Briefly: in our opinion, full (250% of the regular size of the position) speculative short position in gold, silver, and mining stocks is justified from the risk/reward point of view at the moment of publishing this Alert.

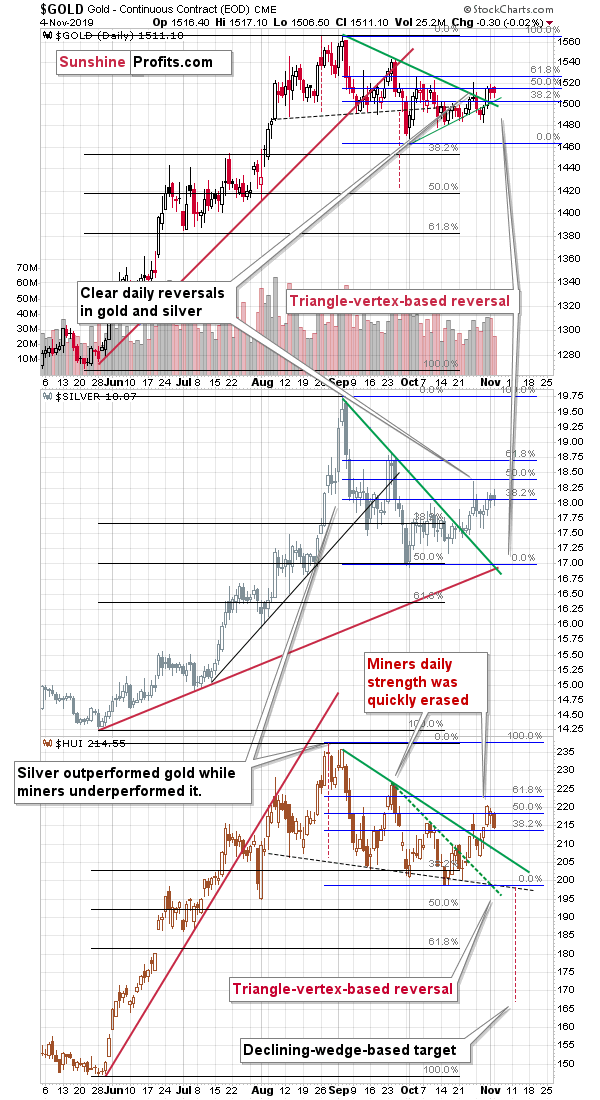

In yesterday's analysis, we wrote that there were some positive signs for gold and mining stocks, but that one should not take them at face value. We also mentioned that the potential upside for gold was relatively limited to the late-September top, and that the outlook didn't really stop being bearish. The preceding rally - we stated - actually had bearish implications because of the triple triangle-vertex-based reversal. And what did the precious metals market do? It declined right after the reversal.

Examination of the PMs Reversal

Gold declined only a bit yesterday, but the move continues in today's pre-market trading at the moment of writing these words.

And it was not only gold that declined. The move in silver was negligible, but the mining stocks declined rather profoundly. To be clear, the move was not huge on a stand-alone basis, but given the relatively small decline that we saw yesterday in gold, miners did move significantly.

The HUI Index declined, erasing the daily strength that raised bullish hopes at the end of October. It also closed well below the previous intraday high and very close to the October 25 closing price. Moreover, it closed in the proximity to the 38.2% Fibonacci retracement. Gold didn't do the above, which means that miners' short-term outperformance is likely over. This means that what seemed as something that could indicate further gains, was most likely nothing more than a short-term price noise.

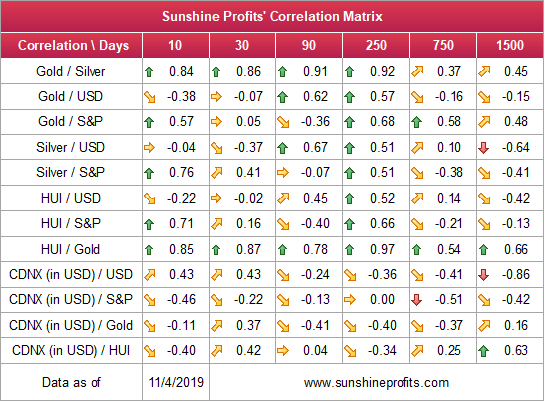

One of the reasons behind strong performance of mining stocks could have been the recent rally in the general stock market. Let's take a look at our Correlation Matrix for details.

The 10-trading-day column for HUI / S&P 500 Index shows significant correlation of 0.71. Why? Because in the last two weeks, two markets have been moving in tune with each other. "Correlation doesn't imply causation" is generally true, but in this case it's quite obvious that the entire market (dog) influences how a part of the market - gold stocks (tail) moves (wags).

Please note that the analogous reading for silver is 0.76, which also explains to some extent why silver was reluctant to decline recently. Silver has many industrial uses, so in the short run it's likely to move in tune with stocks every now and then. That's the case, because increased demand for silver from companies that use it can be linked with overall good performance of these companies, which in turn is linked with how the stock indexes such as S&P 500 perform.

One would expect this relationship to wane over time, because ultimately silver has its own supply and demand combination that determines its prices. And indeed - as we move further to the right in the above table, the Silver / S&P 500 correlations become (on average) lower and finally move into the negative territory in case of the very long-term correlation coefficients.

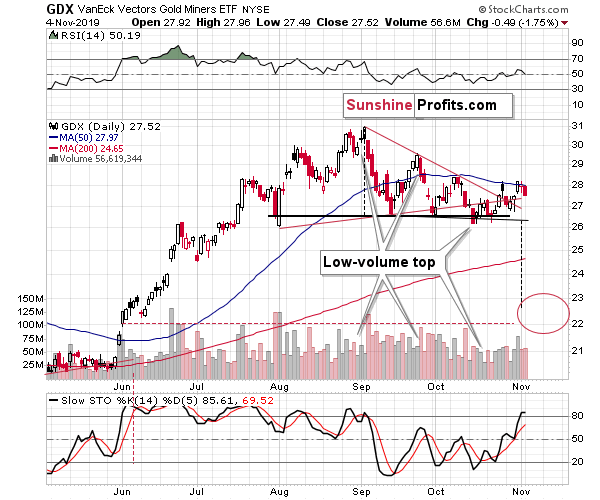

Let's move back to the mining stocks. Maybe it was a coincidence that the HUI Index declined and other proxies for the miners don't confirm it?

The truth is exactly the opposite.

The GDX ETF declined even more on a relative basis and it closed below the October 25th closing price, thus invalidating the breakout above it. The volume was not extremely high, but it was not low either, which is exactly what one might expect to see at the beginning of a decline.

away, because there's a 30-day money back guarantee. Subscribe today.

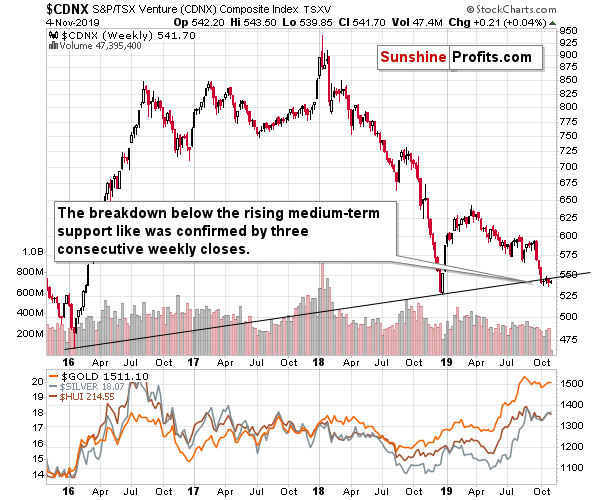

And what about the junior mining stocks?

Juniors Also Concur

The juniors broke significantly below the rising support line and they confirmed the breakdown below it. They are still moving back and forth below it, but given the breakdown, it's very likely that it's only a matter of time before another big wave down starts. Please note that it was the initial part of the big 2018 slide in juniors that was accompanied by the year's biggest decline in gold, silver, and senior miners.

Confirmed breakdown and consolidation below the broken support is exactly what one sees before the initial part of the move. In fact, some may already view this consolidation as the first part of the decline. The implications for the precious metals market are strongly bearish.

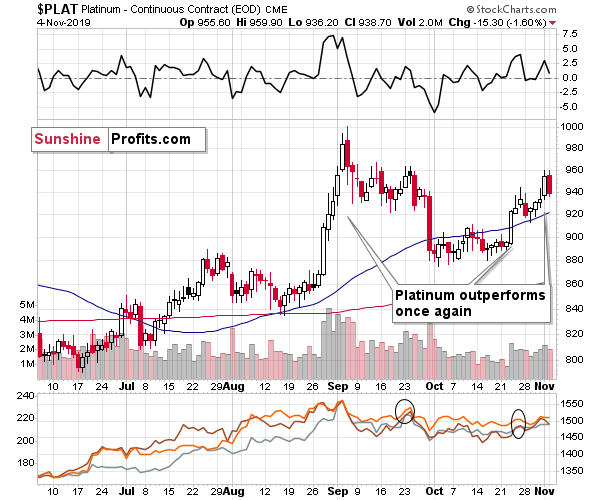

Before summarizing, let's take a look at the platinum price movement.

And So Does Agree Platinum

In late October, after platinum's big daily rally, we wrote the following:

The first detail is that any market that is generally weak, but then acts strong at a certain time, might simply be rallying just because everything is rallying as the investment public (that enters the market last and buys close to the top) is buying everything without looking at its potential. And in particular if something looks cheaper than something else (e.g. because it was declining previously or precisely because it has unfavorable fundamentals). This means that just by looking at the performance of the weak parts of a given market one can detect the moment, when the investment public is entering the fray, and thus that the top is being formed.

The second detail is that platinum is currently the weakest part of the precious metals sector and this perfectly fits the above-mentioned type of reaction. The size of the platinum market is also relatively small. The fundamental situation for platinum is rather grim as it's being used as a catalyst for diesel car engines that are no longer as often produced as in the past. Gasoline engines are growing in popularity relative to the former and in their case, palladium is used. Both could be hit when electric cars start to take over the market, but that's something that will take many years. The fundamental outlook is one source of information and the technical situation is another one [and the decline in the platinum to gold ratio confirms the above].

The rally that we saw in platinum in August confirmed the end of a multi-week rally in the precious metals sector. Yesterday's upswing in "la platina" may not seem significant enough to matter, but let's keep in mind that gold, silver, and mining stocks are currently after a small rally that took several days, not after a several-month-long one. Consequently, just a daily - but significant - show of strength from platinum may be enough to confirm that the top is in, or very close to being in.

The above-mentioned strength in platinum was indeed followed by a small decline in gold, silver, and mining stocks, but - just like platinum - they moved higher once again. But, platinum outperformed gold and showed strength once again. This means that the above-mentioned sell signal is now even more prominent.

Naturally, the other key bearish factors for the medium term remain intact.

Key Factors to Keep in Mind

Critical factors:

- The USD Index broke above the very long-term resistance line and verified the breakout above it. Its huge upswing is already underway.

- The USD's long-term upswing is an extremely important and bearish factor for gold. There were only two similar cases in the past few decades, when USD Index was starting profound, long-term bull markets, and they were both accompanied by huge declines in gold and the rest of the precious metals market

- Out of these two similar cases, only one is very similar - the case when gold topped in February 1996. The similarity extends beyond gold's about a yearly delay in reaction to the USD's rally. Also the shape of gold price moves prior to the 1996 high and what we saw in the last couple of years is very similar, which confirm the analysis of the gold-USD link and the above-mentioned implications of USD Index's long-term breakout.

- The similarity between now and 1996 extends to silver and mining stocks - in other words, it goes beyond USD, gold-USD link, and gold itself. The white metal and its miners appear to be in a similar position as well, and the implications are particularly bearish for the miners. After their 1996 top, they erased more than 2/3rds of their prices.

- Many investors got excited by the gold-is-soaring theme in the last few months, but looking beyond the short-term moves, reveals that most of the precious metals sector didn't show substantial strength that would be really visible from the long-term perspective. Gold doesn't appear to be starting a new bull market here, but rather to be an exception from the rule.

- Gold stocks appear to be repeating their performance from 20 years ago, which means that a bottom in the entire precious metals sector is quite likely to form at much lower prices, in about a year

Very important, but not as critical factors:

- Long-term technical signs for silver, i.a. the analogy in terms of price to what we saw in 2008, shows that silver could slide even below $10.

- Silver's very long-term cycles point to a major reversal taking place right now and since the most recent move was up, the implications are bearish (this is also silver's technical sign, but it's so important that it deserves its own point)

- Long-term technical signs for gold stocks point to this not being a new gold bull market beginning. Among others, it's their long-term underperformance relative to gold that hint this is rather a corrective upswing within a bear market that is not over yet.

- Record-breaking weekly volume in gold is a strong sign pointing to lower gold prices

Important factors:

- Extreme volume reading in the SIL ETF (proxy for silver stocks) is an effective indication that lower values of silver miners are to be expected

- Silver's short-term outperformance of gold, and gold stocks' short-term underperformance of gold both confirm that the precious metals sector is topping here

- Gold topped almost right at its cyclical turning point, which makes the trend reversal more likely

- Copper broke below its head-and-shoulders pattern and confirmed the breakdown. The last time we saw something similar was in April 2013, when the entire precious metals sector was on the verge of plunging lower.

Moreover, please note that while there may be a recession threat, it doesn't mean that gold has to rally immediately. Both: recession and gold's multi-year rally could be many months away - comparing what happened to bond yields in the 90s confirms that.

Summary

Summing up, the outlook for the precious metals sector remains very bearish for the following weeks and months and given the current triple reversal it might be the case that the counter-trend rally is already over. If, however, the similarity to how gold performed in 2011 remains intact, we might see a quick run-up to about $1530 - $1,540 in gold futures before gold slides once again.

Naturally, one might prefer to take advantage of the above-mentioned bullish possibility, but it seems that given gold's downside potential, the risk to reward ratio continues to favor keeping the current short position intact. Also, given the possibility that gold forms a temporary bottom close to $1,460, we are going to strongly consider closing the current short position or even entering long position once it gets there. However, we are not adjusting the binding exit prices for the current trade, because the $1,460 support is not as strong as the combination of the factors that made us place the targets at their current levels.

Time will also be an important factor here. If gold moves close to $1,460 around mid-December, the odds are that it will reverse there. But, if gold quickly slides to e.g. $1,450 before the end of November, while gold miners underperform, then it will serve as a strong indication that gold is likely to fall further before starting a counter-trend rally. In this case, we will not automatically close our positions even though the $1,460 level is (b)reached.

The profits from the short position in gold, silver and mining stocks are likely to be legendary, but the difficult part is not to miss the decline, which is why we're rather reluctant to exit the short position very often.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short position (250% of the full position) in gold, silver, and mining stocks are justified from the risk/reward perspective with the following stop-loss orders and binding exit profit-take price levels:

- Gold: profit-take exit price: $1,391; stop-loss: $1,573; initial target price for the DGLD ETN: $36.37; stop-loss for the DGLD ETN: $25.44

- Silver: profit-take exit price: $15.11; stop-loss: $19.06; initial target price for the DSLV ETN: $24.88; stop-loss for the DSLV ETN: $14.07

- Mining stocks (price levels for the GDX ETF): profit-take exit price: $23.21; stop-loss: $30.11; initial target price for the DUST ETF: $14.69; stop-loss for the DUST ETF $6.08

In case one wants to bet on junior mining stocks' prices, here are the stop-loss details and target prices:

- GDXJ ETF: profit-take exit price: $30.32; stop-loss: $41.22

- JDST ETF: profit-take exit price: $35.88 stop-loss: $12.46

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that the in the trading section we describe the situation for the day that the alert is posted. In other words, it we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices, so that you can decide whether keeping a position on a given day is something that is in tune with your approach (some moves are too small for medium-term traders and some might appear too big for day-traders).

Plus, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one, it's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade) we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGLD, DGLD, USLV, DSLV, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (DGLD for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and DGLD as still open and the stop-loss for DGLD would have to be moved lower. On the other hand, if gold moves to a stop-loss level but DGLD doesn't, then we will view both positions (in gold and DGLD) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels on a daily basis for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Additionally, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA

Editor-in-chief, Gold & Silver Fund Manager