Some analysts has argued that the manufacturing sector reached a through. But this not the case. The latest Fed's report on the industrial production and capacity utilization clearly shows that the pundits were wrong again. As they so often are. The industrial production fell 0.8 percent in October, much more than expected. It was the third drop in the industrial production in the past four months, following a 0.3-percent decrease in September, and the largest decline since May 2018.

Of course, the United Auto Workers strike at General Motors negatively affected the October report, pushing down automotive production by 7.1 percent. However, the weakness was not limited to the car industry. Excluding motor vehicles and parts, the index for total industrial production moved down 0.5 percent. The decline was broad-based: the index for manufacturing edged down 0.1 percent, mining production decreased 0.7 percent, while utilities output fell 2.6 percent. And the capacity utilization for the industrial sector decreased by 0.8 percentage point in October to 76.7 percent, the lowest level in 25 months.

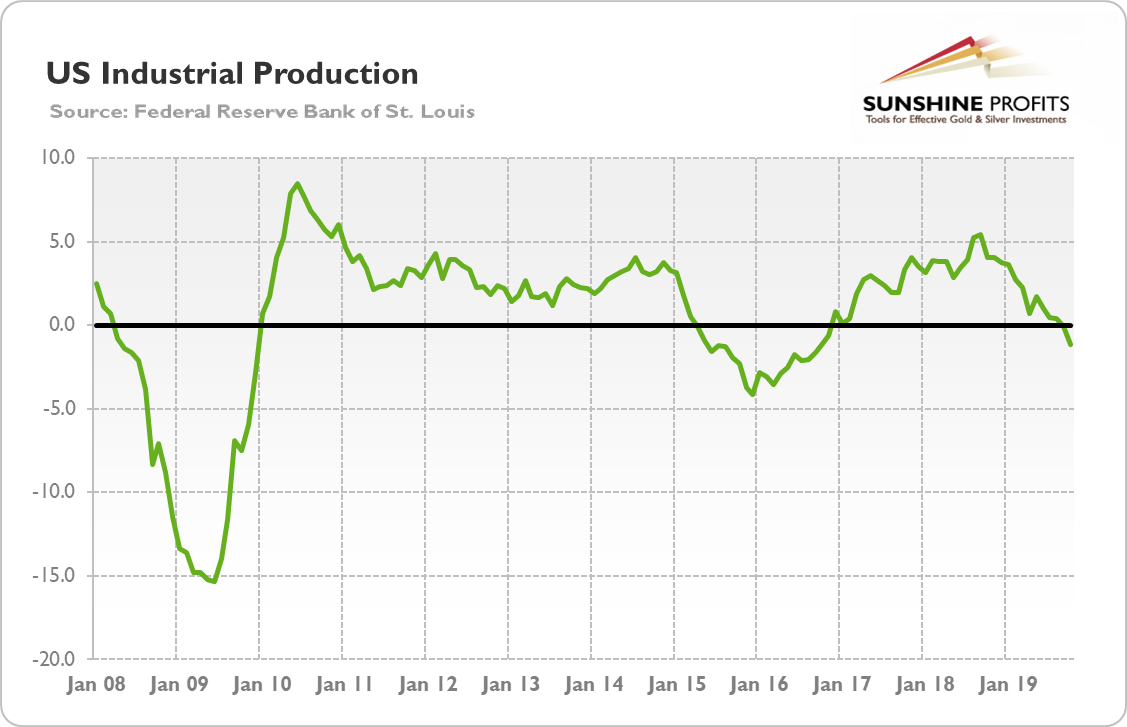

The situation in the industrial sector does not look good on an annual basis either. As the chart below shows, the industrial production fell 1.1 percent over the twelve months ending in October, moving decisively into the contraction area.

Chart 1: US Industrial production from January 2008 to October 2019

So, now it should be clear that the industrial sector was significantly hit by weak global demand and trade wars, and entered recession. It should be worrying for the policymakers, but the Fed Chair downplayed the dangers. Powell said that the weakness in the manufacturing sector has not spilled over into the broader economy. He also pointed out the economy is driven by the consumers, not manufactures, so we should not worry: "the 70% of the economy that represents the consumer is healthy, with high confidence, low unemployment, wages moving up."

The fallacy stems from focusing on the GDP. You see, GDP is the sum of consumption, investment, government expenditures and net exports (exports minus imports). And when you look at data, you will indeed find that consumption is the largest part of the U.S. GDP. For example, in 2018, the American GDP was 69.4% personal consumption, 18.3% business investment, 17.1% government spending, and negative 4.8% net exports.

However, there is one fly in the ointment here. The GDP does not accurately reflect the size of the whole economy. As you probably know, to avoid the double counting, the GDP contains only the final goods, i.e., goods which do not undergo any further transformation in the production process. So, for example, it counts only the value of bread in the grocery shop or the gold teeth in the dentist office, but it omits the value of wheat grain, the flour, the bread in bakery, the transportation of bread to the shop, or the value of mined gold nuggets, the refining, distribution, etc. In other words, all the intermediate goods are not included in the GDP.

It means that the GDP leaves out a big part of the economy by not including business-to-business transactions. When we count it in, and calculate the gross output, or the total output, it turns out that the size of the U.S. economy is over $45 trillion, not the $21 trillion currently used. Figured this way, we see that consumer spending is actually less than 40 percent of the total economic activity, not the 70 percent figure that is often reported by the media. So, it should be clear now that although the ultimate economic goal is higher consumption, the business investments and production are what really drives the economy.

What does it imply for the U.S. economy and the gold market? First of all, investors who want to better understand what is going in the economy, should not pay too much attention to consumption. Consumption expenditures are important part of the GDP, but much smaller part of the total output. Simultaneously, we should not neglect the business sector. What is now happening in the industrial sector may be more important than many so-called experts believe.

The industrial sector has contracted in October for the second month in a row. It may signal the upcoming broad-based recession. It does not have to, as sometimes industrial production gives false signals, but this is definitely possible, even if consumption remains strong. After all, consumption logically follows production.

Hence, the industrial recession may be more dangerous than many people believe. Which could turn out to be beneficial for the gold prices. The next economic crisis will be surprising for many pundits who overlook the developments in the supply side of the economy and focus on consumer spending and aggregate demand. To be clear, right now the gross output is predicting a slowdown rather than the full-blown recession, but the relevant data on it are published with a three months lag. Anyway, from the fundamental perspective, it's quite reasonable to have some gold as a safe-haven asset during the industrial recession (after all, the 2019 inversion of the yield curve also signals economy-wide problems), especially that gold does not need a full-blown crisis to shine. After all, 2019 is not a bad year from the macroeconomic point of view, but gold still managed to rise significantly.

Thank you.

Arkadiusz Sieron, PhD

Sunshine Profits - Effective Investments through Diligence and Care

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts.