Briefly: in our opinion, full (300% of the regular position size) speculative short positions in mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert. We are moving the profit-take levels higher.

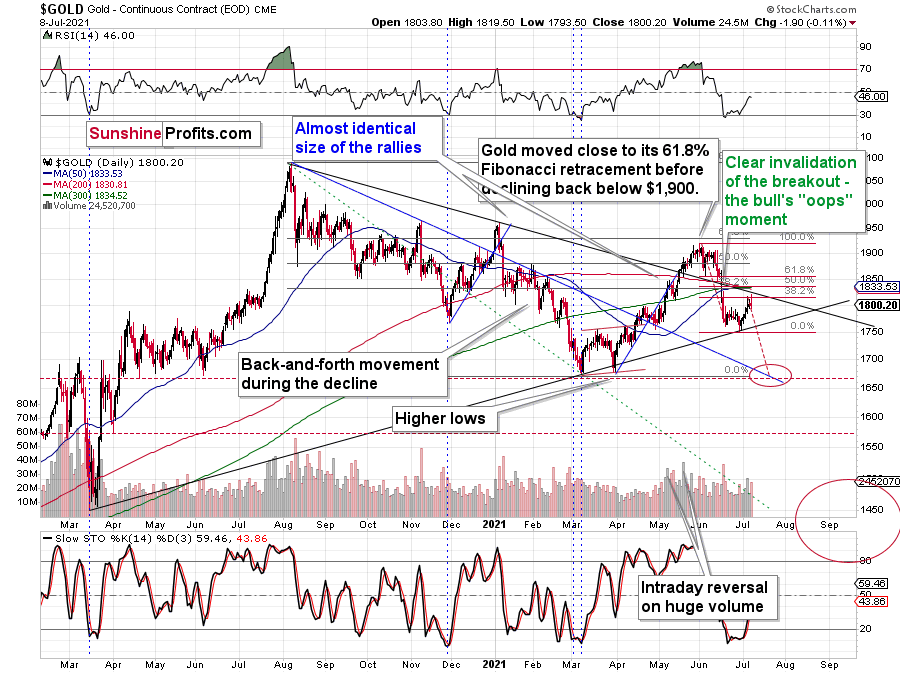

Gold made another reversal yesterday, and the miners declined profoundly – also once again. Just as in early 2013 – that’s extremely bearish.

Gold futures moved to new intraday highs yesterday, but they ended the session $1.90 lower, creating yet another shooting star reversal candlestick. Seeing just one reversal is bearish on its own, but seeing more than one in a row is profoundly bearish.

Please note that gold reversed after moving slightly above the 38.2% Fibonacci retracement based on the recent decline. The minimum one of the likely correction sizes was reached, so the decline can now continue. The RSI is no longer oversold, but rather close to the middle of its trading range. This tells us that bearish gold forecasts are clearly justified. Also based on the reversals that we just saw, this move is likely to be to the downside.

The Gold Miners

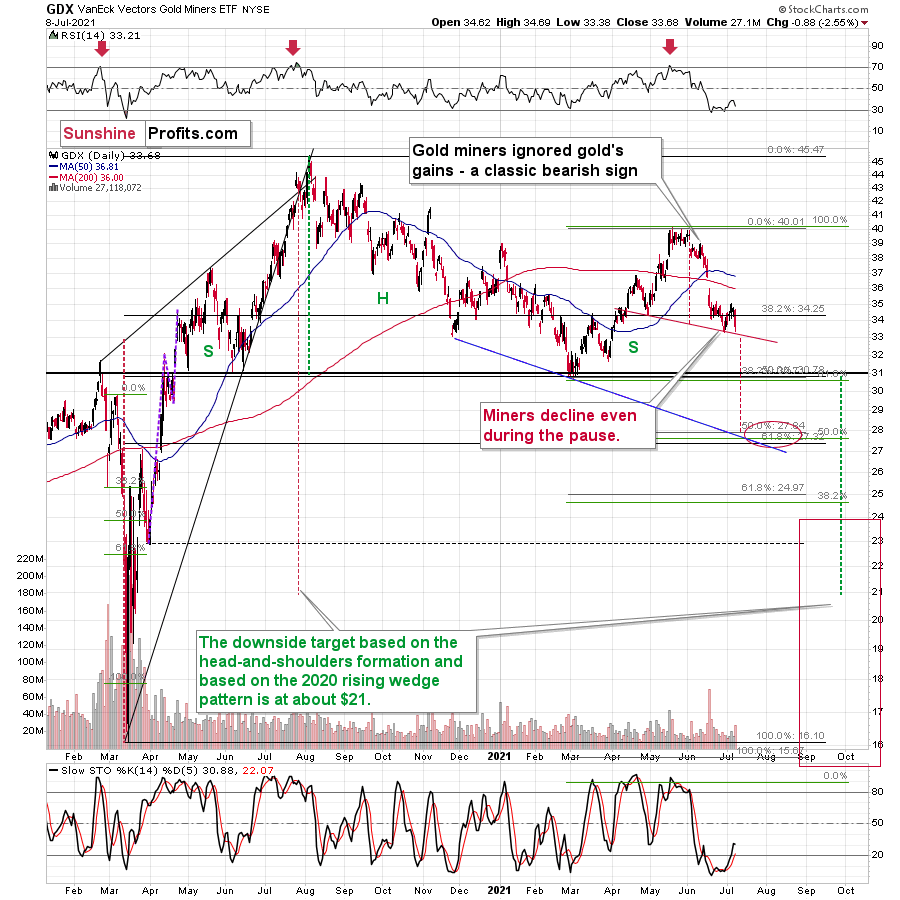

Another detail that serves as a bearish confirmation is the performance of the mining stocks.

While gold moved slightly above its recent highs during yesterday’s session, the gold stocks moved to their previous lows. If this is not a shocking proof of extreme underperformance, then I don’t know what would be one.

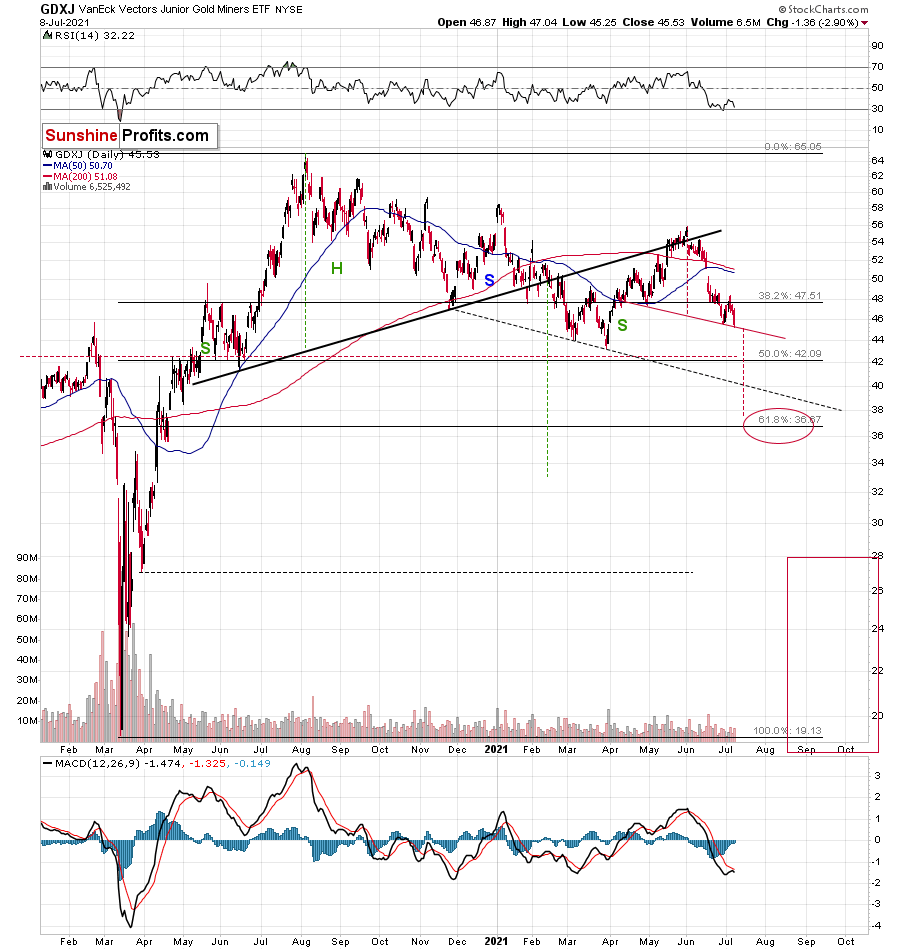

The mining stocks simply can’t wait to break to new lows. In fact, the junior miners – my proxy of choice for the current (profitable) short trade – already broke to new lows.

On June 29 (the June low), the GDXJ ETF closed at $45.83, and yesterday it closed at $45.53. Ladies and gentlemen, we have a breakdown.

Of course, it was not confirmed yet, but the fact that we saw a new low while gold made a new short-term intraday high is extremely bearish.

The interesting detail about both (GDX and GDXJ) ETFs is that the recent price moves created bearish head-and-shoulders formations in them. The targets based on such formations are based on the size of their heads. I marked the height of the head and the targets with red, dashed lines.

It seems that we might see a move below $38 in the GDXJ before it corrects in a more meaningful way.

Ok, but shouldn’t March lows provide strong support and trigger a rebound?

Yes, the previous lows provide relatively important support, but:

- Miners have been very weak relative to gold recently, and they don’t even need to keep it up in order to slide below the March lows – they could behave “normally” for this to happen.

- Gold seems to be ready to slide significantly – to its March lows or so. In order to do it, it would need to approximately repeat its June slide.

If gold repeats its June slide, it will decline by about $150.

Taking the entire decline into account (since August 2020), for every $1 that gold fell, on average, the GDX was down by about 4 cents (3.945 cents) and GDXJ was down by about 6.5 cents (6.504 cents).

This means that if gold was to fall by about $150 and miners declined just as they did so far in the past year (no special out- or underperformance), they would be likely to fall by $5.92 (GDX) and $9.76 (GDXJ). Given yesterday’s closing prices, this would imply price moves to $27.76 (GDX) and $35.78 (GDXJ).

Interestingly, both above-mentioned price levels are in perfect tune with the target areas that I placed on the charts based on the head and shoulders patterns and the 61.8% Fibonacci retracement level (which is based on the entire 2020 rally). This adds to their credibility. Naturally, I will be making updates as the situation develops and we get more information.

Having said that, let’s take a look at the market from the fundamental angle.

An Emotional Bond

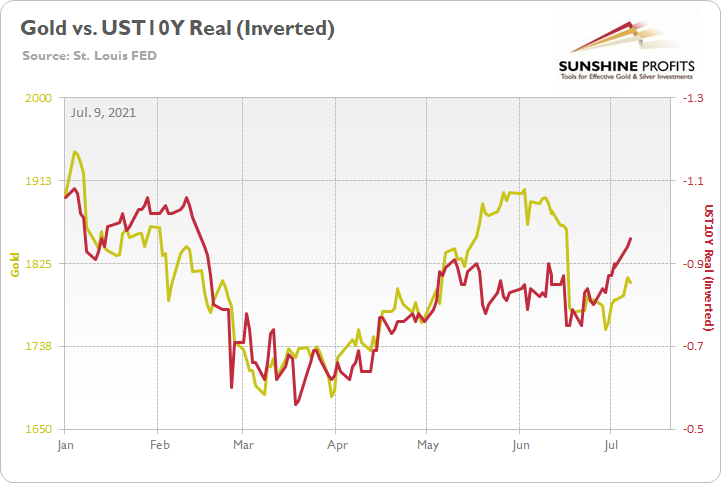

With the U.S. 10-Year Treasury yield losing its wits in recent days, the love-hate relationship between gold and the U.S. 10-Year real yield is once again on full display. For example, it was roughly five months ago that a surging U.S. 10-Year real yield pushed gold over a cliff. Then, once the former reversed its course, the yellow metal rallied precipitously from March through May.

And with the pair reprising their roles, gold’s short-term strength has been underwritten by a significant decline in the U.S. 10-Year real yield. However, this time around, gold’s response has been relatively weak (once bitten, twice shy) and the driving force behind the move lacks empirical credibility.

Please see below:

To explain, the gold line above tracks the London Bullion Market Association (LBMA) Gold Price, while the red line above tracks the inverted U.S. 10-Year real yield. For context, inverted means that the latter’s scale is flipped upside down and that a rising red line represents a falling U.S. 10-Year real yield, while a falling red line represents a rising U.S. 10-Year real yield.

If you analyze the relationship, you can see that one’s pain is often the other’s gain. And if you focus your attention on the right side of the chart, you can see that the U.S. 10-Year real yield’s recent malaise has uplifted the yellow metal.

But what’s causing the jitters in the bond market?

Well, for one, the Delta variant has spread across the globe, and investors fear that its wrath could upend economic growth. For context, I warned on Jun. 23 that the outbreak had the potential to quell some of the recent momentum.

I wrote:

Absent a severe spread of the Delta variant – which White House chief medical advisor Dr. Anthony Fauci said was “the greatest threat in the U.S. to our attempt to eliminate COVID-19” – U.S. economic growth should easily outperform its developed-market peers.

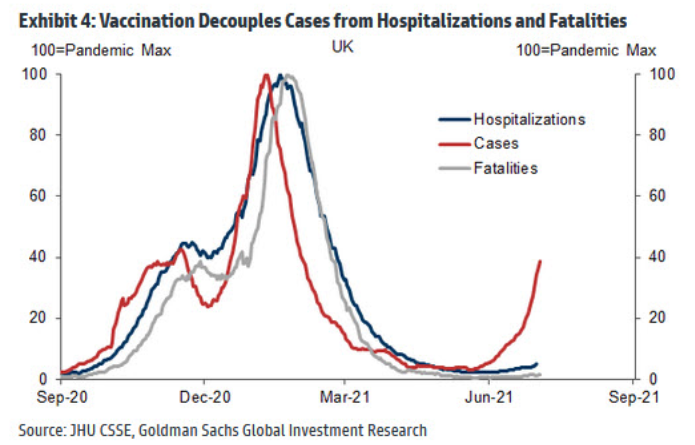

However, while I don’t claim to be an epidemiologist, the rollout of vaccines has helped suppress the threat of COVID-19.

Please see below:

To explain, the red, blue and gray lines above track the U.K. cases, hospitalizations, and deaths that have resulted from COVID-19. If you analyze the right side of the chart, you can see that the mammoth spread of the Delta variant didn’t result in a surge in hospitalizations or deaths. As a result, with roughly 55% of U.S. citizens already after receiving at least one dose of a COVID-19 vaccine (as of Jul. 7), the bond market’s reaction seems rather excessive.

Second, and more importantly, the recent behavior of the U.S. 10-Year Treasury yield is indicative of a short-covering rally. To explain, when the minority calling for higher yields eventually became the consensus, over-positioning led to an imbalance between investors that were long and short the U.S. 10-Year Treasury. And with the Delta variant, sentiment, and the FED’s taper talk creating the perfect storm, the narrative shifted from ‘economic Renaissance’ to ‘growth is about to fall off a cliff.’

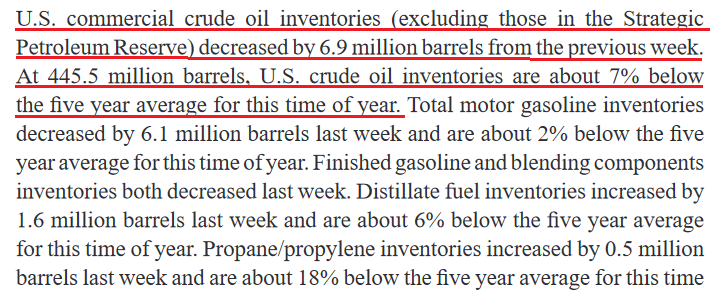

However, it’s noteworthy that the U.S. 10-Year Treasury yield began 2021 at 0.92%. As a result, the Treasury benchmark is still up by more than 40% year-to-date (YTD). In addition, the U.S. Energy Information Administration (EIA) revealed on Jul. 8 that crude inventories declined by 6.9 million barrels week-over-week (WoW) – ahead of the consensus estimate of 4.033 million barrels – and the WTI ended the day in the green. Thus, does it seem like economic growth is about to collapse?

Source: EIA

Source: EIA

Long-Term Treasuries

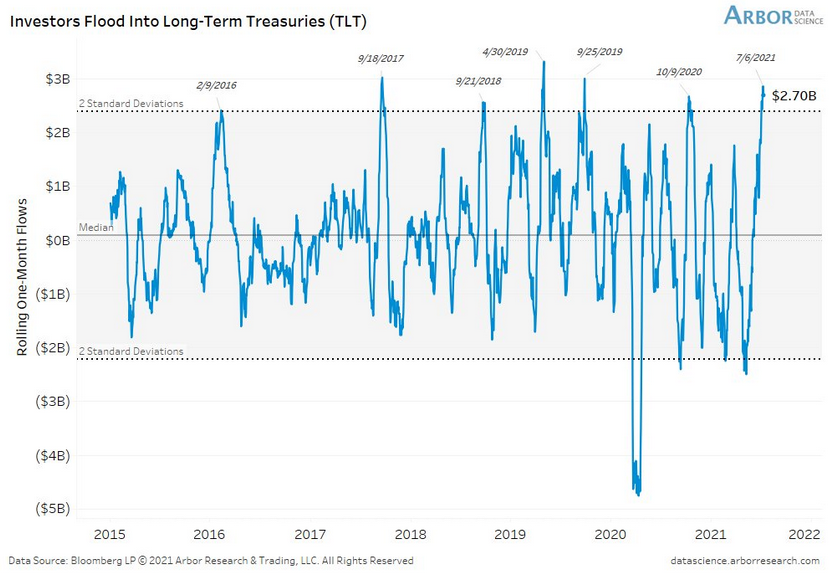

Furthermore, with investors panic-buying bonds, the iShares 20+ Year Treasury Bond ETF (TLT) recorded more than $2.7 billion in inflows, which is more than two standard deviations above its monthly average.

Please see below:

To explain, the blue line above tracks the rolling one-month fund flows in-and-out of TLT. If you analyze the right side of the chart, investors’ overreaction is on full display. To that point, the last six times that monthly inflows exceeded two standard deviations, 83% of the time the U.S. 30-Year Treasury yield was higher the following month by a median of 15 basis points (0.15%). Thus, if the 30-year yield catches its second wind, the 10-year yield will likely follow suit.

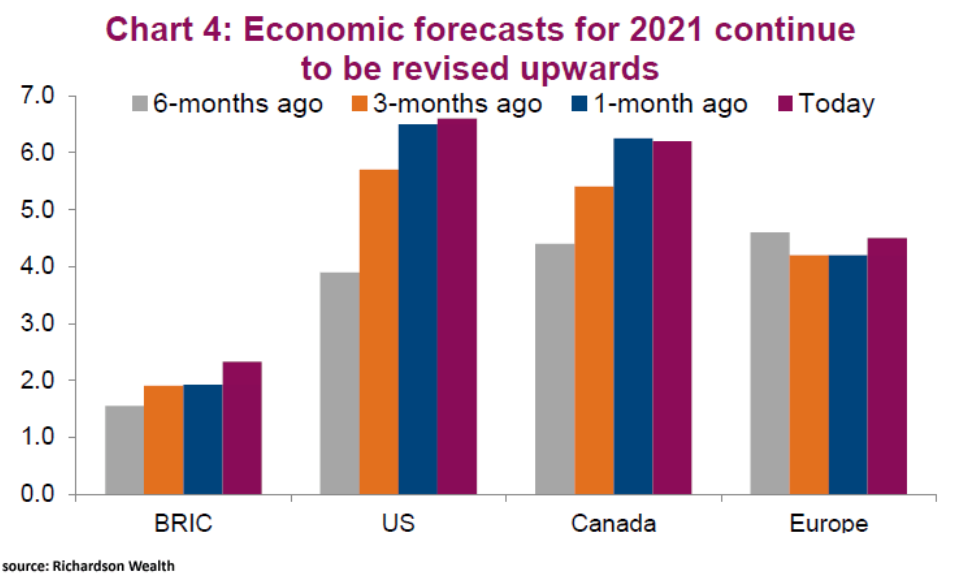

On top of that, with the U.S. economy steadily healing, economists continue to increase their U.S. GDP growth forecasts.

Please see below:

To explain, the various bars above depict economists’ consensus regional GDP growth estimates from the beginning of 2021 until now. If you analyze the purple bar from the “US” column, you can see that growth expectations continue to trek higher. Furthermore, while Canada’s optimism has been reduced and the Eurozone is a distant third, U.S. outperformance is bullish for the USD/CAD and bearish for the EUR/USD.

Surprise, Surprise!

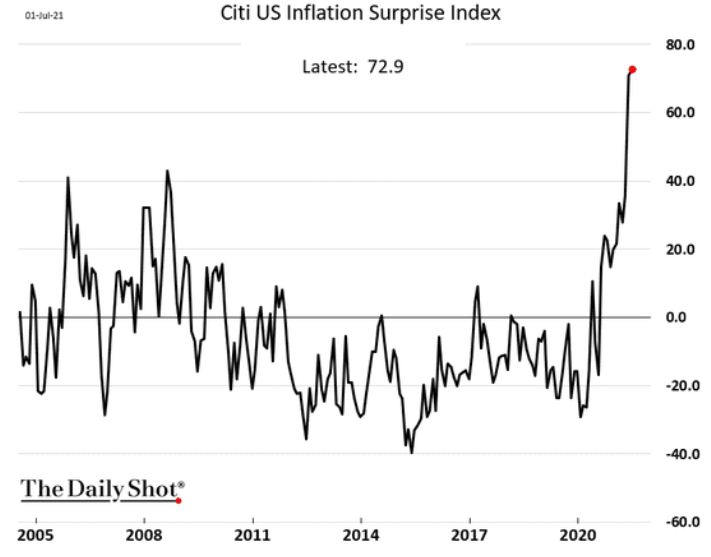

If that wasn’t enough, while I’ve been warning for months about the forthcoming inflationary pressures, the FED has essentially admitted its mistake. Conversely, while the bond market continues to resist, the Citigroup US Inflation Surprise Index (ISI) has gone parabolic. For context, the index rises (falls) when realized inflation comes in above (below) expectations.

Please see below:

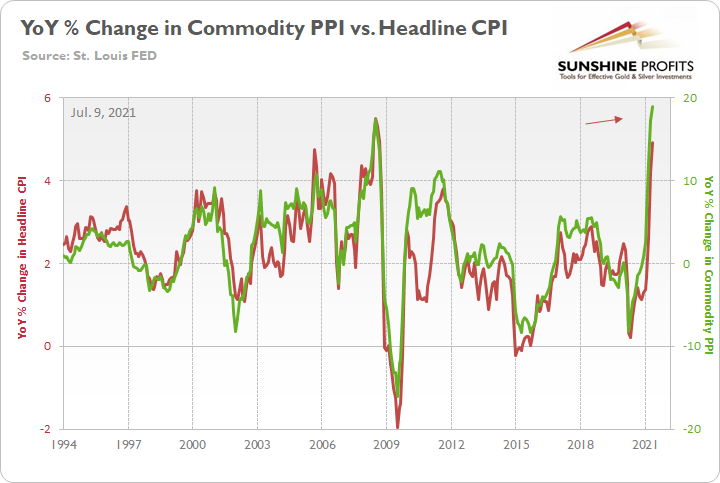

To that point, with the Consumer Price Index (CPI) scheduled for release on Jul. 13, another dose of reality could be forthcoming. Case in point: with the Commodity Producer Price Index (PPI) surging by 18.98% year-over-year (YoY) in May – the highest YoY percentage increase since 1974 – the print implies a roughly 5% to 5.5% YoY increase in the headline CPI.

Please see below:

To explain, the green line above tracks the YoY percentage change in the commodity PPI, while the red line above tracks the YoY percentage change in the headline CPI. If you analyze the relationship, you can see that the pair have a close connection. More importantly, though, when the commodity PPI increased by 17.4% YoY in July 2008, the headline CPI rose by 5.3% in August. Thus, with the commodity PPI surging by 18.98% in May, all signs point to another ‘surprising’ headline CPI print for June.

In conclusion, while the PMs were uplifted by the bond market’s recent freak-out, the latter’s paranoia is extremely overblown. With crude inventories declining and U.S. job openings hitting another all-time high on Jul. 7, the U.S. recovery remains on track. Moreover, with the FED’s hawkish shift moving up the taper timeline, the front-end of the U.S. yield curve can upend the PMs on its own. However, with the U.S. 10-Year Treasury yield near an all-time low relative to realized inflation and U.S. GDP growth prospects, a return to reality should add to the PMs’ drama over the medium term.

Overview of the Upcoming Part of the Decline

- The barely visible corrective upswing in gold might already be over, and another huge decline is likely just around the corner.

- After miners slide in a meaningful and volatile way, but silver doesn’t (and it just declines moderately), I plan to switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this would take place – perhaps with gold close to $1,600. I plan to exit those short positions when gold shows substantial strength relative to the USD Index, while the latter is still rallying. This might take place with gold close to $1,350 - $1,500 and the entire decline (from above $1,900 to about $1,475) would be likely to take place within 6-20 weeks, and I would expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold – after gold has already declined substantially) is likely to be the best entry point for long-term investments, in my view. This might also happen with gold close to $1,475, but it’s too early to say with certainty at this time.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector would be likely to bottom about three months after the general stock market tops.

- The above is based on the information available today, and it might change in the following days/weeks.

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Leveraged ETF Target Calculation

Every now and then I get a question as to how I arrived at a target for a given leveraged ETF, especially when I’m adjusting the targets. So, I thought that I would explain it right away since I’m changing the profit-take levels today.

I base the calculations of the leveraged instrument on the target of the unleveraged instrument that it’s based on. The JDST is based on the GDXJ (it doubles the inverse of daily price changes), so that’s what I’m using as the basis.

So, starting with yesterday’s closing price of the GDXJ ($45.53), I checked how low it’s likely to move. It’s $37.12 in this case. Another assumption needed is how long the move is likely to take. Let’s assume that it will take about 30 trading days.

If the GDXJ was to fall from $45.53 to $37.12 in 30 trading days, it would be declining on average by 0.67841% per day. Let’s check: 45.53 x (1-0.0067841)^30 = ~$37.12, so that’s correct.

The JDST doubles the daily price move, so on each day when the GDXJ falls by 0.67841%, the former should theoretically rally by about 1.35681% (it’s not perfect multiplication because of rounding).

Yesterday’s closing price for the JDST was $10.90. If it was to rally for 30 days by 1.35681% each day, it would move to: 10.90 x (1+0.0135681)^30 = $16.33. And that’s our target.

If we did the same thing but assumed that the decline would take place over just 10 trading days, the final JDST target would be about $16.20. And if it was 50 trading days, the JDST target would be $16.36.

So, we see that it doesn’t change that much, and – being conservative – it might be best to move the profit-take level a bit below the lowest of these scenario-based targets. And since $16 is a relatively round number (might trigger resistance), it might be an even better idea to move the profit-take level slightly below it – to $15.96. And that’s how to get the current value of the profit-take level.

Ideally, it would be best to adjust the target every day, but being realistic, it makes the most sense to do so once we move relatively close to the target, as that’s when it will really matter – when the target is within the reach.

One final note – the above is not a perfect approximation, as one would need to know the exact future (!) price path of the GDXJ in order to estimate the exact target. The above includes a simplification – the assumption that the GDXJ will fall by the same amount (percentage-wise) each trading day. This almost certainly won’t happen, but it’s still the best approximation that we can get relatively easily (analogy: a democracy is not a perfect system, but it’s still better than whatever else had been widely tried). The closer we get to the target, the less the future price path can change, as there are fewer days in which it could do something random.

Summary

To summarize, even though gold could still move somewhat higher in the near term, it seems that having a short position in the junior mining stocks is much more justified from the risk-to-reward point of view than having a long one in any part of the precious metals market. Gold miners’ underperformance along with a self-similar pattern in the USD Index (pointing to the breather being over) and the length of the “bottoming” process in gold that no longer resembles a bottom (but rather a pause within a slide) all make the bearish outlook justified from the risk-to-reward point of view.

Due to the increased clarity regarding the likely next interim bottom in gold (previous 2021 lows) and mining stocks (below their previous 2021 lows), I’m moving the profit-take levels on our current short position higher. This does not imply that the entire decline is going to be smaller than first believed. It’s simply a consequence of the short-term target becoming more crystallized.

After the sell-off (that takes gold to about $1,350 - $1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and this March, and it seems that we’re about to make much more on the upcoming decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

By the way, we’re currently providing you with a possibility to extend your subscription by a year, two years or even three years with a special 20% discount. This discount can be applied right away, without the need to wait for your next renewal – if you choose to secure your premium access and complete the payment upfront. The boring time in the PMs is definitely over and the time to pay close attention to the market is here. Naturally, it’s your capital, and the choice is up to you, but it seems that it might be a good idea to secure more premium access now, while saving 20% at the same time. Our support team will be happy to assist you in the above-described upgrade at preferential terms – if you’d like to proceed, please contact us.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $37.12; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $15.96; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $37.02; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures upside profit-take exit price: unclear at this time - initially, it might be a good idea to exit, when gold moves to $1,683

Gold futures upside profit-take exit price: $1,683

HGD.TO – alternative (Canadian) inverse 2x leveraged gold stocks ETF – the upside profit-take exit price: $12.88

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief