Briefly: in our opinion, full (300% of the regular position size) speculative short positions in mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Welcome to this week's flagship Gold & Silver Trading Alert. As we promised you previously, in our flagship Alerts, we will be providing you with bigger, more complex analyses (approximately once per week) and it will usually take place on Monday.

Quite a few things happened recently, including the last several hours, so today's analysis will feature mostly new comments. However, there are still some parts of the analysis that didn't change in the previous days, and we will put them in italics.

The most important fundamental factor right now remains the Covid-19 pandemic and the serious economic implications. The expectations of the new stimulus, worries about the pace of economic recovery, and concerns about rising tensions between the U.S. and China have all contributed to gold's rally in the very recent past.

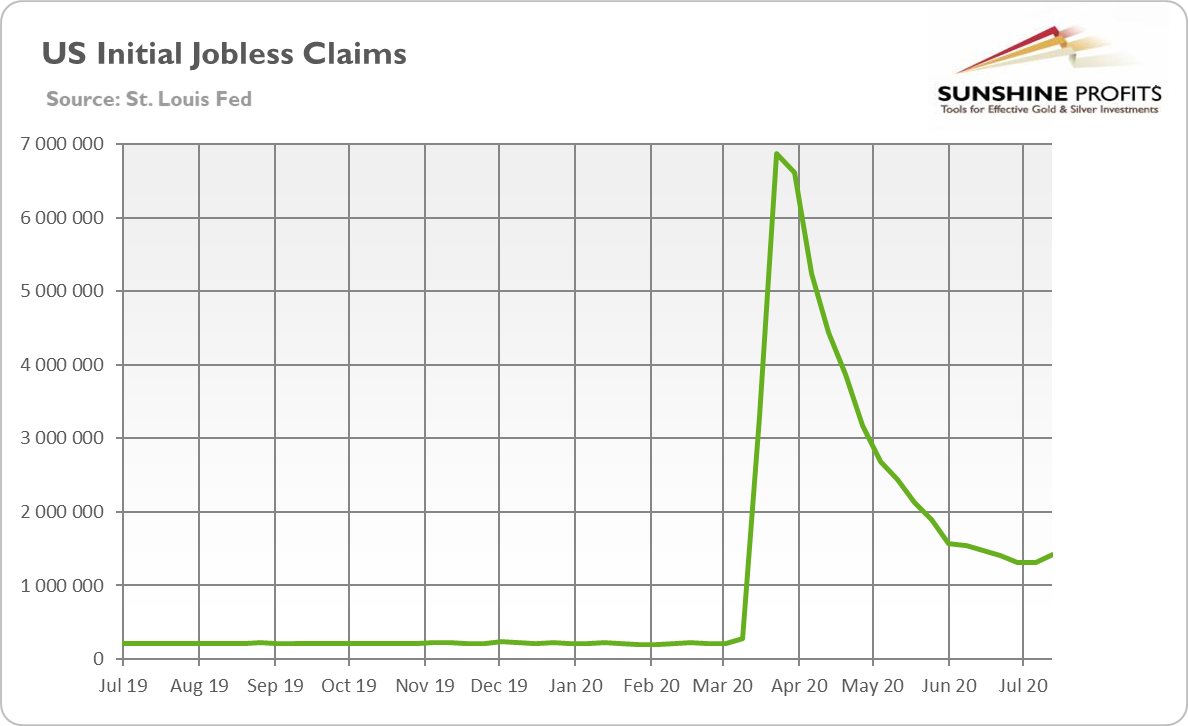

Please take a look at the chart below that presents the U.S. initial jobless claims. What do you see?

The number of people claiming unemployment benefits has recently risen. To be precise, in the week between July 11 and July 18, initial jobless claims increased from 13.1 million to 14.2 million. Instead of falling, they went up! Surely, we should never read too much into a single report. However, the increase in the number of applications for unemployment benefits is not something we should expect during firm, V-shaped recovery. The decline in initial jobless claims was already very sluggish, and the recent reversal in trend will only add to worries that the second wave of coronavirus is slowing down the economy.

In other words, the recovery could be more fragile and less vigorous than many people hoped for. Increased worries about the pace of recovery are positive for gold prices, but not necessarily in the very short term. The yellow metal should then gain not only as a safe haven but also thanks to the expectations that sluggish rebound would force the Fed and Treasury to another rounds of monetary and fiscal stimulus. Then again, please keep in mind that gold first plunged in March, when people got really scared of the economic implications.

Geopolitical concerns are another factor that supports gold prices right now. The already heightened tensions between the United States and China have recently escalated to a new level recently. Both superpowers are at odds on almost every front, from still unresolved trade wars to Taiwan, the Covid-19 pandemic, China's human rights abuses in Hong Kong and Xinjiang, and South China Sea. The latter issue has become a flashpoint amid increasing number of naval drills and encounters. On July 13, the U.S. Secretary of State Mike Pompeo signaled a tougher stance, rejecting in a statement most of China's claims to the South China Sea. He said:

We are making clear: Beijing's claims to offshore resources across most of the South China Sea are completely unlawful, as is its campaign of bullying to control them (...) The world will not allow Beijing to treat the South China Sea as its maritime empire."

And, last week, the U.S. ordered China to close its consulate in Houston, Texas, following accusations of spying. It was called by the Chinese Foreign Ministry an "unprecedented escalation" in recent actions taken by Washington. According to some analysts, the risk of an unplanned confrontation is growing as relations worsen very quickly, which could push both countries closer towards war. Such fears increase the safe-haven demand for gold.

The fundamental outlook has been very positive for gold recently, and this continues to be the case right now.

And yet, just as it was in March, it seems that the visible worsening in the economic situation might trigger a sell-off.

At this point we would like to quote what we wrote about the aspects of the virus scare and how the market reacts to them. In short, gold (and other markets) reacted when people started to strongly consider the economic implications and this topic was ubiquitous in the media.

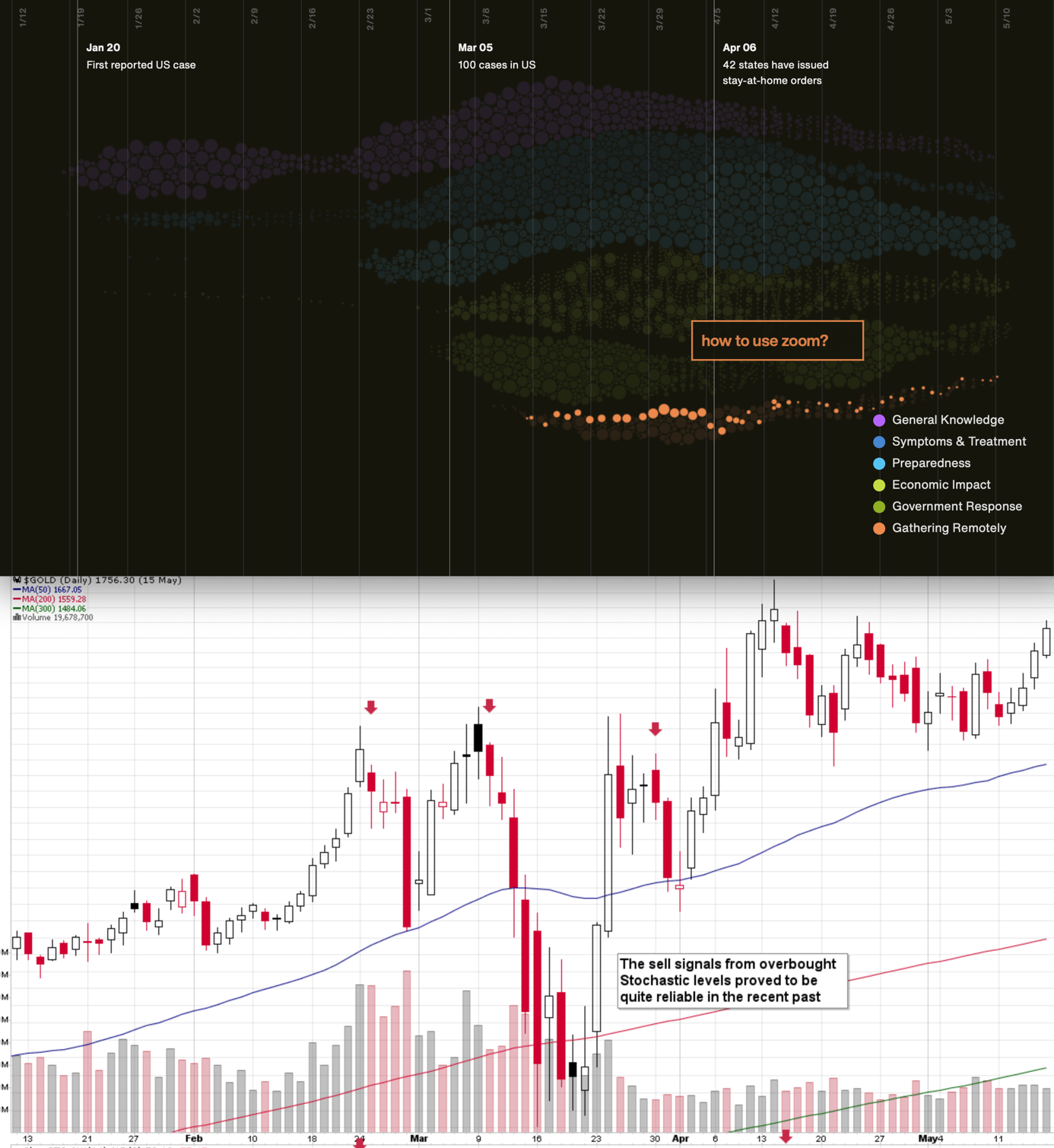

The particularly important factor for gold will likely be the economic implications of the second Covid-19 wave. How do we know that? Because we compared what people were searching for (online) with how gold prices shaped. There's a lot more data available on https://searchingcovid19.com/ but we'll focus on the chart that shows when people were getting interested in what aspects of the pandemic and we'll compare them to gold.

We aligned both charts with regard to time. The chart on the bottom is from Stockcharts.com and it features gold's continuous futures contract. The gold price (and the USD Index value) really started to move once people got particularly interested in the economic impact of the pandemic and in the government's response.

In the recent days (and weeks) the news is dominated by other issues. Once people start considering the economic implications of the second wave of this coronavirus, the prices would be likely to move.

The news coming from the Fed is positive for gold in the long run, but in the short term, they continue to indicate risk for the economy. This risk is likely to translate into lower stock values and initially gold is likely to slide given the above - just like it did in March.

All in all, gold is likely to rally far in the long run, but in the short run it's vulnerable to a sizable decline, when the economic implications of the pandemic's continuation become obvious to investors.

The surprising jump in the initial jobless claims might be the first crack in the dam of investors' optimism. And we can see something similar from the technical point of view.

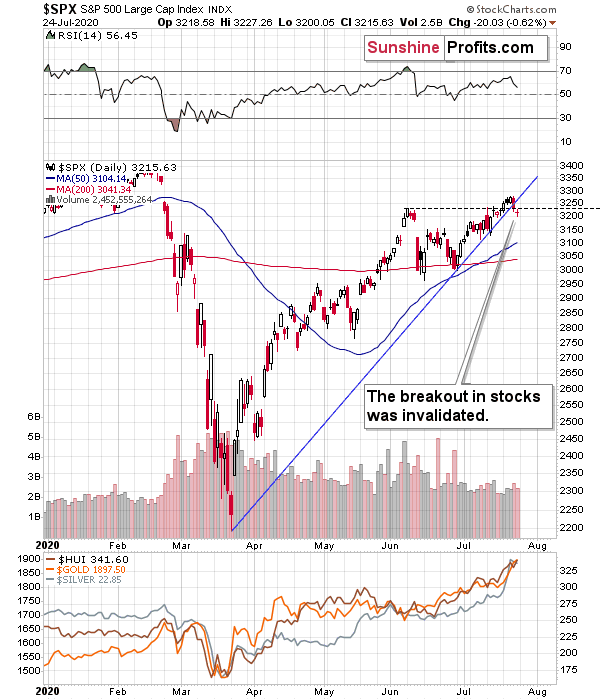

The S&P 500 invalidated the breakout above its June high and it also broke below (and closed the week) its rising blue support line. This breakdown is likely to indicate trouble for the stock bulls.

Besides, do you remember what happened in February when the S&P 500 lost its upward momentum? They plunged, and that was when tops in mining stocks and silver formed. Gold made another attempt to move higher but ultimately declined profoundly in the following days.

Back then, crude oil was relatively weak - and we see this weakness also this time. The black gold's upswing seems to have ended in June, but it made another attempt to move higher recently. It failed to move above the 61.8% Fibonacci retracement based on the entire 2020 decline and it seems to be ready to move lower shortly.

It appears that on one hand, everything that could have gone well for gold on the fundamental front, has already one well, and it already rallied, and on the other hand, we have many signals pointing to the situation being excessive. This means that as some of the bullish factors ease (perhaps temporarily) and investors get scared about economy's ability to really recover, gold is likely to correct significantly, before continuing its upward march.

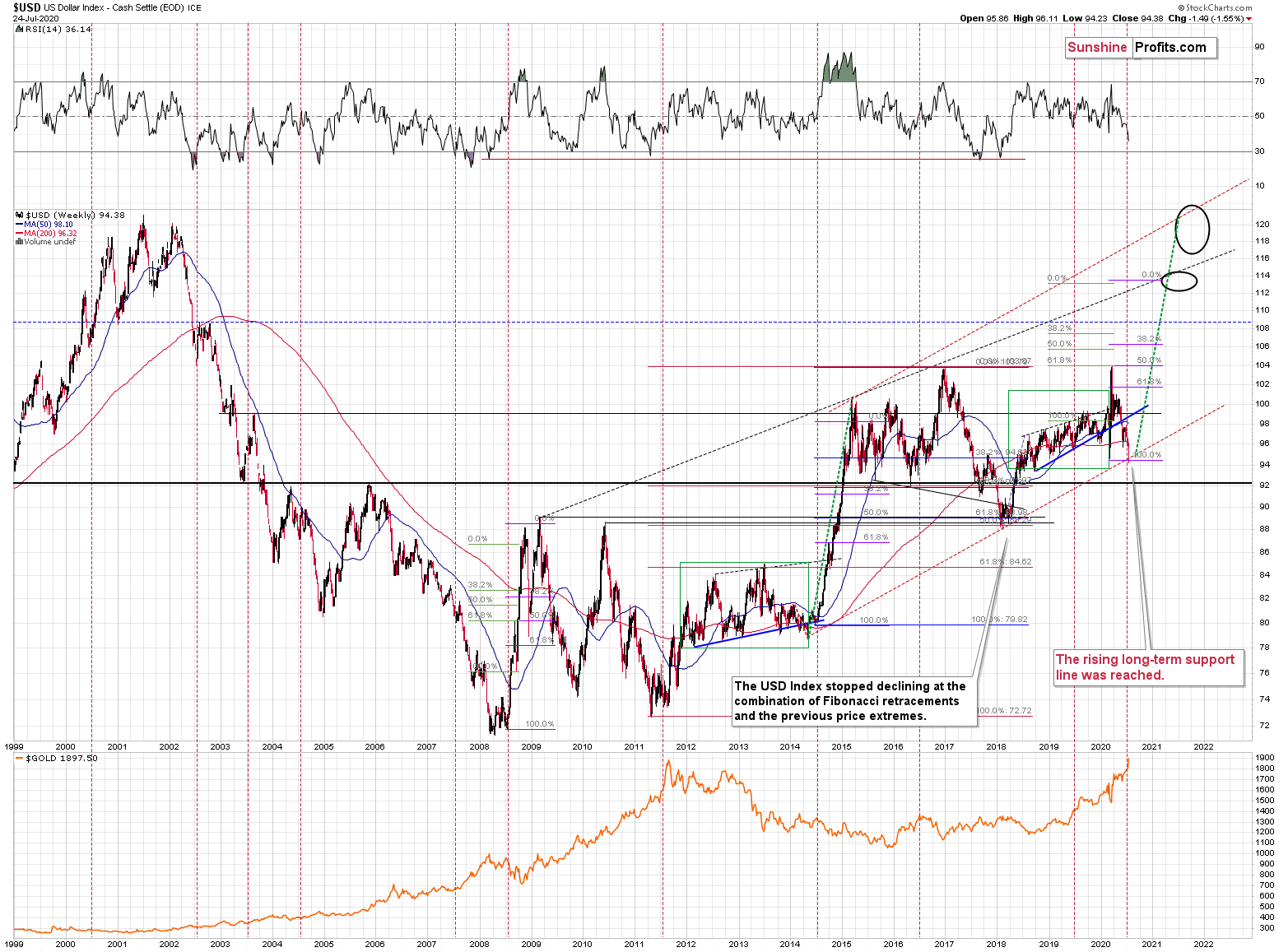

Speaking of indications pointing to the situation being excessive, let's take a look at the USD Index.

Remember when in early 2018 we wrote that the USD Index was bottoming due to a very powerful combination of support levels? Practically nobody wanted to read that as everyone "knew" that the USD Index is going to fall below 80. We were notified that people were hating on us in some blog comments for disclosing our opinion - that the USD Index was bottoming, and gold was topping. People were very unhappy with us writing that day after day, even though the USD Index refused to soar, and gold was not declining.

Well, it's the same right now.

The USD Index is at a powerful combination of support levels. One of them is the rising, long-term, red support line that's based on the 2014 and 2018 bottoms. The other support levels are visible once we zoom in a bit.

The USD Index just moved slightly below the 38.2% Fibonacci retracement level that's based on the 2014 - 2020 rally, and below the 61.8% Fibonacci retracement level that's based on the 2018- 2020 rally.

Each of these retracements is powerful on its own, but taking them both into account and then combining them with a rising long-term support line creates a very powerful support.

And this time, people are also hating on me due to me speaking out about what I see on the charts and what is my opinion about it. I can't imagine what obscenities are written about the analyst who - on Forbes.com - wrote an article entitled "Stay The Hell Away From Gold".

On a side note, the hateful comments are quite surprising. Yes, it would have been much better to become bearish only right now, and not early before the mining stocks refused to move to new highs. Yes, we were too early with the current short position in the miners (we didn't feature shorting suggestions for silver or gold, though, only price targets as they were requested by our readers). Yes, if possible, we would love to get back in time and delay opening our current trading positions. We are not 100% correct and will never be, and the same applies to everyone else in this business, which is why position sizing is so important. With the benefit of hindsight, all tops and bottoms are obvious, and nobody will pick all of them. However, at any given time, when I made an observation, comment or decision, I did so with greatest care about my subscribers and readers.

The thing that's not that intuitive is that for an analyst this "greatest care" means being as objective as possible and not automatically going with majority or with what's currently most popular, easy to write, or easy to read. In fact, an analyst, who would do that, would be completely useless, as a simple online survey asking about people's sentiment, could easily replace them.

The value that the analyst can generate comes from providing a synthesis of what they view as important, including analogies, patterns, fundamentals, cycles, and whatever they find as justified based on a reasonable methodology. Then, investors can use this information along with some other details about the market (perhaps other analysts, perhaps their own research, perhaps a certified investment adviser) or about themselves (risk tolerance, ability to take on risk, liquidity requirements and so on) to make informed investment decisions. By not speaking their mind (even against what the majority thinks), the analyst is actually refusing to do what they are supposed to do, and how they should be providing value to investors.

The analysts' responsibility is to provide their opinions as objectively, as thoroughly as possible and without worrying about "pleasing" others with their comments. That's how they can really care about people. Analysts are not responsible for each investor's gains or losses, as they are not pulling the final strings. Of course, the analyst can exercise extra care by providing hints regarding position sizing (we're linking to our complex article on that matter in each of our Gold & Silver Trading Alerts, usually more than once; plus we are providing a simple simulation of excessive and relatively normal position sizes), but it is the investor who is responsible for executing all that.

Sadly, it is sometimes the case that people use the analyses as a "scapegoat" should they need it - and they need it rather sooner than later if they use excessive position sizes. Instead of really digging into the details of a given analysis and position sizing, people sometimes use all or most of their capital for a single (perhaps even leveraged) trade, especially if a single article makes a good job explaining a given analyst's reasoning. If this trade works in their favor, they are ecstatic and ready to gain more adrenaline on their next over-leveraged trade. When a trade finally doesn't go as well as planned (it has to, as nobody is always correct), their losses are already so big that they can't recover. And then they find a scapegoat in the form of someone, whose opinion they decided to use, as if it wasn't their investment decision, but this "someone's". And the more they are really angry with themselves (and the less they are willing to accept the responsibility for their investment decisions), the more anger they will express toward others, regardless of what they've done previously for them or in general (like very few people remember that we made money on the March decline and then we made money on the rebound buying precisely on March 13).

This is all very much connected with the overall concept of ego and ownership that a former Navy Seal leader Jocko Willink is discussing in his book called "Extreme Ownership". That's one of the best books that I read, definitely worth your time, but watching him speak about it on YouTube would also be a good idea if you're short on time (who isn't?).

I think that I already diverted from the regular analysis too much, so I will be getting back on track, but I would like to say that again regarding the responsibility:

The analysts' responsibility is to provide their opinions as objectively, as thoroughly as possible and without worrying about "pleasing" others with their comments. That's how they can really care about people. Analysts are not responsible for each investor's gains or losses, as they are not pulling the final strings. Investors/traders are responsible for their gains and losses, and for making sure they get enough details before making their investment decisions. I - and everyone at Sunshine Profits - strive to help you as much as I can, but these will be your profits, and your responsibility if you make them (or not).

Analysts will be right, and analysts will be wrong. No exceptions. We disagree with Mr. Larry Light, who suggests one to "stay the hell away from gold", as we think that gold is a great buy long term, but it still needs to correct profoundly before soaring. However, we realize that Mr. Light might be right here or in many other ways, and while we disagree with him, we disagree respectfully.

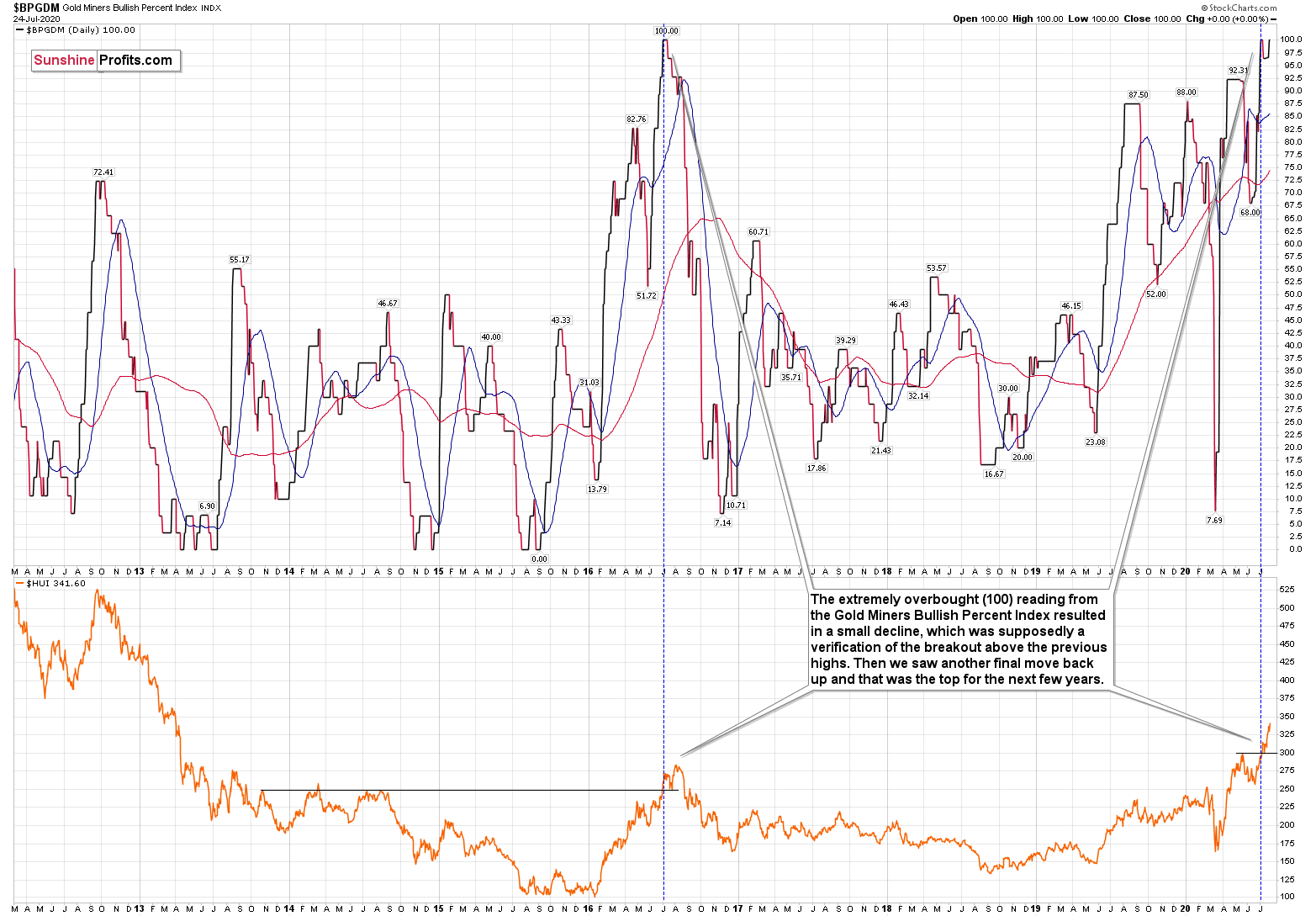

We also disagree with those, who say that gold will soar indefinitely without bigger corrections, especially now, shortly after the Gold Miners Bullish Percent Index flashed the extreme oversold signal. And once again - we disagree respectfully.

The excessive bullishness was present at the 2016 top as well and it didn't cause the situation to be any less bearish in reality. All markets periodically get ahead of themselves regardless of how bullish the long-term outlook really is. Then, they correct. If the upswing was significant, the correction is also quite often significant.

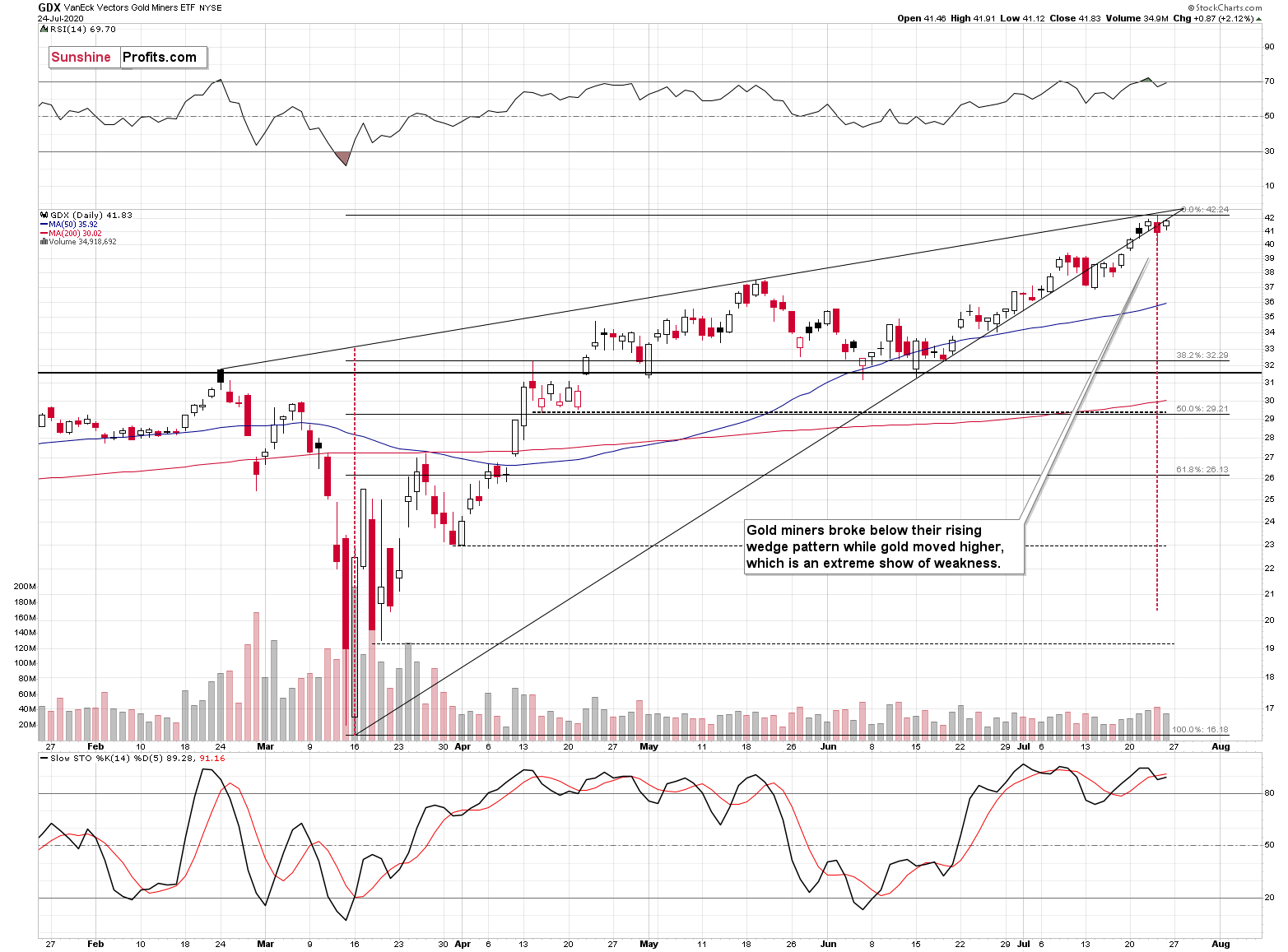

On Friday, gold moved higher once again, but miners refused to move to new highs. Given the size of today's upswing in gold, it's very likely that miners will manage to move to new 2020 highs, but we doubt that they would be able to hold these gains. As gold ultimately corrects - and we think that it will correct and profoundly so - miners would be likely to slide as well. The invalidation of the breakout above the previous 2020 highs would be a great trigger for such a move.

Please note that the huge rising wedge pattern is about to form a vertex today or tomorrow. The same rule that applies to triangles has implications also here. The vertex is quite likely to mark a reversal date. Given the overbought status of the RSI (given today's upswing, its almost certain to move above 70 once again) as well as miners recent unwillingness to track gold during its continuous rally, it's highly likely in my view that this will be a top.

Let's turn to metals themselves.

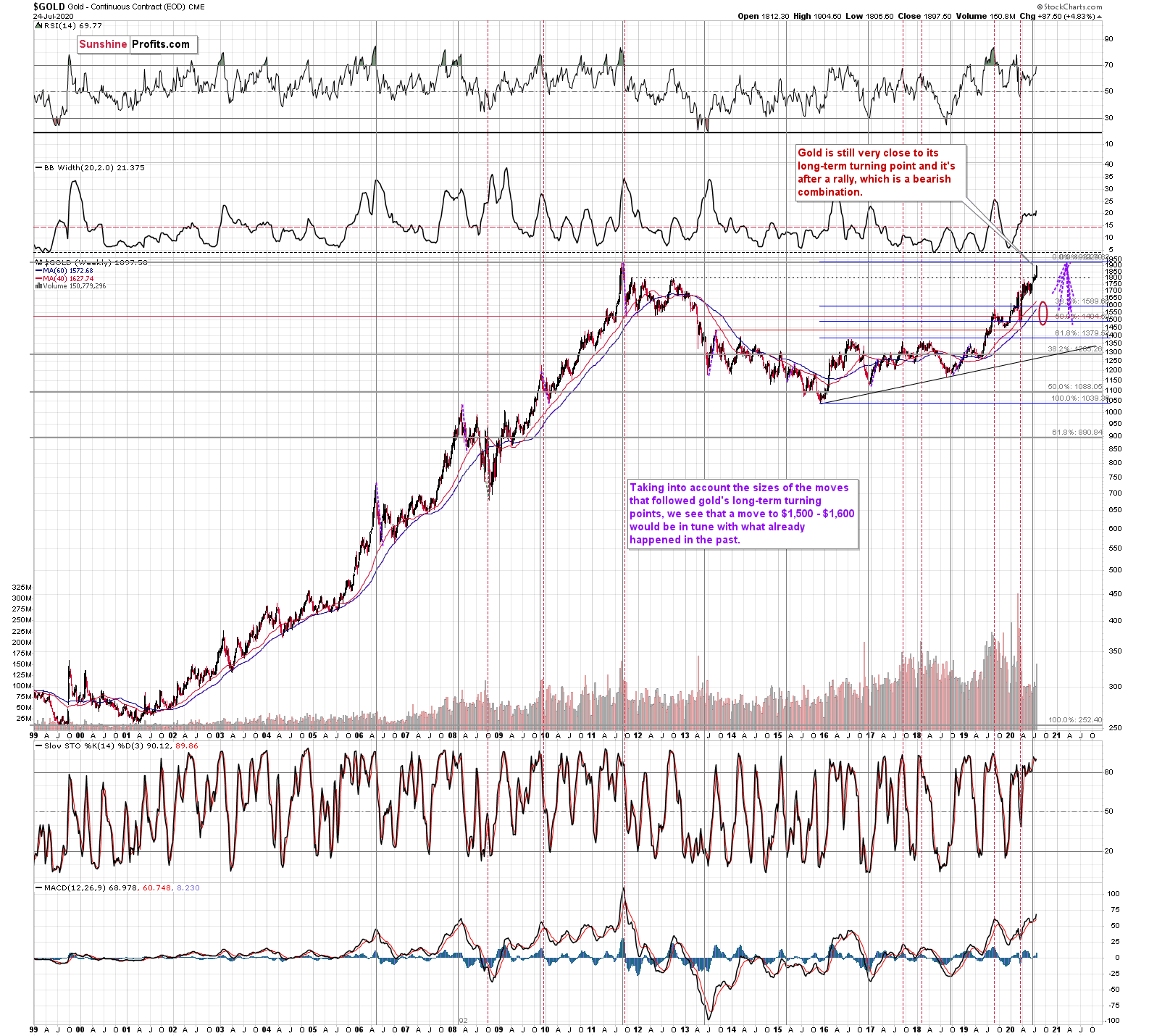

Gold just moved above its 2011 high in a volatile overnight move. This breakout was visible, but it's far from being confirmed. At times, one might say that a given breakout was confirmed through the size of the move or the volume that accompanied it, but neither of these factors applies right now. Consequently, we should wait for several (at least 3) consecutive closes above the 2011 highs to say that the breakout is confirmed. Before that happens, invalidation of the breakout is much more likely in our view. In particular, because of what we already wrote with regard to the outlook for the USD Index, but also because of the immense strength of the resistance that the previous all-time high provides.

Gold's very long-term turning point is here and since the most recent move has definitely been to the upside, its implications are bearish.

We used the purple lines to mark the previous price moves that followed gold's long-term turning points, and we copied them to the current situation. We copied both the rallies and declines, which is why it seems that some moves would suggest that gold moves back in time - the point is to show how important the turning point is in general.

The big change here is that due to gold's big rally, we moved our downside target for it higher. Based on the information that we have available right now, it seems likely that gold will bottom in the $1,500 - $1,600 area. That's very much in tune with how much gold moved after the previous long-term turning points. It's also very much in tune with how low gold moved in 2011 after trying to break above $1,900.

Also, while we're discussing the long-term charts, please note the most important detail that you can see on the gold, silver, and mining stock charts, is hidden in plain sight. Please note how much silver and miners rallied.

Gold just moved above its 2011 high. And silver?

Silver is yet to reach even the first of the classic Fibonacci retracement levels (38.2%) based on the entire 2011 - 2020 decline.

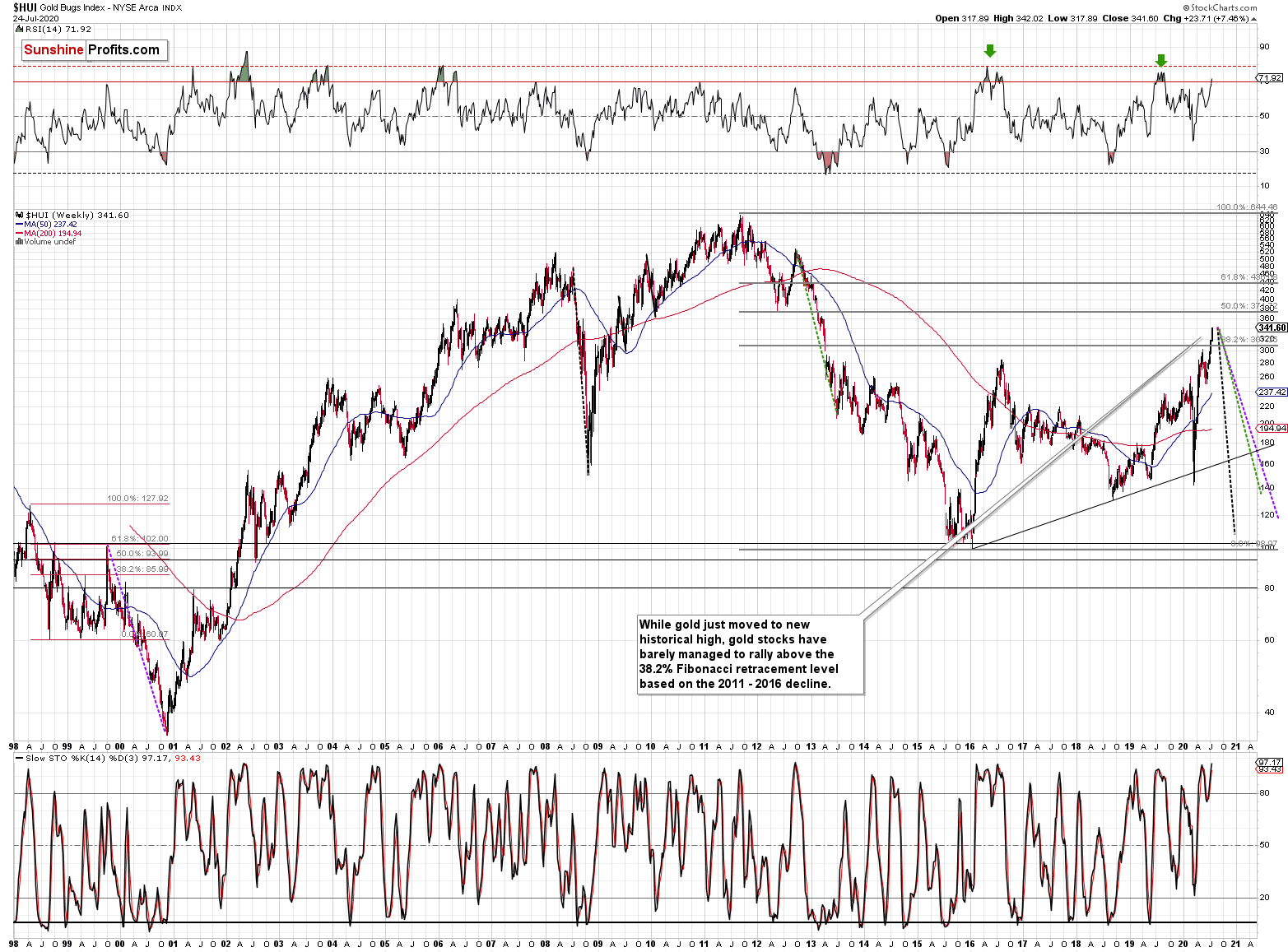

Meanwhile, despite their recent run-up, gold stocks - HUI Index - are just a bit above the 38.2% Fibonacci retracement based on the 2011 - 2016 decline.

It's mostly gold that is making the major gains - not the entire precious metals sector.

Moving back to silver, it's good to note that the time the current rally is taking, is still very similar to the time that the final part of the 2016 run-up took. The current move is bigger, but in terms of time, they are still very alike. This adds to the bearish implications of the situation in the USD Index and gold miners' extremely overbought condition along with their vertex-based reversal that's due today or tomorrow.

Overview of the Upcoming Decline

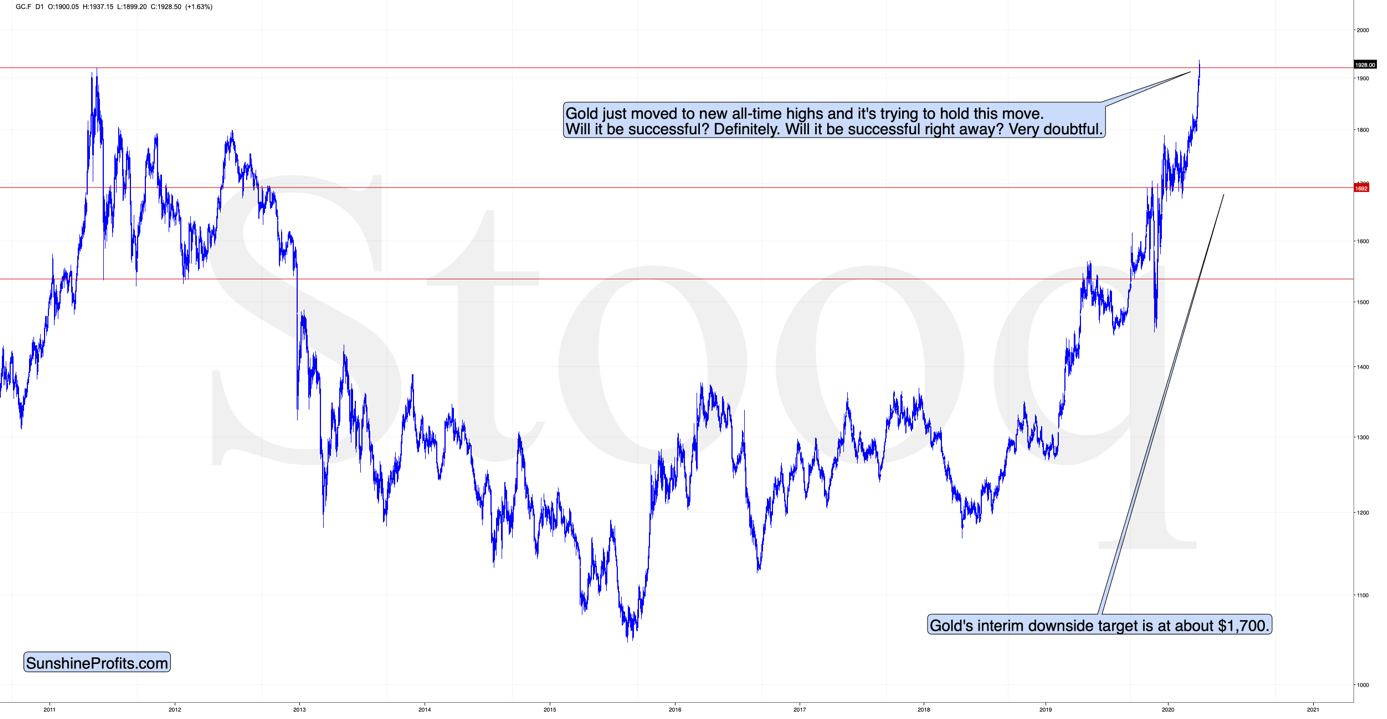

As far as the current overview of the upcoming decline is concerned, I think that after bottoming temporarily at about $1,700, gold, silver and miners will bounce back - perhaps $30-$50 or so in gold, and then we will probably see another move lower, with silver declining more than miners. That would be in tune with how the markets initially reacted to the Covid-19 threat.

However, we are not married to this outlook. Gold moved to almost $1,900 and starting from this level instead of $1,700 or so and moving to $1,400 would imply a decline almost twice as big now. Consequently, there is a chance that the decline to $1,700 is all there would be to see, before the PMs move higher.

At this time it seems that after the initial decline to $1,700, gold could correct and then decline to $1,500 - $1,600 and that would be the final bottom - one that would hold for years, perhaps decades.

How will we tell, which scenario is more likely - a decline visibly below $1,700 or just to it? Based on the way different parts of the precious metals sector react to the decline and to the initial rebound. If silver catches up with the decline when gold moves to $1,700, but miners lead on the way back up (strongly so), it will be more likely that the bullish scenario prevails. If we see the opposite - miners are weak during the rebound and silver doesn't catch up with the decline once gold approaches $1,700, the bearish case will prevail. Anything in between will require additional confirmations and we will keep our subscribers updated in any case.

The impact of all the new rounds of money printing in the U.S. and Europe on the precious metals prices is very positive in the long run, but it doesn't make the short-term decline unlikely. In the very near term, markets can and do get ahead of themselves and then need to decline - sometimes very profoundly - before continuing their upward march.

Summary

Summing up, the extremely overbought reading from the Gold Miners Bullish Percent Index and the individual price moves make the current case very similar to the 2016 topping pattern, and other important indications (especially gold's and USD's long-term cycles) point to likely - sizable - decline in the following several weeks.

The fact that gold just moved above its 2011 high doesn't change the above. Based on the latest information, we are updating our downside target for gold to the $1,500 - $1,600 area, but we are not adjusting the expectation regarding the big correction before gold truly takes off.

The above doesn't impact our targets for mining stocks, as they are based on the more short-term decline to $1,700 or so.

Naturally, everyone's trading is their responsibility, but in our opinion, if there ever was a time to either enter a short position in the miners or to increase its size if it wasn't already sizable, it's now. We made money on the March decline and on the March rebound, and it seems that another massive slide is about to start. When everyone is on one side of the boat, it's a good idea to be on the other side, and the Gold Miners Bullish Percent Index literally indicates that this is the case with mining stocks.

After the sell-off (that takes gold below $1,600), we expect the precious metals to rally significantly. The final decline might take as little as 1-6 weeks, so it's important to stay alert to any changes.

Most importantly - stay healthy and safe. We made a lot of money on the March decline and the subsequent rebound (its initial part) price moves (and we'll likely make much more in the following weeks and months), but you have to be healthy to really enjoy the results.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in mining stocks is justified from the risk to reward point of view with the following binding exit profit-take price levels:

Senior mining stocks (price levels for the GDX ETF): binding profit-take exit price: $32.02; stop-loss: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the DUST ETF: $28.73; stop-loss for the DUST ETF: none (the volatility is too big to justify a SL order in case of this particular trade)

Junior mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $42.72; stop-loss: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the JDST ETF: $21.22; stop-loss for the JDST ETF: none (the volatility is too big to justify a SL order in case of this particular trade)

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway. In our view, silver has greater potential than gold does):

Silver futures downside profit-take exit price: $8.58 (the downside potential for silver is significant, but likely not as big as the one in the mining stocks)

Gold futures downside profit-take exit price: $1,382 (the target for gold is least clear; it might drop to even $1,170 or so; the downside potential for gold is significant, but likely not as big as the one in the mining stocks or silver)

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that the in the trading section we describe the situation for the day that the alert is posted. In other words, it we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices, so that you can decide whether keeping a position on a given day is something that is in tune with your approach (some moves are too small for medium-term traders and some might appear too big for day-traders).

Plus, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one, it's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade) we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGLD, DGLD, USLV, DSLV, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (DGLD for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and DGLD as still open and the stop-loss for DGLD would have to be moved lower. On the other hand, if gold moves to a stop-loss level but DGLD doesn't, then we will view both positions (in gold and DGLD) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels on a daily basis for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Editor-in-chief, Gold & Silver Fund Manager