Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

You might have already heard the key news of the day. If not, here’s a quote from Bloomberg:

Russia launched a barrage of missile, artillery and air attacks early Thursday, triggering the worst security crisis Europe has witnessed in decades. Ukraine’s Interior Ministry warned that the capital, Kyiv, was being targeted and urged citizens to go to shelters. Ukraine’s border guard said that it was being shelled from five regions, including from Crimea in the south and Belarus to the north, and that Russian forces had crossed into the country.

The unlikely, and – unthinkable – became reality. I hope the peace will be achieved soon and with as little bloodshed as possible.

It is my responsibility to analyze the situation and report to you how it’s likely to impact the markets and what it implies for one’s trading positions. What’s justified from the risk-to-reward point of view and what’s not? So, that’s exactly what I’m going to do. Before I proceed, please note that today’s text is going to be sent before it’s edited, so it could include some typos – I want to send you this analysis as soon as possible.

Let’s start with the global implications. This article from Reuters does a good job in describing some of them in this article: Expert views on Russian forces invading Ukraine

It can be summarized in the following way: war and/or sanctions are likely to trigger crises and higher prices globally, hitting some countries more than others. It also sets a precedent for the taking over of smaller countries by big ones with nuclear warheads at their disposal. This doesn’t bode well for Taiwan and the South and East China Seas.

Now, let’s try to look behind the curtain.

Based on what I’ve been writing for days, weeks, and months, you know that a massive crisis and stock market crash were bound to happen. Huge inflation was likely to emerge. What’s the real reason for this? Ridiculously low interest rates for a very long time and an enormous, unthinkable scale of money printing.

How can the governments (in general) and monetary officials NOT be held responsible for that unavoidable crash?

With a scapegoat, of course!

The pandemic, lockdowns, etc. were a great way to justify even more money printing, and now, when it’s obvious that the interest rates have to be raised, that’s likely to trigger a market crash, we have… A Russian invasion that immediately sunk the world stock indices, triggering the decline.

How convenient for “The Powers That Be”. Now and for the months and years to come, the narrative can be that it was not because of the money that was printed, not because of the wide-spread lockdowns, not because of anything that any non-Russian politician was responsible for. Putin might be the only one the world's media and history will blame for the incoming market crash and its resulting consequences (deaths, poverty, I don’t event want to start thinking how many various traumas people experience). If Putin were to accept this kind of role, he would want to get something in return – something he values more than the above. And perhaps that’s where his invasion of Ukraine comes in.

Look, I’m not saying that I have any proof of the above, of any conspiracy, etc., and the above is just a speculation on my part.

Still, it seems that wars are rarely waged for the officially stated reasons – perhaps the real reasons this time are as above…

What does it translate to in terms of market movement? In particular, the precious metals market?

First of all, the general stock market is likely to be negatively affected by all that. This seems kind of obvious to me, so I’m not going into details. This means that a repeat of the 2008 and 2020 scenarios is becoming more likely. Note: that’s mostly based on supply-chain disruptions and sanctions, not on war itself. Consequently, this factor – being bearish for gold, silver, and mining stocks – is likely to come into play with full force over the medium term, not necessarily immediately.

Second, nothing changed with the following rule: gold is likely to peak along with peak uncertainty. While it previously seemed that the peak of uncertainty was behind us, it wasn’t. However, with the invasion already taking place right now, it’s obvious that the peak uncertainty is practically right now, unless it escalates into a World War 3, and – while many unlikely things have happened recently – it still seems extremely unlikely in my view.

Third, mining stocks, especially junior mining stocks, don’t have to react just as gold does. In fact, they are not likely to, based on the analogy to what happened when Russia took over Crimea in 2014. I already wrote about that previously, and it’s worth quoting it once again:

What would happen then is that PMs would be likely to rally until the conflict actually starts, then a bit more, and then they would likely continue their medium-term decline. It already happened in 2014, when Russia took over Crimea. Interestingly, it was more or less at the same time of year. By mid-Feb, the majority of the rally was over. The entire rally in gold was about $200, and the part that continued after mid-Feb. was about $50.

Thus, considering December 2021 as the starting point of this rally, gold is up by about $150 now – so the history rhymes here.

Consequently, IF (and that’s a big if) the tensions escalate and Russia takes over a part of Ukraine once again, we might be looking at “only” an extra $50 rally in gold or so and a top in mid-March – and then the medium-term slide would be likely to continue.

When I wrote the above, gold was trading at about $1,900. It’s trading just below $1,950 at the moment of writing these words, so we now have a to-the-letter analogy to 2014. And in this analogy, the “peak concern” and “peak gold” have likely already materialized.

Oh, and by the way, GDXJ actually topped in mid-Feb 2014, and then it just moved back and forth until gold topped in mid-March 2014. OK, to be precise, the GDXJ’s intraday high in March was about 3% above its mid-Feb high, and it was then followed by an immediate decline.

It seems like the worst time to be exiting short positions in junior mining stocks. Instead, it might be a perfect time to be entering or adding to them (if one doesn’t have the desired exposure yet).

Well, since gold is about $200 above its late-2021 low, thus completing the analogy to 2014, let’s check if junior miners are also behaving similarly.

In today’s London trading, the GDXJ is up, but not very significantly so. Today’s intraday high (so far) is 38.86. The recent intraday high was 37.79. This means that today’s intraday high is 2.83% higher, which is in perfect tune with what happened in 2014.

Please note that we already saw an intraday decline, despite the higher open, which is also what accompanied the early-2014 top in the GDXJ. Of course, the session is far from being over, so this could change. It’s a weak (but present) indication, while the near-3% size of the rally above the previous highs is a strong indication that the situation is similar to what we saw in 2014. And this has bearish implications for the following weeks in case of the junior mining stocks.

And speaking of analogies to the past, let’s check what gold did when troops crossed borders in case of other relatively recent wars.

The arrow on the above chart shows what happened on the day when the U.S. – Iraq war started.

There was an intraday rally, but ultimately the start of the war itself was not a bullish factor for gold.

The above chart features the same thing with regard to the U.S. – Afghanistan war. Gold moved higher in the immediate aftermath, but then declined profoundly, as the tensions subsided.

You already saw the analogy to the invasion on Crimea in 2014, so you saw that there was only a short-term rally after the military action took place (in 2014, it took the following form: On 27 February, masked Russian troops without insignia took over the Supreme Council (parliament) of Crimea and captured strategic sites across Crimea.

So, while it might be contrary to one’s intuition about such events, based on the most recent historical analogies, it seems that the Ukraine-war-based rally in the precious metals sector is either over or very close to being over.

And this is even more likely to be the case with junior mining stocks. In case of the latter, it seems that we are witnessing a top in the making at this very moment.

It might be hard to view the above statement as justified in light of the huge rally in gold that we just saw, but the facts and analogies are in place nonetheless.

Technically, gold just encountered very strong resistance provided by its 2021 and late-2020 highs, and the breakout above the mid-2021 highs is not confirmed.

Let’s keep in mind that for gold to decline, the war doesn’t have to end, it doesn’t have to be won by either side. The only thing that matters with regard to it, is how big the uncertainty and concern is. And the peak uncertainty/concern might be today, as everything is new, and the situation is dramatically changing the geopolitical environment in Europe.

For comparison, remember Covid-19 cases, deaths in early 2020? That was just a tiny fraction of what we saw later. However, it was new and unknown. People were particularly scared then, and the markets moved particularly significantly then – not based on additional millions of cases and thousands of deaths next year.

Investing and trading are difficult. If it was easy, most people would be making money – and they’re not. Right now, it’s most difficult to ignore the urge to “run for cover” if you physically don’t have to. The markets move on rumor and sell the fact. This repeats over and over again in many (all?) markets, and we have direct analogies to similar situations in gold itself. And junior miners are likely to decline the most, also based on the massive declines that are likely to take place (in fact, it already started) in the stock markets.

Having said that, let’s take a look at the markets from a more fundamental point of view (please note that the fundamental parts of the analysis are prepared before the above technical/general parts, so it’s not the case that I’ve spent time writing about the fundamental issues while keeping you waiting to get the current analysis of the situation; it’s exactly the opposite, I wrote and sent it as fast as possible).

The Fed’s Fury

As more Russia-Ukraine headlines whipsaw financial assets in competing directions, the PMs were on the right side on Feb. 23. However, while I warned that geopolitical risks would likely dominate the narrative for some time, the PMs' medium-term fundamentals are heading in the wrong direction.

For example, San Francisco Fed President Mary Daly said on Feb. 23 that "I expect we will start raising rates in March, and will be raising them in subsequent meetings to get closer to neutral." In addition, she added that "the geopolitical situation is part of larger uncertainty to navigate, but is not disrupting plans for liftoff."

As a result, she concluded that "raising rates at least four times would be my preference…. Most likely, it will need more than four rate hikes."

Thus, while the PMs rally each time reports of a Russia-Ukraine escalation surface, they're ignoring the more important fundamental development. With inflation surging and the Fed poised to tighten monetary policy in less than a month, the medium-term outlooks are bullish for the USD Index and U.S. real yields, not the PMs.

Furthermore, while U.S. inflation doesn't need any help, the Russia-Ukraine saga only intensifies the pricing pressures. To explain, Russia is the third-largest oil-producing country in the world. And with the political fallout potentially disrupting global supply, higher oil prices remain problematic.

For example, reports surfaced on Feb. 23 that U.S. President Joe Biden plans to tap America's Strategic Petroleum Reserve (SPR) – which is essentially a savings account of oil that can be used when supplies shrink. For context, Biden released roughly 50 million barrels in November.

Moreover, Bob McNally, President of Rapidan Energy Group, said "it sounds like coordination planning is advanced if not about to execute." As such, The White House remains concerned about inflation derailing the U.S. economy, and in turn, its administration.

Please see below:

To that point, J.P. Morgan commodities strategists led by Natasha Kaneva told clients on Feb. 23 that "geopolitical escalation over the last few days has materially increased the risk of further aggravating commodity market imbalances. At this stage of the conflict, it is hard to see a path towards an easy de-escalation."

More importantly, though, "the world could see an extended period of elevated geopolitical tensions and high risk premium in all commodities given Russia's far reaching impact on global commodities markets."

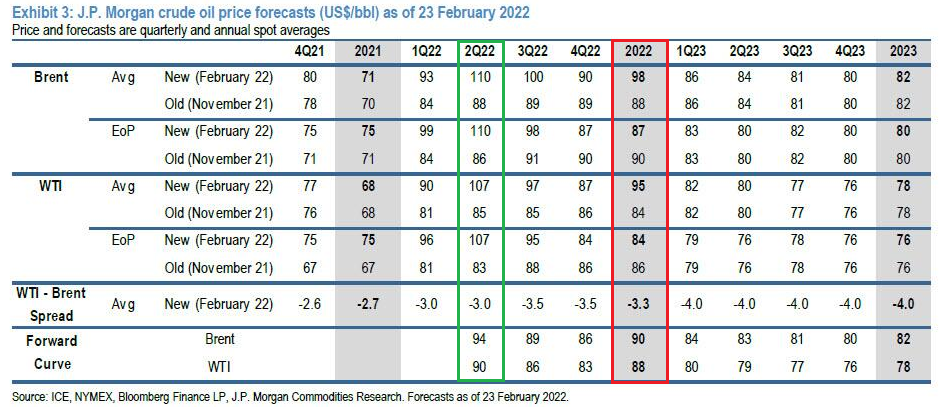

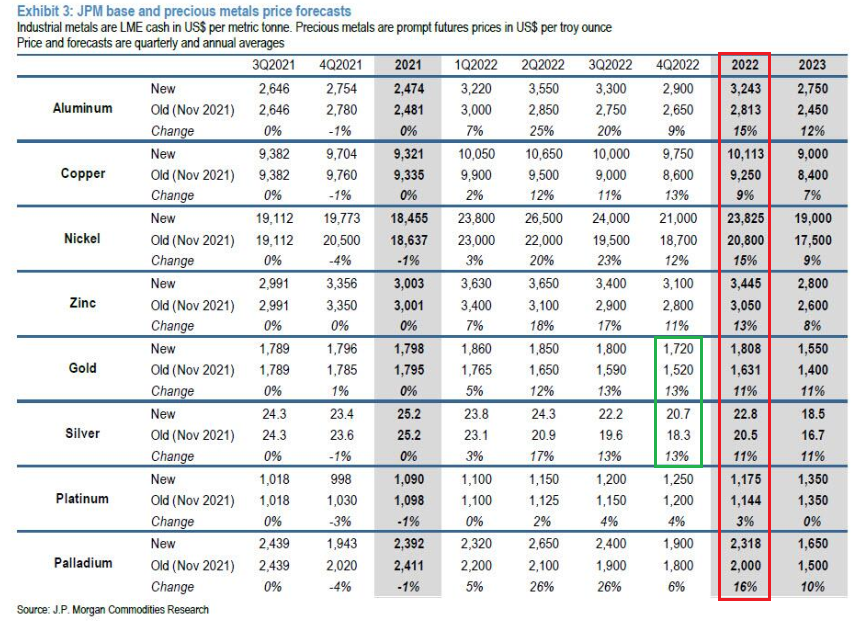

For context, since the PMs are part of the commodity complex, they should benefit from higher risk premiums. Thus, J.P. Morgan's strategists raised their year-end average price target for gold by 11%.

However, even with an invasion, J.P. Morgan expects gold to average $1,808 in 2022. For context, the initial average price target was $1,631. As a result, according to J.P. Morgan, if a de-escalation occurs, gold is significantly overvalued. Similarly, if an escalation occurs, then gold is still overvalued. Thus, however you slice it, lower prices should confront the yellow metal in the coming months.

Furthermore, while these two charts have become staples in recent Gold & Silver Trading Alerts, it's important to remember that geopolitical forces often wane over time. Likewise, investors have short attention spans, and once prevalent narratives often become irrelevant sooner rather than later. As such, we believe that J.P. Morgan's previous average price target of $1,631 is more reflective of fundamental reality.

For context, I wrote on Feb. 14:

With another dire warning from the White House uplifting gold and mining stocks on Feb. 11, Russia and Ukraine's 'will they or won't they' saga has shifted sentiment. However, it's important to remember that geopolitical risk rallies often have a short shelf life and dissipate over the medium term.

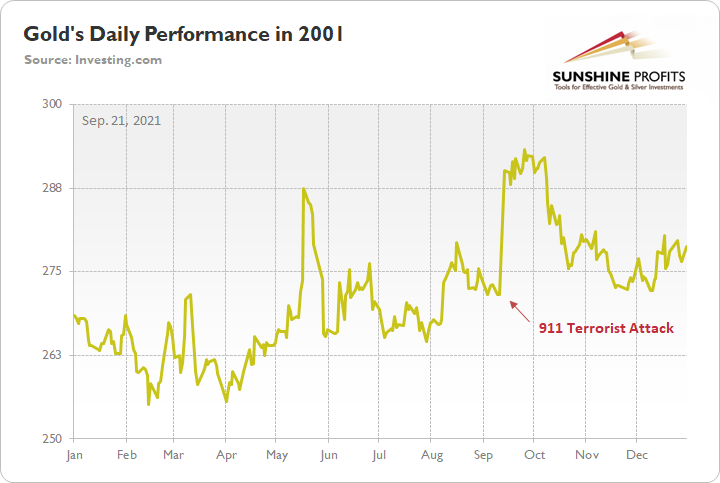

To explain, I wrote on Sep. 21:

When terrorists attacked the World Trade Center roughly 20 years ago, gold spiked on Sep. 11, 2001. However, it wasn’t long before the momentum fizzled and the yellow metal nearly retraced all of the gains by early December. Thus, when it comes to forecasting higher gold prices, Black Swan events are often more semblance than substance.

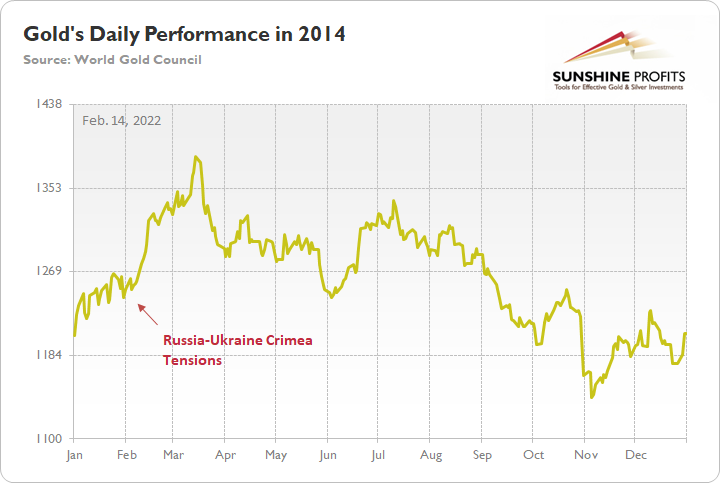

As further evidence, when Russia annexed Crimea from Ukraine in 2014, similar price action unfolded. For example, when rumors swirled of a possible invasion, gold rallied on the news. Then, when Russia officially invaded, the yellow metal continued its ascent. However, after the short-term sugar high wore off, bearish medium-term realities confronted gold once again. And in time, the yellow metal gave back all of the gains and sunk to a new yearly low.

Please see below:

Thus, while conflicting reports paint a conflicting portrait, the algorithms don’t care whether Russia invades Ukraine or not. With the rumor enough to pique investors’ interest, quantitative traders see it as an opportunity to capitalize on the momentum. However, once that momentum fizzles, history shows that the quants rush for the exits. As a result, is this time really different?

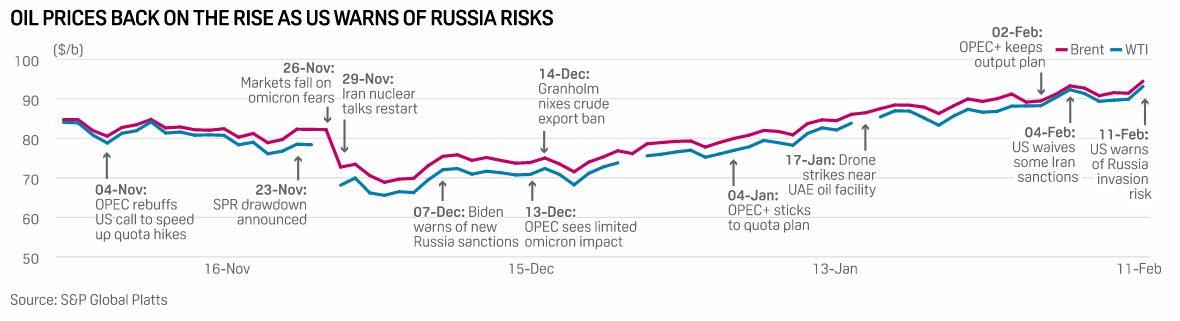

Circling back to the oil market, J.P. Morgan believes the conflict may push Brent and WTI prices to average $110 and $107, respectively, in the second quarter of 2022. And if this outcome materializes, it will only enhance inflation’s reign and put more pressure on the Fed.

Please see below:

To explain, the vertical green and red rectangles above depict J.P. Morgan’s Q2 and full-year 2022 average price targets for Brent and WTI. As you can see, the Biden Administration won’t be celebrating the potential outcomes.

On top of that, further supply shortages driven by the Russia-Ukraine conflict led J.P. Morgan to increase its full-year 2022 average price targets by 15% for aluminum, 9% for copper, 15% for nickel, 13% for zinc, 11% for gold (as mentioned), 11% for silver, 3% for platinum, and 16% for palladium. For context, the figures are listed in the vertical red rectangle below.

However, even more noteworthy, if you analyze the small vertical green rectangle below, you can see that J.P. Morgan’s updated forecasts have gold and silver averaging $1,720 and $20.70, respectively, in Q4 2022. Moreover, the old estimates had the pair averaging $1,520 and $18.30. As a result, while we expect the latter to materialize over the medium term, gold and silver are still overvalued either way.

The bottom line? While the Russia-Ukraine conflict will likely dominate the headlines and help uplift the PMs, the implications actually worsen their fundamental outlooks. For example, while industrial metals and crude supply shortages provide a fundamental thesis for higher prices, there is little risk of gold and silver supply shortages. As a result, the PMs are simply riding the bullish wave that’s swept across the commodity complex.

Furthermore, financial markets are eliciting extreme panic, and prophecies of World War 3 are now circulating. However, if NATO avoided conflict in 2014, is this time really different? Thus, if cooler heads prevail or investors tire of the continuous headlines (which happened in 2014), the PMs likely have plenty of room to fall.

In conclusion, the PMs rallied on Feb. 23, as more fear equals higher precious metals prices. However, if history is any indication, the recent rallies will fade, and lower lows should confront gold, silver and mining stocks in the coming months. Moreover, with the USD Index and U.S. real yields poised to rally as the Fed begins its rate hike cycle (likely in less than a month), these fundamental realities will likely elicit a material shift in sentiment.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is now over or very close to being over , and that gold, silver, and mining stocks are now likely to continue their medium-term decline.

- It seems that the first (bigger) stop for gold will be close to its previous 2021 lows, slightly below $1,700. Then it will likely correct a bit, but it’s unclear if I want to exit or reverse the current short position based on that – it depends on the number and the nature of the bullish indications that we get at that time.

- After the above-mentioned correction, we’re likely to see a powerful slide, perhaps close to the 2020 low ($1,450 - $1,500).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place, and if we get this kind of opportunity at all – perhaps with gold close to $1,600.

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold close to $1,350 - $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,375, but at the moment it’s too early to say with certainty.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector is likely to bottom about three months after the general stock market tops.

- The above is based on the information available today, and it might change in the following days/weeks.

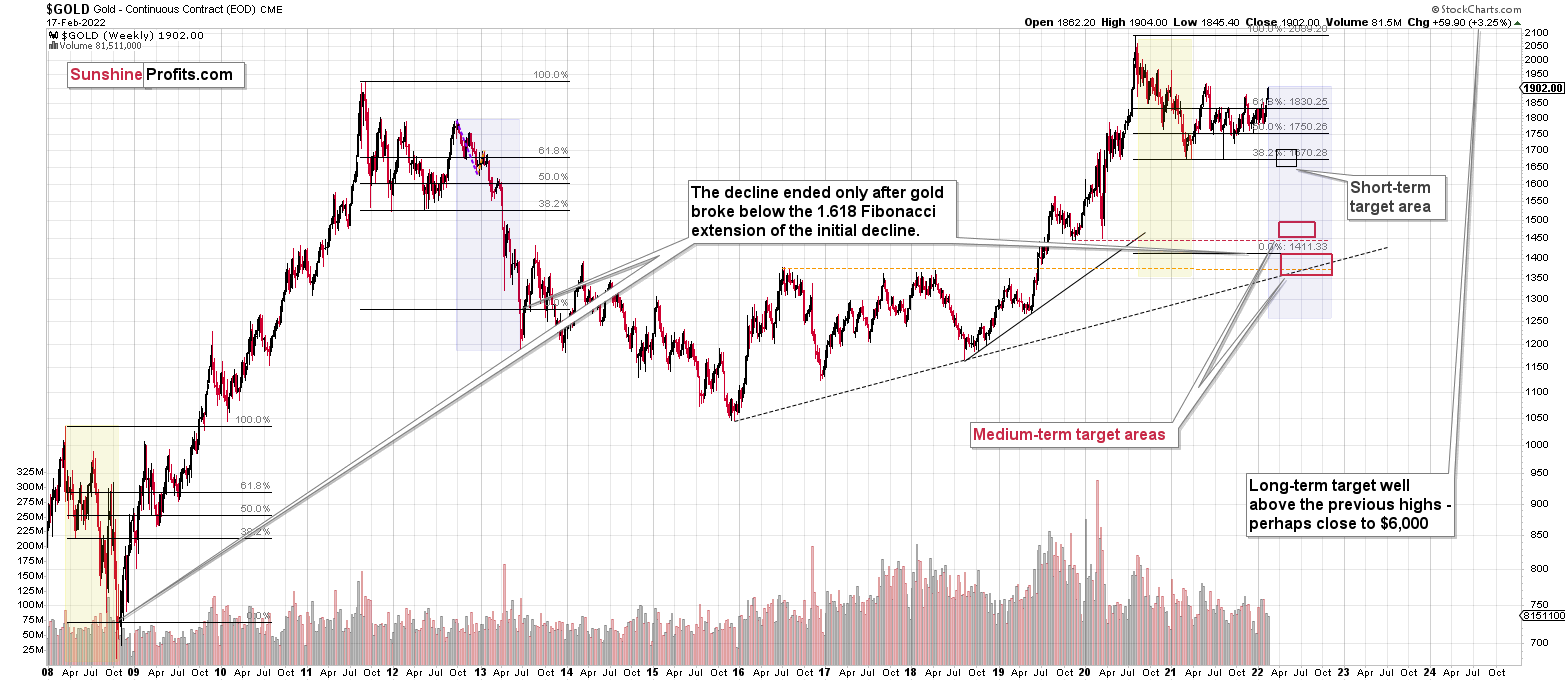

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Summary

Summing up, despite today’s rally in gold, the outlook for junior mining stocks remains exactly as I described previously.

Gold is up about $200 from its late-2021 low, just like how much it rallied in 2014 when Russia took over Crimea. When that happened, junior miners moved about 3% above their previous highs, and we see something very similar in today’s London trading of the GDXJ.

It looks like the “peak uncertainty” and “peak gold” are already here or very, very close. It’s even more likely that the top in junior mining stocks is in, or about to be in.

Investing and trading are difficult. If they were easy, most people would be making money – and they’re not. Right now, it’s most difficult to ignore the urge to “run for cover” if you physically don’t have to. The markets move on buy the rumor and sell the fact. This repeats over and over again in many (all?) markets, and we have direct analogies to similar situations in gold itself. Junior miners are likely to decline the most, also based on the massive declines that are likely to take place (in fact, it already started) in the stock markets.

Consequently, I’m keeping my short position in the GDXJ intact. In fact, as it declined in value due to recent movement, and the outlook didn’t change (in fact, the downside potential is even bigger), I just added by my short position in the junior miners. Please note that it doesn’t mean the increase of the desired position size – it’s making sure that the desired size of the position remains as I want it to be. If that’s not a clear confirmation of putting one’s money where one’s mouth is, then I don’t know what would be one.

Moreover, let’s keep in mind that there are triangle-vertex-based reversals in mid- and late-February, so even if we see more back-and-forth trading soon, it’s likely that the decline resumes later this month.

I continue to think that junior mining stocks are currently likely to decline the most out of all the parts of the precious metals sector.

From the medium-term point of view, the two key long-term factors remain the analogy to 2013 in gold and the broad head and shoulders pattern in the HUI Index. They both suggest much lower prices ahead.

It seems that our profits from the short positions are going to become truly epic in the coming months.

After the sell-off (that takes gold to about $1,350 - $1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and this March, and it seems that we’re about to make much more on the upcoming decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $34.63; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $14.98; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $25.48; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $19.12

SLV profit-take exit price: $17.72

ZSL profit-take exit price: $38.28

Gold futures downside profit-take exit price: $1,683

HGD.TO – alternative (Canadian) inverse 2x leveraged gold stocks ETF – the upside profit-take exit price: $11.79

HZD.TO – alternative (Canadian) inverse 2x leveraged silver ETF – the upside profit-take exit price: $29.48

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief