tools spotlight

-

How the EUR/USD Affects Miners; Which ETF Will Suffer More?

March 12, 2021, 9:46 AMIt’s all connected. The Eurozone’s underperformance boosts the USD, thus placing pressure on gold and the ETFs. So, which ETFs will suffer most?

A large part of yesterday’s free version of the analysis focused on the Eurozone’s economic outlook and how it affects the precious metals. We’ll eventually get to Europe again later in today’s analysis, but let’s first examine gold related ETFs, namely the GDX and GDXJ. How low can they go? That will depend on the general moves in the stock market.

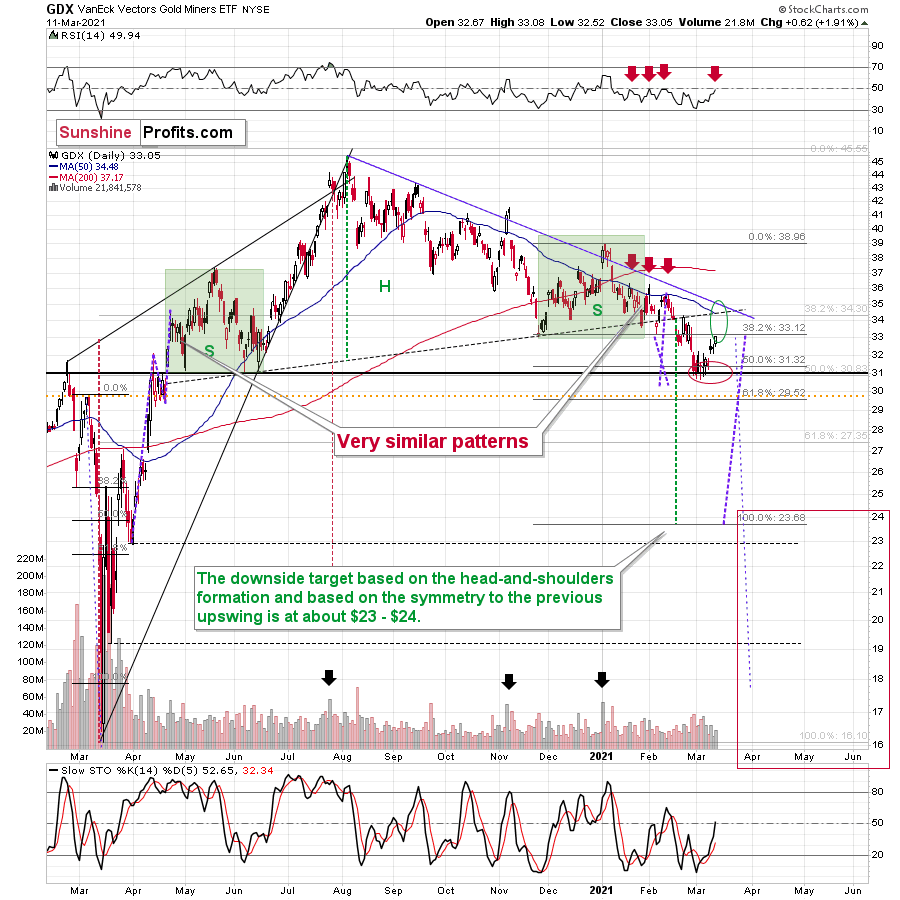

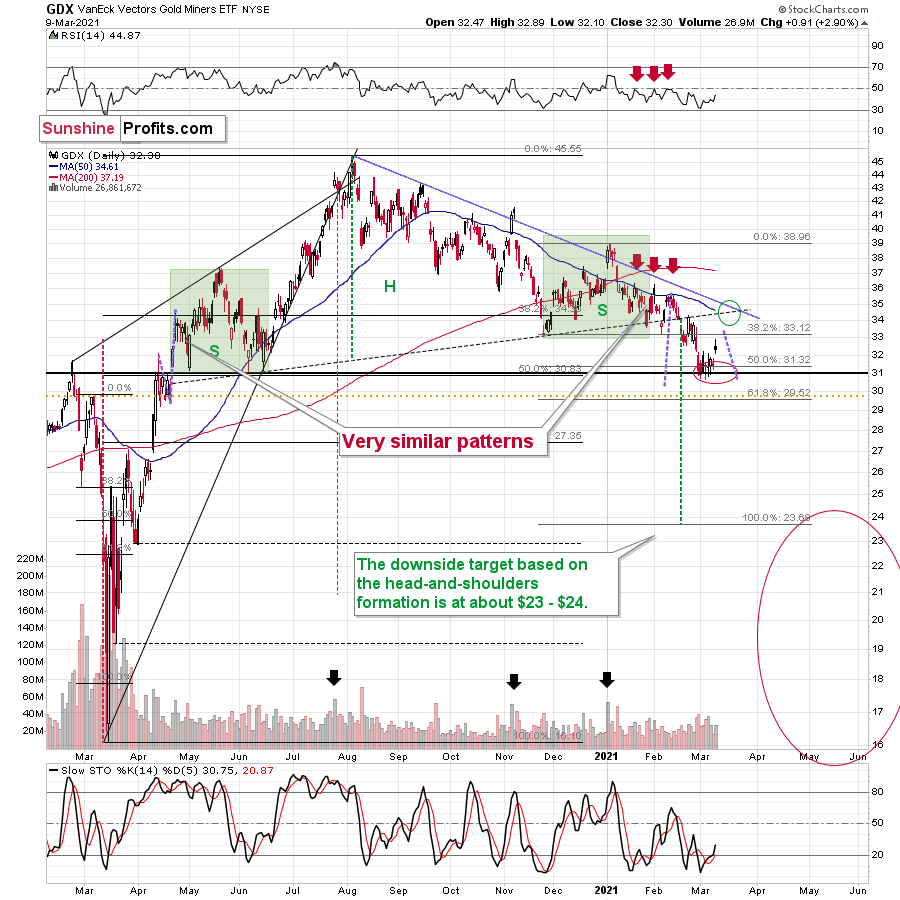

The GDX ETF didn’t move to the strongest combination of nearby resistance levels, but it did flash a few bearish signs, anyway.

The resistance that it reached was notable as it moved to its November 2020 low. Consequently, “it makes sense” for the mining stocks to have topped here.

In yesterday’s (Mar. 11) regular analysis, I wrote the following about the above chart:

Miners generally paused yesterday (Mar. 10), which is quite natural after a sharp daily rally. They closed the day slightly higher, but the RSI is not yet at 50 and the volume that accompanied yesterday’s small move up was nothing to call home about. It was just a pause, and the preceding short-term move is now likely to continue.

Yesterday’s volume was nothing to call home about, but the RSI moved to 49.94 – close enough to 50 to be viewed as a sell signal.

Moreover, please note that while spike-high volume would be a reversal indication, it’s not required for a top to form. The recent small tops formed without high volume.

Consequently, it could be the case that the top in the mining stocks is in, and that by selling GDX at $32.96 yesterday (March 11) we exited the long positions (and entered short ones) practically right at the top – a week after buying in the $30.80 - $31 area.

Before anyone asks, yes, miners were strong relative to gold yesterday, but it was practically the only thing that was positive about yesterday’s session and the USDX’s performance along with gold’s weakness seem more important.

Please keep in mind that every now and then miners very briefly (!) fake their strength (or weakness) relative to gold right before the reversal. The 2016 rally started with a fake breakdown and fake underperformance of gold. So, while the continuous underperformance of miners (compared to gold) is very often bearish, a single day of strength or weakness might be a trap.

How low can the GDX ETF go? Our final downside target area ($15 – $24.5) is quite broad, because a lot depends on what the general stock market will do. I’ll be looking at gold for the key signs along with a few other factors (including the Gold Miners Bullish Percent Index) and determined the buying opportunity based on them – not necessarily based on the price of the GDX or GDXJ by itself.

Yes, this target is quite low, and thus might appear unrealistic, but let’s consider the following:

- Miners are slightly above their early-2020 high – just like gold.

- Gold is likely to decline to its 2020 lows or so

- General stock market might have just topped.

Considering all three above factors it’s clear that a move to even the 2020 lows is not out of the question.

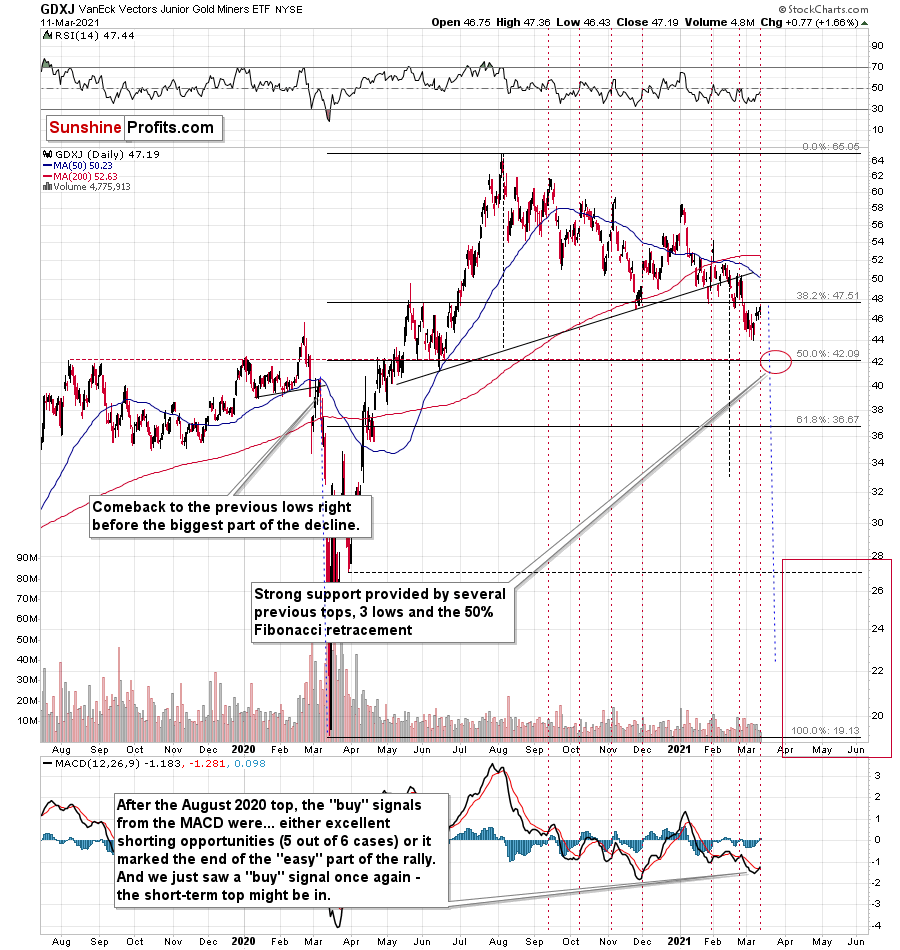

And this means that junior miners might decline more than senior miners. A move from the current levels to the 2020 would imply a decline by about 50% in case of the GDX, and by about 60% in case of the GDXJ.

Speaking of the GDXJ, let’s take a look at its chart.

The most interesting thing on the above chart is a big red warning flag for beginner investors. The flag reads: “verify the efficiency of a given tool on a given market, before applying it”.

The bottom part of the above chart features the MACD indicator. Normally, when the indicator line (black) crosses its signal line (red), we have a signal. If it’s moves above the signal line, it’s a buy sign, and if it moves below it, it’s a sell sign.

But.

If one actually looks at what happened after the previous “buy signals” in the recent months, they will see that in 5 out of 6 cases, these “buy signals” practically marked the exact tops, thus being very effective sell signals! In the remaining case, it was a good indication that the easy part of the corrective upswing was over.

I’m not only describing the above due to its educational value, but because we actually saw a “buy signal” from the MACD, which was quite likely really a sell signal. Today’s pre-market decline in gold (and the move lower in the GDXJ in the London trading) seems to confirm it.

So, how low can the GDXJ go? As it is the case with the GDX, a lot depends on the general stock market and our final target area is quite broad (between $18 and $26), and the key indications will come from other markets and the way they behave relative to each other.

There’s an interim (and strong) support provided by the $42.5 level, which might trigger a corrective upswing, but since we have just seen one, it’s far from being certain that we’ll see another corrective upswing so soon. This could be another opportunity to profit on a long position in the gold miners, but we can’t say that we’ll definitely go long at that time – at least not based on the information that we have available right now. Naturally, we’ll keep monitoring the situation and send out regular (and intraday) Alerts with details as more information becomes available.

Having said that, let’s take a look at the market from the more fundamental angle.

Fundamental Frailty (Part 2)

As you’ve likely noticed, I spend a lot of time analyzing the EUR/USD – that’s because the currency pair accounts for nearly 58% of the movement in the USD Index. And due to Europe’s economic underperformance and the relative outprinting by the European Central Bank (ECB), a sharp rerating of the EUR/USD could be the engine that drives the USD Index back above 94.5

For some time, I’ve warned that the ECB’s bond-buying program was likely to accelerate. On Jan. 22, I wrote:

The ECB decreased its bond purchases toward the end of December (2020), Then, once January hit (2021), it was back to business as usual. As a result, the ECB’s attempt to scale back its asset purchases was (and will be) short-lived. And as the economic conditions worsen, the money printer will be working overtime for the foreseeable future.

And with Eurozone fundamentals continuing to deteriorate, I added on Mar. 9:

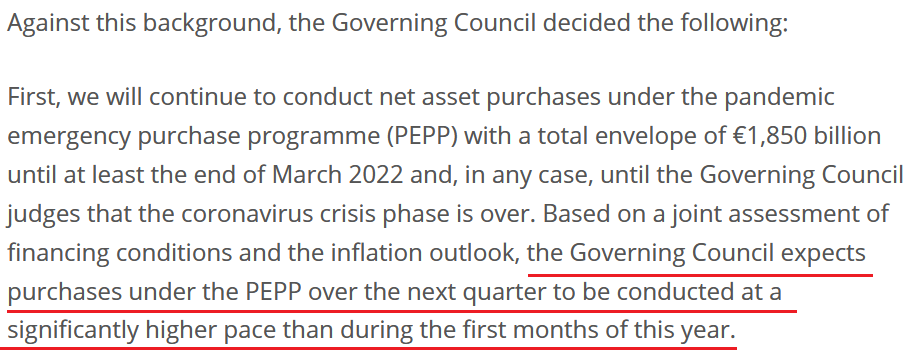

The ECB’s splurge could begin as early as this week. With Eurozone bond yields already on the rise and the debt-ridden economy unlikely to tolerate a sustained ascension, the ECB’s weekly PEPP purchases (pandemic emergency purchase program) are likely to accelerate.

And what happened?

Well, on Mar. 11, the ECB stuck another fundamental dagger into the heart of the euro. Lamenting the rise in European bond yields, ECB President Christine Lagarde told reporters that “market interest rates have increased since the start of the year, which poses a risk …. Sizeable and persistent increases in these market interest rates, when left unchecked, could translate into a premature tightening of financing conditions.”

And why is she so worried?

Well, if you analyze the chart below, you can see that Goldman Sachs’ Financial Conditions Index (FCI) has moved moderately higher. For context, the FCI is derived by calculating the weighted-average impact of the ECB’s overnight lending rate, sovereign bond yields, corporate bond spreads, equity prices and cross-border trade conditions.

Please see below:

To explain, when the white line above is falling, it creates an environment where money is cheap, abundant and easy for corporations to obtain. Conversely, when the white line is rising, it creates the opposite environment. As you can see, excess liquidity has begun to evaporate.

So, what was the ECB’s response?

Source: ECB

As expected, the ECB’s weekly PEPP purchases will now “be conducted at a significantly higher pace.”

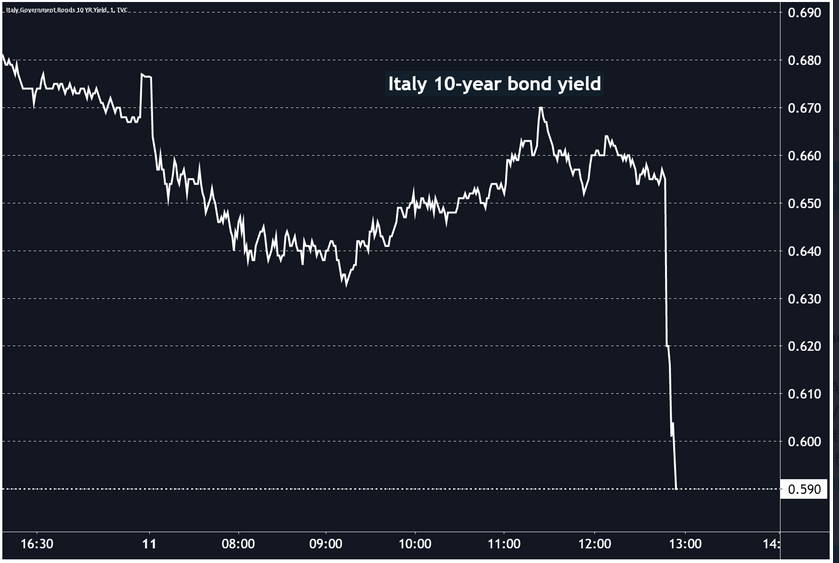

Far from news for those that have been paying attention, Europe is extremely allergic to higher bond yields. Just yesterday, I wrote that rising Eurozone interest rates remain extremely unlikely. And because a picture is worth a thousand words, notice the reaction from the German 10-Year Government Bond yield?

Source: Holger Zschaepitz

Moving in lockstep, the Italian 10-Year Government Bond yield also followed suit.

Source: Jeroen Blokland

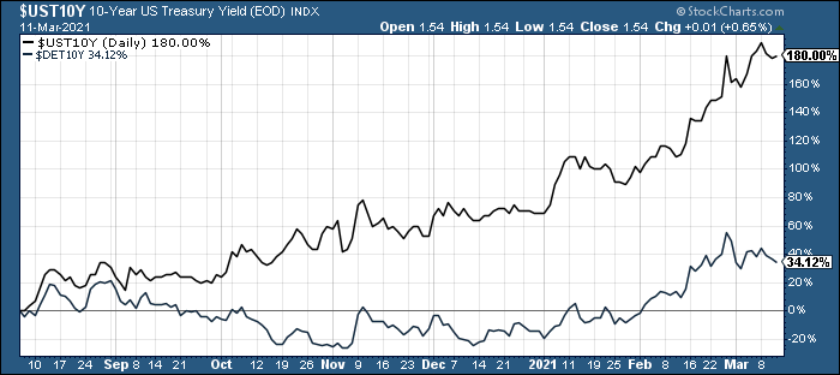

In stark contrast, the U.S. 10-Year Treasury yield actually rallied on Mar. 11. And demonstrating material outperformance, since bottoming on Aug. 6, the benchmark has raced past the German 10-Year Government Bond yield.

Please see below:

What’s more, European lawmakers seem to believe that an economic resurgence is forthcoming. Projecting 3.8% GDP growth in 2021 – headlined by 5.5% growth in France (Europe’s second-largest economy behind Germany) – European officials believe that fiscal support will unleash pent-up demand once the coronavirus pandemic subsides.

For context, I wrote on Feb. 11:

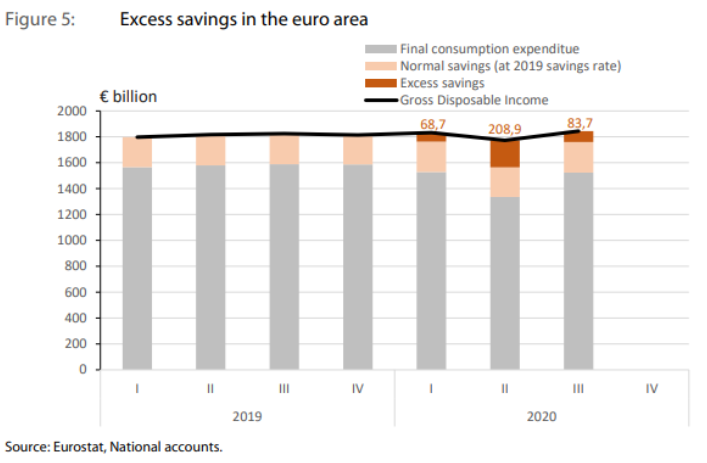

Wishing, wanting and hoping, European lawmakers anticipate that more than €300 billion in excess household savings will lead to an economic renaissance in 2021. However, when you break it down, the balance only amounts to 4% of annual household income. Thus, the short-term bounce (if any) won’t last very long.

And to that point, if you analyze the chart below, you can see that excess household savings in the Eurozone are now less than $84 billion.

To explain, the brown bars above represent excess household savings in the Eurozone. And from the second-quarter to the third quarter of 2020, European households have spent nearly 60% of their Q2 excess savings. Thus, at this pace, there won’t be any “excess savings” left.

Also signaling economic weakness, the slump in Eurozone retail sales (released on Mar. 4) shows that consumers are spending their money on necessities and not discretionary items that boost GDP.

Please see below:

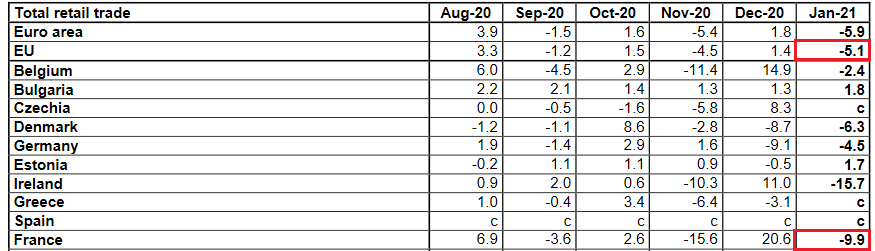

Falling off a cliff, Eurozone retail sales declined by 5.1% in January. Even more revealing, France (– 9.9%) – which is projected to be a beacon of Eurozone growth in 2021 – underperformed the bloc average, with December’s momentum quickly fading in January.

Source: Eurostat

On the flip side, U.S. retail sales rose by 5.3% in January (5.1% excluding food).

Please see below:

And while fundamentals continue to chip away at the EUR/USD, activity in the futures and options markets are signaling a shift in sentiment. Remember, narratives overpower fundamentals in the short-term, thus, changing opinions is like trying to fill a glass from a dripping faucet. However, the pressure may be rising.

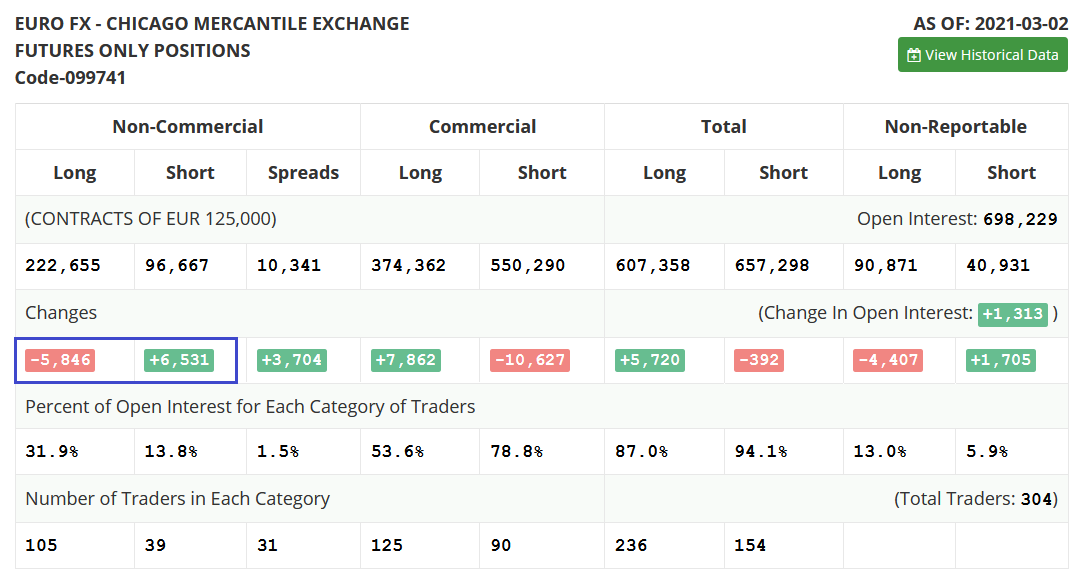

Case in point: the latest Commitments of Traders (COT) report shows that non-commercial futures traders (speculators) have increased the EUR/USD short positions by more than 6,500 contracts, while reducing their EUR/USD long positions by nearly 5,900 contracts (the blue box below).

Source: COT

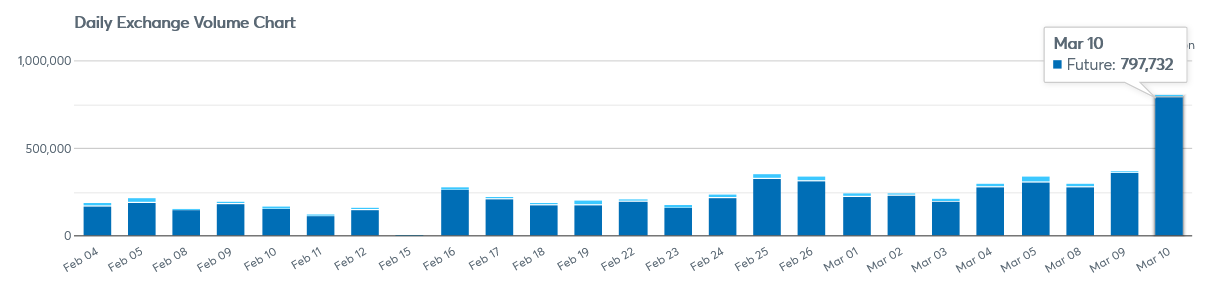

Even more interesting, EUR/USD futures’ volume exploded on Mar. 10. If you analyze the right side of the chart below, you can see that an abnormal number of contracts exchanged hands.

Source: CME Group

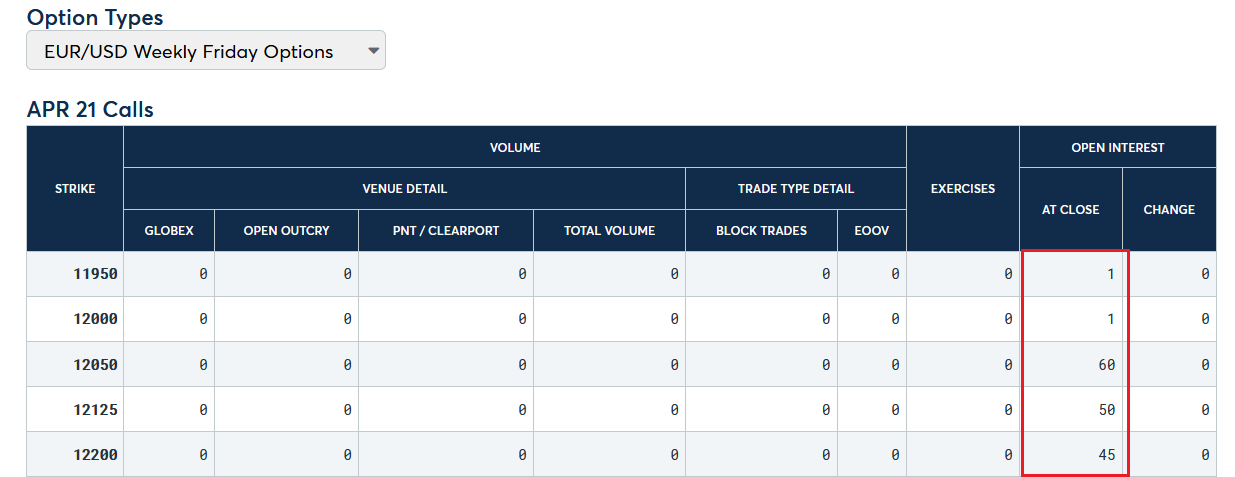

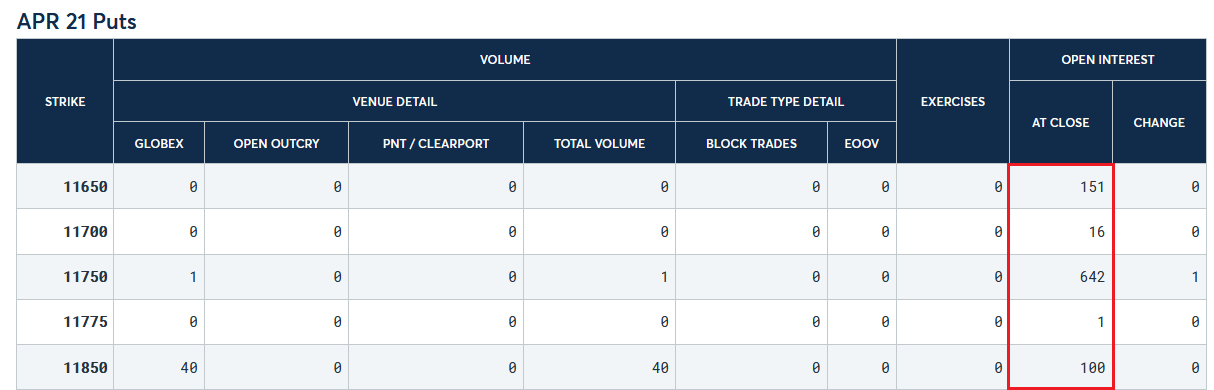

And while the volume data doesn’t tell us whether these are bullish or bearish bets on the EUR/USD, the CME Group’s options data signals that it’s the latter. If you analyze the graphic below, you can see that there is little open interest for bullish bets of 1.1950 or above.

Source: CME Group

In stark contrast, there is plenty of open interest for bearish bets of 1.1850 or below – with 1.1750 the most popular (642 contracts still outstanding).

Source: CME Group

In conclusion, the EUR/USD continues to swim against the fundamental current. And while daydreams of a Eurozone economic boom propel European equity bourses to new highs, the misguided optimism has also lifted the euro. However, with the USD Index already verifying its medium-term breakout and a boost from the EUR/USD likely to push it beyond the 94.5 level, the PMs medium-term outlook remains profoundly bearish. And while their correlations with the S&P 500 remains supportive in the short-term (which I predicted would be the case this week), a severe correction of U.S. equities increases the likelihood of a significant slide over the next few months.

LETTERS TO THE EDITOR

Q: Gold has risen with the dollar many times before – even in 2016. The S&P breaks resistance today and has a breakout. Maybe we get a pull back to 3650 but we do have a breakout to 4400 at least for starters.

A: As I explained earlier today, gold is doing exactly the opposite of what it should be doing if it was to indicate that it’s going to rally along with the USD Index. There will be times when they rally together – and in fact, I think that seeing this after a big slide will be a very important bullish confirmation – but we are not there yet.

Stocks could rally here, but it seems that the PMs would decline anyway because of what’s going on in the USD Index and how gold reacts to it. And since at the moment of writing these words, S&P 500 futures are down by 0.67%, the next big move lower could have already started – we’ll see.

Q: Thanks for the alert I took a position in April gold contracts CGJ12 pretty close to the bottom and closed the position 3-10-2021. I was kicking myself this morning because I left money on the table, but I did not like the movement of gold – it felt like it was at the top. It would be helpful to know the intermediate top in gold before the decline, perhaps with an Alert for those of us that want to go short in the futures market. Are we at the top now?

A: It would have definitely been helpful to know the intermediate top in gold before the decline – and the same applies to mining stocks. And we had indicated the targets beforehand. Still, one cannot “get married” to a certain outlook and should always be looking for things that might invalidate it. That’s what I found yesterday, and I reported it accordingly. Based on today’s pre-market decline in gold, it seems that it was a good decision to take profits off the table yesterday and get back on the short side of the market.

Q: Thank you for remembering me. I appreciate that. Do you expect a violent fall or a calm/gradual fall?

A: I’m happy to reply to the questions that I receive in order to maximize the chance that everyone will be able to benefit thanks to my analyses. I think that the decline will get more volatile close to its end (perhaps in the second half of April and in May) and it might be more measured for the next few weeks. Perhaps this would correspond to a steadier decline to $1,600, but then a fast and brief slide below $1,500. It’s unclear at this time, but it seems that the intermediate support levels might become clearer as gold moves lower.

Right now, it doesn’t seem to be a good idea to plan trading another small counter-trend rally, but if such an opportunity presents itself and several markets show signs of an upcoming reversal, we might go long once again.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

How Euro’s Troubles Can Exacerbate Gold’s Woes

March 11, 2021, 9:24 AMThe EUR/USD currency pair faces significant headwinds. How does this affect the precious metals? What does it spell for gold?

Many people, analysts included, often overlook the multitude of external factors influencing the precious metals. It’s something that I point to and stress in many analyses. These factors can include the shape of the European economy, for example. One has to look at the big picture.

Here’s how it works. Because the EUR/USD accounts for nearly 58% of the movement in the USD Index, anytime that Europe’s economy underperforms that of the U.S. (which is what it’s currently doing), it’s a negative for the euro and bonus points for the dollar. Because the precious metals have a strong negative correlation with the USD Index, a rise in the dollar in the very near future will further serve as downward pressure on the metals.

Additionally, higher inflation and resultant higher interest rates in the U.S. are another negative factor for the euro and a positive one for the USD.

However, before we travel to Europe, let’s take a look at how the precious metals are currently doing, starting with gold.

Gold rallied strongly after bottoming right in the middle of my target area and after moving almost right to its June 2020 bottom, and after almost doubling its initial January decline. Yesterday’s rally also meant invalidation of the brief breakdown below the 61.8% Fibonacci retracement level based on the entire 2020 rally. Thus, the very short-term trend is up.

Please keep in mind that the upswing might be relatively short-lived – perhaps lasting only one week or so. There’s a triangle-vertex-based reversal point coming up this Monday (Mar. 15), so it wouldn’t be surprising to see an interim top at that time, especially considering that:

- The triangle-vertex-based turning points have been working particularly well in the recent past – they marked the January and February tops.

- The corrective upswings during this medium-term decline (especially in mining stocks) often took about a week to complete – at least the easy part of the upswing took a week.

The thing that I want to add here – that already takes us to the part where I discuss the gold-USD link – is that gold rallied overnight. It’s currently up by about $10. This doesn’t mean much by itself, but it does mean a lot, when we compare it with the analogous action in the USD Index.

Namely, the USD Index is up by 0.06%. It’s not important that it’s 0.06%, but it’s important that it’s a tiny upswing and not a decline.

In other words, gold just continued to move higher, even though the USD Index paused after a brief decline. This tells us that the shape of both price moves doesn’t have to be identical. Well, to be clear, it was known right from the start, but it’s often the case that the daily price moves in gold and USDX mirror each other.

So, can the bottom in the USD Index form at about 91.6 while gold rallies to ~$1,770. Of course.

One of the ways in which this could be done is for the USD Index to rally a bit here while gold ignores that and rallies anyway – which is what we already see taking place right now – and then when the USD Index declines to 91.6 or so, gold would rally even more. Gold is only $40 away from the above-mentioned upside target, so it won’t take much to get it there. For instance, we might see another $10 rally while the USD Index pauses, and then a $30 rally when the USDX finally declines, and bottoms.

Moreover, please note that the USD Index could move below 91.6 on an intraday basis and then rally back to it in terms of the daily closing prices. The previous 2021 high in terms of the closing prices was 91.52. So, actually, the USDX could decline to one of the Fibonacci retracements on an intraday basis before getting back up. The classic retracements based on the recent move higher are:

- 38.2% - 91.44

- 50% - 91.10

- 61.8% - 90.77

Also, based on the entire 2021 rally, the retracements would be:

- 38.2% - 91.25

- 50% - 90.85

- 61.8% - 90.45

Consequently, the USD Index could decline to one of those levels (more likely to 91.10 – 91.44 than to 90.45 – 90.85) and then rally back up on an intraday basis, and the analogy to how the situation developed in 2018 would still remain intact.

Combining both above details (gold’s temporary outperformance and the possibility for the USD Index to decline below 91.6 on a very temporary basis) suggests that the rally to $1,770 in gold, and the brief decline in the USD Index can indeed take place together.

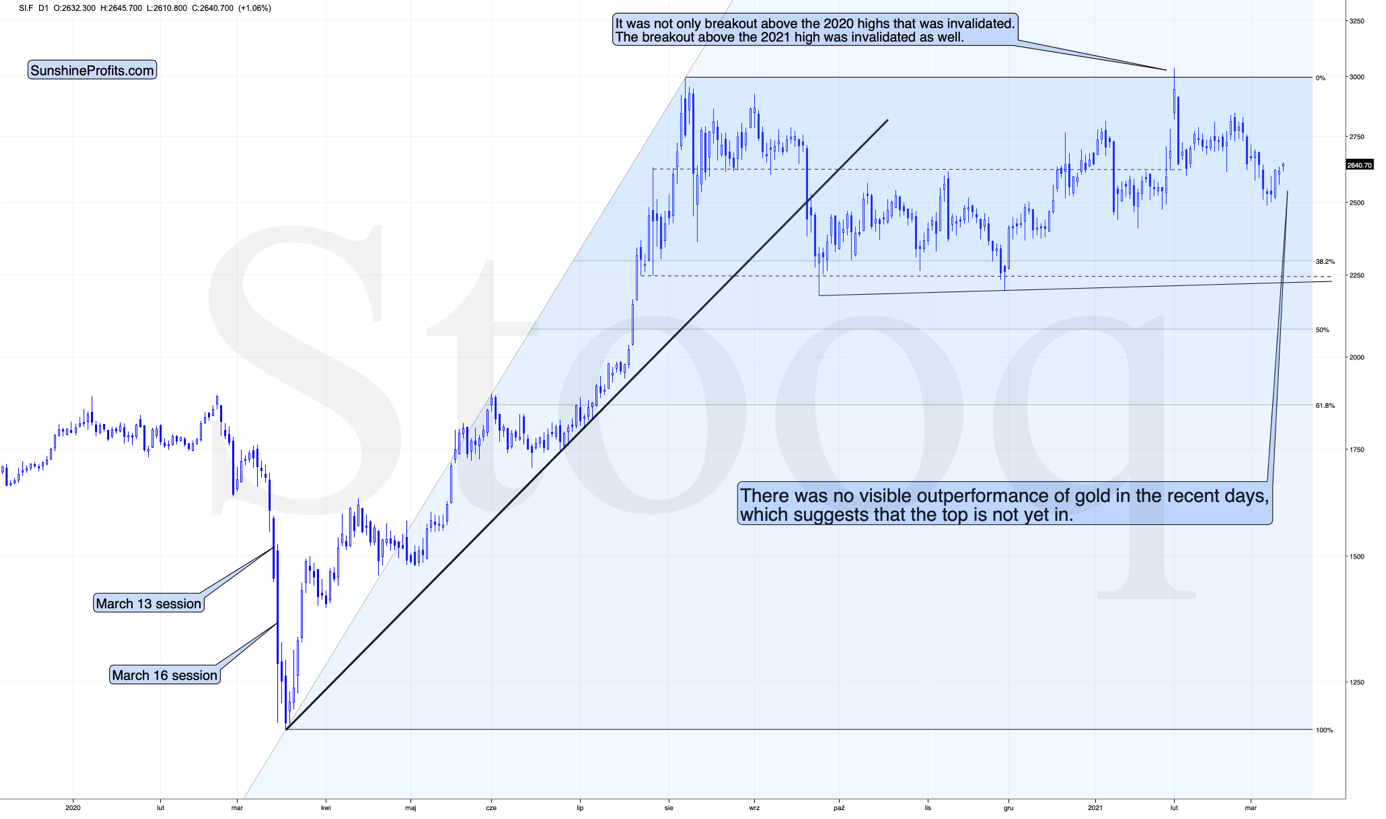

Let’s take a look at the silver market.

The thing that I want to emphasize here, is that silver’s recent performance was… Average. This is informative, because silver tends to outperform gold in a visible way close to the top. Average performance means no outperformance, which in turn means that the top is likely not yet in.

Having said that, let’s take a look at the market from the more fundamental angle.

Fundamental Frailty

With the USD Index taking a breather, the PMs should continue their short-term shine.

However, with the USD Index poised to soar over the medium-term, the EUR/USD will play a significant role. For context, the EUR/USD accounts for nearly 58% of the movement in the USD Index. As a result, Europe’s fundamental underperformance should help ignite the USD Index’s fire.

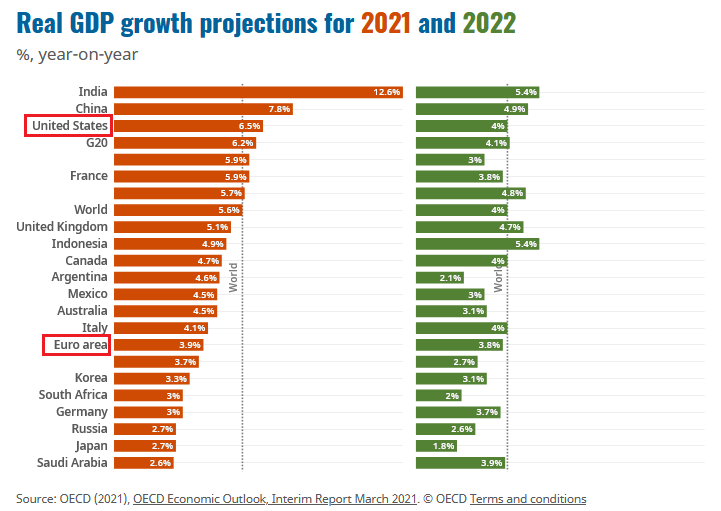

On Mar. 9, The Organisation for Economic Co-operation and Development (OECD) released its Interim Economic Outlook. And revealing what I’ve been writing about for over a month, the latest projections are dollar-positive and euro-negative.

Please see below:

If you analyze the chart above, you can see that the U.S. economy is projected to grow by 6.5% in 2021 and 4.0% in 2022. Conversely, the Eurozone economy is projected to grow by 3.9% in 2021 and 3.8% in 2022.

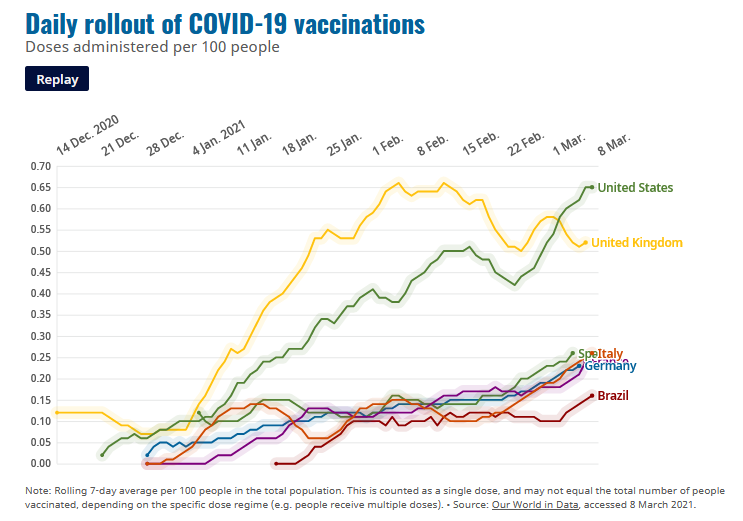

At the core of the expected divergence, daily COVID-19 vaccinations in Germany, France, Italy and Spain – Europe’s four-largest economies – lag the U.S. by a staggering margin.

What’s more, Joe Biden’s $1.90 trillion stimulus package is expected to have a profound impact on the U.S. economy. And the Eurozone? Well, not so much.

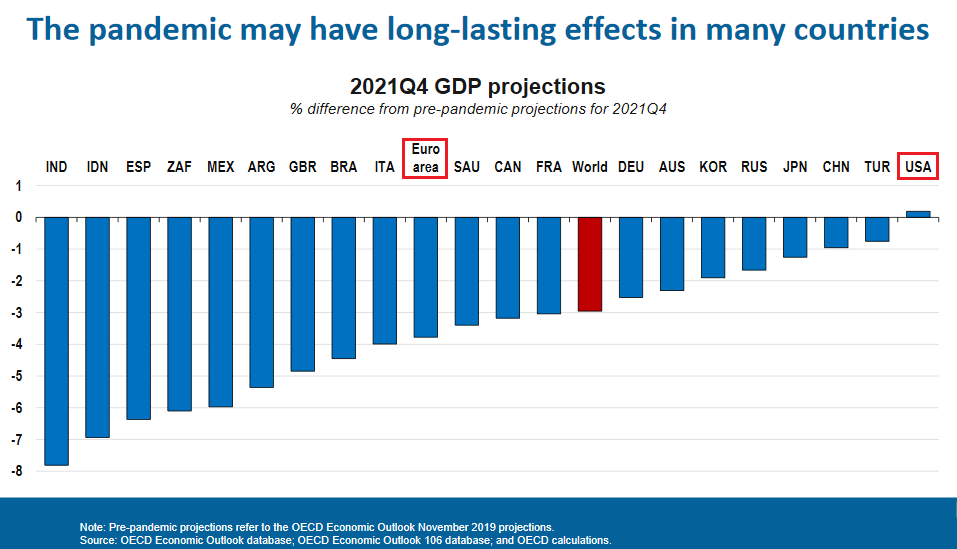

Furthermore, pandemic-induced scarring is expected to burden the Eurozone economy for some time. If you analyze the chart below, you can see that OECD analysts have reduced their Eurozone Q4:2021 GDP forecast by 4.0%. In stark contrast, the group has actually increased its U.S. Q4:2021 GDP forecast.

But because seeing is believing, notice how Eurozone economic activity does, and is expected to, lag the U.S. by a wide margin?

Source: OECD

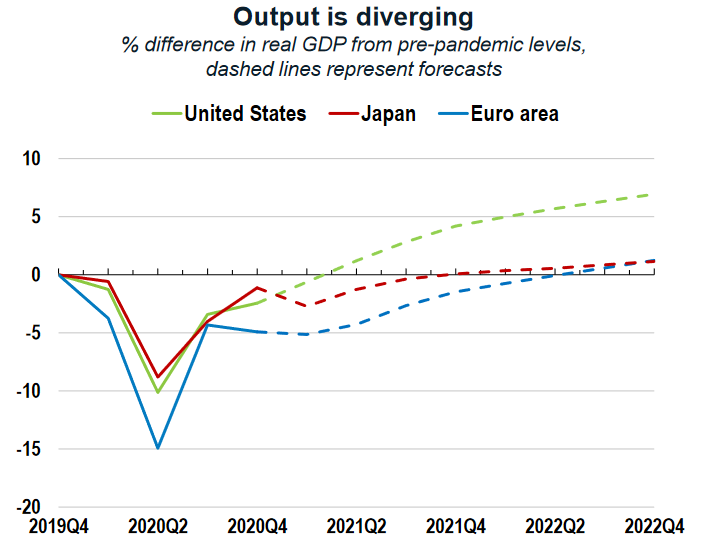

Source: OECDTo explain, the solid (and dotted) green line above depicts the performance of U.S. real GDP, while the sold (and dotted) blue line above depicts the performance of Eurozone real GDP. Representing historical data, if you focus on the two solid lines, you can see that the U.S. recovery is tracking well-ahead of the Eurozone. And because the dotted sections track OECD analysts’ projections, you can also see that the U.S. is expected to recoup its pre-pandemic GDP growth by roughly the second-quarter of 2021. Conversely, the Eurozone isn’t expected to recoup its pre-pandemic GDP growth until the second-quarter of 2022.

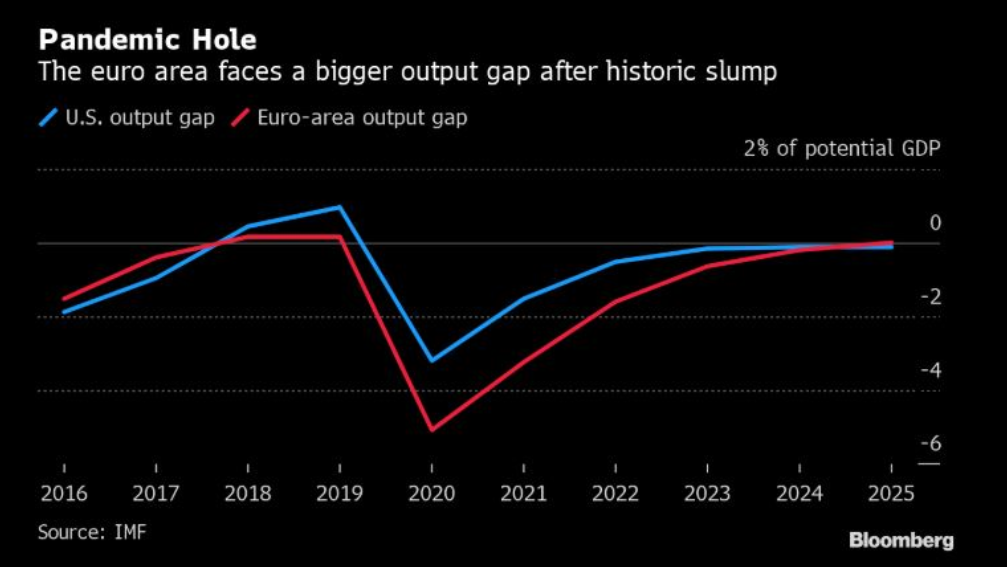

To that point, data compiled by Bloomberg is just as pessimistic.

Please see below:

To explain, an output gap is the difference between a region’s actual and its potential GDP. With the blue line above representing the U.S. and the red line above representing the Eurozone, you can see that the U.S. is expected to close its output gap by 2023. But lagging behind, the Eurozone isn’t expected to close its output gap until 2024.

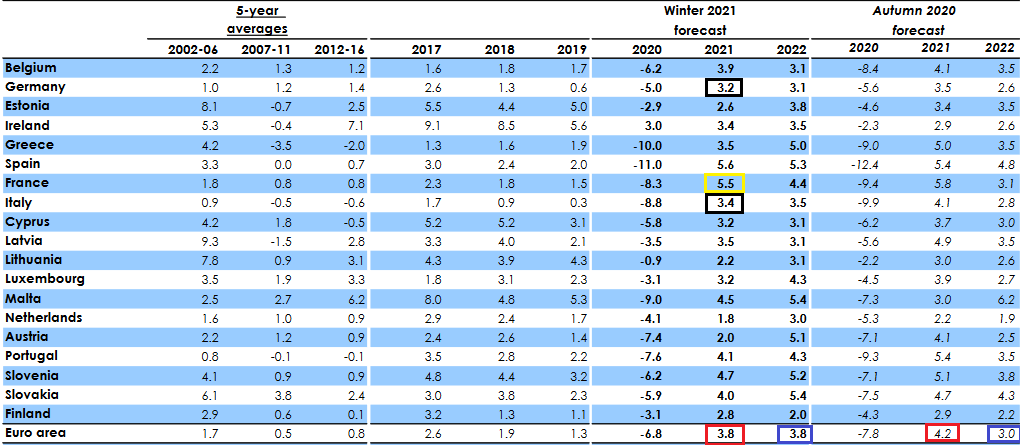

On a more granular level,The European Commission’s Winter 2021 Economic Forecast (released on Feb. 11) predicted that Eurozone GDP growth (3.8%) would be headlined by France’s outperformance in 2021.

On Feb. 17, I wrote:

The report forecasts that France (the yellow box below) – Europe’s second-largest economy – will deliver 5.5% GDP growth in 2021.

Source: European Commission Winter 2021 Economic Forecast

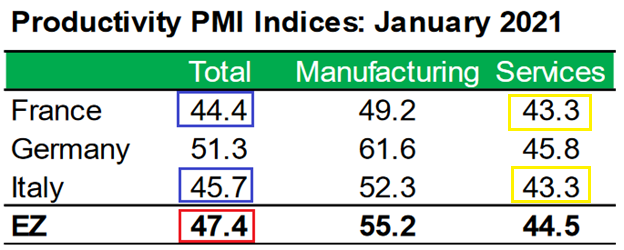

Source: European Commission Winter 2021 Economic ForecastWith ambitious being an understatement, it was less than two weeks ago (Feb. 4) that IHS Markit’s Eurozone Productivity PMI fell for a third-straight month (to 47.4 in January) and declined at its fastest pace since June. More importantly though, the report cited France and Italy’s service sectors as the main weak spots (the yellow boxes below).

Source: IHS Markit

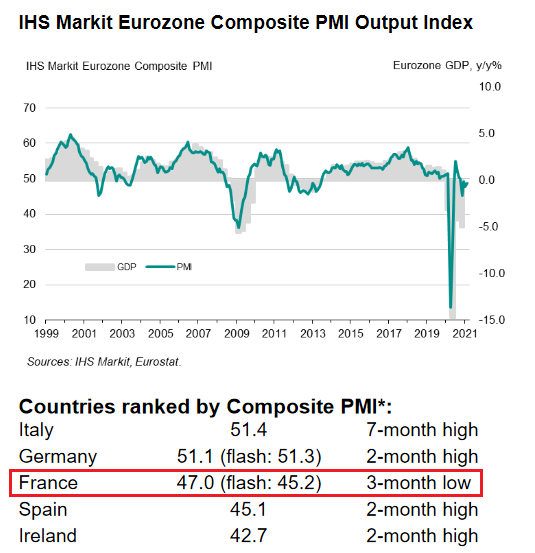

Source: IHS MarkitAlso contradicting the projection, IHS Markit’s Eurozone Construction PMI report (released on the same day) read that “France posted the steepest rate of contraction.” With that in mind, does it seem likely that France will outperform 18 of 19 European countries in 2021?

And with the latest data not instilling any more confidence, February’s IHSMarkit’s Eurozone Composite PMI (released on Mar. 3), revealed that “overall declines were recorded … with Ireland again recording the sharpest contraction, followed by Spain and then France.”

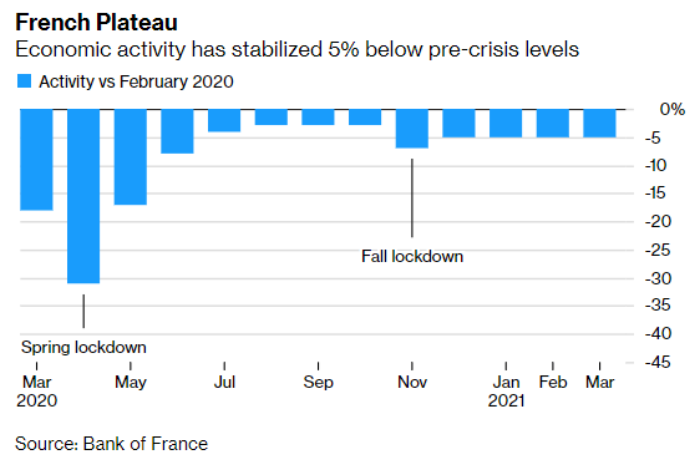

If that wasn’t enough, data from the Bank of France confirms that the French economy has plateaued – at 5% below pre-pandemic levels – since November.

Please see below:

Also raising alarm bells, I warned on Feb. 19 that the European banking sector remains on high alert.

If you analyze the chart above, you can see that S&P 500 banks (the white line) have traded sharply higher since September. In stark contrast, European banks (the yellow line) have struggled to keep pace.

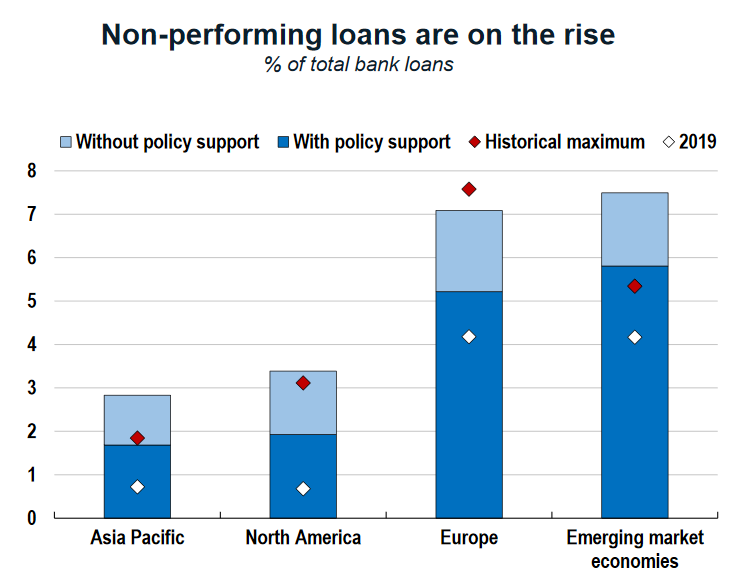

And able to see the forest through the trees, European officials warned on Feb. 15 that the Eurozonecould be on the verge of“wide-scale corporate distress.” In a document presented to European finance ministers, officials highlighted that 25% of European businesses were in financial trouble prior to the New Year. And with the “underlying deterioration” masked by government assistance, banks’ loan loss provisions may have underestimated the potential impact.

And hitting the nail on the head, the OECD’s report shows that more than 7% of bank loans across Europe are considered nonperforming. For context, a nonperforming loan (NPL) means that a borrower has failed to make interest and/or principal payments over a period of 90 or 180 days (usually). The International Monetary Fund (IMF) also considers a loan nonperforming when it’s been delinquent for less than 90 days, but there is significant uncertainty regarding future payments.

Please see below:

Source: OECD

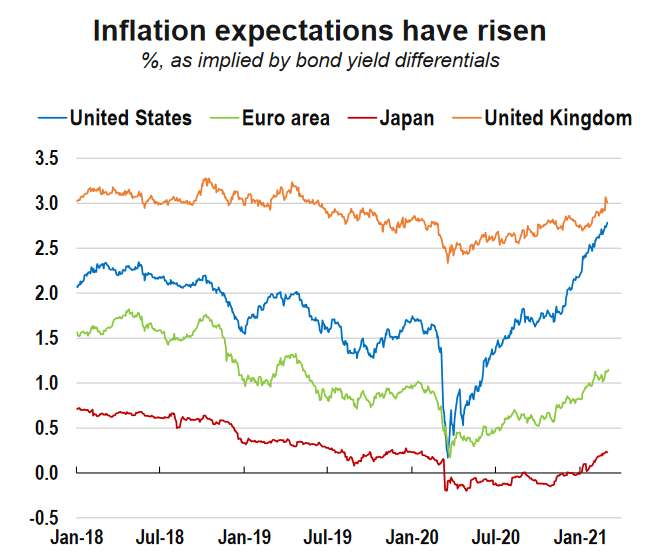

As another negative for the euro, European inflation expectations continue to lag the U.S. Creating a domino effect, I’ve noted on several occasions that higher inflation is a precursor to higher interest rates. And because higher interest rates are a precursor to a stronger currency, U.S. inflation outperformance is bearish for the EUR/USD.

Source: OECD

Source: OECDTo explain, the green line above tracks inflation expectations in the Eurozone, while the blue line above tracks inflation expectations in the U.S. As you can see, the blue line has moved sharply higher, while the green line has delivered a modest uptick. Thus, rising Eurozone interest rates remain extremely unlikely.

In conclusion, fundamental headwinds continue to shake the EUR/USD. And despite bouncing over the last two trading days (after declining for six of the previous seven), the fundamental divergence should catch up to the currency pair over the medium-term. Moreover, given its significant influence over the USD Index, a material decline in the EUR/USD should propel the basket back above 94.5. As a result, the PMs strong negative correlation with the USD Index clouds their medium-term outlook. For now, though, we still have time to enjoy the PMs short-term upswing.

Letters to the Editor

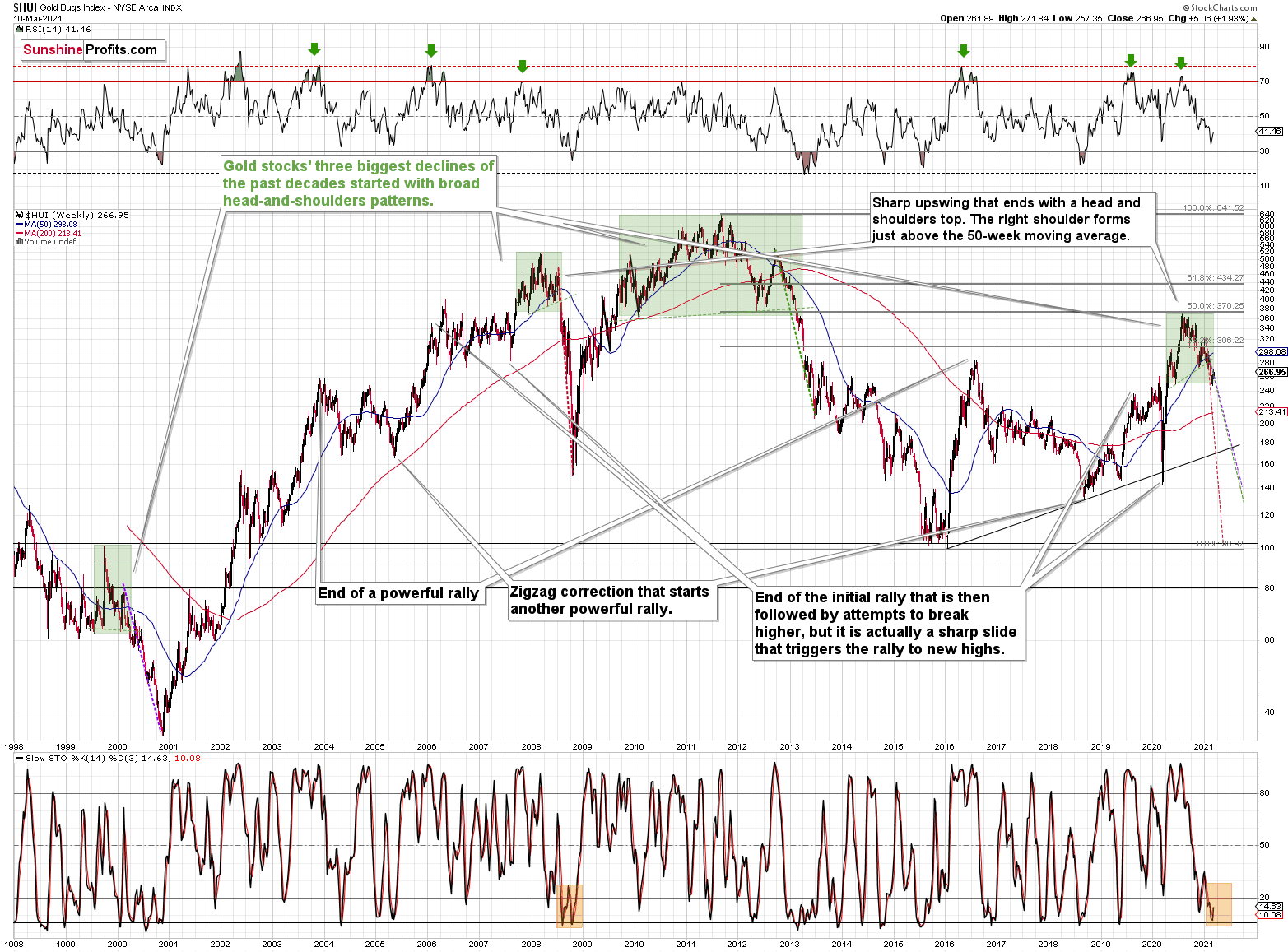

Q: I am a premium member and I saw the following chart. You should probably send it to PR so he can see it. I have a feeling that it is geared towards him.

A: Thank you. Naturally, technical analysis is subjective in general, and while some analysts might see certain patterns, others might not. You already saw the GDX chart earlier today, so I’ll include the long-term HUI Index chart (another proxy for the mining stocks that’s been around longer than the GDX) below for you to check for yourself if you see the head and shoulders patterns as the starting points of massive declines – or not. I marked them with green rectangles. In each case, the pattern was characterized by higher lows, so the necklines were moving higher.

The 1999 – 2000 H&S pattern is not a classic example of the pattern, as the tops are relatively pointy instead of being round, but the 2007 – 2008, 2009 – 2013, and the recent 2020 – 2021 formations are crystal-clear to me. The market seems to agree too, as the most recent performance of gold stocks is very similar to the follow-up of the previous three big H&S patterns. I marked the post-pattern declines with dashed lines of different colors – the HUI Index is moving right between them, which means that it’s already following the analogy to the previous declines.

Q: Trading is hilarious. I have the GDXJ pinned at a resistance of 46.75, with a downside target of $42.5. I’m expecting the selling tonight, but we will see. No capitulation and no catalyst for this to be a bottom. We should know something by USA open.

A: In my opinion the GDXJ will move to 42.5 (and perhaps pause there and then decline further) but not before moving a bit higher first. I don’t think that the final bottom for this medium-term decline was in yet, but I also don’t think that the corrective rally is over.

In case of the GDXJ, the situation is somewhat odd, because this ETF – by itself – didn’t move to an important support level before moving back up. However, it’s so closely tied to the performance of senior miners (GDX) and (to a much smaller extent, but still) the general stock market. Since both moved higher recently (the GDX moved to an important support, after all), GDXJ had little choice but to rally as well.

Q: Your accuracy on the movements in the PM sector is just uncanny. It seems that no one, a week ago, believed that gold could ever again breach $1700. I have a general question. Since your analysis points to gold possibly testing 1350, I would assume that the equity markets are in for a big crash. If gold is down 30% from its 2020 highs, could one assume a 50% correction in the equities markets? Also, could silver retest the lows from March 2020?

A: Thank you for the compliments! Indeed, very few people thought that gold would move below $1,700. Now, very few think that it could (ever) go below $1,500.

Yes, I think that gold might (!) test $1,350, but I view $1,450 and the 2020 bottom as a more likely target.

And yes, I think that equities are in for a big (really big) crash. I think that the equities will move to their 2020 lows and then move below them. Yes, I know that it sounds crazy, in a world when the stock market used to only go up, but… The cycle seems to have changed. We are likely in the very early part of the Kondratiev winter after a very long autumn. We’ll likely see a confirmation (or invalidation) of the above soon.

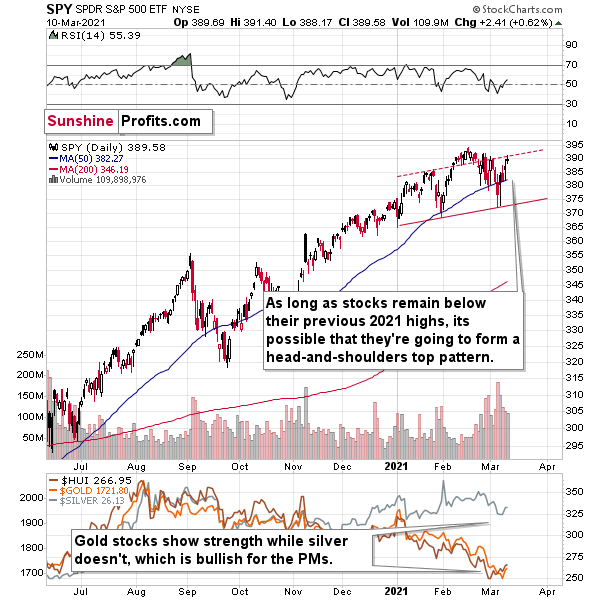

If stocks remain within the head and shoulders pattern and break below its neck level in the upcoming weeks, it will be a very good indication that another huge downswing is already underway. This seems likely in my view, as a rallying USD would be making the U.S. exports less competitive, and I definitely expect to see the former.

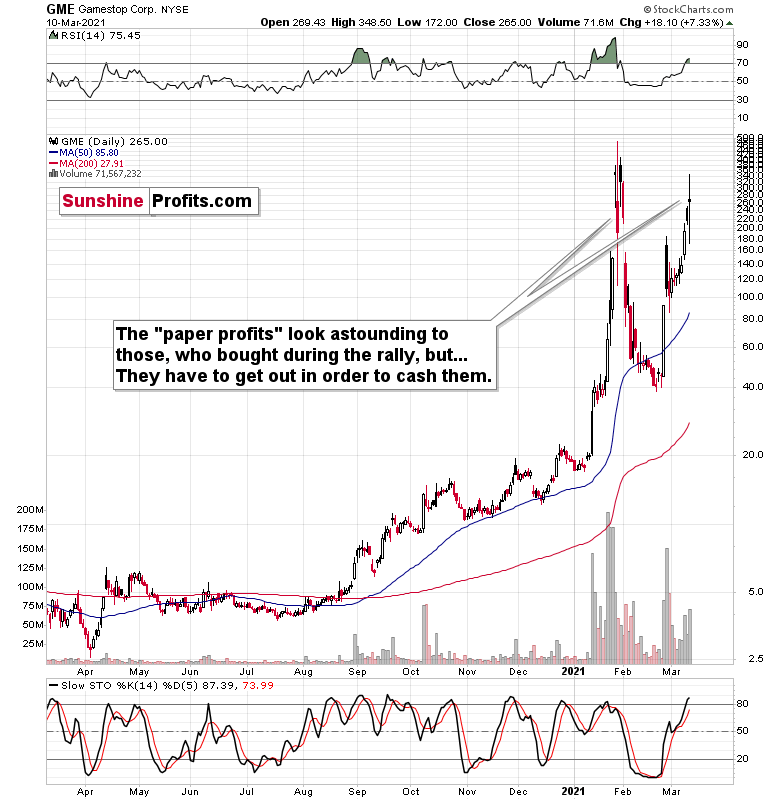

The very strong performance of the Gamestop stock emphasizes the fake nature of the recent upswing in stocks. This company’s fundamentals are not favorable at all and yet people flock to the stock based on its recent popularity. This could be the effect that the recent round of stimulus had (or expectations thereof – people already bought knowing that the checks are coming), and whether this is the case or not, it seems that it is the general investment public that is making these purchases. And this is the group of investors that is entering the market at the end of the bull market.

Regardless, a 50% decline in the market is not out of the question, but I doubt that it would happen quickly, without periodic corrections. And I would like to emphasize that I expect the precious metals sector to decline along with stocks only initially. That was the case in 1929, in 2008 and in 2020 (miners bottomed before the S&P did). Based on the analogy to the past cases (especially the first two), I expect the PMs to bottom about 3 – 3.5 months after the stock market tops. If the top was in the middle of February, then the final bottom in the PMs should form in mid or late May.

And yes, silver could re-test its lows from March 2020. As I emphasized previously, the silver market tends to catch up big-time in the final part of the move. That’s also what it did in March 2020 – miners bottomed when silver was only (approximately) halfway done declining. In fact, the powerful slide in silver is one of the things that I expect to see as a confirmation that the final bottom is in. This time the silver catch-up could be particularly profound due to the big number of individual investors that bought silver when it was popular (see #silversqueeze) in late January and early February. Since those investors likely bought based on short-term emotions and based on only limited research, they are likely to get out of their holdings when prices decline and the emotions toward the PMs get negative, thus adding further fuel to the bearish fire.

Q: Hi Przemyslaw. Once again you are spot on with your Gold and Gold miners daily analysis. Thank you for the follow up from Thursday's 3/4/21 trading alert. On Friday 3/5 I went long on NUGT and GDX. I WAS SO HAPPY WHEN I GOT UP TODAY AND SAW A $5.00 GAIN ON NUGT RIGHT AT THE OPEN. Your exit price targets on gold at $1770, and gold miners at $33.92 to $34.27 are so helpful I can't thank you enough. In addition, your call on the US Dollar dropping is amazing...it did just what you said, topping out near 92.55 and breaking below 92.00 at the close. I'm your biggest admirer; You are unbelievable.

A: Thank you! I’m incredibly flattered by the compliments and even more happy to know that people are profiting from the analyses. A word of caution might be useful here - please remember that I can (and definitely will) be incorrect about the market in the future as it’s impossible to predict it in each and every case. It might be tempting to put a lot of capital in the market after a series of successful trades, but please keep in mind that it’s even more important to be able to continue to trade even after a few bad calls. In other words, it’s critical to keep the position sizes reasonable (you will find more details in the “Position Sizes” part of the Gold & Silver Portfolio Structuring report).

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks.We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFAFounder, Editor-in-chief -

Gold, Miners: How Long Will Short-Term Rally Last?

March 10, 2021, 9:36 AMGold rallied, gold miners soared to new March highs and the USD Index finally moved lower; and most likely, these price moves are not yet over.

The precious metals market finally moved yesterday (Mar. 9) after providing us with bullish indications for quite a few days. Let’s jump right into charts and examine the details, starting with the part of the precious metals market that showed particular strength – mining stocks.

Figure 1 - VanEck Vectors Gold Miners ETF (GDX)

Even though gold moved lower in early March, gold miners stopped declining after reaching my target area based several techniques – most importantly the 50% Fibonacci retracement based on the entire 2020 rally, and the previous lows and highs. Just as miners’ relative weakness had previously heralded declines for the entire precious metals sector, their strength meant that a rally was about to start. And that’s just what we saw yesterday (Mar. 9).

Ultimately, it seems that the above corrections will result in the GDX ETF moving to about $34 or so.

The resistance levels in the $34 - $35 area are provided by:

- The late-February 2020 high

- The rising neck level of the previously completed head and shoulders pattern

- The analogy to how big miners’ correction was in April (assuming that the mirror similarity continues)

- The declining blue resistance line

- The 50-day moving average

Additionally, please note that the last few local tops were accompanied by RSI at about 50. The latter is currently below 45, suggesting that this rally has more potential, but that it’s not particularly extreme.

The confirmation that the top is indeed in might come from the volume. Please note that the last three times when we saw really important tops, the GDX rallied on particularly strong volume. If we see something like that within the next 5 trading days or so (quite likely on Monday or close to it), we’ll have an even bigger chance of catching the reversal.

Consequently, the GDX is likely to form a top in the above-described area.

After breaking below the head-and-shoulders pattern, gold miners would then be likely to verify this breakdown by moving back up to the neck level of the pattern. Then, we would likely see another powerful slide – perhaps to at least $24.

This is especially the case, since silver and mining stocks tend to decline particularly strongly if the stock market is declining as well. And while the exact timing of the market’s slide is not 100% clear, the day of reckoning for stocks is coming, and it might be very, very close.

As I explained previously, based on the similarities to the 1929 and 2008 declines, it could be the case that the precious metals sector declines for about three months after the general stock market tops. And it seems that we won’t have to wait long for the latter. In fact, the next big move lower in stocks might already be underway, as the mid-Feb. 2021 top could have been the final medium-term top.

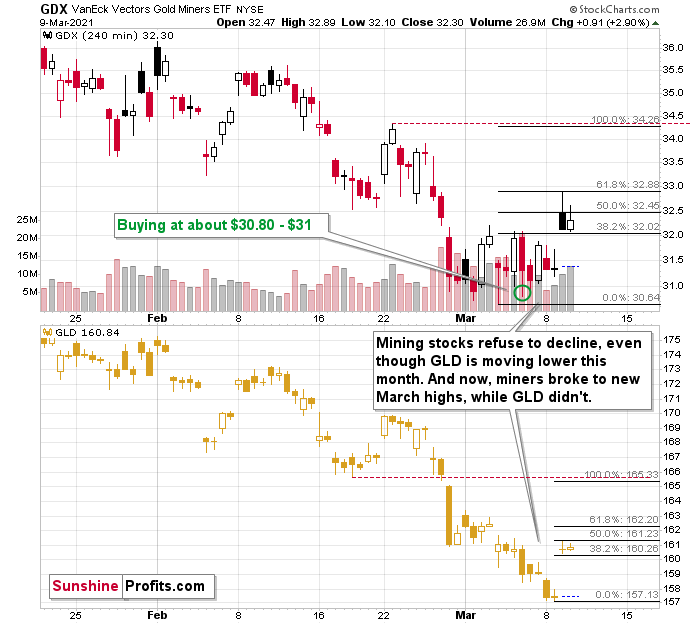

Let’s consider what the GDX and GLD did on an intraday basis yesterday.

Figure 2 - VanEck Vectors Gold Miners ETF (GDX) and Gold ETF (GLD) Comparison

As I already wrote, mining stocks rallied to new monthly highs, and the above 4-hour chart (each candlestick represents 4 hours of trading) makes it crystal-clear that the late-February bottom was the moment after which miners stopped declining and started to trade sideways. Gold (here: the GLD ETF, which I’m using to have an apples-to-apples comparison – both ETFs trade on the same exchange) continued to decline in March. Well, to be precise, miners did form new yearly lows in March, and we went long almost right at one of those intraday lows, but the moves were not significant enough to really change anything.

So, since miners no longer wanted to decline, and there were only two other things left for them to do: either nothing or rally.

They had been doing nothing for several days, due to the lack of bullish leadership in gold. They just got this leadership yesterday, and they soared.

Now, let’s keep in mind what I wrote in yesterday’s intraday Alert – namely, that mining stocks tend to rally particularly well in the initial part of the upswing, and then they underperform during the final part of the rally. So, when gold is above $1,750 or so, miners might already be rallying to a limited degree. Consequently, miners might rally above $34.27, but that is far from being certain. They might actually rally slightly less – perhaps to exactly $34 or so.

I applied the Fibonacci retracement levels to the above chart, but I actually used them as Fibonacci extensions. My current upside target for gold is at about $1,770 (which corresponds to about $166 in the GLD ETF) and it’s at about $34 for mining stocks (GDX ETF). The Fibonacci extensions emphasize that if both targets were to be reached, then it means that gold so far rallied (intraday) about half of its entire rally, while mining stocks rallied (intraday) about 61.8% of their entire rally. This perfectly fits miners’ tendency to outperform in the initial part of a given move, which makes both price targets more reliable.

Having said that, let’s move to gold.

Figure 3 - COMEX Gold Futures

Gold rallied strongly after bottoming right in the middle of my target area and after moving almost right to its June 2020 bottom, and after almost doubling its initial January decline. Yesterday’s rally also meant invalidation of the brief breakdown below the 61.8% Fibonacci retracement level based on the entire 2020 rally. Thus, the very short-term trend is up.

Please keep in mind that the upswing might be relatively short-lived – perhaps lasting only one week or so. There’s a triangle-vertex-based reversal point on Monday, so it wouldn’t be surprising to see an interim top at that time, especially considering that:

- The triangle-vertex-based turning points have been working particularly well in the recent past – they marked the January and February tops.

- The corrective upswings during this medium-term decline (especially in mining stocks) often took about a week to complete – at least the easy part of the upswing took a week.

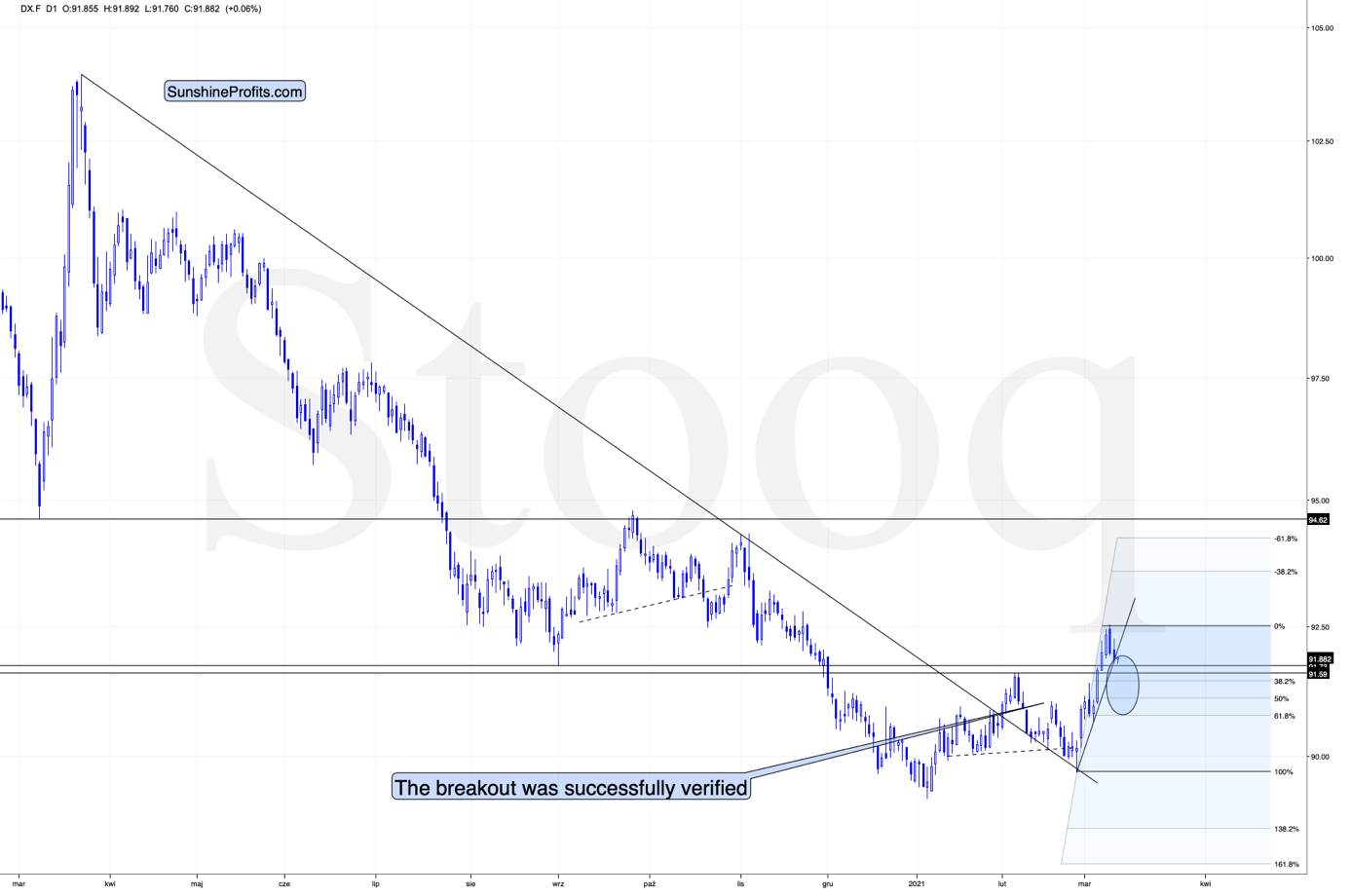

The USD Index has been rallying relentlessly – just like in 2018 – in the last couple of days, but a quick pullback would not be surprising. In fact, it seems that one is already underway.

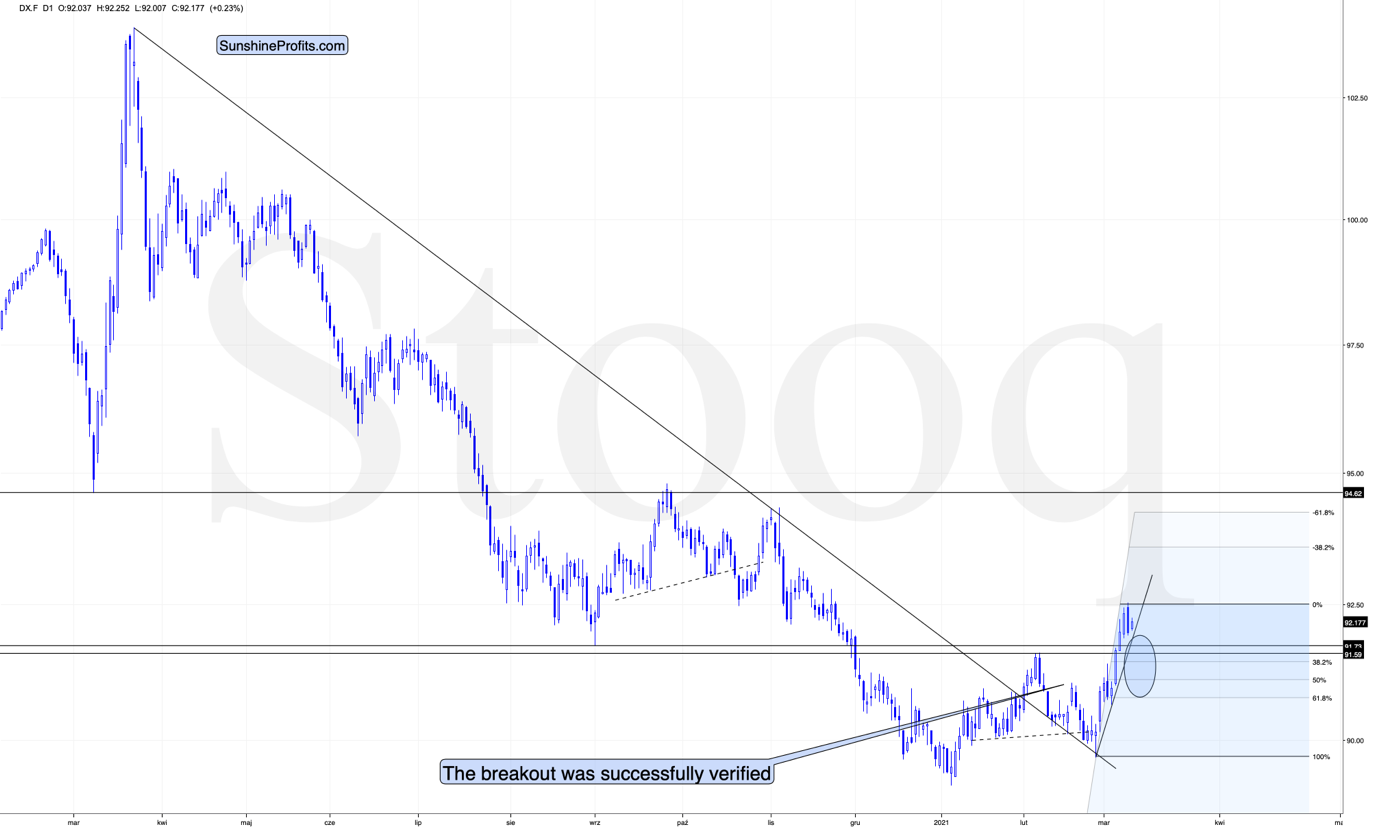

Figure 4 - USD Index (DX.F)

On March 8, the USD Index had closed above its lowest daily closing price of August 2020 (92.13), but yesterday, it closed back below this resistance. This means that we just saw an invalidation of the breakout – which is a bearish sign for the short term.

How low could the USD Index move during this pullback? Not particularly low, as the similarity to 2018 implies a rather unbroken rally. The February 2021 high of 91.6 seems to be a quite likely target, but we might see the USDX move a bit lower as well – perhaps to one of the classic Fibonacci retracements based on the recent upswing – lowest of them (the 61.8% one) being at about 90.8.

This pullback might trigger a question about the validity of the analogy to the 2018 rally, which seems to have taken place without any interruptions.

Figure 5

The analogy seems to remain intact when looking at it from the long-term point of view. Let’s keep in mind the recent decline was a bit sharper and it took less time to complete.

The 2017 – 2018 decline took 387 day (between the top and the first low) and then there were 82 days between the initial and the final low (21.19% of the decline).

This time, there were 269 days between the top and the first low. Adding 21.19% to this time, points to Feb. 12 as the "proportionately identical" bottom time target. The final bottom formed on Feb. 25 - just 9 trading days away from the analogy-based target. The analogy remains clearly intact.

“So, doesn’t it imply that there shouldn’t be any pullbacks until the USD Index rallies above 94?”

No. And this becomes obvious once we zoom in.

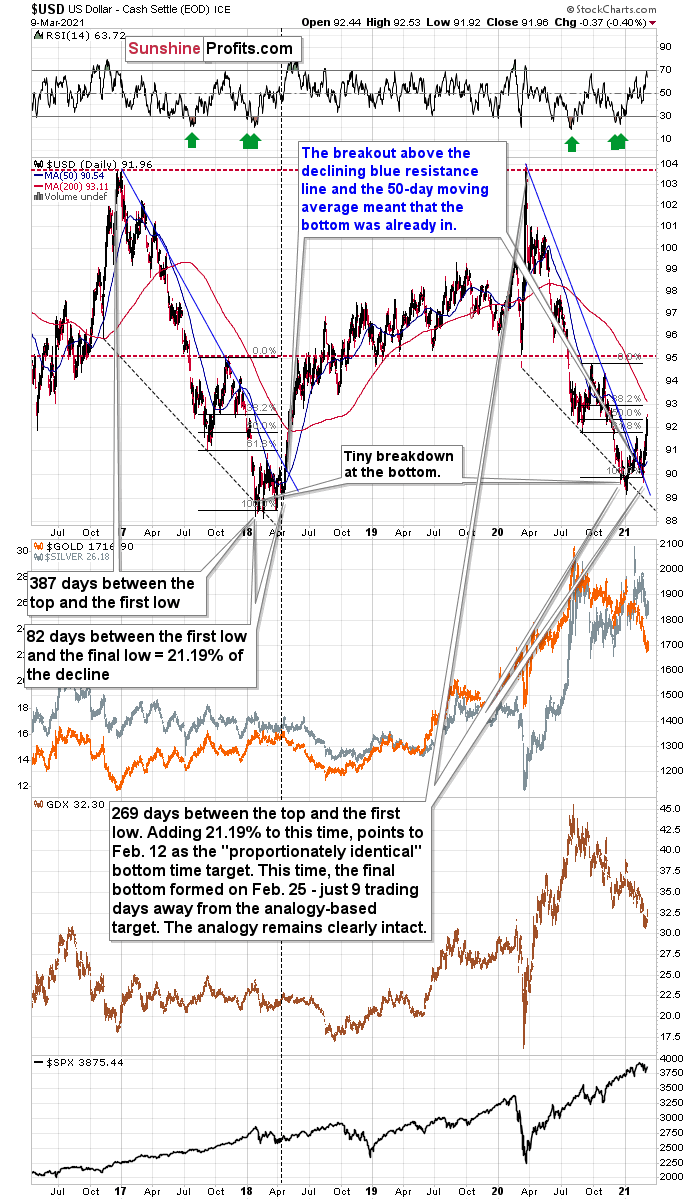

Figure 6

You see, it’s not true that there were no pullbacks during the 2018 rally. There were, but they were simply too small to be visible from the long-term point of view.

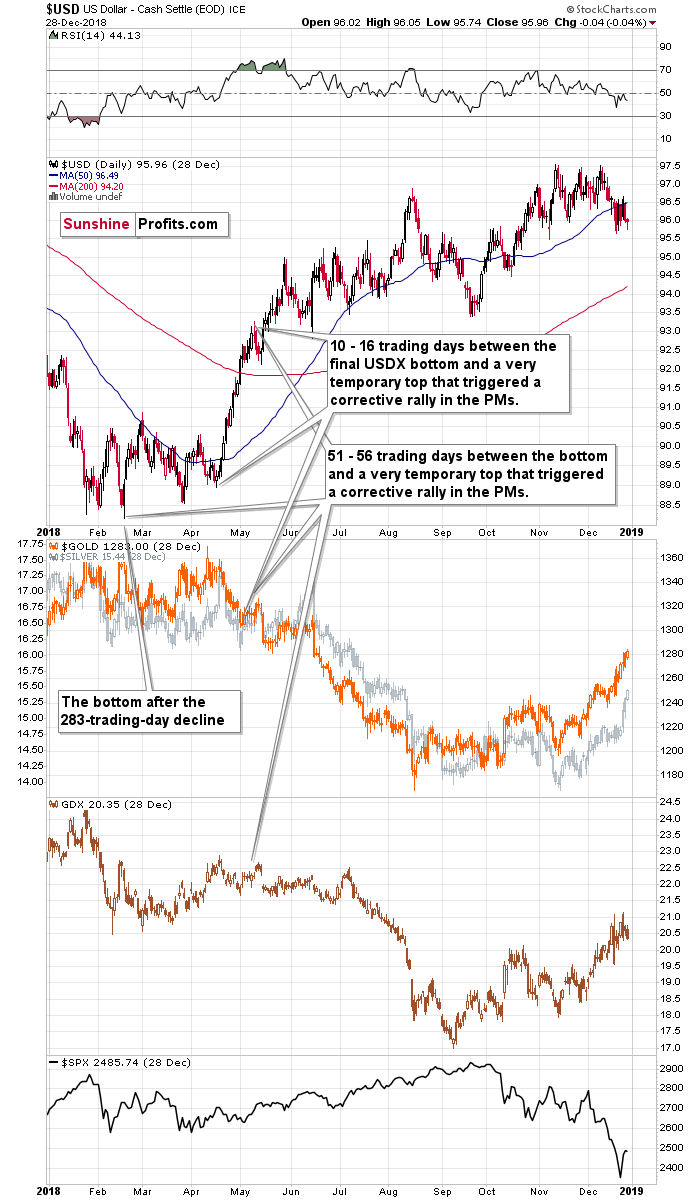

The first notable pullback took place in early May 2018, and it contributed to a corrective upswing in the precious metals market. To be precise, the USD Index declined after rallying for 56 trading days, but gold rallied earlier – 51 trading days after the USD Index’s final bottom. The USDX’s immediate-top formed 16 trading days after its final bottom, and gold’s bottom formed 10 trading days after the USD’s final bottom.

Comparing this to the size of the previous decline in terms of the trading days, it was:

- 51 – 56 trading days / 283 trading days = 18.02% - 19.79%

- 10 – 16 trading days / 283 trading days = 3.53% - 5.65%

Now, let’s examine the current situation.

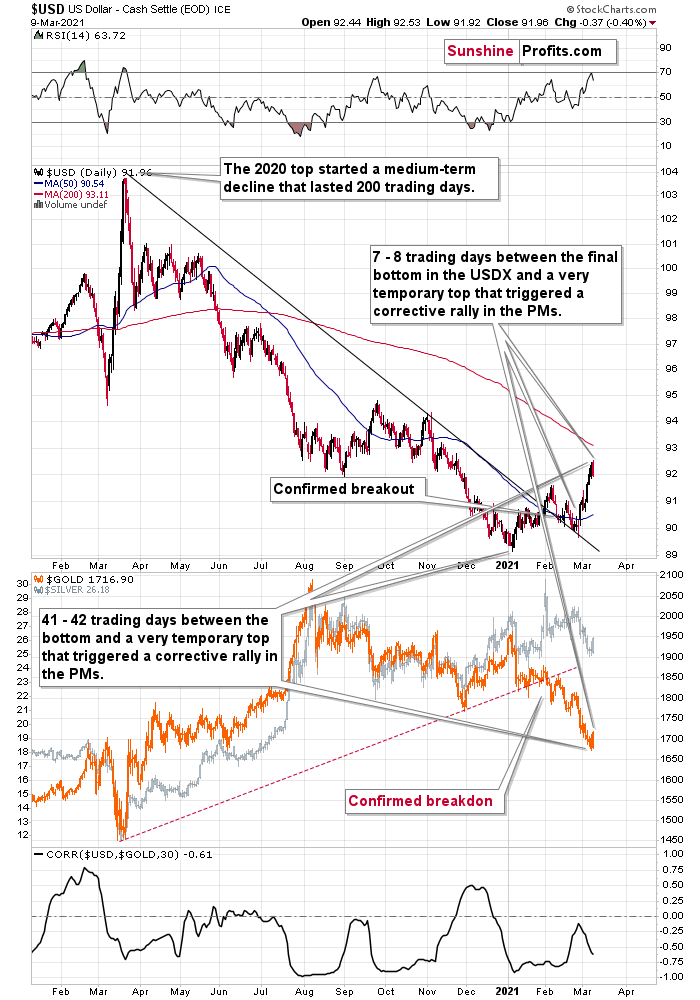

Figure 7

The preceding decline lasted for 200 trading days and there were 41 – 42 trading days between the final USDX bottom and the short-term reversals in gold and USDX. Comparing this to the final USDX bottom, we get 7 – 8 trading days.

Applying the previous percentages to the length of the most recent medium-term decline in the USD Index provides us with the following:

- 18.02% - 19.79% x 200 trading days = ~36 - ~40 trading days

- 3.53% - 5.65% x 200 trading days = ~7 - ~11 trading days

The above estimation of about 36 – 40 trading days almost perfectly fits the current 41 – 42-day delay, and the estimation of about 7 – 11 trading days almost perfectly fits the current delay of 7 – 8 trading days.

In other words, the analogy to the 2018 performance does not only remain intact – it actually perfectly confirms the validity of the current corrective upswing. Once again, it’s very likely just a pullback, not a big trend reversal.

Also, please note that back in 2018, the USD Index corrected after moving back above its mid-2017 lows and now we see the analogy to that – the USDX corrects after moving back above its mid-2020 lows. Back in 2017, the USD Index corrected to approximately its previous short-term high (the January 2018 high). Now, the February high is providing strong support at about 91.6 – that’s where this brief correction might end – on an approximate basis.

The above perfectly fits the scenario in which the precious metals market rallies on a very short-term basis (likely to about $1,770 in gold and about $34 in GDX), and then resumes its medium-term decline.

Letters to the Editor

Q: Dear Mr. Radomski,

I am currently long Silver. Can you please indicate the target price for silver or should I just exit when gold touches $1750?

Warm regards

A: Silver is the least predictable of the classic precious metals trio (gold, silver, and mining stocks) – at least at this time. The biggest problem with silver’s upside targets is that silver tends to overshoot resistance levels and create “fakeouts” (instead of breakouts) right before plunging. This means that using the tool that is so useful in case of other markets (resistance lines and levels) is often misleading in case of the white metal.

Still, I’ll attempt to provide a useful upside target for it.

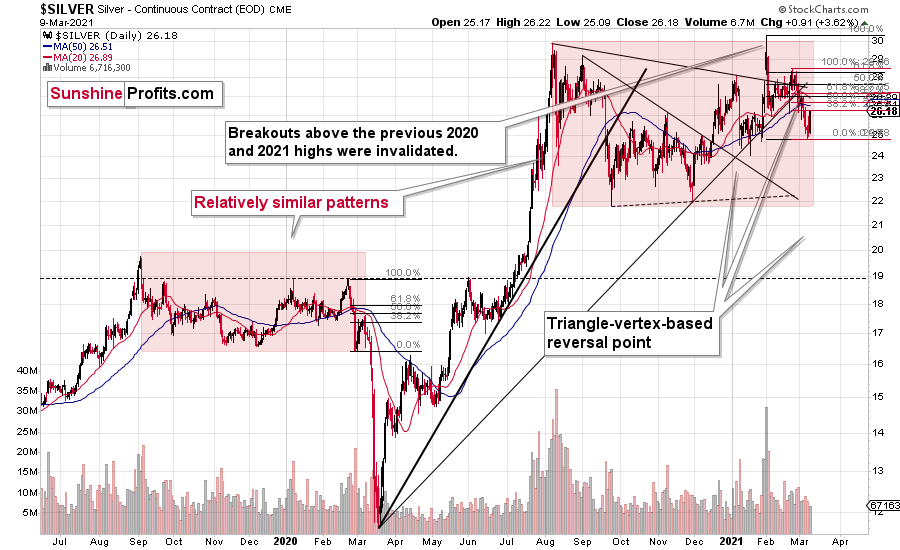

Figure 8

The recent silver price pattern is somewhat similar to what we saw between mid-2019 and early 2020. I marked them both with red rectangles. If this similarity continues to some extent, then we can expect silver move higher in the very near term. Back in March 2020, silver corrected about half of the recent upswing and it topped close to both: it’s 20-day moving average (marked with red) and the previous lows.

Silver’s 20-day moving average is currently at $26.89, and the mid-February lows are between $26.75 and $27.33 (I’m not counting the February 19 low, which seems relatively accidental). The 50% retracements are at $27.60 (if we take the 2021 high as the start of the decline) and $26.64 (if we use late-February top as the start of the decline).

Based on the above levels, it seems that silver’s next short-term top is likely to form in the $26.60 - $26.85 range.

But, if I had a long position in silver, would I wait until the above area is reached? No, I would focus on gold and exit the long position in silver, when gold moves to $1,758 ($12 below its upside target of $1,770). Gold seems more predictable at this time, so I’d use the above silver target area only as additional information. If silver is there when gold is at about $1,758, it would further validate this target.

Also, please note that the above is my opinion on the silver and gold market in general – it’s not investment advice / information directed to you only (I can’t tell you, specifically, what you should do, as that depends on more factors than just the outlook for the markets).

Q: Thank you for providing a valuable service with a genuine and considerate tone toward your clients.

It amazes me that PR is brilliant with analyses and yet takes the time to share his insights for others. It must take hours to compile the facts that confer a risk to reward short to medium term strategy, and then to write a comprehensive report at a level anyone can grasp. A lesser mortal – a selfish person – would keep the knowledge close to the chest and profit with less effort.

Please pass on my sincere respect and appreciation.

A: Thank you very much for your kind words – I’m very happy to see that you appreciate the results of my (and the entire Sunshine Profits Team’s) work. The fact that I can contribute to people’s investment successes and the realization of their plans and dreams is very satisfying and motivating. As well, longer reports are actually usually quicker and easier to write than the short ones, because when I notice something that’s particularly interesting to me (like the analogy in the USD Index to 2018 that I described today), I’m typing the analyses quickly naturally. It’s more difficult when the situation is boring from my point of view and there’s little worth commenting on (again from my point of view), but at the same time I realize that many subscribers will still want to read about the market on a given day – so I’m preparing the analyses on those days, anyway. Fortunately, it seems that the boring days for the precious metals investors are over.

Q: Hi PR. Regarding the typo on Mar. 8 – thank you for the correction. But I read your report word for word and then backwards. I knew what you meant – it’s all good. By the way, thank you. Its takes a great deal of trust to part with your hard earned dough on somebody else’s advice ( for me that's the case anyway ). I've been watching gold go down like a rock falling in water, and it was difficult this time to go long. But I did and spread my coin amongst three Aussie Gold miners for the counter trend rally. Catalyst Metals asx Cyl, Perseus PRU and Ramelius resources RMS. I am learning from you and your team. Thanks a million.

A: Thank you. I’m very happy to read that you’re benefitting from my analyses. It might be more difficult to profit from the brief price moves in the non-US exchanges as the currency price moves could be a relatively important factor with regard to the total rate of return. Still, it seems to me that these three stocks would be likely to rally along with the GDX in the next several days.

Q: Hi PR / Team

Thanks for the update, I'm out of this countertrend rally as soon as Gold reaches $1750 assuming it’s in Australian time. I can only trade between 10 am and 4 pm.

A: If your broker allows this, it might be a good idea to enter a limit sell order that could be realized also outside of the regular trading hours (in the pre-market / after-market trading) – this applies also to other exchanges, including the U.S. exchanges. That’s the kind of order that I have placed on my account.

Why? Because this might increase the chance of the trade being realized. Gold might move above $1,770, but it might do that when the U.S. markets are closed. Putting the profit-take price below this level is one of the ways in which I’m aiming to increase the chance of the trade being realized, but extending the time during which the trade could take place is another tool that would be useful in my view.

As always, the above is just my general opinion, not an investment advice or recommendation directed at anyone specifically.

Q: Phenomenal email - and exactly what I'd expect from a top-rate alert service.

Warmest Regards

A: Thank you! That’s our promise – to keep our subscribers updated, and that’s what we’re doing through not only the regular (and flagship) Gold & Silver Trading Alerts, but also through the intraday Alerts, if the situation seems to warrant it.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks.We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFAFounder, Editor-in-chief

Gold Investment News

Delivered To Your Inbox

Free Of Charge

Bonus: A week of free access to Gold & Silver StockPickers.

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM