tools spotlight

-

Powell’s Magic Won’t Cure Gold’s and Silver’s Ills

March 18, 2021, 10:19 AMIn a classic example of trying to control the narrative, the Fed now admits that inflation can be an issue, thus giving the precious metals a potential boost – albeit one that will likely be short-lived.

Underneath the magic, the fundamentals remain the same. The reality on the ground is different than how investors’ sentiment sees it. The same applies to Europe and the EUR/USD currency pair. But before examining the Fed and Europe, let’s have a look at where gold might be headed in the very short-term as the USDX stumbled.

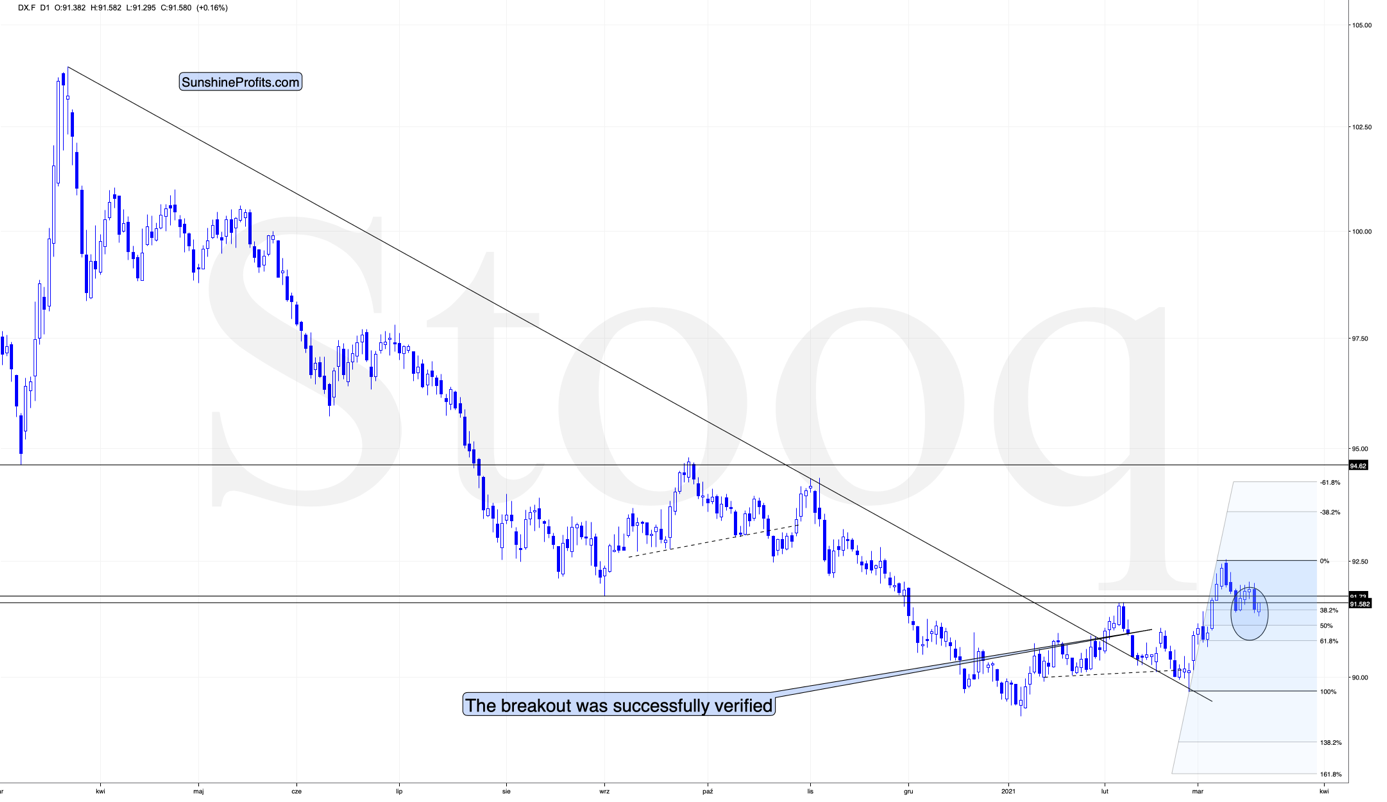

Exactly one week ago (March 11), I wrote the following on the above USD Index chart:

[I wrote that when the USD Index was at about 91.9 and gold was at about $1,733 as a response to a question whether a small move lower in the USDX could indeed trigger a ~40 rally in gold.]

So, can the bottom in the USD Index form at about 91.6 while gold rallies to ~$1,770. Of course.

One of the ways in which this could be done is for the USD Index to rally a bit here while gold ignores that and rallies anyway – which is what we already see taking place right now – and then when the USD Index declines to 91.6 or so, gold would rally even more. Gold is only $40 away from the above-mentioned upside target, so it won’t take much to get it there. For instance, we might see another $10 rally while the USD Index pauses, and then a $30 rally when the USDX finally declines, and bottoms.

Moreover, please note that the USD Index could move below 91.6 on an intraday basis and then rally back to it in terms of the daily closing prices. The previous 2021 high in terms of the closing prices was 91.52. So, actually, the USDX could decline to one of the Fibonacci retracements on an intraday basis before getting back up. The classic retracements based on the recent move higher are:

- 38.2% - 91.44

- 50% - 91.10

- 61.8% - 90.77

Also, based on the entire 2021 rally, the retracements would be:

- 38.2% - 91.25

- 50% - 90.85

- 61.8% - 90.45

Consequently, the USD Index could decline to one of those levels (more likely to 91.10 – 91.44 than to 90.45 – 90.85) and then rally back up on an intraday basis, and the analogy to how the situation developed in 2018 would still remain intact.

Combining both above details (gold’s temporary outperformance and the possibility for the USD Index to decline below 91.6 on a very temporary basis) suggests that the rally to $1,770 in gold, and the brief decline in the USD Index can indeed take place together.

In the following days, I added that the easy part of the rally was over, and based on some technical factors, it was no longer so likely that gold would indeed reach $1,770.

What actually transpired in the following days was that the USD Index indeed moved higher and then once again lower while gold exceeded the previous highs. It didn’t move to $1,770, though, but to $1,754 (at least so far). The USD Index bottomed (assuming that today’s overnight low was the final bottom for this decline) at ~91.3, which is more or less in the middle of the downside target area that I put in bold in the above quote.

After moving to ~91.3, the USD Index rallied back above its March 11 low, thus invalidating the breakdown below it.

Technically, it seems that we just saw a zigzag corrective pattern in the USD Index, which is one of the most common shapes that a correction could take. Consequently, it seems that the rally might continue now.

Having said that, let’s take a look at the market from a more fundamental angle.

Abracadabra

Pulling another rabbit out of his hat, at 2 p.m. ET, Jerome Powell, Chairman of the U.S. Federal Reserve (FED), made the PMs’ short-term problems disappear.

Please see below:

I warned on Mar. 17 that the PMs could receive a major boost if he strikes the right tone. And delivering a magical performance, Powell’s presence did just that. Remember though: despite his ability to talk down the USD Index and suppress U.S. Treasury yields, the medium-term ramifications will likely be unkind.

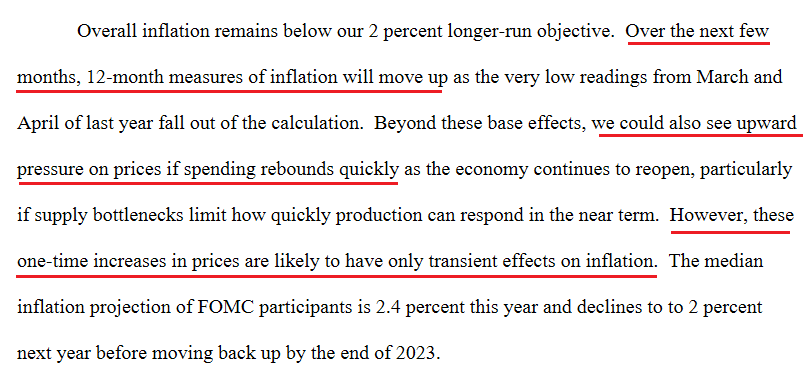

Over the last few months, Powell was adamant that he didn’t see any “unwelcome inflation.” However, on Mar. 17, the FED Chair slightly changed his tone.

Please see below:

Source: U.S. FED

Source: U.S. FEDOn Mar. 4, I wrote that Powell’s deny-and-suppress strategy is seemingly evolving into acknowledge-and-deflect. Thus, not wanting to deny the obvious, Powell finally admitted that inflation “could” be an issue.

More importantly though, his assertions of “one-time” and “transient” are the most newsworthy. Think about it: when inflation was visible, Powell said that it was non-existent. Now that inflation is screaming, he describes it as “transient.”

Behind the curve?

Remember, Powell didn’t major in inflationary honesty: he earns his diploma by maintaining a halcyon environment across fixed income and equity markets. Case in point: when asked to define an “overshoot” of the FED’s inflation target, he responded, “we have resisted the temptation to try and quantify what that means, but when we are above target … we can do that.”

Translation? He’ll let us know.

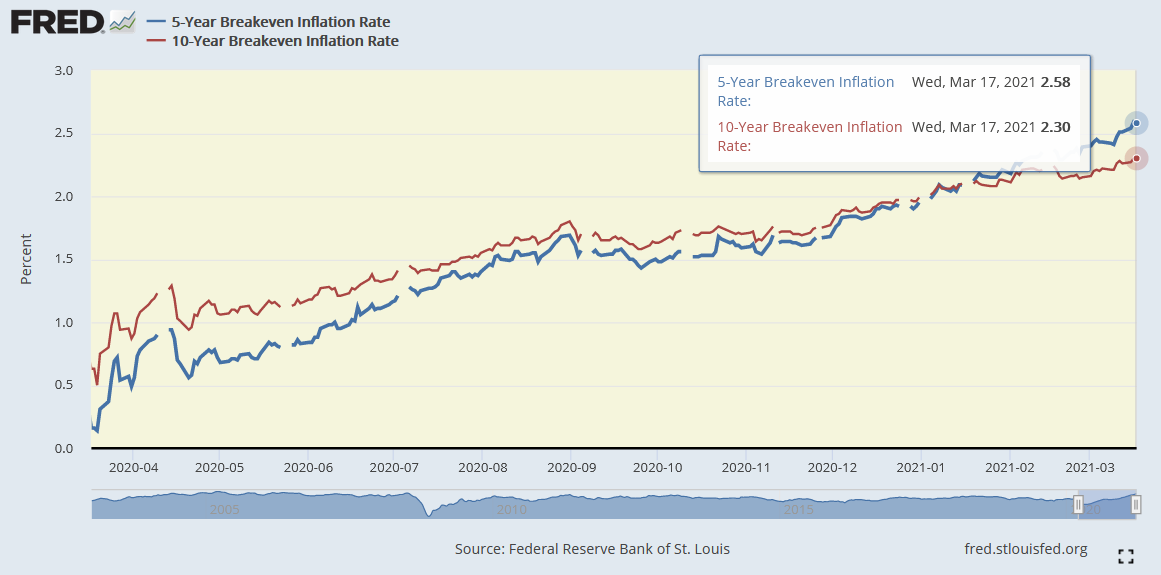

Ironically, he also said that "we want inflation expectations at 2%."

Well, if you analyze the chart below, you can see that U.S. 5-Year and 10-Year inflation expectations are well above 2%.

However, in an effort to thread the needle, Powell told reporters: “with regard to interest rates, we continue to expect it will be appropriate to maintain the current 0 to .25% target range until labor market conditions have reached levels consistent with the committee’s assessment of maximum employment and inflation has risen to 2% and is on track to moderately exceed 2% for some time. I would note that a transitory rise in inflation above 2%, as seems likely to occur this year, would not meet this standard.”

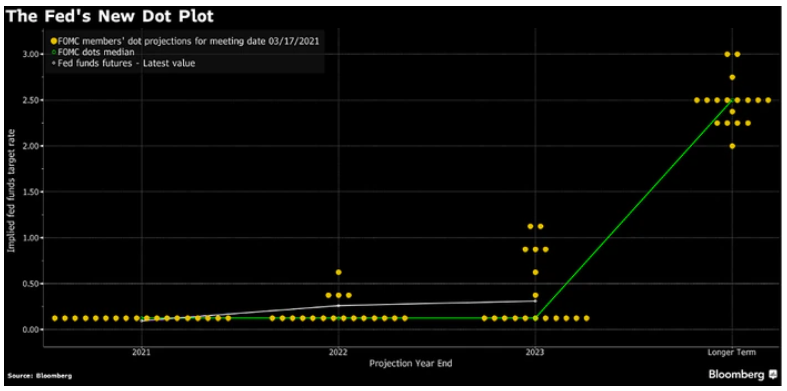

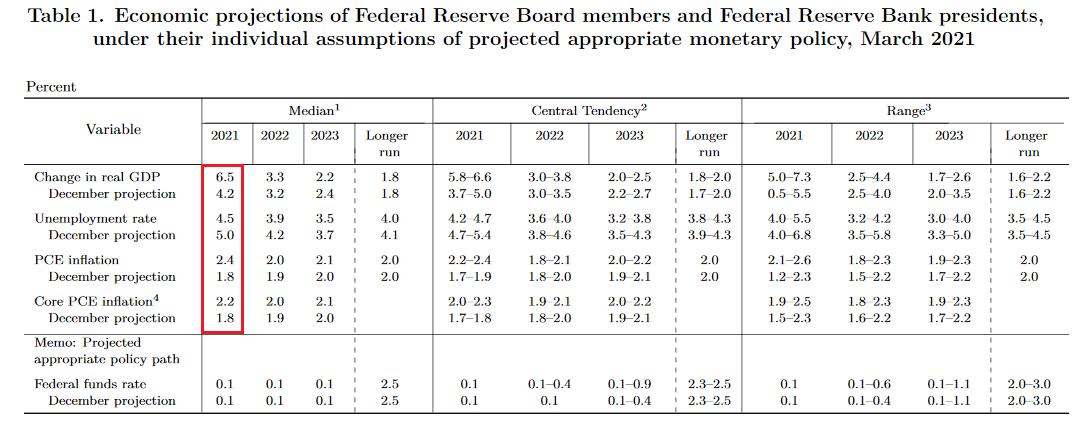

Thus, moving from no “unwelcome inflation” to above 2% is “likely to occur this year,” bond investors aren’t the only ones raising their eyebrows. Within the FOMC’s latest dot plot, four out of 18 FOMC members now expect a rate hike by 2022 (up from one during the December meeting).

Please see below:

To explain, the yellow dots above represent FOMC members’ projections for the federal funds rate (the short-term overnight lending rate). If you analyze the four dots in the middle of the chart (2022), you can see that FED officials are slowly moving up their rate-hike expectations.

As a result, while Powell is quite successful at pacifying financial markets, the fundamentals remain the same. In the short-term, markets rally on what they hope to achieve. Over the medium-to-long-term, reality reveals what has actually been achieved.

Case in point: immediately following Powell’s performance, the U.S. 10-Year Treasury yield plunged.

Conversely, the EUR/USD surged (sinking the USD Index in the process).

However, while sentiment moves markets, the economic reality is much different on the ground. Case in point: as the EUR/USD enjoyed a 0.66% rally on Mar. 17, German Chancellor Angela Merkel’s economic advisers reduced their 2021 GDP growth forecast from 3.7% to 3.1%. For context, Germany is Europe’s largest economy and the original projection (3.7%) – made only four and a half months ago – is now below economists’ consensus estimate.

Please see below:

In addition, while Bundesbank President Jens Weidmann called Germany “sufficiently resilient” and implied that a recovery would “arguably only be postponed,” hope remains investors’ favorite therapy. In reality though, Europe’s fundamental underperformance of the U.S. is one of the worst-kept secrets.

Source: Bloomberg

Source: BloombergContrasting Germany’s downgrade, the FOMC actually increased its 2021 U.S. GDP growth forecast from 4.2% (which it made in December) to 6.5% (the red box below). Furthermore, the U.S. unemployment rate is expected to fall to 4.5% (versus a December forecast of 5.0%).

Source: U.S. FED

Source: U.S. FEDThus, when U.S. economic outperformance of Europe is increasing, why is the EUR/USD rallying? And if FOMC members are increasing their rate-hike expectations, why are the U.S. 5-Year and 7-Year Treasury yields falling?

Well, as I mentioned above, in the short term (and especially very short term), investors create their own reality.

Keep in mind though: a few choice words and a reinforced narrative doesn’t solve Powell’s fundamental quandary. With breakeven inflation rates failing to follow nominal yields lower, the FED Chair remains stuck in a medium-term inflation trap. Moreover, with the EUR/USD bought on hope and sold on reality, the USD Index should reap the benefits over the medium-term.

In fact, the quick Powell-induced decline in the 10-year yields might already be over. One of the previous charts showed that the yields declined substantially initially, they still ended the day higher.

Source: Marketwatch

Just as the move lower in yields was temporary, the move lower in the USD Index and the rally in the precious metals sector might be (has been?) very short-lived.

In conclusion, the PMs received a short-term boost on Mar. 17, but their fundamental ills have yet to be cured. The USD Index’s negativity was mind over matter, and despite the volatility, the U.S. 10-Year Treasury yield actually ended the day up by 0.62%. As a result, the medium-term outlook for the PMs remains profoundly bearish. A Powell-induced pause, followed by a continuation of the theme, will likely haunt the PMs over the medium-term.

Letters to the Editor

Q: I am enjoying your guidance very much, thank you. In your analyses I have read how it would be better to short the GDXJ, and not use the JDST because of the time decay of leveraged ETFs.

If a person decides to short in this case, they lose leverage, unless they short a leveraged ETF. So, this is something I haven’t seen your comments on. If I short NUGT, I see three advantages.

1) I’m shorting, thereby avoiding the time decay.

2)I gain leverage by using a 2x ETF,

3) I’m guessing here, but if there is time decay in this trade, doesn't the time decay now work in my favor?

Looking forward to hearing how I’m wrong about this. Your sharp mind and words can straighten this out for me. Again, Thank you!

A: Thank you for the kind words. In many cases, shorting JNUG (or NUGT) would indeed be a nice compromise between leverage and the ability to stay in a given position, even if the market does nothing for prolonged periods.

However, since there’s no free lunch in general, let’s consider what one would be resigning from or in what way would one be paying for this. There are two factors here:

- While the time decay now works in one’s favor, the possible loss on the trade is theoretically unlimited. In case of the unleveraged positions, that also applies, but in case of leveraged positions this is becoming increasingly more important.

- The leverage is not as big as it seems in this case. The 2x leverage works on a day-to day-basis, not based on the entire move.

Here’s what it means in practice:

If the GDXJ moves from $48.74 to $24.12 over the next 40 trading days and it declines by the same % each day, it would imply a decline by about 1.74327% each day. This means that – given the 2x leverage – JNUG would decline by about 3.48655% each day, and JDST would rally by about 3.48655% each day – for these 40 trading days.

Now, since on each day it would move by a certain percentage of its previous days price, it means that the situation is not as symmetrical as it may seem.

Yesterday’s closing prices for JNUG and JDST were $92.83 and $10.63, respectively.

So, by rallying 3.48655% each day for 40 trading days, starting at $10.63, JDST would be likely to increase to about $10.63 x (1+0.0348655)^40 = $41.87

However, by declining 3.48655% each day for 40 trading days, starting at $92.83, JNUG would be likely to decline to about $92.83 x (1-0.0348655)^40 = $22.45.

Buying JDST at $10.63 and selling it at $41.87 means more or less quadrupling one’s capital dedicated to this trade (profit of about 294%).

Shorting JNUG at $92.83 and covering the short position at $22.45, means a profit of less than 100% (about 76%).

So, the former approach would have yielded almost 4x as good results.

Now, what would happen if one was on the wrong side of the market for an identical move? Well, if – given the same scenario – one shorted JDST / went long JNUG, one would either lose 294% of the initial position (assuming that they would be increasing the deposit necessary for shorting in order to prevent the position from being closed), or “only” 76%.

I’m quite sure that after considering the above simulation the idea of shorting leveraged products no longer seems so attractive to many people. But am I saying that one should never do it? No – I’m just saying that one needs to know exactly what they are getting themselves into. There are myriads of strategies in financial engineering, but there’s never any free lunch. And if there is, it’s being exploited too quickly by various algorithmic trades that individual investors won’t be able to really reap any meaningful profits from it.

I’d say that if one is expecting a bigger move to happen relatively soon, then regular long positions (either leveraged or not, depending on one’s preference) would be preferred, but if one thinks that a given move is very likely to take place but it’s not clear when that would take place and if we would see some sideways trading for weeks or months before, then shorting leveraged instruments might be worth considering, while keeping the position sizing principles in mind. In general, it’s best to consider such strategies only after one gets more experience in the markets – I definitely don’t recommend that to everyone (or most people).

Q: I’m not sure if you are tracking this or not, but since the gold peak in August 2020, gold has dropped $3.15 per each one basis point increase in the 10-year yield. If this continues, and the Fed starts YCC at a 10-year yield of 2%, then the trough in the price of gold will be circa $1624. As such, $1350 - $1500 gold might just be a bridge too far.

A: That’s a very interesting observation, thank you. There are two things that I’d like to say here:

- The Fed might not start the YCC program (Operation Twist 3.0) for longer, if stocks don’t plunge profoundly. This would confirm my previous points, when I was writing that I expect PMs and stocks to decline together during the first part of stocks’ decline (exactly what happened after the 1929 top and after the tech bubble burst). This might happen with yields closer to 3%. If that takes place, it would imply – based on your calculations – a bottom about $315 lower than $1,624, meaning at about $1,309.

- Your calculations are based on average movement, and my targets are based on the extremes that gold might reach during the emotional slide. Gold and yields go together, but it’s not a perfect alignment. For instance, right now, the yields just moved to new yearly highs, while gold didn’t, because it had previously declined too much too quickly, and it had to correct. In the final part of its decline, gold would be likely to get ahead of itself too and decline more than “it should”.

In my view, based on any of those reasons, gold could bottom close to $1,500, and based on some (even partial) combination of both, it could temporarily move even lower.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Have the Ides of March Come for Silver?

March 17, 2021, 10:38 AMGold’s volatile little brother had an interesting run thus far, with internet forums buoying its price. But will fundamentals prevail? Where is silver headed?

“The Ides of March are come,” said Caesar. “Aye Caesar; but not gone,” replied the soothsayer. The Ides of March quotation is often bandied about in financial articles midway through the month. Caesar was assassinated on March 15th in 44BC (or BCE), at a meeting of the Roman Senate. Written about by Plutarch and further popularized by Shakespeare (who dramatized the event), the day has often been used as a harbinger of ill fortune. So, if we’re to look at silver, should we be concerned about anything at this time?

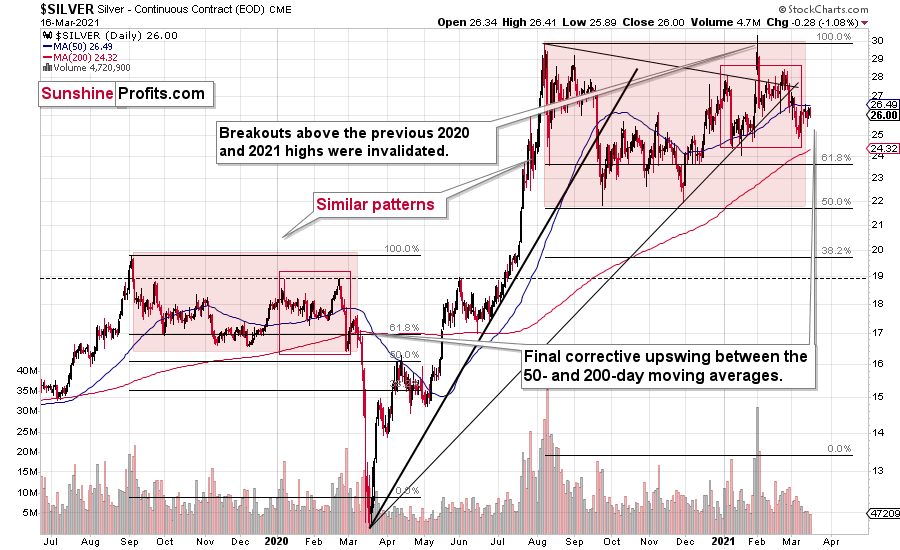

Silver is moving similarly to what we saw in the second half of 2019 and early 2020, before the huge slide. I marked the very broad tops that followed a quick rally in the red-shaded rectangles, and I also created solid-line red rectangles based on the last two – normal – tops and the initial decline that followed them.

Based on the sudden increase in silver’s popularity, it spiked 1.5 months ago, but this move to new highs was quickly invalidated. The nature of this move was more or less random – it didn’t stem from a change in fundamentals or from a specific technical pattern, but rather from a sudden growth of interest in silver based on forum posts. Because of that, and because this upswing was quickly invalidated, this quick upswing didn’t really break the self-similarity pattern.

Right now, we see a corrective upswing between – approximately - the 50- and 200-day moving averages (marked with blue and red). This upswing corresponds to the corrective upswing in gold and mining stocks (which allowed us to profitably go long in case of the latter). We saw – approximately – the same thing about 12 months ago, right before the huge slide.

And speaking of time, please note that the final corrective upswing of early 2020 took place in very late February and early March, while the two – normal – tops that created the red-line rectangle formed more or less at the turn of the year and in late February. This year, it’s all taking place at almost exactly the same time of the year.

If this self-similar pattern is indeed materializing, then the implications are very bearish, and we can expect a major downturn any day or week now.

Let’s be realistic - so far, the analogy might seem too unclear to be viewed as a reliable base for making a silver forecast.

But what if… What if there was a very similar pattern in the past that also preceded a massive decline? This would greatly increase the reliability of the above self-similarity.

There was indeed such a pattern!

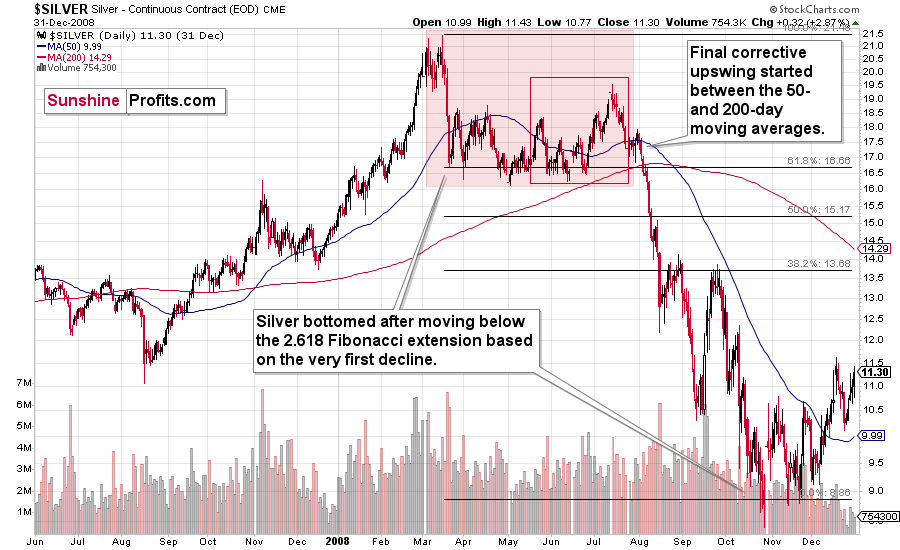

That’s what silver did in 2008 before it declined.

The August 2007 – March 2008 rally (please note the interim top in November 2007 that was followed by a zigzag decline, more or less in the middle of the rally) is similar to the March 2020 – August 2021 rally (please note the interim top in June 2020 that was followed by a zigzag pattern, more or less in the middle of the rally).

Afterwards, we saw a double top in both cases that was followed by a sizable slide. Then silver formed a specific U-shaped broad top, where the final top was below the initial one (exception: in this case the forum-based rally took silver slightly above the previous high, but due to the specific / random nature of the move, it “doesn’t count” as something that invalidates the analogy).

After the top, silver declined, and the final corrective upswing took place approximately between the 50- and 200-day moving averages.

Please note that in both previous (2008 and 2020) cases silver then truly plunged, and it kept on declining until it moved below the 2.618 Fibonacci extension based on the initial downswing. The above charts illustrate that by showing the first decline at the 38.2% retracement (1 / 0.382 = approximately 2.618). Applying the same to the current situation (the initial decline took silver from below $30 to below $24) provides us with the minimum decline target at about $13.50. Will silver really decline as low? In my view, it’s imperative to watch other markets for indications as they might have more reliable targets (for instance gold), but I wouldn’t say that this target (or lower price levels) is out of the question. Of course, that’s just on a temporary basis – silver will likely soar in the following months and years (after this decline).

Before summarizing, please note silver’s tendency to decline sharply in March – that’s what happened in 2008 and 2020. Even if the entire self-similar pattern doesn’t continue, based on this seasonality, silver is likely to decline soon, anyway.

Summing up, if the similarity to what happened in 2020 and 2008 is upheld, then it seems that we’re about to see a big decline in the price of the white metal. Naturally, that’s not the only reason to expect silver’s weakness in the following weeks and months (not necessarily days) – you will find other reasons in my previous analyses.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

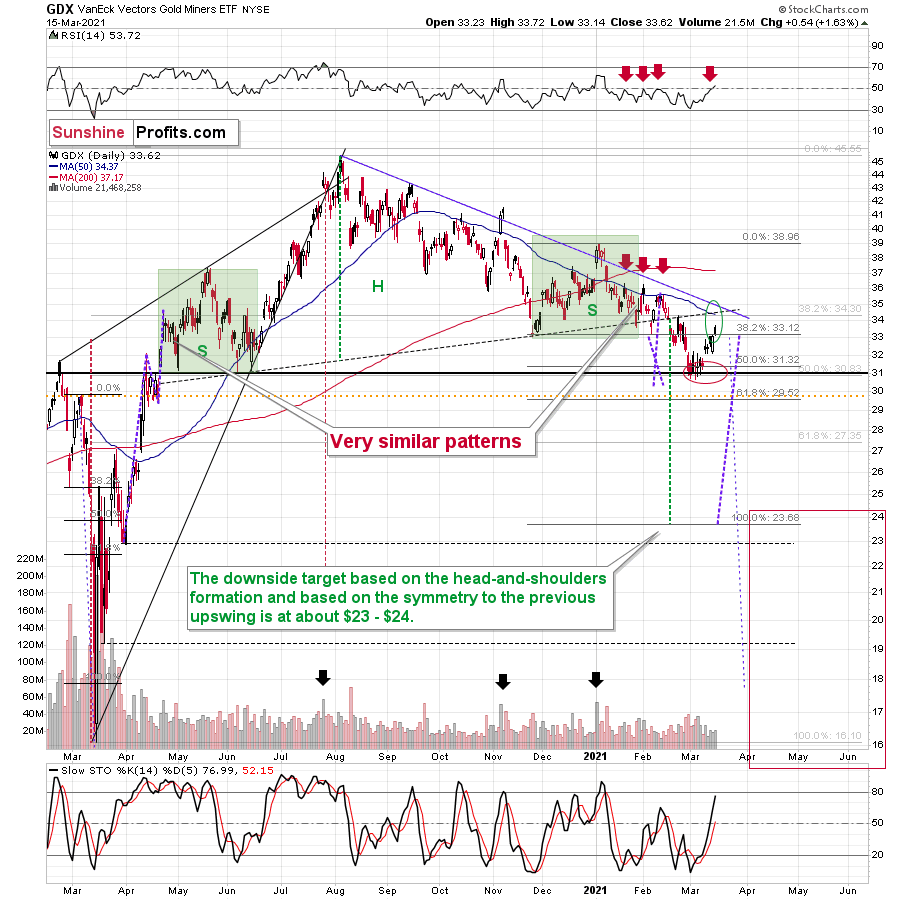

Looking at Gold's and Miners’ Next Moves

March 16, 2021, 10:33 AMGold, silver, and mining stocks moved higher yesterday (Mar. 15), and they did so without the bullish push from the declining USD Index. Conversely, the USD Index ended yesterday’s session a bit higher. Is this strength an indication that a bigger rally in gold is on the horizon?

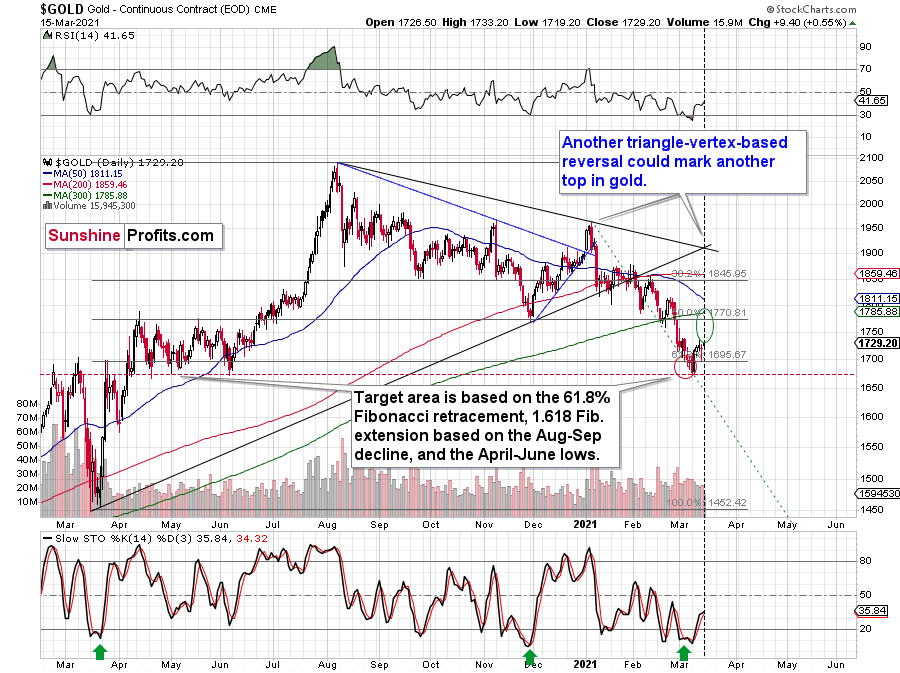

In my opinion, this is not necessarily the case. This kind of supposedly bullish action could still be a purely technical (emotional) development. This week’s triangle-vertex-based reversal is due more or less now (or it was due yesterday – more on that shortly), which means that the yellow metal is likely to reverse shortly or that it has already done so. If it’s about to reverse right now, and the next big move is going to be to the downside, it means that gold practically had to rally beforehand. Therefore, the fact that it did is relatively normal and neutral, not bullish.

Based on the above chart, the triangle-vertex-based reversal point was due yesterday. However, based on the chart below, it’s due today.

There might be slight differences between chart providers, which – if applied to relatively long-term lines – can distort the implications by a few pixels on the chart. These few pixels might mean a day (or so) of a difference in the case of the triangle-vertex-based formation.

Instead of going over charts of multiple providers on each day, it’s more useful to notice that the triangle-vertex-reversal points work on a near-to basis and thus expect a given reversal to take place close to the point suggested by the above technique, rather than going all-in based on the assumption that it will work perfectly. Every now and then it does work perfectly, but the “broad” approach is overall more useful.

At the moment of writing these words, I see that gold futures formed a small top just about $2 below the previous March high ($1,738). Consequently, both following scenarios would make sense in light of the current triangle-vertex-based reversal:

- Gold could decline right away as it doesn’t have to form a new high at the reversal point – just “a high”

- We could see another small, several-dollar rally, which would take gold to new monthly highs and make the triangle-vertex-based reversal work in a classic way, where it detects the final top for a given rally. The FOMC weeks tend to have higher intraday volatility, especially right before the interest rate decision is announced and during the press conference. This means that gold could move up and down in a quite volatile manner shortly.

Both scenarios seem quite possible and it’s hard to tell which of them is more likely. In both cases, it seems quite likely that another – big – decline will begin soon. Of course, I can’t promise that the rally is going to be completely over today, but this seems quite likely. And if not, it seems that it’s going to be over shortly, anyway.

And what about mining stocks?

The mining stocks remain in my upside target area, which means that they could have already topped, or that they could top a bit higher. Regardless, based on all the reasons that I discussed yesterday, and also based on the above comments on gold’s reversal, it seems that the days of this rally are numbered (and it’s not a big number, either).

The neck level of the previously broken head and shoulders pattern, the declining blue resistance line, the 50-day moving average, the late-February high – they all create a very strong short-term resistance not far above yesterday’s closing price. But does it mean that the mining stocks have to move higher from here, or that such a rally would be likely?

Not necessarily. While miners managed to close yesterday’s session above the November low, they didn’t manage to close the day above the January and early-February lows in terms of the closing prices. About a month ago, the GDX tried to invalidate the breakdown below these levels, and this move failed – it was followed by a decline to new yearly lows. Will we see the same thing once again? It seems very likely in my view – the history tends to rhyme.

But how low could the GDX ETF go? My previous comments on that matter remain up-to-date, but I would like to stress that just because the downside target area is relatively far, it doesn’t mean that we will necessarily hold our positions until it’s reached. If we see signs of strength that seem reliable (like miners refusing to decline even though gold moves lower combined with gold reaching an important support level while the USDX encounters resistance), I might write about temporarily closing this position – and perhaps even going long one more time – and we might be able to reap additional profits on the corrective upswing, just as I did earlier this month.

Our final downside target area ($15 – $24.5) is quite broad, because a lot depends on what the general stock market will do. I’ll be looking at gold for the key signs along with a few other factors (including the Gold Miners Bullish Percent Index) and determined the buying opportunity based on them – not necessarily based on the price of the GDX or GDXJ by itself.

Yes, this target is quite low, and thus might appear unrealistic, but let’s consider the following:

- Miners are slightly above their early-2020 high – just like gold.

- Gold is likely to decline to its 2020 lows or so

- General stock market might have just topped.

Considering all three above factors it’s clear that a move to even the 2020 lows is not out of the question.

And this means that junior miners might decline more than senior miners. A move from the current levels to the 2020 would imply a decline by about 50% in case of the GDX, and by about 60% in case of the GDXJ.

Letters to the Editor

(I’m including just one question today, separated into two parts; please keep in mind that even though it’s provided as a conversation, it’s my general opinion, not individual investment advice.)

Q1: I hope you are doing fantastic. I have a very important question for you, and I hope you can give me your opinion. If I measured the amount of profit shorting the GDXJ (1x) or going long with JDST (2x) or the GDXD (3x) from the time Gold peaked in Aug 2020 to Dec 2020, shorting the GDXJ is by far the best choice, as you also mentioned in a previous newsletter. Now, in one of my personal accounts I'm using to follow your recommendations and benefit from the upcoming decline, it does not let me short the GDXJ ETF (it does let me go long on anyone), due to the nature of the account. So, if you'd have to pick another ETF that you could use and go long (i.e., JDST, GDXD), what else would you use as a proxy for the GDXJ? I reviewed your list of short ETFs, and like I said, the performance is not there – I understand the 2x, 3x leverage is the main factor. Is there another (1x) long ETF of your preference? Thanks again for everything – your time and dedication to your subscribers.

A1: Thank you, I’m doing quite fine these days, and I hope everything’s fine on your end as well.

Unfortunately, I don’t know of any unleveraged AND inverse ETF / ETN for gold mining stocks.

[EDITED: If anyone does, I’d appreciate bringing this to my attention. After my previous request for that, I received no input, so it seems that there simply aren’t any available.]

One unleveraged and inverse option would be to use the SBUL (WisdomTree Gold 1x Daily Short), but it’s an inverse gold product, not one based on gold mining stocks.

Another idea would be to use (buy) put options (with a relatively long time to expiration - at least several months) but use only a small amount of capital for it.

And yet another idea would be to change the brokerage to one that allows you to short the GDXJ (but I guess this is out of the question).

Q2: Thanks for the reply, PR. I appreciate and value your opinion; I’m your # 1 fan. The main reason why I asked you this – besides of course one being the nature of my account and not being able to short the GDXJ – is also because of your comments on the JDST (2x) and the GDXD (3x), and how this type of leverage is not recommended for everyone.

The long stocks you’ve recommended are currently trading JDST $11.12 – profit take at $39.87 and the GDXD currently trading $24.08, and your profit take suggested of $94.87. I understand the huge significant day-to-day volatility we might see because of the leverage, but based on the targets you’ve provided, there is a clear upside with your targets, so is there another reason why you would not recommend using the JDST(2x) and GDXD (3x)?

Thanks for your response last night – it was beneficial to see that that there is an opportunity with the SBUL (1x) option.

And thanks again for your suggestions and opinions with this, I’ll try not to take up too much of your time after this one.

A2: Thanks, and I’m very happy to reply to you and share these replies with others – this also helps in providing a better service, as it’s usually the case that many people are wondering about the same thing.

One reason against the highly leveraged products is the volatility, which not everyone can handle emotionally.

Another reason against the highly leveraged ETF/ETNs is that this high leverage makes one lose capital over time if the market is simply moving back and forth in a significant way (decline by 50% and a rally by 50% doesn’t mean getting even – after a 50% decline one needs to gain 100% to get back even).

Due to the above, if the market is moving in the “right” direction, but at a relatively slow pace, the negative effect of short-term volatility can cancel out the positive effect of being right on the direction of the market – that’s what you noticed when you wrote that shorting the GDXJ would have provided better results than going long JDST in August 2020.

The final reason is connected with both the above – patience is sometimes required until a given move starts, and before that takes place, one could see their position significantly underwater for weeks (or months in more extreme cases). Based on my experience, most people can’t handle that, and they abandon their trades before the move takes place (often at the worst possible moment), as that’s when emotions hit extremes.

The more advanced traders tend to remember to trade only limited amounts of capital and they make sure that they can easily afford to lose this capital, and when they enter a position, they really know why they entered it, and they know for how long they are going to hold it.

There’s no easy way around the former – keeping the positions reasonable is imperative.

As far as the latter is concerned, one could say that it’s easy because they would follow the Gold & Silver Trading Alerts. We just cashed out nice profits on the previous long position… But what if a position was going nowhere for many weeks? I – the person conducing the analysis – am sure that my techniques were useful, and that if a position remains justified, I’ll feel confident and calm holding it. I am also accepting that some trades will be losing ones, and this doesn’t affect my sleep, etc. But would this be equally true to others, who are relying on me being correct about the market? Theoretically, everyone knows that it’s impossible to be right each and every time, but practice shows that nobody wants to hold a losing position for longer. Every time they look at their portfolio statistics, they will feel the pain of loss all over again. More advanced traders know not to look at their portfolio statistics too frequently as it makes them more emotional about the market, which actually decreases the chance of being successful in trading. They also know that even if they lose this trade, it won’t matter much, as there will be many more trades in the future.

You see where I’m getting with this? The leverage, especially leverage on ETFs/ETNs that is connected with the time decay is like putting the above mechanism on steroids. And just like steroids - it seems to work in theory and in some cases it’s reasonable, but in most cases, the side effects are not worth it.

Am I saying a definitive “no” to leverage? I’m not. I’m just emphasizing that – as a chef’s knife – it can be useful, and it can be dangerous. And it tends to be more useful and less dangerous as one gets more advanced in investment and trading and is more confident in what they’re doing.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

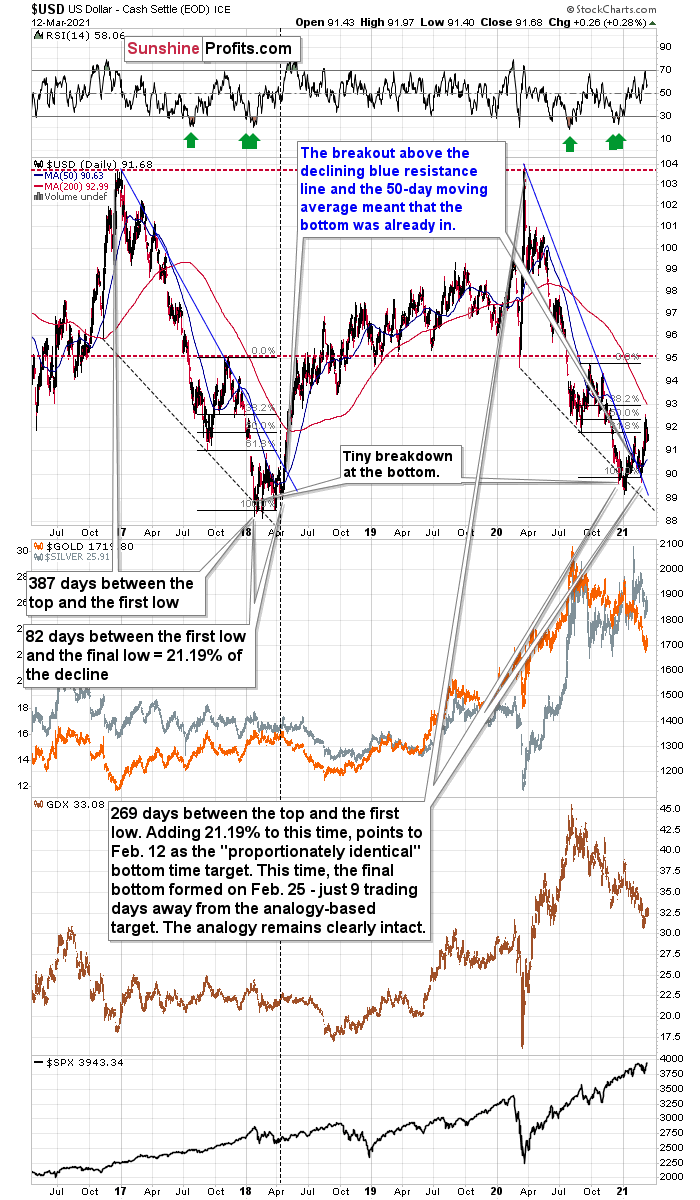

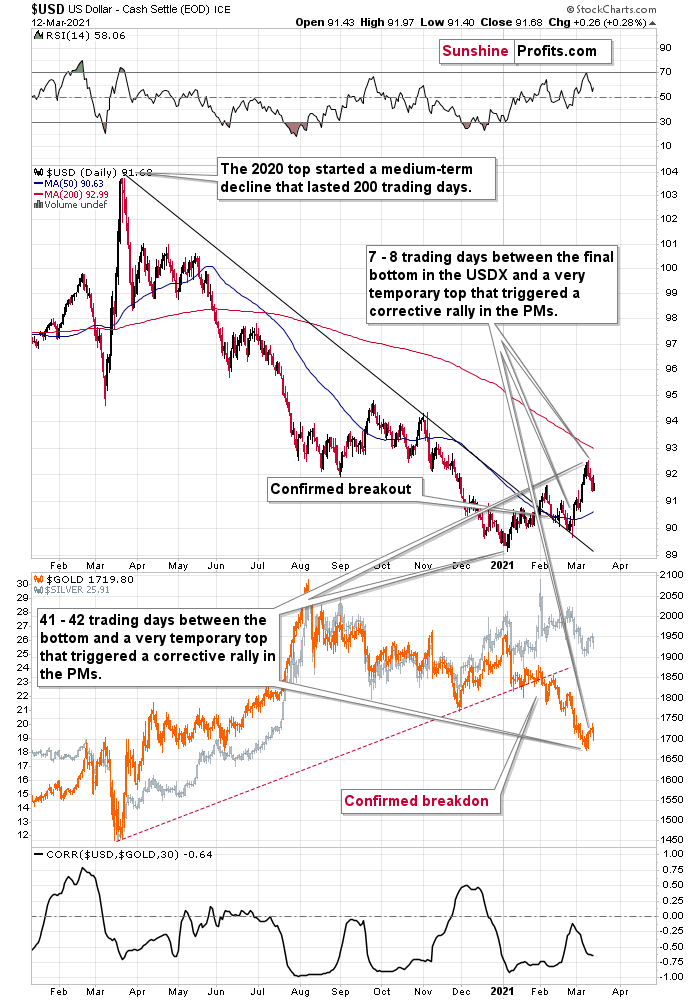

History Rhymes: Does USDX’s Uprising Mean Gold’s Climax?

March 15, 2021, 11:04 AMThe yellow metal’s behavior looks more bearish now than it did in 2017-2018. The USDX has a lot of bullets in its chamber, and gold can be riddled with them.

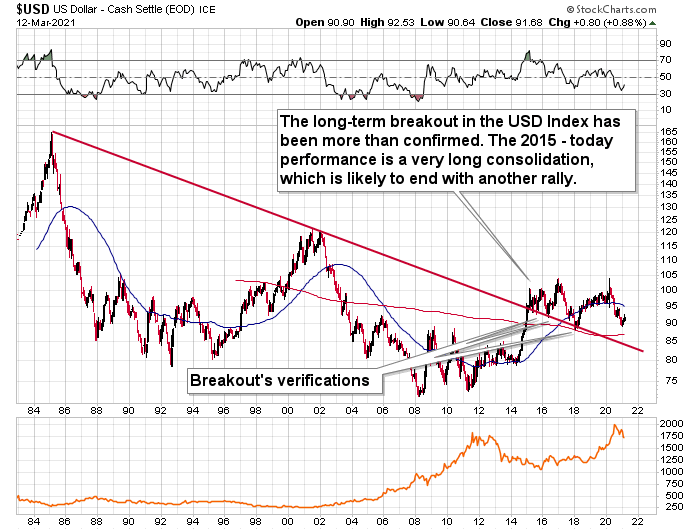

Plenty of warning signs on the near-term horizon: The USDX is after a long-tern breakout, traders are reducing net-short positions, and the slightest shift in U.S. dollar sentiment can lead the rest of the herd to follow. If a USDX resurgence is combined with an equity shock, then the precious metals are in for trouble.

Last Friday (Mar. 12), we focused quite a bit on the moves in the gold miners and how their related ETFs (GDX and GDXJ) are faring and which will suffer most during the next phase of the decline. We also touched on this subject last Wednesday as well. It was important to shed light on the miners because they’ve been leading the charge in the corrective upswing. I also wanted to explain the Eurozone’s impact on the precious metals and how crucial it is to examine the bigger picture and how the pieces are all connected. Today, let’s shift our attention over to the currency perspective, namely the USDX.

The price shape and time analogies are truly remarkable right now. It’s quite often the case that history rhymes, but it’s rare for it to rhyme so closely and clearly to what we now see in the case of the USD Index. And the implications for precious metals investors are profound.

On Mar. 8, I warned that with the USD Index confronting its mid-2020 lows (resistance), a short-term dip could occur in the coming days. But after declining by 0.34% last week, the negativity could be short lived.

Case in point: the 2017-2018 analogue is already in full swing, and while short-term dips were part of the historical journey, the USDX could be about to exit its consolidation phase.

Please see below:

You can also see the similarity between two periods and the technical patterns that they included in the chart below:

Even while looking at the price moves for just a second, the size and shape of the 2017-2018 analogue clearly mirrors the 2020-current price action. Although this time, it took less than 118 days for the USD Index to move from peak to trough.

In 2017-2018, it also took 82 days for the USDX to form a final bottom (the number of days between the initial bottom and the final bottom) and the duration amounts to 21.19% of the overall timeframe. If we applied a similar timeframe to today’s move, then the USD Index should have bottomed on Feb. 12. It actually bottomed (finally) on Feb. 25, which was just 8 trading days away from the former date. Taking into account the sizes of the moves that preceded the previous declines (they took approximately one year to complete), this is extremely close and an excellent confirmation that the self-similar pattern remains intact.

In addition, as the USDX approached its final bottom in 2017-2018, gold traded sideways. Today, however, gold has been in a downward spiral. From a medium-term perspective, the yellow metal’s behavior is actually more bearish than it was in 2017-2018.

Finally, the USD Index’s breakout above its 50-day moving average (which it still holds today) is exactly what added gasoline to the USDX’s 2018 fire. Case in point: after the 2018 breakout, the USDX surged back to its previous high. Today, that level is roughly 94.5.

Moreover, gold’s trepidation alongside the USD Index strength on Mar. 12 adds even more validity to the 2017-2018 analogy.

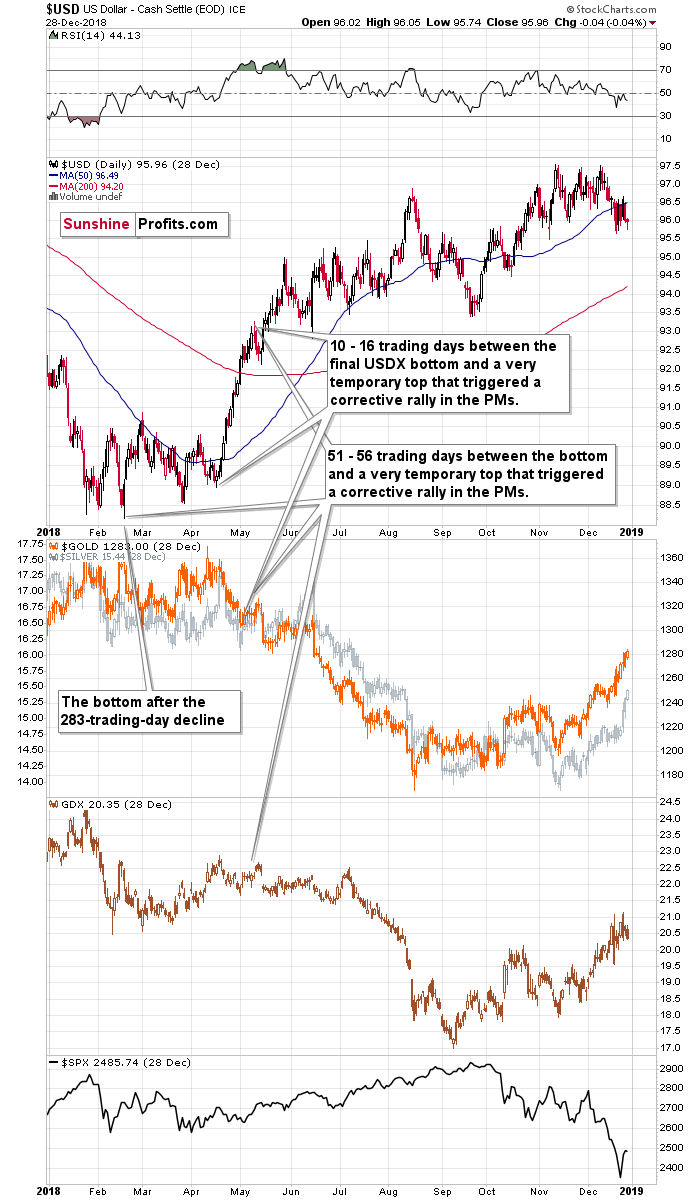

I wrote on Mar. 10:

It’s not true that there were no pullbacks during the 2018 rally. There were, but they were simply too small to be visible from the long-term point of view.

The first notable pullback took place in early May 2018, and it contributed to a corrective upswing in the precious metals market. To be precise, the USD Index declined after rallying for 56 trading days, but gold rallied earlier – 51 trading days after the USD Index’s final bottom. The USDX’s immediate-top formed 16 trading days after its final bottom, and gold’s bottom formed 10 trading days after the USD’s final bottom.

Comparing this to the size of the previous decline in terms of the trading days, it was:

- 51 – 56 trading days / 283 trading days = 18.02% - 19.79%

- 10 – 16 trading days / 283 trading days = 3.53% - 5.65%

More importantly though, when the USD Index turned a short-term decline into consolidation in mid-2018, gold’s hesitant reaction highlighted the yellow metal’s anxiety. And what followed? Well, gold’s next move was significantly lower, while the USD Index’s next move was significantly higher. This means that it was likely a good idea that we took profits from our long positions recently when the GDX moved to $32.96 (opening at $30.80 - $31).

Please see below:

In addition, if we analyze the pairs’ very recent price action, it’s a splitting image.

On Friday (Mar. 12), the USD Index rallied by 0.28%, while gold was (roughly) directionless despite the intraday volatility. And just like in 2017-2018, the yellow metal’s behavior signals a forthcoming climax. As a result, gold and the USD Index are behaving exactly as they did before going their separate ways in 2017-2018. And this means a bearish gold price prediction for the following weeks (not necessarily hours, though).

Please see below:

To explain, I wrote on Mar. 10:

Let’s examine the current situation: the preceding decline lasted for 200 trading days and there were 41 – 42 trading days between the final USDX bottom and the short-term reversals in gold and USDX. Comparing this to the final USDX bottom, we get 7 – 8 trading days.

Applying the previous percentages to the length of the most recent medium-term decline in the USD Index provides us with the following:

- 18.02% - 19.79% x 200 trading days = ~36 - ~40 trading days

- 3.53% - 5.65% x 200 trading days = ~7 - ~11 trading days

The above estimation of about 36 – 40 trading days almost perfectly fits the current 41 – 42-day delay, and the estimation of about 7 – 11 trading days almost perfectly fits the current delay of 7 – 8 trading days.

In other words, the analogy to the 2018 performance does not only remain intact – it actually perfectly confirms the validity of the current corrective upswing. Once again, it’s very likely just a pullback, not a big trend reversal.

The bottom line?

Given the size of the 2018 upswing, 94.5 on the USD Index is likely the first, of many, potential upside targets.

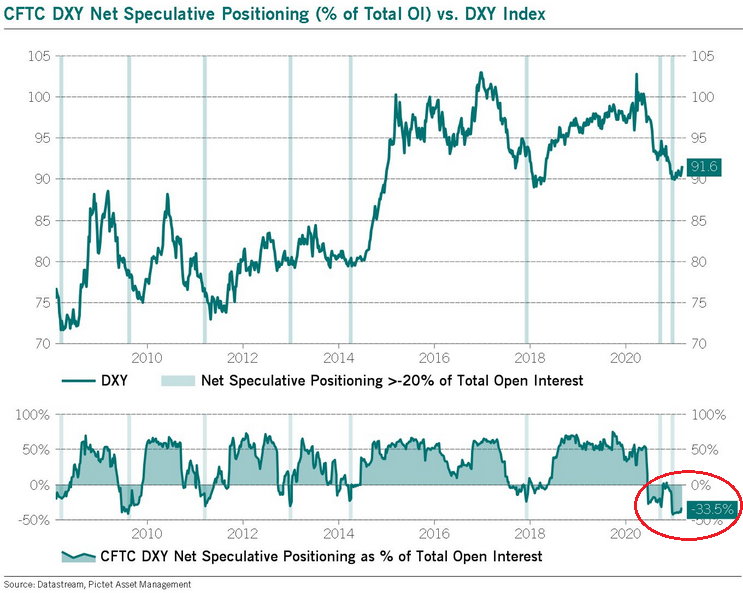

Adding to the list of upside catalysts, the USD Index still has plenty of other bullets in its chamber. For instance, we’re also in the early innings of a shift in U.S. dollar sentiment. With short interest hitting an all-time high in late-2020, it was a complete fire sale. Today, however, short interest may have peaked.

Please see the below chart based on the CoT report:

Please consider how big rallies followed the moments when the net speculative position as % of total open interest started to rally back up after being oversold for months. The situation here is still more extreme than it was in early 2018 and 2014, suggesting that the upcoming rally might be bigger than the ones that we saw then.

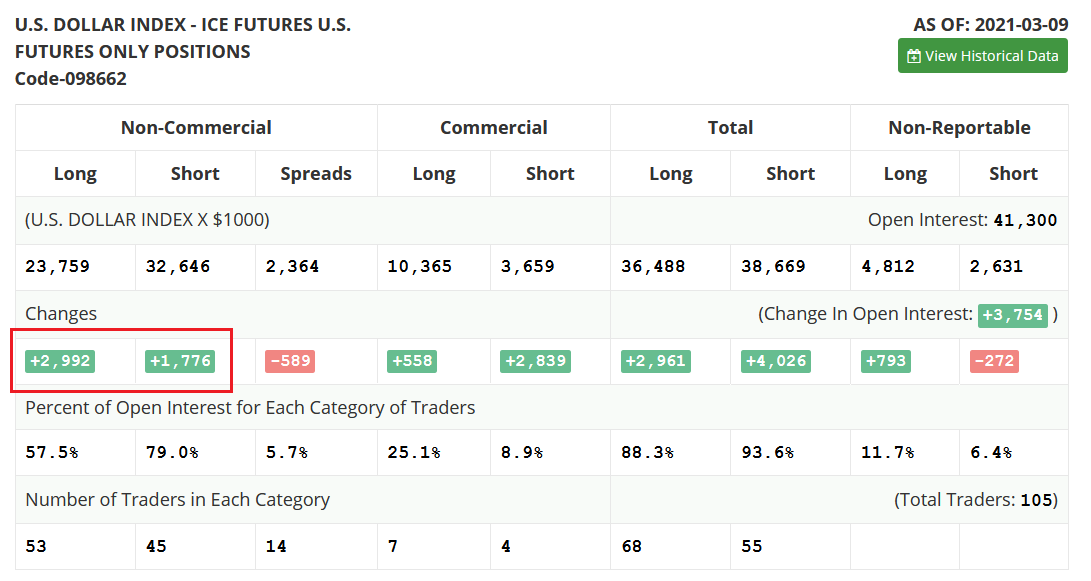

As further evidence, speculative futures traders (non-commercial) actually reduced their net-short positions by 1,216 contracts last week (the net of the two values in the red box below). As a result, the slightest shift in sentiment could lead the rest of the herd to follow.

Finally, let’s not forget that the USD Index is after a long-term, more-than-confirmed breakout. This means that the long-term trend for the U.S. dollar is up.

In conclusion, the USD Index is likely shifting from consolidation to ascension. With the size, scope and duration of the recent price action mirroring 2017-2018, it’s only a matter of time before the USD Index’s medium-term breakout gives way to a material breakthrough. What’s more, the USD Index is finally reacting to the rise in U.S. Treasury yields. Initially ignoring the late-2020 surge, a bottom, and subsequent rally in the U.S. 10-Year Treasury yield has lifted the USD Index 80% of the time since 2003. And with the relationship seemingly restored in 2021, the combination is profoundly bearish for the PMs, especially given today’s triangle-vertex-based reversal in gold.

LETTERS TO THE EDITOR

Q: I was just about to join your Gold service, when I noticed the option to receive ALL trading advice, stocks, oil, etc. But I am confused by something. At the moment, PR seems to think that we may possibly have seen the top in U.S. stocks, and even if not, that a top is not far away (correct me if I have misinterpreted his advice).

But when I look at your stock advice section, Matthew Levy seems to be of the opposite opinion.

How is this intra-company variance possible – your senior (PR) adviser giving out (what I interpret to be) advice that contrasts with another member of your team?

I will definitely join the Gold service, but I'd just like to understand the nature of the other advice before deciding if I want access to it or not.

Many thanks

A: Thank you for the question – this is an important subject to explain. Before replying more precisely, I would like to stress that we don’t provide investment advice, only our general opinions on the markets.

Having said that, I would like to stress that I’m not imposing my views about any market to any other analyst that is providing their analyses on SunshineProfits.com, nor am I consulting my analyses (and require approval) from other analysts. To be 100% clear, every now and then, we’re discussing some issues with each other, but with mutual respect, we then describe the situation exactly as each of us sees it, which may or may not be in tune what others think.

This means that at times two people providing analyses might have opposing views on the same market.

For now, there is only one person specializing in directional trades in the case of any single market, but this will not be the case in the future – there will be more authors for a single market that might have different views, different strategies, different philosophies and approaches. This is not a “bug” but a “feature”. If everything was “set” by one person (for example, by me), there would be little-to-no benefit from having access to the thoughts and views offered by other authors, as there would be no real additional value from reading the same views.

Besides, based on my knowledge and market research, people usually want to read diverse opinions on the internet before making up their mind about something. Therefore, that’s exactly what we want to provide them with through our service. Why can’t people get diverse opinions without having to leave the platform?

I’m not afraid that my views get challenged, as it is not my goal to prove that I’m going to be always correct (which is obviously not possible), nor am I interested in “flexing” power. My goal is to provide the best service to people who join our platform. I think the way to achieve this is through allowing authors to be independent and true to their views.

What I do mind is that the points taken in analyses be well researched, that the analyses are professional, ethical, and are created with great care regarding readers. Moreover, the authors need to adhere to my and this company’s WHY, which is: “to discover and share knowledge with people, so that they can improve their lives”. The analyses can’t be used to promote personal agendas or try to indoctrinate people with regards to an author’s political (or other) views (in fact, there was even a case where an author was forbidden to publish their analyses with us due to this very reason). The analysts are also forbidden to take any remuneration from any companies or ETFs that they might describe in their analyses in order to avoid both real and potential conflicts of interest. However, having opposite views to other authors on the platform is not and will not be forbidden, even if one would have opinions about the market that oppose the ones of the Editor-in-chief. I – PR – will be carefully reviewing the work, approach, and professional background of those that want to join our platform.

Also, Matthew Levy, CFA spotted many profitable trades in the specific (sector-based, including emerging markets) ETFs, which I wasn’t paying attention to, as that’s not my specialty (the precious metals sector is). If you’re considering broadening the scope of available services, and you’re interested in the stock market, I suggest that you give Matthew Levy’s Stock Trading Alerts a try.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Gold Investment News

Delivered To Your Inbox

Free Of Charge

Bonus: A week of free access to Gold & Silver StockPickers.

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM