The latest WGC reports show that institutional allocation to gold will increase. What if there is more to it than just “higher demand, higher price”?

In July the WGC published three interesting reports. The first one, Rethink, Rebalance, Reset: Institutional Portfolio Strategies for the Post-Pandemic Period, is an interesting survey of 500 institutional investors around the world ran by Greenwich Associates between October 2020 and January 2021. The study investigated investors about portfolios, allocations and views on various markets, gold, and other individual asset classes.

The main result of the survey is that institutional allocations to gold are expected to increase over the next three years. To be more specific, the study finds that, currently, only 20% of institutions have an allocation to gold in their portfolios, which amounts to 4% of their portfolios, on average. However:

Almost 40% of current gold investors expect to increase their allocations in the next three years, and about 40% of institutional investors who do not have gold exposure but have a target or have considered it, plan to make an investment in that time frame.

The growing allocation to gold partially reflects rising concern about inflation and a search for inflation-protection assets. According to the WGC, gold performs well in periods of high inflation: in the years when the US CPI annual rates were higher than 3%, gold prices rose 15%, on average. My own research shows that gold doesn’t protect against low inflation readings; it hedges only against high and accelerating inflation.

However, the study suggests that institutional investors have a broader view of gold than just as an inflation hedge. Actually, portfolio diversification tops inflation-hedging as the major role gold plays in the portfolios. After all, market downturns often boost demand for gold, as the yellow metal has a negative correlation to risk assets, which often increases when these assets sell off. Also, institutions use gold for long-term risk-adjusted return enhancement, especially in the environment of negative interest rates.

Importantly, gold may be useful not only for commercial financial institutions but also for the central banks. The second recent WGC report, Monetary gold and central bank capital, discusses the vulnerabilities specific to central bank balance sheets and discusses how gold holdings can mitigate the risks posed. The publication points out that gold provides central banks with extra protection, as it mitigates the risk of asset losses. In particular, gold offsets gains and losses in the US dollar held as a reserve by central banks all around the world:

Gold can play a role as a counter-cyclical hedge to USD exposure because, as the dollar weakens, gold strengthens. Hence, revaluation gains on a central bank’s gold portfolio should offset losses suffered on its USD portfolio and help to maintain its core equity.

The last report is Gold mid-year outlook 2021: Creating opportunities from risks. The main thesis is that the negative impact of higher bond yields would likely be offset by inflation and stronger demand for gold as a portfolio-diversification in an environment of ultra-low real interest rates and strong risk-taking.

The WGC’s thesis corresponds with my observation that gold is at a crossroads of a more hawkish Fed and higher inflation (I will elaborate on this in the upcoming edition of the Gold Market Overview). The report rightly states that gold’s performance in H1 2021 was driven primarily by higher interest rates, which could continue to create headwinds for the yellow metal in the second half of the year.

However, the WGC believes that the Fed will be cautious with its tightening cycle. Although that may be true, gold is likely to struggle during the period of strengthening expectations of quantitative tightening and rising interest rates.

Implications for Gold

What can we learn from the recent WGC reports? Well, I believe that the most important information is that the institutional allocation to gold is going to increase in the upcoming years. Given that investment demand for gold is the most important driver of its price, this is positive news for gold bulls.

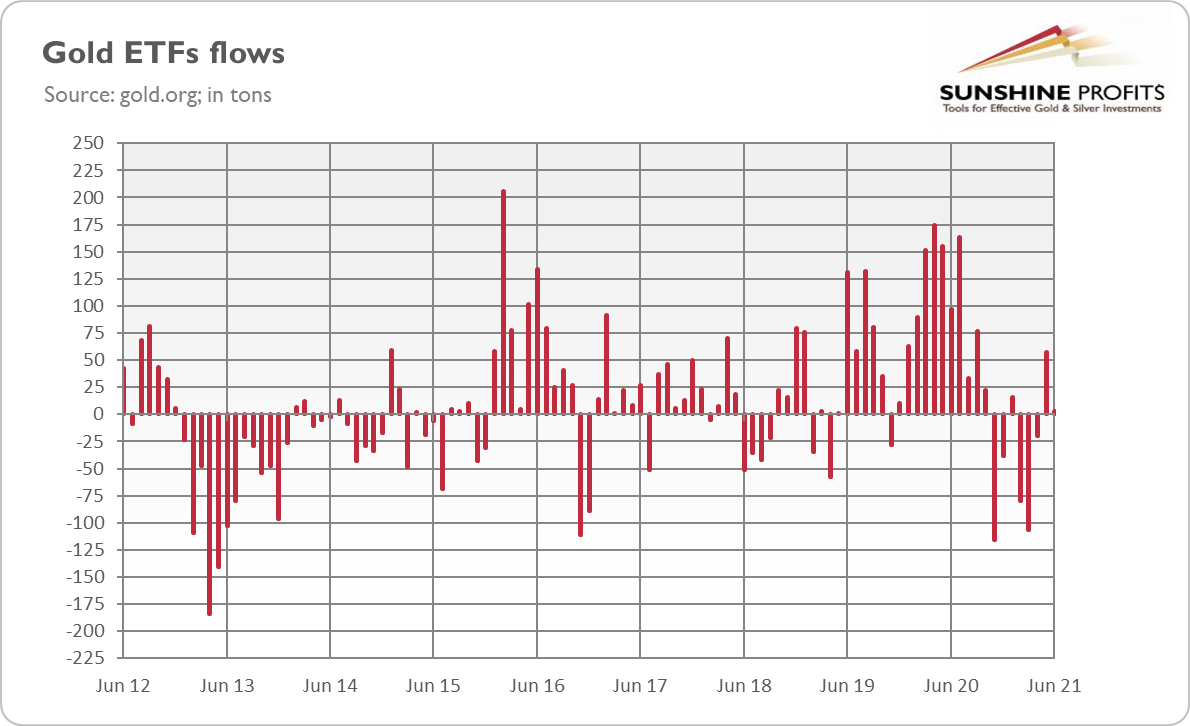

The survey results should always be taken with a pinch of salt, but the recent ETF flows confirm that there is still significant interest in gold. In June, the inflows to gold ETFs slowed down, as the chart below shows, but remained positive (+2.9 tons) despite the plunge in gold prices.

According to the WGC, this adjustment suggests that “investors may have taken advantage of the lower price level to gain long gold exposure”. In other words, gold could decline even more, but inflation concerns provided some support. What’s important, the recent dynamics of the ETFs flows don’t look as bad as in 2013 (at least not yet) when gold definitely sank into the bear market. So, although ETFs flows don’t necessarily drive the gold prices, there is a hope that the upcoming Fed’s tightening cycle will be less harmful to gold than the infamous 2013 taper tantrum.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.

-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.