Briefly: in our opinion, small (50% of the regular size of the position) speculative long positions in gold, silver, and mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Does gold seem to have declined recently? That's true - it seems to be this way. But that's not the truth. At the moment of writing these words, gold is trading higher than it closed yesterday, higher than it had closed on Friday, and even higher than it had closed on Thursday. The intraday highs and intraday lows were both lower on each of the above-mentioned days, but after the dust settled, it turns out that nothing major really happened. Or should we say, nothing particularly bearish happened from the short-term point of view. Let's take a closer look at what gold is doing right now.

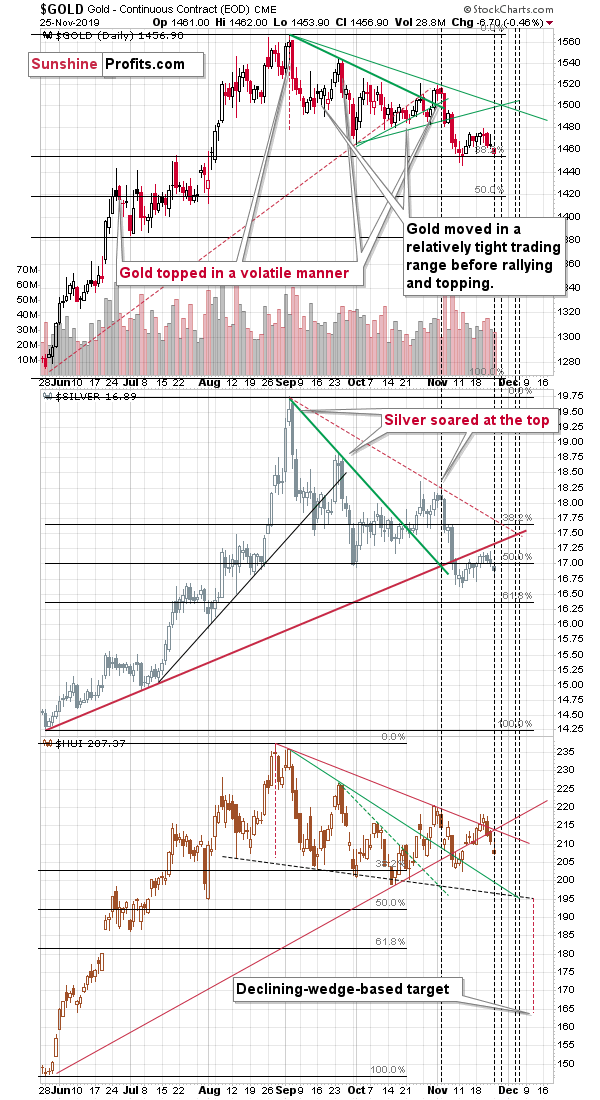

Gold's Very Short-Term

Gold moved back up after touching its 61.8% Fibonacci retracement based on the mid-November upswing. This is a very short-term pullback within a short-term rally, nothing else.

The 61.8% retracement is the most classic of them all, as it's directly based on the Phi number. Long story short, this number is ubiquitous in many places in nature, and since people are part thereof and they are active in markets, perhaps it would be present in the market movement. It turns out that it is indeed present, and it quite often works remarkably well as a tool to detect support or resistance levels. At times, it can be used to make forecasts by multiplying one of the previous moves by 1.618. And, well, it tends to work quite often, despite there being theoretically no specific reason (other than mentioned above) why 1.618 should work, and not 1.792 or 1.123 or any other random number above 1.0.

This time, this level suggested a rebound and - voila - that's exactly what we saw in today's pre-market trading. Of course, the session is far from being over, and it could all change before the closing bell, but the odds are that it won't.

The below chart shows three more things.

Precious Metals Short-Term

One thing is that the shape of the recent price movement in gold doesn't resemble what we saw at the previous local tops. Conversely, it resembles the consolidations that took place before the final - and biggest - part of the short-term upswings.

Second thing is that the previous tops were accompanied by silver's strong outperformance and we definitely don't see this kind of strength right now.

Third thing is that yesterday was the first of the triangle-vertex-based reversals, which means that given yesterday's daily decline, the precious metals sector is now likely to move higher. And that's exactly what's taking place right now.

Based on the following three reversals, it seems that we'll see the next local top this or the next week.

But what about the short-term, what else can we say about our long position opened right after the November 12 reversal? Apart from outlining the take-profit targets, the full version of this analysis dives into the short-term indication from the gold miners. Similarly, the long-term interest rates are sending a valuable signal of its own to act upon. Bottom line, these are invaluable tools in planning when and where to profitably switch market sides - just as our preceding success with the earlier short position. Please note that you can still subscribe to these Alerts at very promotional terms - it takes just $9 to read the details right away, and then receive follow-ups for the next three weeks. Profit along with us.

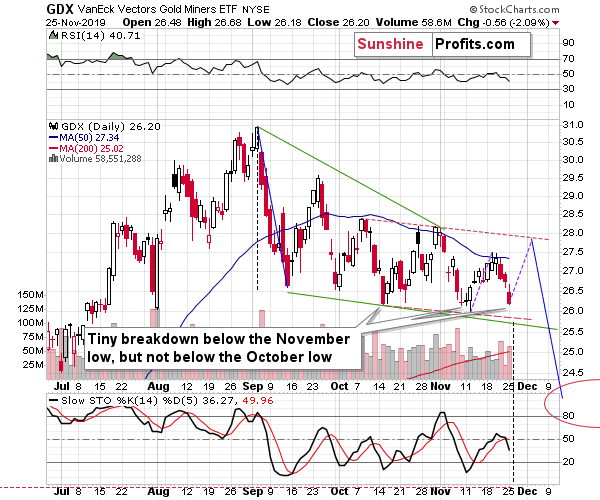

The Gold Miner Have Their Say

Some may say that the close in the GDX ETF below the previous November low is a major breakdown. It isn't. The move was not confirmed and GDX didn't break below the October low.

Interestingly, if the GDX rallies from here in a way that's very similar to how it rallied earlier in November, it will move exactly to our price target in early December - and that's to the letter what we've been writing about for days.

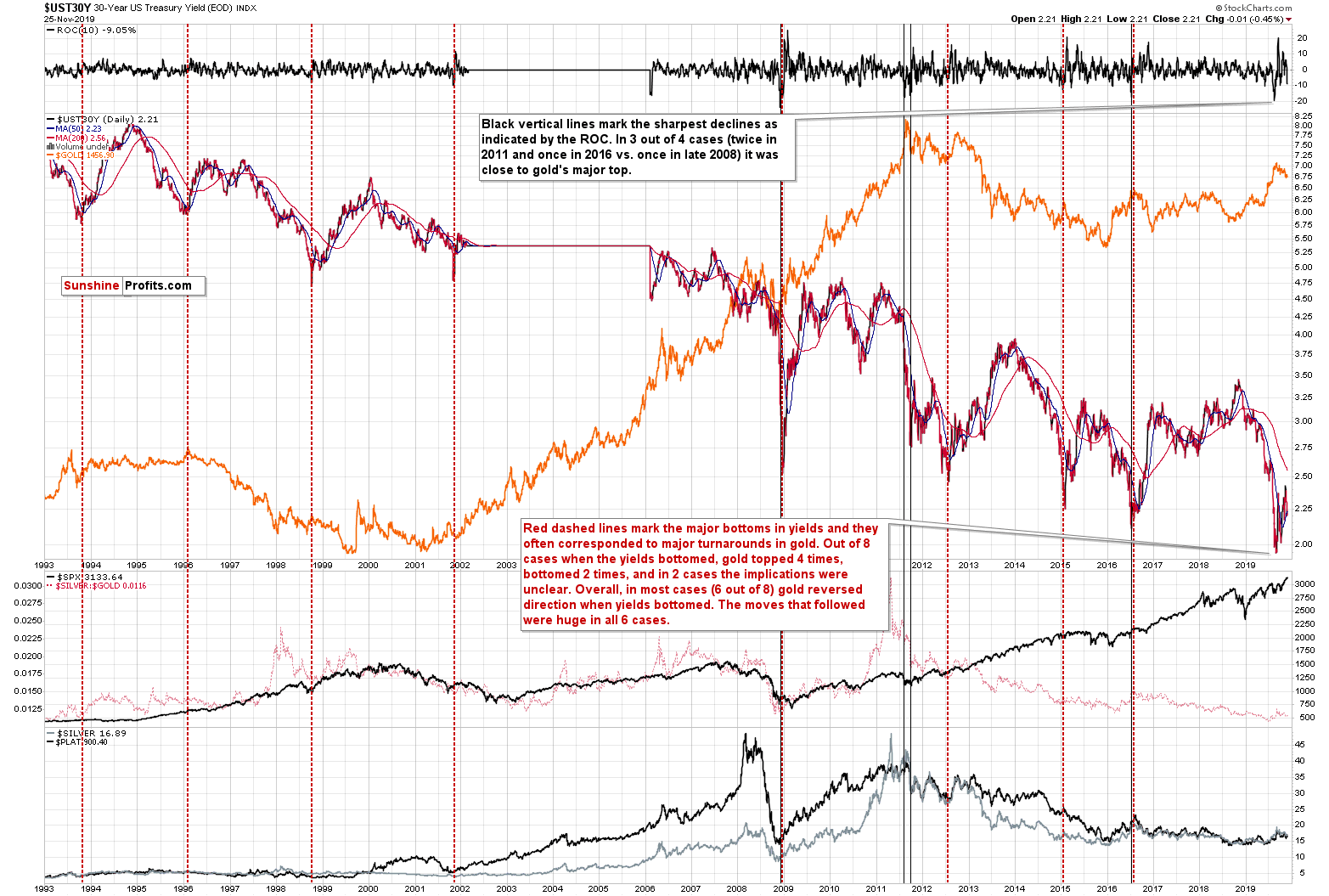

Before summarizing, let's examine one of the long-term charts that emphasizes what's likely to happen in the following months. This time, we'll take a closer look at the link between gold and the very long-term interest rates.

Gold Performance and Interest Rates

On September 26th, we wrote the following regarding the above chart (the quote is quite long, but it's definitely worth your time, if you haven't read the above-mentioned Alert):

As the Fed turned dovish this year, not only did the short-term interest rates move down - the long- and very-long-term ones also declined. Why would this be the case? After all, the long-term rates are set by market forces, not through Fed's direct decision... More importantly, though, why should you, the precious metals investor, care? What kind of signal does it send to the gold market for the following months and years?

It's not that the Fed directly controls the long-term rates that is the issue here - it doesn't.

The long-term interest rates are based on supply and demand, which are in turn based on market expectations. After all, markets are forward looking.

And what does the Fed provide in addition to interest rate decisions? Forward guidance.

Year after year, public debts have been increasing across the world's most advanced economies, and it's becoming increasingly obvious that this debt cannot be repaid using regular revenue of the official sector (taxes). The debt can be repudiated but that's an unthinkable proposition - take a look at how Greece's efforts turned out. Realistically, the debt will need to be inflated away... Or maybe it won't have to be. After all, in the scenario where long-term interest rates go below zero, the debt is no longer ballooning due to interest. Either way, the interest rates are likely to be lower in the long run based on the above. This is the core of financial repression - artificially low rates. But that's just one of the reasons.

The direct comments from the Fed clearly support the above - the rates are getting lower and that's happening even without incoming data that would support a rate cut. All the talk about the Fed being data-driven didn't amount to much after Trump started openly criticizing Fed and demanding rates be cut. He delivered the "trade risk" which served as justification of a rate cut. That's not an official statistic the Fed was supposed to follow - it's smoke and mirrors that helps to keep rates in a long-term downtrend. Then, it's no wonder that forward-looking investors expect rates to be lower in the following years, not only months. What does it imply for gold? In the very long term it's very bullish, because when the risk-free rate goes to (or below) zero, an asset that doesn't yield any interest becomes much more desirable. In normal circumstances, it's better to have an interest-yielding asset than one without. But when the long-term interest rates go below zero and investors can't earn money through bonds, gold will be a much better alternative. Especially when it outshines inflation.

The key thing to keep in mind is that the above is a long-term fundamental factor. It doesn't tell us where the market will move either in the short term or in the medium term. It's practically a factor of zero importance for day trading.

The markets are forward looking, which means that they are already discounting the above taking place and they aim to frontrun the obvious consequences even before they occur. The markets discount more than news and fundamentals, though. They also discount investors and traders' emotions for people tend to get ahead of themselves in terms of expectations and reactions to news. Consequently, the market could get ahead of itself and then decline regardless of the fundamental situation being positive. Or it might be in a medium-term downtrend and forced to move against it based on series of unexpected events. How do we know what price movement is real and which one is fake? The truth is that one can never be 100% certain with regard to any price movement. However, there is a way to detect what is likely and what's not. That happens by comparing the current situation to similar cases in the past and how consistently the follow-up actions unfolded. That's more or less what technical analysis is all about. There are more sophisticated techniques, but the overall general rule is as simple as the above.

So, without further ado, let's take a look at what the very long-term (30-year) interest rates are currently doing and how similar cases impacted the gold market in the past.

In short, we recently saw a huge drop in the long-term rates. It was neither the first one, nor the biggest one though. We saw similar developments several times in the previous years, and the 2008 drop was the most significant one.

Long-term rates are definitely in a long-term downtrend, but they are not declining in a straight line. There are big slides, just like the one that we saw recently, and there are upswings that take up to- or even over a year. The rates moved to new lows recently and then rallied back above the previous lows. This suggests that the short- or even medium-term bottom in the rates is in. Moreover, that's exactly what happened in 2015 and 2016, and gold topped at both lows in the rates. Of course, these are not the only cases when the rates bottomed, so let's check what happened in all previous cases since 1993.

Not taking into account the August top, out of 8 cases when the 30-year Treasury yields bottomed, gold topped 4 times, it bottomed twice and in the 2 remaining cases, the implications were unclear. In other words, gold rallied in only 25% of cases (in 2001 and 2013), but in both cases the exact bottom in gold took place along with the bottom in the rates. This means that in both cases when the implications were bullish, gold declined beforehand. This was definitely not the case recently. Gold topped along with the bottom in the rates in August, which makes it similar to the 4 cases when the slide and bottom in the rates were actually great shorting opportunities for gold traders.

This means that while the overall trend lower in rates is positive for gold for the following years, the very recent slide in rates does not have bullish implications for the short or even medium term. Whatever bullish action was likely to happen based on it, is likely already behind us.

Please take a look at what happened with the long-term interest rates at the 1996 top. This is particularly important, because based on what's happening in the USD Index, the current situation is just like what we saw in the mid-90s. The long-term interest rates formed a short-term bottom, then they rallied for a few months, consolidated and then declined once again for more than a year. And you know what happened in gold? Gold declined for practically the entire time. It even declined after the rates bottomed in 1998. That's exactly what we might see in the following months.

The USD Index is likely to soar next year (quite likely also this year) and while the rates might move lower in the long run, they are likely to bounce in the short term. And gold? It has likely topped just as it did in early 1996, and is now starting a major decline even though it's likely to move higher in the next several days.

Key Factors to Keep in Mind

Critical factors:

- The USD Index broke above the very long-term resistance line and verified the breakout above it. Its huge upswing is already underway.

- The USD's long-term upswing is an extremely important and bearish factor for gold. There were only two similar cases in the past few decades, when USD Index was starting profound, long-term bull markets, and they were both accompanied by huge declines in gold and the rest of the precious metals market

- Out of these two similar cases, only one is very similar - the case when gold topped in February 1996. The similarity extends beyond gold's about a yearly delay in reaction to the USD's rally. Also the shape of gold price moves prior to the 1996 high and what we saw in the last couple of years is very similar, which confirm the analysis of the gold-USD link and the above-mentioned implications of USD Index's long-term breakout.

- The similarity between now and 1996 extends to silver and mining stocks - in other words, it goes beyond USD, gold-USD link, and gold itself. The white metal and its miners appear to be in a similar position as well, and the implications are particularly bearish for the miners. After their 1996 top, they erased more than 2/3rds of their prices.

- Many investors got excited by the gold-is-soaring theme in the last few months, but looking beyond the short-term moves, reveals that most of the precious metals sector didn't show substantial strength that would be really visible from the long-term perspective. Gold doesn't appear to be starting a new bull market here, but rather to be an exception from the rule.

- Gold stocks appear to be repeating their performance from 20 years ago, which means that a bottom in the entire precious metals sector is quite likely to form at much lower prices, in about a year

Very important, but not as critical factors:

- Long-term technical signs for silver, i.a. the analogy in terms of price to what we saw in 2008, shows that silver could slide even below $10.

- Silver's very long-term cycles point to a major reversal taking place right now and since the most recent move was up, the implications are bearish (this is also silver's technical sign, but it's so important that it deserves its own point)

- Long-term technical signs for gold stocks point to this not being a new gold bull market beginning. Among others, it's their long-term underperformance relative to gold that hint this is rather a corrective upswing within a bear market that is not over yet.

- Record-breaking weekly volume in gold is a strong sign pointing to lower gold prices

Important factors:

- Extreme volume reading in the SIL ETF (proxy for silver stocks) is an effective indication that lower values of silver miners are to be expected

- Silver's short-term outperformance of gold, and gold stocks' short-term underperformance of gold both confirm that the precious metals sector is topping here

- Gold topped almost right at its cyclical turning point, which makes the trend reversal more likely

- Copper broke below its head-and-shoulders pattern and confirmed the breakdown. The last time we saw something similar was in April 2013, when the entire precious metals sector was on the verge of plunging lower.

Moreover, please note that while there may be a recession threat, it doesn't mean that gold has to rally immediately. Both: recession and gold's multi-year rally could be many months away - comparing what happened to bond yields in the 90s confirms that.

Summary

Summing up, the outlook for the precious metals sector remains very bearish for the following months (also because of the record open interest in gold), but it seems that we will first see a short-term upswing before the decline continues. Based on what we saw in the last few days, the bullish outlook remains justified. It seems that the profits on our long positions will become bigger before we close it. We expect to close the long position this or next week. Then, we plan to open a short position shortly thereafter.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Small speculative long position (50% of the full position) in gold, silver, and mining stocks is justified from the risk/reward perspective with the following stop-loss orders and binding exit profit-take price levels:

- Gold: profit-take exit price: $1,489.80; stop-loss: $1,437; initial target price for the UGLD ETN: $135.88; stop-loss for the UGLD ETN: $122.10

- Silver: profit-take exit price: $17.47; stop-loss: $16.27; initial target price for the USLV ETN: $89.33; stop-loss for the USLV ETN: $72.44

- Mining stocks (price levels for the GDX ETF): profit-take exit price: $27.88; stop-loss: $25.47; initial target price for the NUGT ETF: $30.27; stop-loss for the NUGT ETF $23.08

In case one wants to bet on junior mining stocks' prices, here are the stop-loss details and target prices:

- GDXJ ETF: profit-take exit price: $39.27; stop-loss: $35.38

- JNUG ETF: profit-take exit price: $67.97; stop-loss: $49.83

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that the in the trading section we describe the situation for the day that the alert is posted. In other words, it we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices, so that you can decide whether keeping a position on a given day is something that is in tune with your approach (some moves are too small for medium-term traders and some might appear too big for day-traders).

Plus, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one, it's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade) we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGLD, DGLD, USLV, DSLV, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (DGLD for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and DGLD as still open and the stop-loss for DGLD would have to be moved lower. On the other hand, if gold moves to a stop-loss level but DGLD doesn't, then we will view both positions (in gold and DGLD) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels on a daily basis for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Editor-in-chief, Gold & Silver Fund Manager