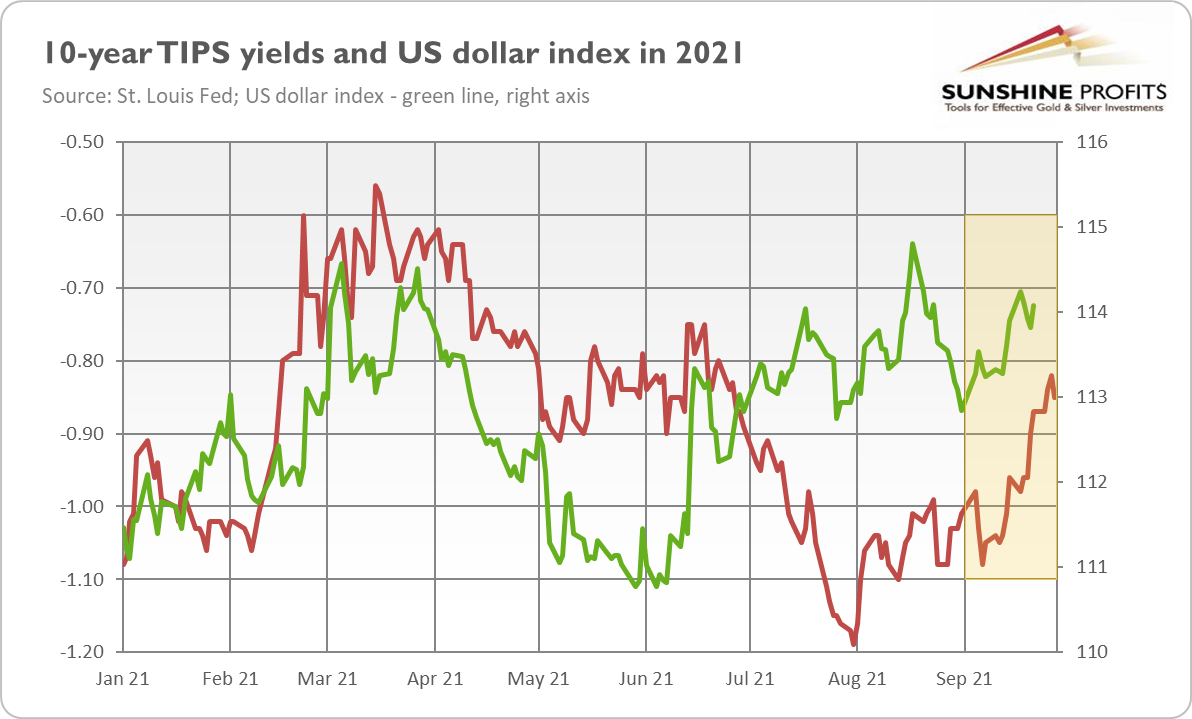

But why did gold perform so poorly last month despite elevated inflation and all the risks present to the US economy? Long story short, rising bond yields and the stronger greenback were the main headwinds for gold in September and, more generally, in the whole Q3 2021, as one can see in the chart below.

In the first half of the year, the US dollar performed rather poorly, but a more hawkish Fed helped to revive the greenback and push interest rates higher. In such an environment, any safe-haven bets – amid the uncertainty about the debt ceiling, debt problems in China, etc. – were channeled into the US dollar alone. In other words, because of the expectations of the Fed’s tapering, the recent risk-off sentiment has benefited only the greenback, not gold. So, gold’s appeal as a safe-haven asset has diminished recently. The same applies, actually, to gold’s status as an inflation hedge.

To be clear, the whole issue is more nuanced. I believe that gold still has anti-inflationary features, especially when inflation is very high and accelerating. I also think that gold will retain its purchasing power over the long run. It might simply be the case that rising interest rates counterweighed the reasons for investing in gold during inflation, especially given that it seems that the Fed convinced the markets that inflation would only be temporary.

However, if inflation turns out to be more persistent, the Fed could find itself behind the curve, while the real interest rates could stay at very low levels. In such a scenario, the demand for gold as a hedge against inflation could rise again. As a reminder, there are many arguments for high inflation staying with us for longer. Even Powell admitted last week that inflationary pressure would run into next year:

It’s also frustrating to see the bottlenecks and supply chain problems not getting better — in fact at the margins apparently getting a little bit worse (…) We see that continuing into next year probably, and holding up inflation longer than we had thought.

Implications for Gold

What does it all imply for the gold market? Well, the recent jump in gold prices is quite welcoming. However, it doesn’t change gold’s bearish outlook for the fourth quarter of 2021. Gold has been unable to surpass $1,800, and it looks like it wants to keep falling. In particular, any new hawkish comments from the Fed could push gold prices down even further.

Having said that, I’m more optimistic about gold in 2022. One reason is that, over time, the narrative about transitory inflation will look less and less convincing. Meanwhile, the odds of some inflationary crisis, or stagflation, should be higher and higher.

Second, the Fed’s tightening cycle seems to already be priced in to a large extent. So, the actual moves could start supporting gold at some point, in line with the logic of “sell the rumor, buy the fact”, especially if the moves are accompanied by dovish rhetoric, as it was partially the case during the last tightening cycle of 2015-2019.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

We’re Close to Hitting the Debt Ceiling: Gold Doesn’t Care

September 30, 2021, 9:42 AMAnother fiscal year, another governmental fight to raise the debt limit. A failure spells a crisis, but gold turns a blind eye and continues its fall.

So, America has a new tradition! The government shutdown is coming. A new fiscal year starts tomorrow, and if Congress fails to agree on a budget by the end of today, the government will shut down.

What does it mean for the US economy? According to Treasury Secretary Janet Yellen, the failure to lift the debt ceiling could be a catastrophe:

If the debt ceiling is not raised, there would be a financial crisis, a calamity. It would undermine confidence in the dollar as a reserve currency (…) It would be a wound of enormous proportions (…) It is imperative that Congress swiftly addresses the debt limit. If it does not, America would default for the first time in history. The full faith and credit of the United States would be impaired, and our country would likely face a financial crisis and economic recession.

She also clarified in a separate letter sent to Congress that the Treasury could run out of money by October 18, 2021:

We now estimate that Treasury is likely to exhaust its extraordinary measures if Congress has not acted to raise or suspend the debt limit by October 18. At that point, we expect Treasury would be left with very limited resources that would be depleted quickly. It is uncertain whether we could continue to meet all the nation’s commitments after that date.

Her rhetoric was rather gloomy. As a result, the risk aversion softened, while stock prices dropped. So, gold prices had to increase, right? Well, not exactly. As the chart below shows, the price of the yellow metal continued its downward trend that accelerated in September, partially caused by more hawkish expectations for the tapering timeline and future path of the federal funds rate.

So, what is happening in the gold market? I would point out three crucial factors right now. First, the US dollar has appreciated recently. Yes, despite worries about the debt ceiling, the greenback has strengthened. It shows that there is simply no alternative. Another issue is that people have seen this movie before, and they know how it ends. At some point, Congress will pass a new debt limit and return to its spending spree.

Second, the bond yields have increased. For example, the nominal yields on 10-year Treasuries jumped from about 1.3% last week to almost 1.5% on Monday (September 27, 2021), as the chart below shows. The recent dot-plot revealed that the FOMC members want to raise the federal funds rate earlier than previously thought, which has been transmitted into the yield curve, creating downward pressure on gold. Higher interest rates imply higher opportunity costs of holding bullion.

Third, the market sentiment still seems to be negative toward gold. It’s partially justified by the macroeconomic environment — namely, the rapid recovery from the pandemic recession. As the global economy is improving, the central banks are about to tighten their monetary policy.

Implications for Gold

What does it all imply for the gold market? Well, the environment of strengthening dollar and rising bond yields is negative for the yellow metal. Higher interests make bonds more attractive relative to gold. The worries about the debt ceiling will likely be short-lived and won’t provide gold with a needed lifeline. The current downward trend in gold shows that the market simply doesn’t care about the government shutdown. The only hope is an inflationary crisis, but (so far) worries about inflation have been entailing higher interest rates rather than strong demand for gold as an inflation hedge.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Gold Could See Tapering as Soon as November!

September 28, 2021, 9:01 AMIt’s Powell’s doing, as always... the Chair signaled that tapering could be announced as soon as next month. What does this mean for gold bulls?

In the latest edition of the Fundamental Gold Report, I covered the FOMC’s newest statement on monetary policy and the dot-plot. I concluded that “gold will struggle until the Fed’s tightening cycle is well underway”. As the chart below shows, the yellow metal has been struggling for the most part of this year, and I don’t expect any shifts from that trend anytime soon.

Now, it’s high time to analyze Powell’s press conference! In his prepared remarks, the Fed Chair offered a rather upbeat view on the US economy:

Real GDP rose at a robust 6.4% pace in the first half of the year, and growth is widely expected to continue at a strong pace in the second half (…) Looking ahead, FOMC participants project the labor market to continue to improve.

Powell also downplayed the inflationary risk. He acknowledged that inflation has stayed at a high level for longer than the Fed expected, but, at the same time, he reiterated the Fed’s view of the transitory nature of elevated inflation:

These bottleneck effects have been larger and longer-lasting than anticipated, leading to upward revisions to participants’ inflation projections for this year. While these supply effects are prominent for now, they will abate, and as they do, inflation is expected to drop back toward our longer-run goal.

However, the question is: why should we trust the Fed’s current inflation outlook, given that its previous forecasts were clearly wrong and underestimated greatly the real persistence of inflation?

Last but not least, Powell offered more clues about tapering of quantitative easing. Although no decision has yet been made, “participants generally view that, so long as the recovery remains on track, a gradual tapering process that concludes around the middle of next year is likely to be appropriate”. So, my conclusions would be: given that tapering is said to be very gradual, it’s likely that it will start sooner rather than later.

Powell and Gold

Indeed, the Q&A session suggests that the Fed could announce tapering as soon as November. It all depends on whether the substantial further progress test for employment will be met or not. For Powell it is now “all but met”, even though it could happen as soon as the next meeting. After all, many of the FOMC members believe that this test has already been met:

So if you look at a good number of indicators, you will see that, since last December when we articulated the test and the readings today, in many cases more than half of the distance, for example, between the unemployment rate in December of 2020 and typical estimates of the natural rate, 50 or 60 percent of that road has been traveled. So that could be substantial further progress. Many on the Committee feel that the substantial further progress test for employment has been met. Others feel that it's close, but they want to see a little more progress. There's a range of perspectives. I guess my own view would be that the test, the substantial further progress test for employment is all but met. And so once we've met those two tests, once the Committee decides that they've met, and that could come as soon as the next meeting, that's the purpose of that language is to put notice out there that could come as soon as the next meeting. The Committee will consider that test, and we'll also look at the broader environment at that time and make a decision whether to taper.

It seems as though the only condition to be yet fulfilled is that the September employment report has to be “decent”. It doesn’t have to be fantastic, but it can’t be a disaster. Powell says:

So, you know, for me, it wouldn't take a knockout, great, super strong employment report. It would take a reasonably good employment report for me to feel like that test is met. And others on the Committee, many on the Committee feel that the test is already met. Others want to see more progress. And, you know, we’ll work it out as we go. But I would say that, in my own thinking, the test is all but met. So I don’t personally need to see a very strong employment report, but I’d like it see a decent employment report.

Implications for Gold

What does Powell’s press conference imply for the gold market? Well, the Fed Chair sounded generally hawkish. He was rather optimistic about the GDP growth and progress in the labor market. Powell also downplayed risks related to Evergrande’s indebtedness.

And, most importantly, he signaled that tapering could be announced as soon as November, as many FOMC members believe that the substantial progress towards the Fed’s goal has been already achieved. This is bad news for gold prices.

There is, however, a silver lining. There will be no interest rate hikes while the Fed is tapering. So, the real interest rates should stay at ultra-low levels, providing some support for the yellow metal.

Having said that, the dot-plot shows that half of FOMC members forecast the first interest rate hike by the end of next year. As a consequence, the market odds for the liftoff in December 2022 increased from 52.9% on September 16 to 72.7% on September 23, 2021. If the federal funds rate goes the hawkish way, it should continue to create downward pressure on gold prices.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

Gold Reports

Free Limited Version

Sign up to our daily gold mailing list and get bonus

7 days of premium Gold Alerts!

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM