Briefly: in our opinion, full (300% of the regular position size) speculative short positions in mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Welcome to this week's flagship Gold & Silver Trading Alert. As we’ve promised you previously, in our flagship Alerts, we will be providing you with much more comprehensive and complex analyses (approximately once per week), which will usually take place on Monday.

Predicated on last week’s price moves, our most recently featured outlook remains the same as the price moves align with our expectations. On that account, there are parts of the previous analysis that didn’t change at all in the earlier days, which will be written in italics.

Let’s start with a quick discussion of last week’s news regarding the spending in the U.S. In short, Biden’s speech to Congress was fundamentally positive for gold and something that’s likely to contribute to much higher gold prices in the long run.

Last week was full of big events. The FOMC released its newest statement on monetary policy meeting, while Powell held the press conference. On the same day, President Biden made his first speech to Congress. Let’s take a look at his words.

First of all, Biden laid his American Jobs Plan out, which proposes more than $2 trillion to upgrade the US infrastructure and create millions of jobs. No matter that infrastructure spending has no stimulus effect, according to economic research.

Second, if you think that $2 trillion is a lot of money, given America’s huge indebtedness, you are clearly wrong. Two trillions is practically nothing and definitely not enough, so Biden proposed another $1.8 trillion American Family Plan in investments and tax credits to provide lower-income and middle-class families with inexpensive childcare.

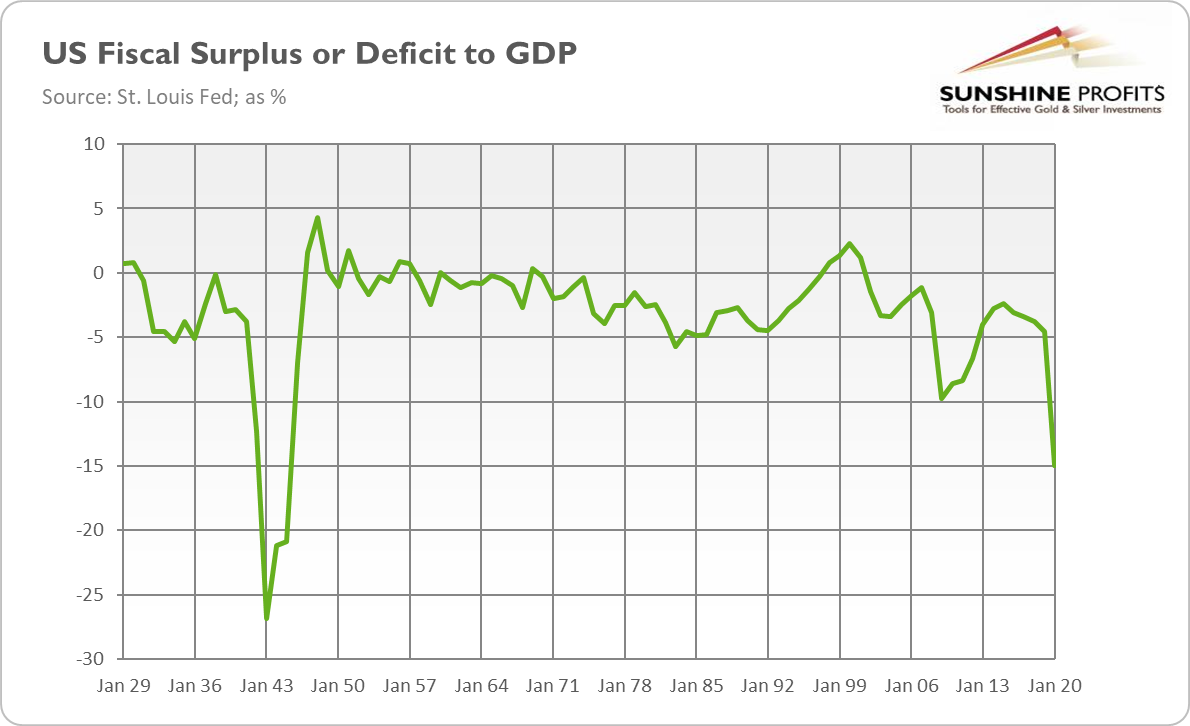

Third, Biden understands that all these expenditures cannot be funded solely by increasing already huge fiscal deficits (see the chart below) and issuing new bonds.

So, he proposed a hike in tax rates:

It’s time for corporate America and the wealthiest 1% of Americans to pay their fair share. Just pay their fair share (…) We take the top tax bracket for the wealthiest 1% of Americans –

those making $400,000 or more – back up to 39.6%.

No matter that corporate taxes are implicit taxes on labor and that the current proposals for tax hikes are unlikely to fund the White House’s ambitious plans.

Biden also proposed several reforms of the labor market: a 12-week of paternal leave for families and an increase of the minimum wage to $15 an hour.

So, in short, his speech called for several bold economic policies aiming to increase the government spending and strengthen the American welfare state. Sounds good… for gold.

What does the Biden speech, and more generally his economic agenda, imply for the precious metals market? Well, it seems that the President cares not only about the workers, but also about the gold bulls. His plan is fundamentally positive for the yellow metal. After all, Biden wants to further increase government spending, which will weaken the long-term pace of economic growth and add to the mammoth pile of the public debt.

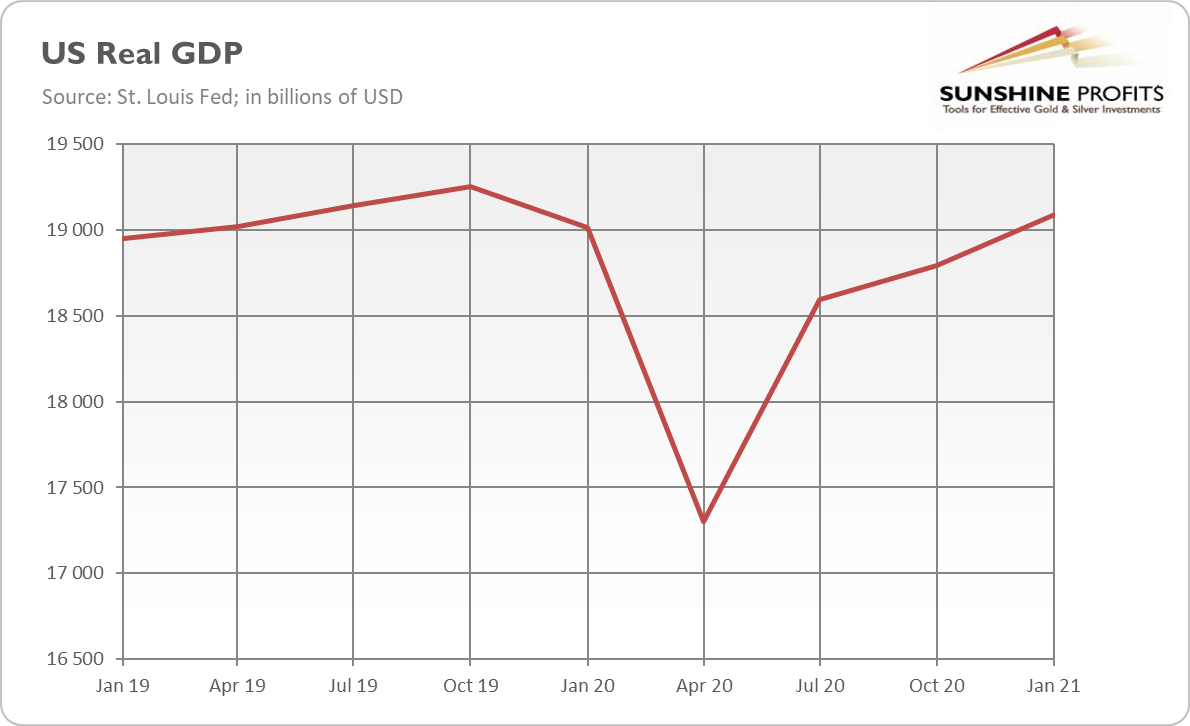

There are also hints that this massive government spending flowing directly to the citizens could ignite inflation. After all, the US economy has already recovered from the pandemic recession, at least in the GDP terms, as the chart below shows. So, Biden’s economic agenda risks that the economy will overheat igniting inflation.

He also adopted a more confrontational stance toward China, which could elevate the geopolitical worries and increase the demand for safe-haven assets such as gold.

Another potential benefit is the proposal to raise corporate taxes, which is clearly negative for the US stock market and the greenback. Hence, gold could gain at their expense, especially if we see a pullback in the equity market…

Last but not least, the increase in the minimum wage, and other labor market reforms, will not help in a quick employment recovery, so the Fed will maintain its dovish policy for longer. Indeed, we should look at the Biden’s message together with the Fed’s signals. Biden proposed trillions of dollars in new spending, while Powell reiterated no hurry to raise interest rates. What a policy mix! We have both easy monetary policy and loose fiscal policy, a golden policy mix, indeed.

Gold didn’t react strongly to these events, which indicates that long-term implications can be one thing, and what’s going to happen in the markets in the short- and medium-term can be quite another thing. Based on multiple technical reasons, it seems that gold has completed its short-term corrective upswing and is now ready to decline substantially once again.

But before moving to the technical details, let’s consider how the cross-asset implications could affect the precious metals in the coming weeks.

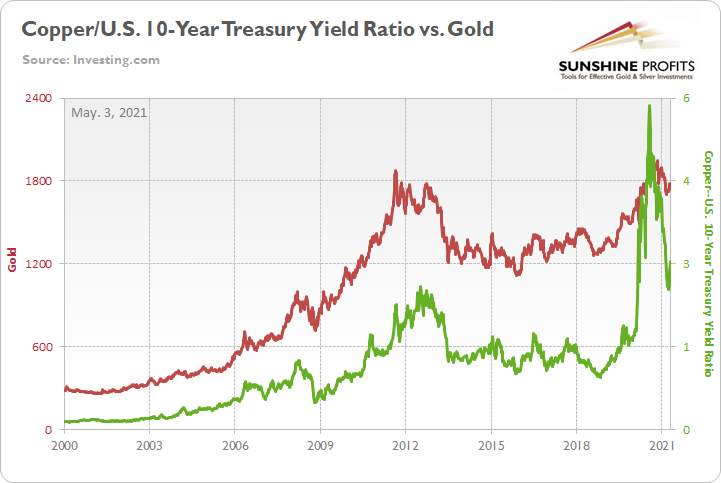

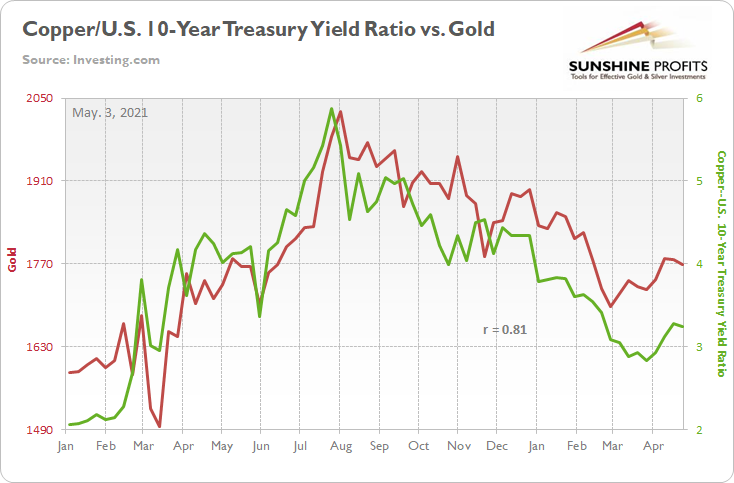

Over the medium-to-long-term, the copper/U.S. 10-Year Treasury yield ratio is a leading indicator of gold’s future behavior.

I wrote previously:

When the copper/U.S. 10-Year Treasury yield ratio is rising (meaning that copper prices are rising at a faster pace than the U.S. 10-Year Treasury yield), it usually results in higher gold prices. Conversely, when the copper/U.S. 10-Year Treasury yield ratio is falling (meaning that the U.S. 10-Year Treasury yield is rising at a faster pace than copper prices), it usually results in lower gold prices.

If you analyze the chart below, you can see the close connection:

Peaking and rolling over within days of one another, gold and the copper/U.S. 10-Year Treasury yield ratios have been in sync since August. And with the latter declining by 1.42% last week, while the former fell by 0.47%, the yellow metal continues to follow in the ratios’ footsteps.

Please see below:

Moreover, while the U.S. 10-Year Treasury yield’s recent consolidation has helped uplift the yellow metal, the Treasury benchmark could be nearing the end of its short-term correction. Case in point: after holding its 50-day moving average and moving higher last week, the U.S. 10-Year Treasury yield may have formed a medium-term bottom.

Please see below:

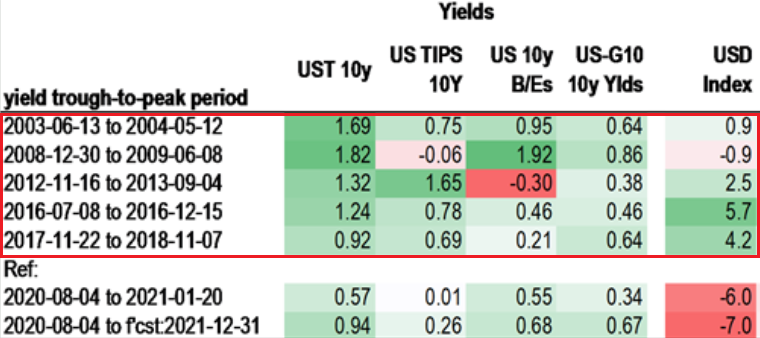

In addition, after defying historical precedent for all of 2020, the USD Index is beginning to mirror the behavior of the U.S. 10-Year Treasury yield. If you analyze the table below, you can see that a bottom (and a subsequent move higher in the U.S. 10-Year Treasury yield) has coincided with a rise in the USD Index 80% of the time since 2003.

And while the former’s decline has weighed heavily on the latter, the continuation of the U.S. 10-Year Treasury yield’s medium-term uptrend should help propel the USD Index higher.

The bottom line? With gold exhibiting a strong negative correlation with the U.S. dollar, if a revitalized USD Index enters the equation, it will add even more concrete to gold’s wall of worry.

On the flip side, if we extend our time horizon, there are plenty of fundamental reasons why gold is likely to soar in the coming years. However, even the most profound bull markets don’t move up in a straight line, and corrections are inevitable.

As it relates to the precious metals, a significant correction (medium-term downtrend) is already underway. However, the pain is not over, and a severe climax likely awaits.

For context, potential triggers are not always noticeable, and the PMs may collapse on their own or as a result of some random trigger that normally wouldn’t cause any major action. However, a trigger will speed things up, and that’s where the S&P 500 comes in:

S&P 500 (SPX) Signals

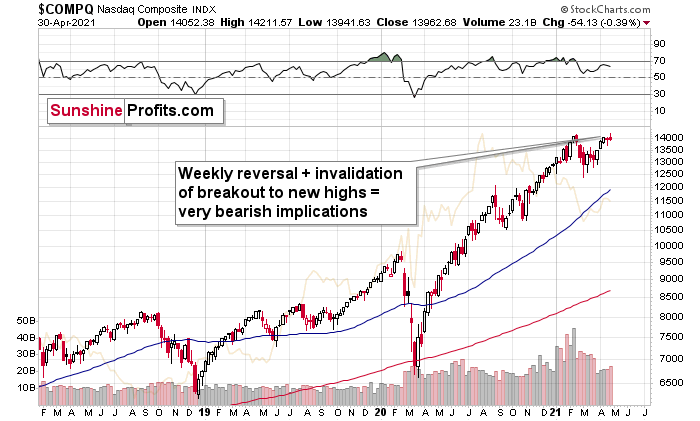

After reversing all of its late-week gains on Apr. 30 and ending the week roughly flat, there is much more to the S&P 500’s about-face than meets the eye. Case in point: not only did the NASDAQ Composite suffer a weekly decline, but it invalidated the breakout to new highs and formed a weekly shooting star candle. For context, a shooting star candle signals a bearish reversal when formed during an uptrend.

Please see below:

More importantly, though, while the ominous trifecta paints a bearish portrait of the NASDAQ Composite’s medium-term outlook, the developments also put the precious metals’ market on high alert. To explain, I’ve mentioned on several occasions that the PMs – based on how they performed in the past - might bottom approximately three months after the stock market tops. Thus, if last week’s rejection solidifies a medium-term top for the NASDAQ Composite, then the PMs are likely to suffer three more months (or so) of bearish price action.

It was not clear what date should one use as the starting point of the three-month countdown, and based on what we saw last week, it seems quite clear now.

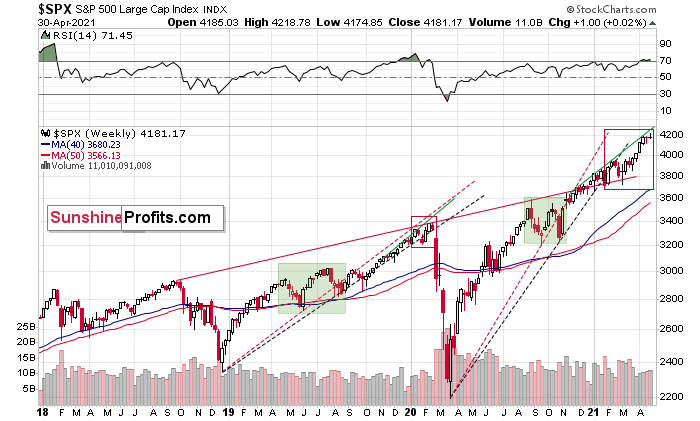

Circling back to the S&P 500, not only is the U.S. equity benchmark likely to follow the NASDAQ Composite lower – given that the six largest companies in the NASDAQ Composite (Apple, Microsoft, Amazon, Tesla, Facebook and Alphabet) are also the six largest companies in the S&P 500 – but the S&P 500 also remains fully-entrenched in its 2018-2019 analogue:

To explain, I wrote previously:

Despite April’s nonfarm payrolls report buoying the S&P 500 above 4,000, the U.S. equity benchmark is still following its 2018-2019 script. Back then, the S&P 500 recorded a sharp move higher, consolidated (with heightened volatility, which I marked with a green box below), continued its uptrend, then suffered a material drawdown. And over the last 12 months, the S&P 500 has already completed the first three steps.

But how did it unfold?

Well, if you analyze the green-shaded area on the left side of the chart, you can see that the S&P 500’s breakdown below the black and red lines (that are based on the previous bottoms) was accompanied by increased volatility. From there, the rally continued before the stock market eventually collapsed.

Analogous to today’s price action, we’ve already witnessed the first three scenes from the theatrical performance. Only this time, the S&P 500 hasn’t plunged… Yet.

However, because fits and starts signal an identical outcome, after breaking below its red and black dashed rising support lines in 2020 and 2021 (on the right side of the chart), the S&P 500 is still trading below both levels. Furthermore, the heightened volatility that unfolded from August to October is a tell-tale sign that the 2018-2019 analogue could eventually rear its ugly head.

In addition, the S&P 500’s RSI (Relative Strength Index) currently signals overbought conditions. Approaching 72, prior readings of this magnitude preceded major tops in 2020 and heightened volatility in 2021.

Keep in mind though: a decline in stocks is not required for the PMs to decline. But a break in the former could easily trigger a sell-off in the latter, and if history decides to rhyme again, silver and the miners will be the hardest hit.

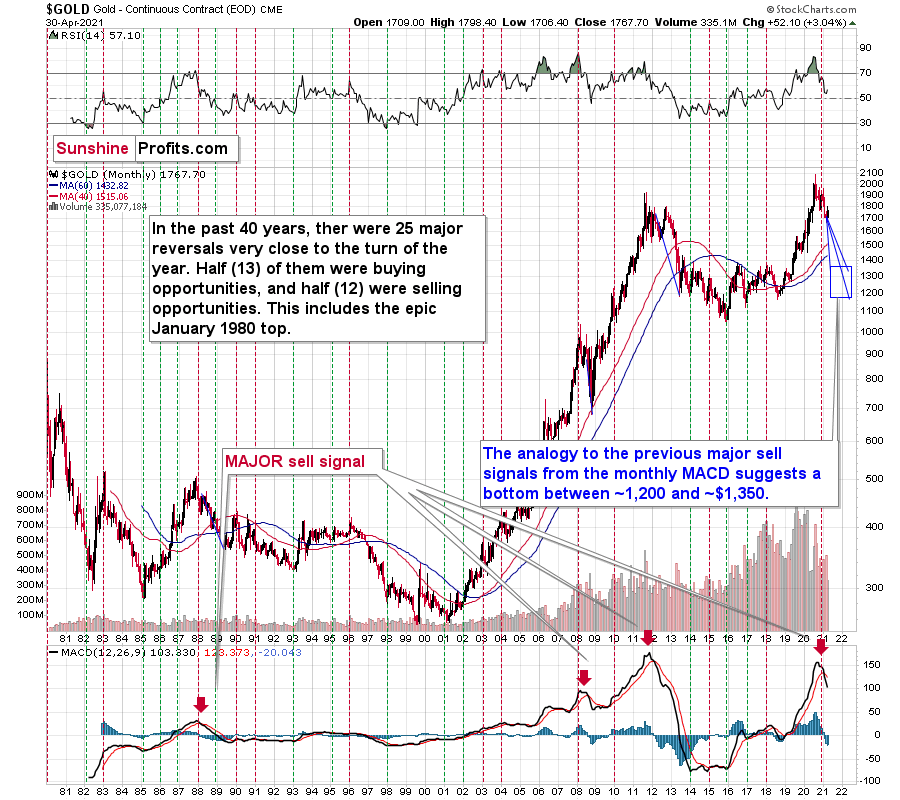

Very Long-term MACD Sell Signal for Gold

Blinded by gold’s recent strength, precious metal investors often can’t see the forest through the trees. Case in point: despite the yellow metal’s recent corrective upswing, the move was immaterial when analyzing from a monthly perspective. And with April’s monthly close doing nothing to disrupt the MACD indicator’s sell-signal – and because countertrend rallies are expected within a medium-term downtrend – gold’s outlook remains profoundly bearish over the next few months.

To explain, I wrote previously:

With February’s monthly close the last piece of the puzzle, the MACD indicator’s sell-signal is now perfectly clear. If you analyze the chart below (at the bottom right), you can see that the MACD line has crossed the signal line from above – a development that preceded significant drawdowns in 2008 and 2011.

Based on gold’s previous performance after the major sell signals from the MACD indicator, one could now expect gold to bottom in the ~$1,200 to ~1,350 range. Given the price moves that we witnessed in 1988, 2008 and 2011, historical precedent implies gold forming a bottom in this range. However, due to the competing impact of several different variables, it’s possible that the yellow metal could receive the key support at a higher level.

Only a shade below the 2011 high, today’s MACD reading is still the second-highest reading in the last 40 years. More importantly though, if you analyze the chart below (the red arrows at the bottom), the last four times the black line cut through the red line from above, a significant drawdown occurred.

Also ominous is that the magnitude of the drawdowns in price tend to coincide with the magnitude of the preceding upswings in MACD. And with today’s reading only surpassed by 2011, a climactic move to the $1,250/$1,450 range isn’t out of the question for gold. The above is based on how low gold had previously declined after a similarly important sell signal from the MACD

Now, the month is not over yet, so one might say that it’s too early to consider the sell signal that’s based on monthly closing prices, but it seems that given the level that the MACD had previously reached and the shape of the top in the black line, it makes the situation so similar to 2011/2012 that the sell signal itself is just a cherry on the bearish analytical cake.

Considering the reliability of the MACD indicator a sell signal for major declines, the reading also implies that gold’s downtrend could last longer and be more severe than originally thought. As a result, $1,500 remains the most likely outcome, with $1,350 still in the cards.

The USD Index (USDX)

After delivering a ferocious 0.75% rally on Apr. 30 – the greenback’s largest single-day gain since Mar. 4 – the USD Index let out a roar that was heard across all corners of the financial markets. And while gold, silver and mining stocks are still cackling in disobedience – as evidenced by the trios’ decelerating correlations over the last 10 days – every once in a while, the lion has to show the jackals who he is.

To explain, as the USD Index’s recent plight elicits whispers of a new order in the currency kingdom, the greenback’s stoic behavior has been misjudged as weakness. And while the vultures circle and prophecies of the USD Index’s demise become louder, the lion is slowly moving to his feet.

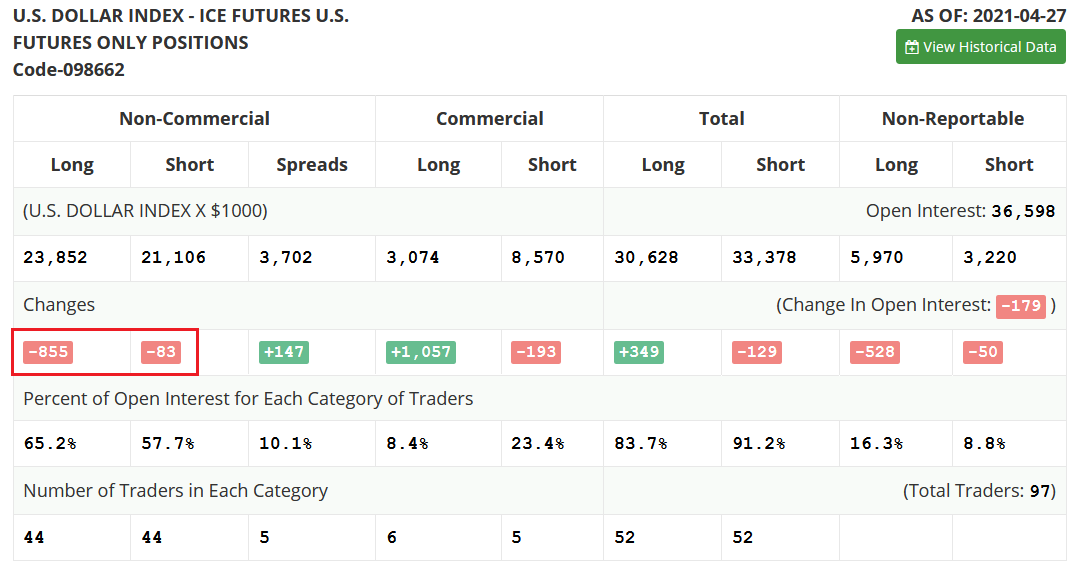

Case in point: with the zeitgeist forecasting new lows for the greenback, non-commercial (speculative) futures traders are still holding firm. Despite the greenback’s suffering, the immaterial decline in net-long positioning last week was relatively muted and highlights investors’ quiet respect for the U.S. dollar.

Please see below:

Source: COT

Source: COT

Moreover, with prior periods of extreme pessimism followed by monumental rallies in the USD Index, unless ‘this time is different,’ it’s simply a matter of when, not if, the U.S. dollar feasts on the precious metals’ overconfidence.

To explain, I wrote previously:

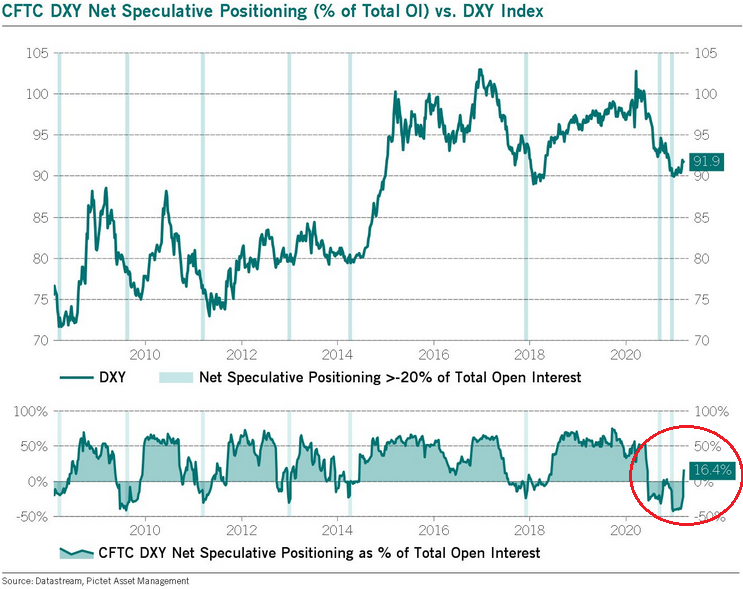

When net-speculative short interest as a percentage of total open interest (based on the CoT data) became extremely high in 2014 and 2018, the USD Index recoded two of its sharpest rallies in history. How sharp? Well, let’s take a look at how things developed in the past – after all, history tends to rhyme.

Let’s focus on what happened when the net speculative positions were significantly (!)negative and then they became significantly (!) positive, without paying attention to any tiny moves (like the one that we saw last summer).

In short, rallies that followed periods of extreme pessimism include:

- The big 2008 rally (over 16 index points)

- The big 2009 – 2010 rally (over 14 index points)

- The 2011 – 2012 rally (over 11 index points)

- The 2013 rally (“only” over 5 index points)

- The big 2014 – 2015 rally (over 20 index points)

- The 2018 rally (over 15 index points)

The current rally started at about 89, so if the “normal” (the above shows what is the normal course of action) happens, the USD Index is likely to rally to at least 94, but since the 5-index point rally seems to be the data outlier, it might be better to base the target on the remaining 5 cases. Consequently, one could expect the USD Index to rally by at least 11 – 20 index points, based on the net speculative positions alone. This means the upside target area of about 105 – 114. Consequently, a comeback to the 2020 highs is not only very likely, but also the conservative scenario.

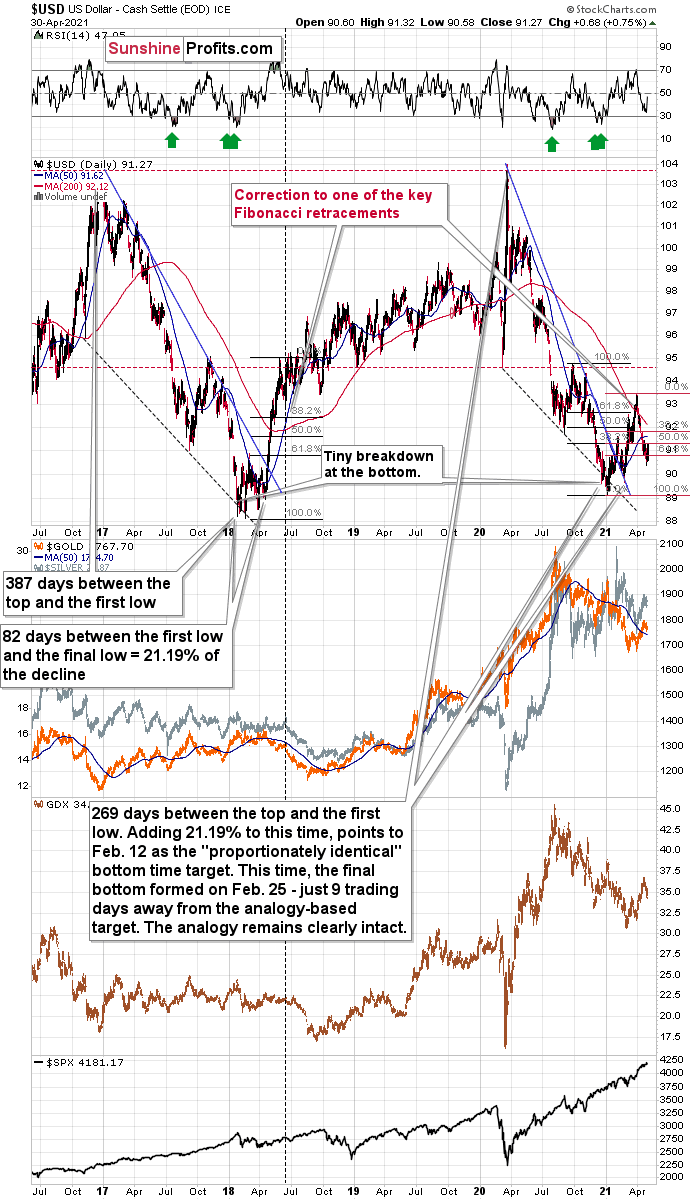

In addition, let’s keep in mind that the very bullish analogy to the 2018 rally remains intact. If you analyze the chart below, you can see that back in 2018, the USD Index rallied sharply and then corrected back to (roughly) the 38.2% Fibonacci retracement level. And while the current decline is of a much larger magnitude than what we saw in mid-April 2018, the USD Index is still following its June 2018 analogue by declining slightly below another critical Fibonacci retracement – the 61.8% one. Moreover, amid the greenback’s surge on Apr. 30 – which I warned was forthcoming – the USD Index invalidated its breakdown below the 61.8% Fibonacci retracement level. The bottom line? The sharp reversal is extremely bullish for the U.S. dollar.

More importantly, though, when the USD Index resumed its uptrend in June 2018 – marked by the vertical dashed line near the middle of the chart – the measured move higher also coincided with an accelerated drawdown of gold, silver and mining stocks.

Please see below:

To explain, I wrote on Apr. 21:

I marked the situation from 2018 that seems similar to what we see right now with a dashed, horizontal line. Back in 2018, the pullback ended when the USD Index moved to its first Fibonacci classic retracement level (the 38.2% one). In case of the current rally, it seems that another classic retracement worked – the 61.8% one.

The very important detail about the June 2018 decline (and bottom) is that while this was the moment after which the USD Index’s started to move higher at a slower pace, it was also the moment after which the precious metals market started to decline faster.

At the beginning of the year, I wrote that the precious metals market was likely to decline and that the preceding rally was likely fake. That’s exactly what happened.

Right now, I’m writing that the recent rally was also fake (a correction within a medium-term decline) and – even more importantly – it seems likely that the next downswing could take place at a higher pace than what we saw so far this year. And – just as was the case in 2018 – this upcoming (fast) decline is likely to lead to the final bottom in the precious metals sector.

As further evidence, I warned on Apr. 30 that the USD Index was ripe for a reversal. And while entering long positions in the USD Index is an appetizing thought, shorting the gold miners offers much more bang for our buck.

I wrote (with regard to possible long positions in the USD Index futures):

I would be looking to re-enter long positions as soon as the USD Index confirms the breakout above the declining resistance line. At the moment of writing these words, the USDX is already trading back above this line, so the only thing that it needs to do now is to stay there. Still, given today’s pre-market movement, it seems that we might even see an invalidation of the move below the 61.8% Fibonacci retracement. A weekly close above both levels would be very bullish for the short term and a sign for me to get back to the long positions.

But – that is all based on the assumption that I would want to have any position in the USDX. And I don’t because I think that having a short position in mining stocks provides a much better risk-to-reward ratio.

That’s exactly what we saw – a weekly close above both levels.

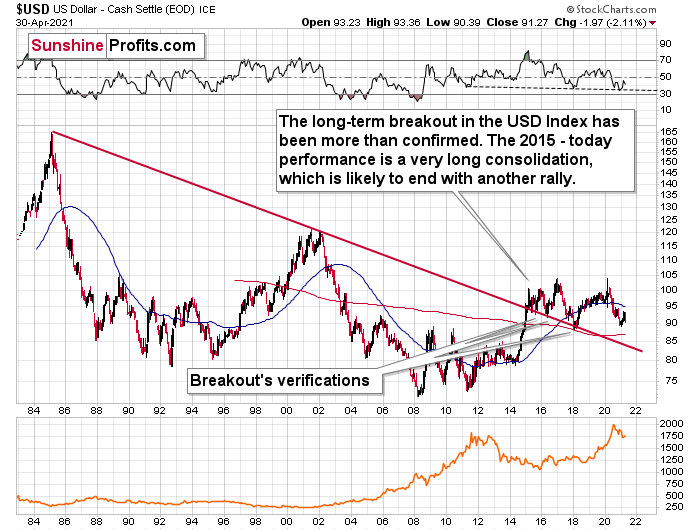

Adding even more ferocity to the USD Index’s roar, the recent downtrend has not invalidated its long-term breakout. And with the long-term implications taking precedence over the medium- and short-term ones, the USDX’s uptrend remains intact.

Please see below:

The bottom line?

Given the magnitude of the 2017-2018 upswing, ~94.5 is likely the USD Index’s first stop. In the months to follow, the USDX will likely exceed 100 at some point over the medium or long term.

Keep in mind though: we’re not bullish on the greenback because of the U.S.’ absolute outperformance. It’s because the region is doing (and likely to do) better than the Eurozone and Japan, and it’s this relative outperformance that matters, not the strength of just one single country or monetary area. After all, the USD Index is a weighted average of currency exchange rates, and the latter move on a relative basis.

In conclusion, with mischievous market participants nipping and clawing at the USD Index’s mane, it’s only a matter of time before the greenback strikes back with a vengeance. And while the precious metals consider the USD Index’s territory up for grabs, the greenback’s pride is unlikely to stay hidden for much longer. As a result, while gold, silver and mining stocks’ gaze across the grassland, the sun has likely set on their recent rallies. However, once the wet season washes away the litany of financial-market imbalances, the eventual bloom will allow the precious metals to grow stronger in the long run.

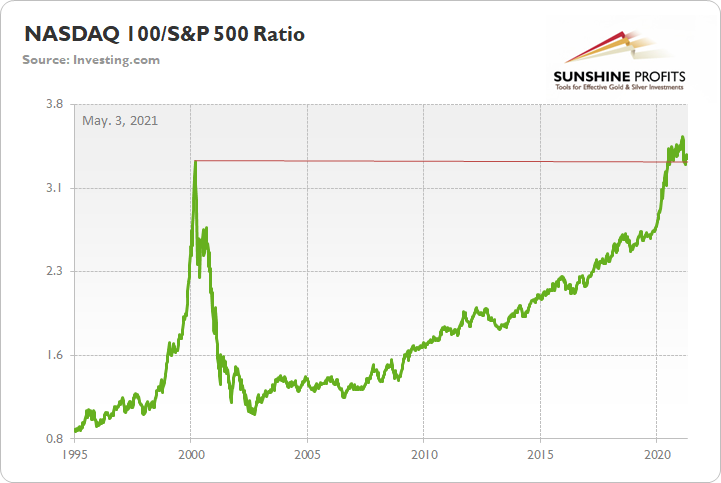

As another potential upside catalyst, a material drawdown of the NASDAQ 100 could eventually rattle U.S. equities. And with the NASDAQ 100/S&P 500 ratio still above its dot-com bubble peak, a reversion to the mean will likely elicit plenty of fireworks.

To that point, given the USDX’s strong negative correlation with the NASDAQ 100, a material reset could propel the greenback back to its March highs. Moreover, following a short-term consolidation, the USDX could even exceed those previous highs.

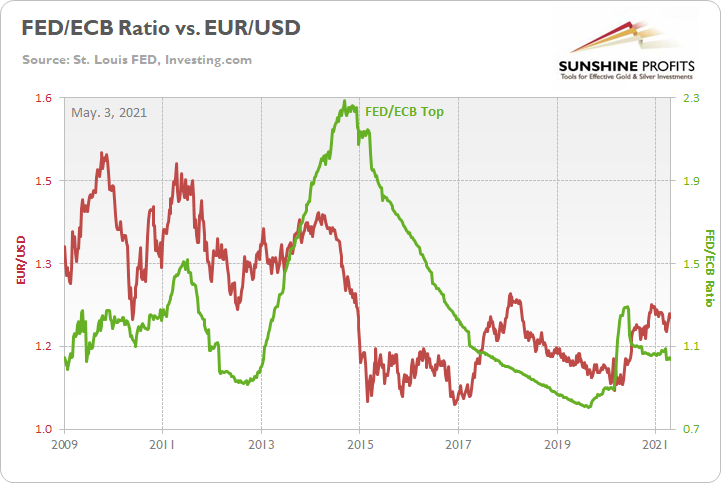

As for the FED/ECB ratio, relative outprinting by the European Central Bank (ECB) remains of critical importance. Last week, the ratio declined by 0.98%, while the EUR/USD fell by 0.65%. Moreover, given that the ratio has declined by more than 19% since May, by nearly 5% over the last five weeks and is showing a material divergence on the right side of the chart below, the EUR/USD still has some catching up to do.

Please see below:

The key takeaway?

With the ECB injecting more liquidity to support an underperforming Eurozone economy, the FED/ECB ratio, as well as EUR/USD, should move lower over the medium term. More importantly, though, because the EUR/USD accounts for nearly 58% of the movement of the USD Index, EUR/USD pain will be the USDX’s gain.

In addition, the top in the FED/ECB total assets ratio preceded the slide in the EUR/USD less than a decade ago, and it seems to be preceding the next slide as well. If the USD Index was to repeat its 2014-2015 rally from the recent lows, it would rally to 114. This level is much more realistic than most market participants would agree on.

The Gold Miners

After investors heralded the GDX ETF’s prior breakout as a game-changer, somber signals from several other ratios were singing a different tune. And with the latter’s negativity casting a shadow over the former – which I warned was forthcoming on Apr. 26 – the GDX ETF suffered a 4.71% drawdown last week.

Please see below:

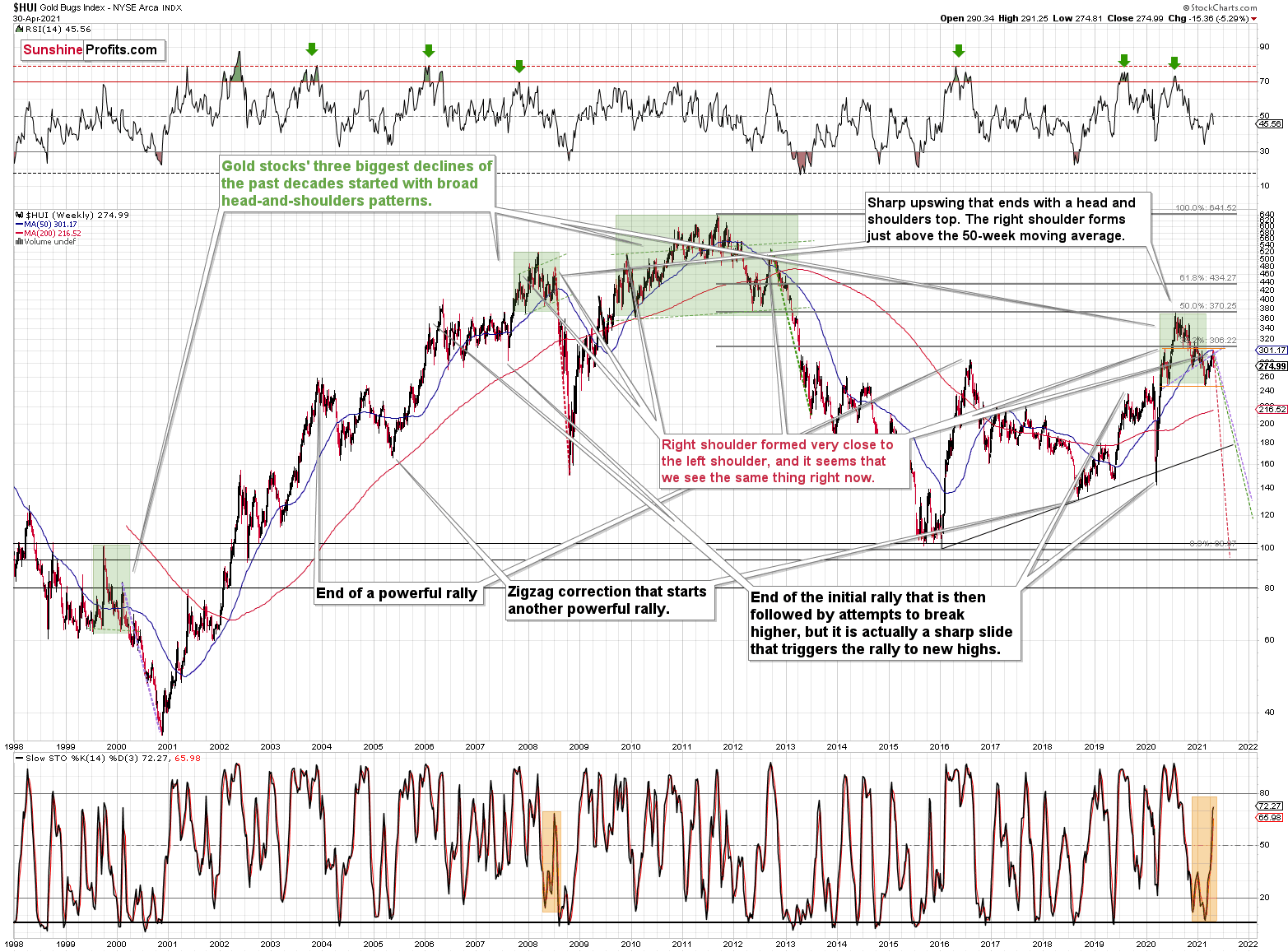

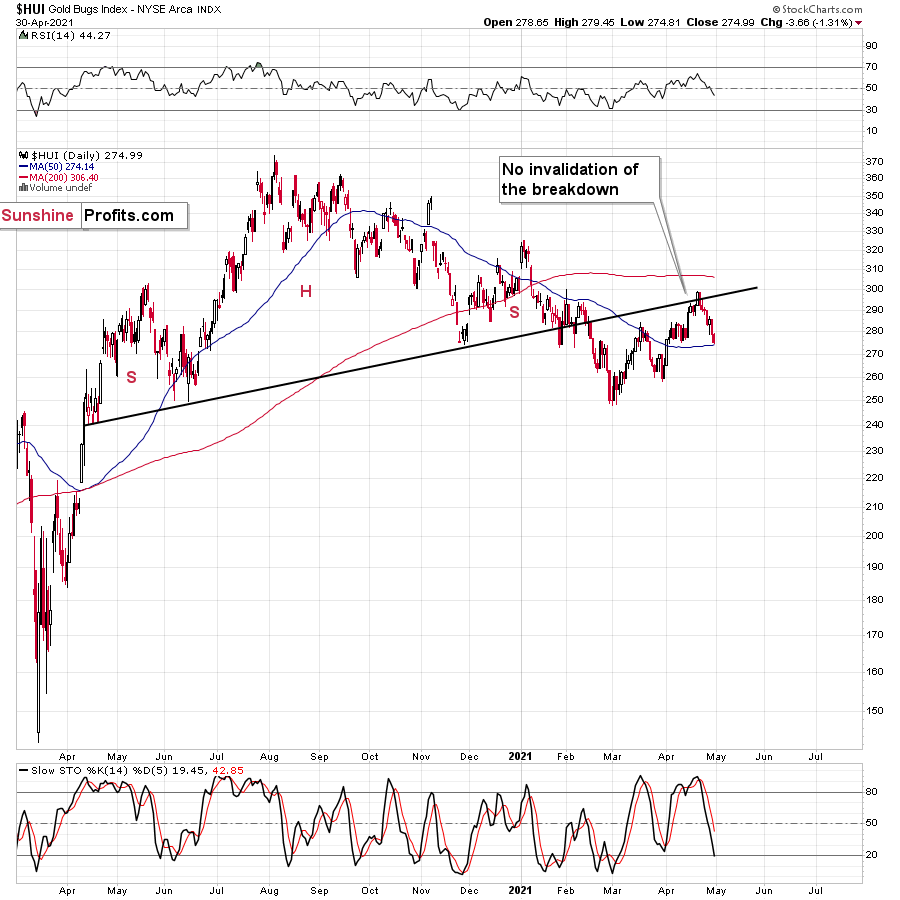

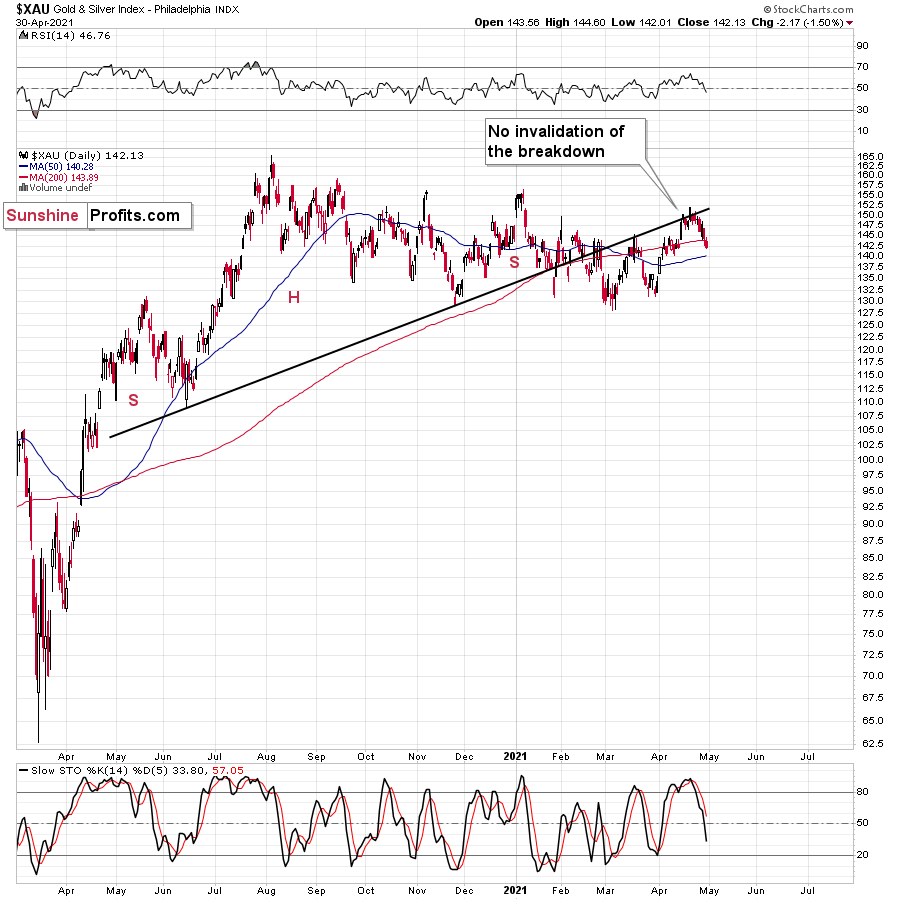

More importantly, though, with the HUI Index (a proxy for gold mining stocks) already verifying the breakdown below the neckline of its bearish H&S pattern – which didn’t occur until later in 2008 – the miners’ current outlook is actually more bearish than it was in 2008.

To explain, note that the 2007 – 2008 and the 2009 – 2012 head and shoulders patterns didn’t have the right shoulders all the way up to the line that was parallel to the line connecting the bottoms. I marked those lines with green in the above-mentioned formations. In the current case, I marked those lines with orange. Now, in both cases, the final top – the right shoulder – formed close to the price where the left shoulder topped. And in early 2020, the left shoulder topped at 303.02.

That’s why I previously wrote that “it wouldn’t be surprising to see a move to about 300 in the HUI Index”. And that’s exactly what we saw – the recent high was slightly above 299. Moreover, with investors rejecting the HUI Index’s attempted advance above its previous highs (depicted on the right shoulder above), the miners’ springtime swoon has likely just begun.

To clarify, one head-and-shoulders pattern – with a rising neckline – was already completed, and one head-and-shoulders pattern – with a horizontal neckline – is being completed, but we’ll have the confirmation once miners break to new yearly lows.

For context, I wrote previously:

The recent rally is not a game-changer, but rather a part of a long-term pattern that’s not visible when one focuses on the short-term only.

The thing is that the vast majority of individual investors and – sadly – quite many analysts focus on the trees while forgetting about the forest. During the walk, this might result in getting lost, and the implications are no different in the investment landscape.

From the day-to-day perspective, a weekly – let alone monthly – rally seems like a huge deal. However, once one zooms out and looks at the situation from a broad perspective, it’s clear that:

“What has been will be again, what has been done will be done again; there is nothing new under the sun.” (-Ecclesiastes 1:9)

The rally is very likely the right shoulder of a broad head and shoulders formation. “Very likely” and not “certainly”, because the HUI Index needs to break to new yearly lows in order to complete the pattern – for now, it’s just potential. However, given the situation in the USD Index (i.a. the positions of futures traders as seen in the CoT report, and the technical situation in it), it seems very likely that this formation will indeed be completed. Especially when (not if) the general stock market tumbles.

In addition, three of the biggest declines in the mining stocks (I’m using the HUI Index as a proxy here), all started with broad, multi-month head-and-shoulders patterns. And in all three cases, the size of the decline exceeded the size of the head of the pattern.

Can we see gold stocks as low as we saw them last year? Yes.

Can we see gold stocks even lower than at their 2020 lows? Again, yes.

Of course, it’s far from being a sure bet, but the above chart shows that it’s not irrational to expect these kind of price levels before the final bottom is reached. This means that a $24 target on the GDX ETF is likely conservative.

In addition, mining stocks are currently flirting with two bearish scenarios:

- If things develop as they did in 2000 and 2012-2013, gold stocks are likely to bottom close to their early 2020 high.

- If things develop like in 2008 (which might be the case, given the extremely high participation of the investment public in the stock market and other markets), gold stocks could re-test (or break slightly below) their 2016 low.

I know, I know, this seems too unreal to be true… But wasn’t the same said about silver moving below its 2015 bottom in 2020? And yet, it happened.

Keep in mind though: scenario #2 most likely requires equities to participate. In 2008 and 2020, the sharp drawdowns in the HUI Index coincided with significant drawdowns of the S&P 500. However, with the words ‘all-time high’ becoming commonplace across U.S. equities, the likelihood of a three-peat remains relatively high.

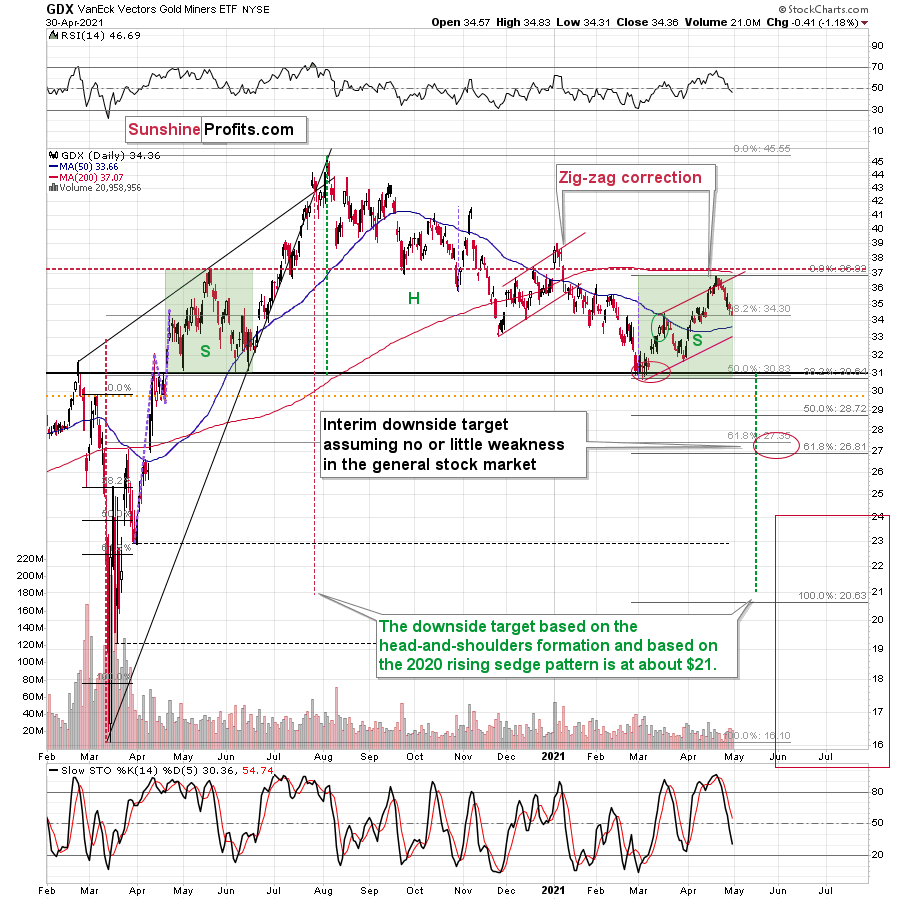

Circling back to the GDX ETF, the senior miners’ superficial strength finally came to a head. Unable to hold the upper trendline of its corrective zigzag pattern, the GDX ETF’s sharp retracement quickly invalidated the breakout above its roughly one-and-a-half-month channel. More importantly, though, after showing a similar pattern in late 2020/early 2021, the GDX ETF eventually broke below its 50-day moving average, then under its rising support line and, in the end, completely lost its wits until support arrived at roughly $31.

Please see below:

If that wasn’t enough, while the GDX ETF is trading relatively close to its mid-February lows – the final ounce of strength before it suffered a profound drawdown – the outlook is even more bearish now than it was then.

Case in point: with the senior miners likely concluding their nearly two-month corrective upswing, the momentum has left the GDX ETF extremely vulnerable. In other words, miners are now after a sizable breather, so they have more “fuel” for bigger declines.

And because the view from its perch implies a long way down before the senior miners find solid ground, the higher they rise, the harder they fall. On top of that, the GDX ETF’s RSI (Relative Strength Index) is significantly elevated relative to the reading in mid-February. Thus, the momentum has also plenty of room to move lower.

The bottom line?

New lows are likely to complete the GDX ETF’s bearish H&S pattern and set the stage for an even larger medium-term decline. And if the projection proves prescient, medium-term support (or perhaps even the long-term one) will likely emerge at roughly $21.

But why ~$21?

- The target aligns perfectly with the signals from the GDX ETF’s 2020 rising wedge pattern. You can see it in the left part of the above chart. The size of the move that follows a breakout or breakdown from the pattern (breakdown in this case) is likely to be equal (or greater than) the height of the wedge. That’s what the red dashed line marks.

- The target is also confirmed when applying the Fibonacci extension technique. To explain, if we take the magnitude of the GDX ETF’s recent peak-to-trough decline and extrapolate it by multiplying it by the Fibonacci sequence, the output results in a target adjacent to $21. I used the Fibonacci retracement tool to show that in the above chart. Interestingly, the same technique was useful in 2020 i n order to time the March bottom.

- The broad head-and-shoulders pattern with the horizontal neckline at about $31 points to the $21 level as the likely target.

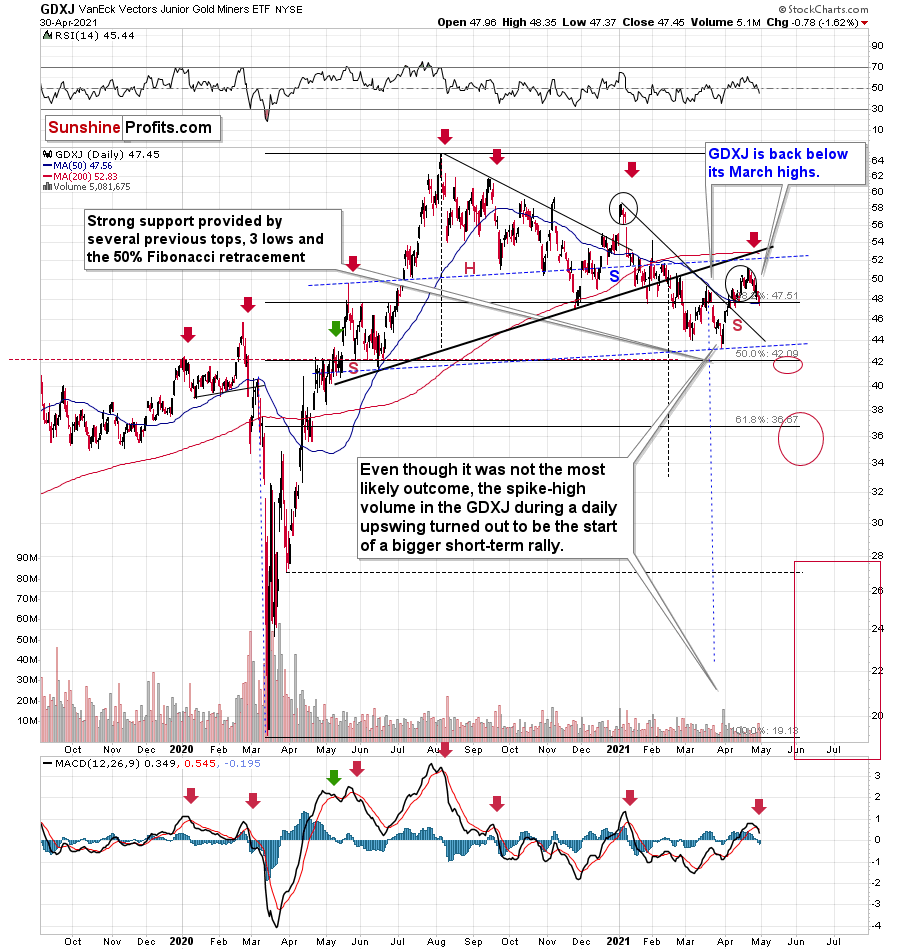

Likewise, when analyzing through the lens of the GDXJ ETF, the junior miners are eliciting the same bearish signals.

Please see below:

To explain, after failing to hold and moving back below its mid-March highs, the GDXJ ETF’s visible underperformance is an ominous sign for the precious metals’ market. What’s more, if you analyze the red arrows on the right side of the chart above (the bottom section), you can see that the MACD indictor has recorded another sell-signal (with the black line crossing the red line from above). Moreover, the junior miners’ RSI is also mirroring the GDX ETF, which implies plenty of room for the momentum to move lower.

For more context, I wrote on Apr. 30:

This ETF for junior gold and silver miners (gold miners have much bigger weight in it, though) moved and closed back below its March 2021 highs.

Consequently, we have a situation in which:

- The USD Index is about to rally.

- Gold signals that it just can’t wait for the USD Index to rally, and it’s already declining (the pace at which it declines is likely to greatly increase once the USD Index takes off).

- Gold miners behave relatively normally, which in this case means that they are declining more than gold does (GLD just closed 1.14% below the highest daily close of April, while the GDX just closed 5.59% below the highest daily close of April). Besides, their recent move back to the May 2020 highs and the subsequent decline further increases the odds that the decline is going to shape the right shoulder of a huge head and shoulders formation with extremely bearish implications (once completed).

- GDXJ is underperforming GDX just as I’ve been expecting it to. While GDX declined by 5.59% so far (in terms of the closing prices), GDXJ declined by 5.67%. This might seem an unimportant level of underperformance, but the perspective changes once one realizes that GDXJ is more correlated with the general stock market than GDX is. Consequently, GDXJ should be showing strength here, and it isn’t. If stocks don’t decline, GDXJ is likely to underperform by just a bit, but when (not if) stocks slide, GDXJ is likely to plunge visibly more than GDX.

The above combination tells me that we are very well positioned in case of our short position in the GDXJ.

Besides, as an analytical cherry on the bearish GDXJ cake, please note that we just saw a sell signal from the MACD indicator (lower part of the chart) while it was visibly above 0, and after a relatively big short-term rally. We saw this kind of performance only several times in the previous year, and it meant declines in almost all cases. We saw it only once before this year – in early January, and a sizable decline followed.

Piggybacking on point #4, the GDXJ/GDX ratio has been declining since the beginning of the year, which is remarkable because the general stock market hasn’t plunged yet. However, once the general stock market suffers a material correction (or a decline), the GDXJ ETF’s underperformance will likely be heard loud and clear.

Please see below:

So, how low could the GDXJ ETF go?

Well, absent an equity rout, the juniors could form an interim bottom in the $34 to $36 range. Conversely, if stocks show strength, juniors could form the interim bottom higher, close to the $42.5 level. For context, the above-mentioned ranges coincide with the 50% and 61.8% Fibonacci retracement levels and the GDXJ ETF’s previous highs (including the late-March/early-April high in case of the lower target area). Thus, the S&P 500 will likely need to roll over for the weakness to persist beyond these levels.

Also, signaling more pain ahead, both the HUI and the XAU indices verified the breakdowns below the rising necklines of their bearish H&S patterns. And with both indices also eliciting sell signals from their stochastic oscillators, the dams could break at any moment.

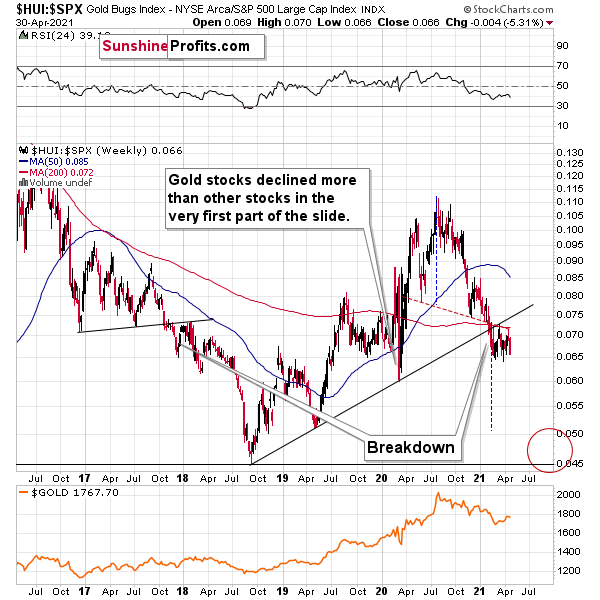

Equally bearish, the HUI Index/S&P 500 ratio has recorded a major, confirmed breakdown. And with the ratio nowhere near recapturing its former glory, it’s another sign that a storm is brewing. Moreover, after moving back and forth for the last few months, not only has the HUI Index/S&P 500 ratio broken below its rising support line (the upward sloping black line below), but the ratio has also broken below the neckline of its roughly 12-month H&S pattern (the dotted red line below). As a result, given the distance from the head to the neckline, the HUI Index/S&P 500 ratio is on a collision course back to (at least) 0.050.

Please see below:

When the ratio presented on the above chart above is rising, it means that the HUI Index is outperforming the S&P 500. When the line above is falling, it means that the S&P 500 is outperforming the HUI Index. If you analyze the right side of the chart, you can see that the ratio has broken below its rising support line. For context, the last time a breakdown of this magnitude occurred, the ratio plunged from late-2017 to late-2018. Thus, the development is profoundly bearish.

Playing out as I expected, a sharp move lower was followed by a corrective upswing back to the now confirmed breakdown level (which is now resistance). Mirroring the behavior that we witnessed in early 2018, after breaking below its rising support line, the HUI Index/S&P 500 ratio rallied back to the initial breakdown level (which then became resistance) before suffering a sharp decline. And with two-thirds of the analogue already complete, the current move lower still has plenty of room to run. Likewise, the early-2018 top in the HUI Index/S&P 500 ratio is precisely when the USD Index began its massive upswing. Thus, with history likely to rhyme, the greenback could spoil the miners’ party once again.

In addition, the HUI to S&P 500 ratio broke below the neck level (red, dashed line) of a broad head-and-shoulders pattern, and it verified this breakdown by moving temporarily back to it. The target for the ratio based on this formation is at about 0.05 (slightly above it). Consequently, if the S&P 500 doesn’t decline, the ratio at 0.05 would imply the HUI Index at about 196. However, if the S&P 500 declined to about 3,200 or so (its late-2020 lows) and the ratio moved to about 0.05, it would imply the HUI Index at about 160 – very close to its 2020 lows.

All in all, the implications of mining stocks’ relative performance to gold and the general stock market are currently bearish.

But if we’re headed for a GDX ETF cliff, how far could we fall?

Well, there are three reasons why the GDX ETF might form an interim bottom at roughly ~$27.50 (assuming no big decline in the general stock market):

- The GDX ETF previously bottomed at the 38.2% and 50.0% Fibonacci retracement levels. And with the 61.8% level next in line, the GDX ETF is likely to garner similar support.

- The GDX ETFs late-March 2020 high should also elicit buying pressure.

- If we copy the magnitude of the late-February/early-March decline and add it to the early-March bottom, it corresponds with the GDX ETF bottoming at roughly $27.50.

Keep in mind though: if the stock market plunges, all bets are off. Why so? Well, because when the S&P 500 plunged in March 2020, the GDX ETF moved from $29.67 to below $17 in less than two weeks. As a result, U.S. equities have the potential to make the miners’ forthcoming swoon all the more painful.

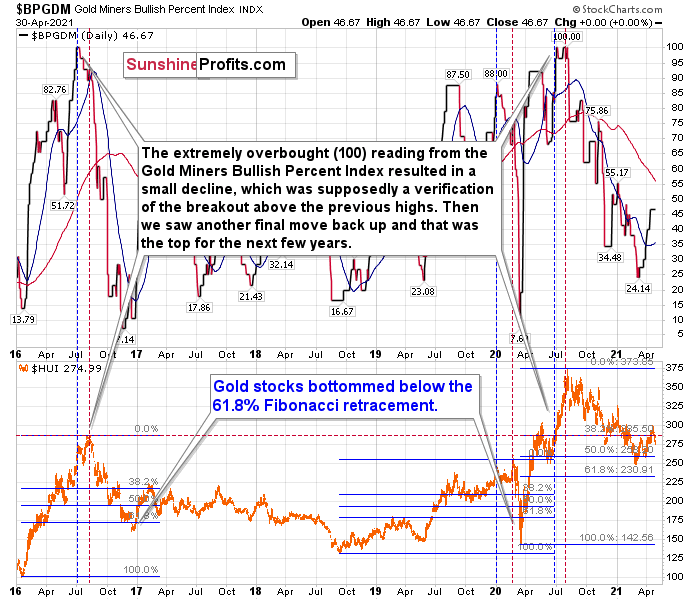

As another reliable indicator (in addition to the myriads of signals coming not only from mining stocks, but from gold, silver, USD Index, stocks, their ratios, and many fundamental observations) the Gold Miners Bullish Percent Index ($BPGDM) isn’t at levels that trigger a major reversal. The Index is now approaching 47. However, far from a medium-term bottom, the latest reading is still more than 37 points above the 2016 and 2020 lows.

Back in 2016 (after the top), and in March 2020, the buying opportunity didn’t present itself until the $BPGDM was below 10.

Thus, with the sentiment still relatively elevated, it will take more negativity for the index to find the true bottom.

The excessive bullishness was present at the 2016 top as well, and it didn’t cause the situation to be any less bearish in reality. All markets periodically get ahead of themselves regardless of how bullish the long-term outlook really is. Then, they correct. If the upswing was significant, the correction is also quite often significant.

Please note that back in 2016, there was an additional quick upswing before the slide, and this additional upswing had caused the $BPGDM to move up once again for a few days. It then declined once again. We saw something similar also in the middle of 2020. In this case, the move up took the index once again to the 100 level, while in 2016 this wasn’t the case. But still, the similarity remains present.

Back in 2016, when we saw this phenomenon, it was already after the top and right before the big decline. Based on the decline from above 350 to below 280, we know that a significant decline is definitely taking place.

But has it already run its course?

Well, in 2016 and early 2020, the HUI Index continued to move lower until it declined below the 61.8% Fibonacci retracement level. The emphasis goes on “below” as this retracement might not trigger the final bottom. Case in point: back in 2020, the HUI Index undershot the 61.8% Fibonacci retracement level and gave back nearly all of its prior rally. And using the 2016 and 2020 analogues as anchors, this time around, the HUI Index is likely to decline below 231. In addition, if the current decline is more similar to the 2020 one, the HUI Index could move to 150 or so, especially if it coincides with a significant drawdown of U.S. equities.

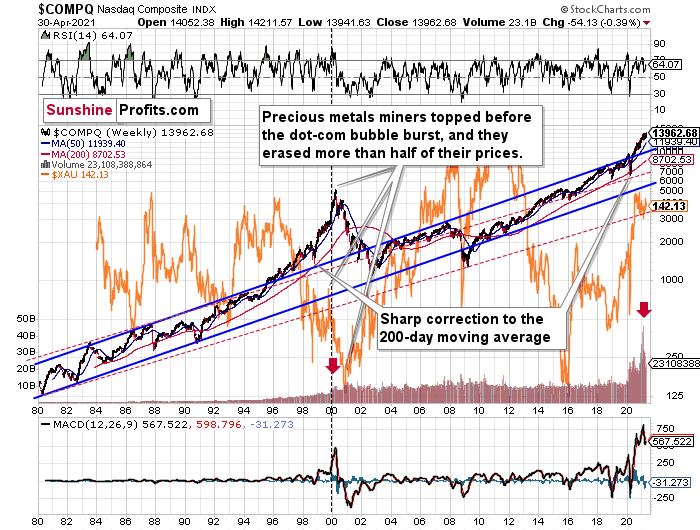

Circling back to the NASDAQ Composite, the unwinding of excessive speculation could deliver a fierce blow to the gold miners. Case in point: when the dot-com bubble burst in 2000, the NASDAQ lost nearly 80% of its value, while the gold miners lost more than 50% of their value.

Please see below:

Right now, the two long-term channels above (the solid blue and red dashed lines) show that the NASDAQ is trading well above both historical trends.

Back in 1998, the NASDAQ’s last hurrah occurred after the index declined to its 200-day moving average (which was also slightly above the upper border of the rising trend channel marked with red dashed lines).

And what happened in the first half of 2020? Well, we saw an identical formation.

The similarity between these two periods is also evident if one looks at the MACD indicator. There has been no other, even remotely similar, situation where this indicator would soar so high.

Furthermore, and because the devil is in the details, the gold miners’ 1999 top actually preceded the 2000 NASDAQ bubble bursting. It’s clear that miners (the XAU Index serves as a proxy) are on the left side of the dashed vertical line, while the tech stock top is on its right side. However, it’s important to note that it was stocks’ slide that exacerbated miners’ decline. Right now, the mining stocks are already declining, and the tech stocks continue to rally. Two decades ago, tech stocks topped about 6 months after miners. This might spoil the party of the tech stock bulls, but miners topped about 6 months ago…

Also, supporting the 2000 analogue, today’s volume trends are eerily similar. If you analyze the red arrows on the chart above, you can see that the abnormal spike in the MACD indicator coincided with an abnormal spike in volume. Thus, mounting pressure implies a cataclysmic reversal could be forthcoming.

Interestingly, two decades ago, miners bottomed more or less when the NASDAQ declined to its previous lows, created by the very first slide. We have yet to see the “first slide” this time. But, if the history continues to repeat itself and tech stocks decline sharply and then correct some of the decline, when they finally move lower once again, we might see THE bottom in the mining stocks. Of course, betting on the above scenario based on the XAU-NASDAQ link alone would not be reasonable, but if other factors also confirm this indication, this could really take place.

Either way, the above does a great job at illustrating the kind of link between the general stock market and the precious metals market (gold, silver, and mining stocks) that I expect to see also this time. PMs and miners declined during the first part of the stocks’ (here: tech stocks) decline, but then they bottomed and rallied despite the continuation of stocks’ freefall.

Even more ominous, the MACD indicator is now flashing a clear sell signal. And because the current reading is analogous to the one that preceded the dot-com bust, the NASDAQ Composite – and indirectly, the PMs – continue to sail toward the perfect storm.

With all of that said: how will we know when a medium-term buying opportunity presents itself?

We view price target levels as guidelines and the same goes for the Gold Miners Bullish Percent Index (below 10), but the final confirmation will likely be gold’s strength against the ongoing USDX rally. At many vital bottoms in gold, that’s exactly what happened, including the March bottom.

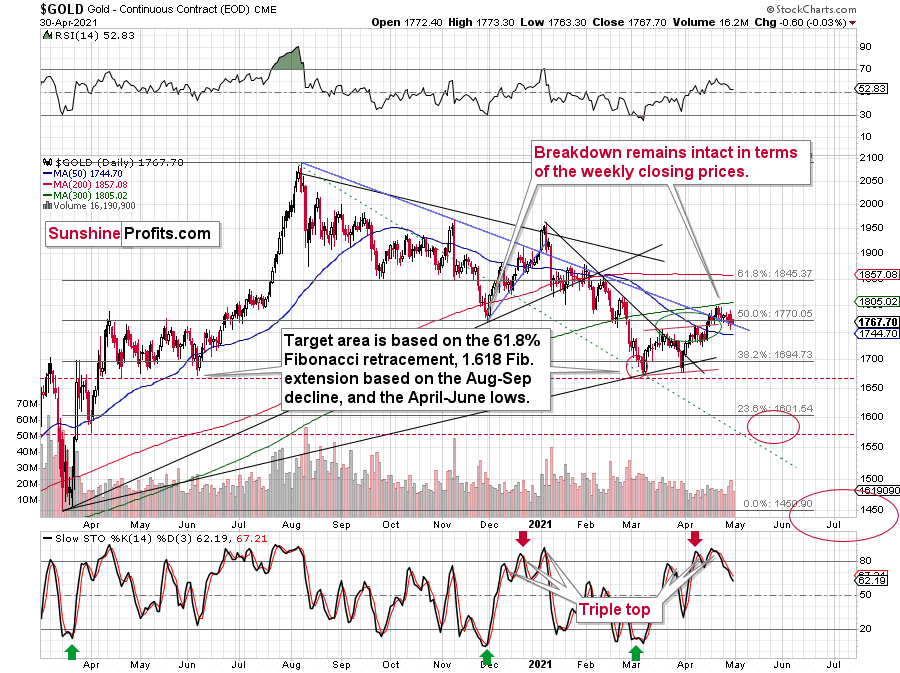

Gold

With a triple-top in gold’s stochastic oscillator akin to three warning signs of a nervous breakdown, the yellow metal is still recovering from last week’s crisis of confidence. And with the price action mirroring what we witnessed in early January – right before gold suffered a significant slide – the yellow metal could soon need therapy.

Please see below:

To explain, while gold’s corrective upswing was slightly bigger than I had anticipated, please note that the length thereof was in tune with the border of the green ellipse I used to mark the likely upside target area. In other words, the recent rally was not a game-changer. The yellow metal’s inability to crack $1,800 highlights the medium-term implications that I’ve been warning about. As a result, it’s become increasingly clear that gold’s recent strength was nothing more than a short-term upswing within a medium-term downtrend.

For more on the significance of gold’s stochastic oscillator, I wrote previously:

The first sell signal occurred slightly below the 80 level, the second was above it, and the same was the case with the third one.

Since back in early 2021, the stochastic indicator moved to new highs – and so far it hasn’t – and since the USD Index might even move slightly lower before finding its short-term bottom, gold could move slightly higher on a temporary basis, before topping. Perhaps (there are no certainties on any market, but this seems quite possible in the near term) it would be the round nature of the $1,800 level and the 300-day moving average that’s very close to it that would trigger a reversal and another massive decline. From the medium-term point of view, another $20 rally doesn’t really matter. It’s the few-hundred-dollar decline that’s likely to follow that really makes the difference.

In addition, it seems that gold is moving in a way that’s somewhat similar to what we saw between mid-April 2020 and mid-June 2020. It’s trading sideways below $1,800 but above ~$1,660. Back in 2020, the range of the back-and-forth movement (size of the short-term rallies and declines) was bigger, but the preceding move was also more volatile, so it’s normal to expect smaller short-term volatility this year (at least during this consolidation).

Why is this particularly interesting? Because both consolidations (the mid-April 2020 – mid-June 2020 one and the March 2021 – today one) could be the shoulders of a broad head-and-shoulders pattern, where the mid-June 2020 – early-March 2021 performance would be the head. The breakdown below the neck level – at about $1,660 – would be extremely bearish in this case because the downside target based on the pattern is created based on the size of the head. The target based on this broad pattern would be at about $1,350 (I marked it with a thin dashed red line on the chart below – you might need to click on it to expand it for this line to become visible). Is this level possible? It is. When gold soared above $2,000, almost nobody thought that it would decline back below its 2011 highs (well, you – my subscribers – did know that). Gold below $1,500 seems unthinkable now, but with rallying long-term rates and soaring USD Index, it could really happen.

“Ok, but what price level would be likely to trigger a bigger rebound during the next big slide?”

Well, the 76.4% Fibonacci retracement level (it’s visible as the 23.6% Fibonacci retracement level on the above chart as inverting the scale is used as a workaround) also coincides with gold’s April 2020 low. Taken together, an interim bottom could form in the ~$1,575 to $1,600 range.

For context, back in early March, the yellow metal continued to decline after reaching the 61.8% Fibonacci retracement (visible as 38.2% Fibonacci retracement) level, while, in contrast, the miners began to consolidate. Gold finally bottomed slightly below the retracement – at its previous lows. This time around, we might witness a similar event. And while the story plays out, the miners’ relative strength should signal the end of the slide (perhaps with gold close to 1,600), while gold will likely garner support sometime thereafter (at $1,575 – $1,580 or so).

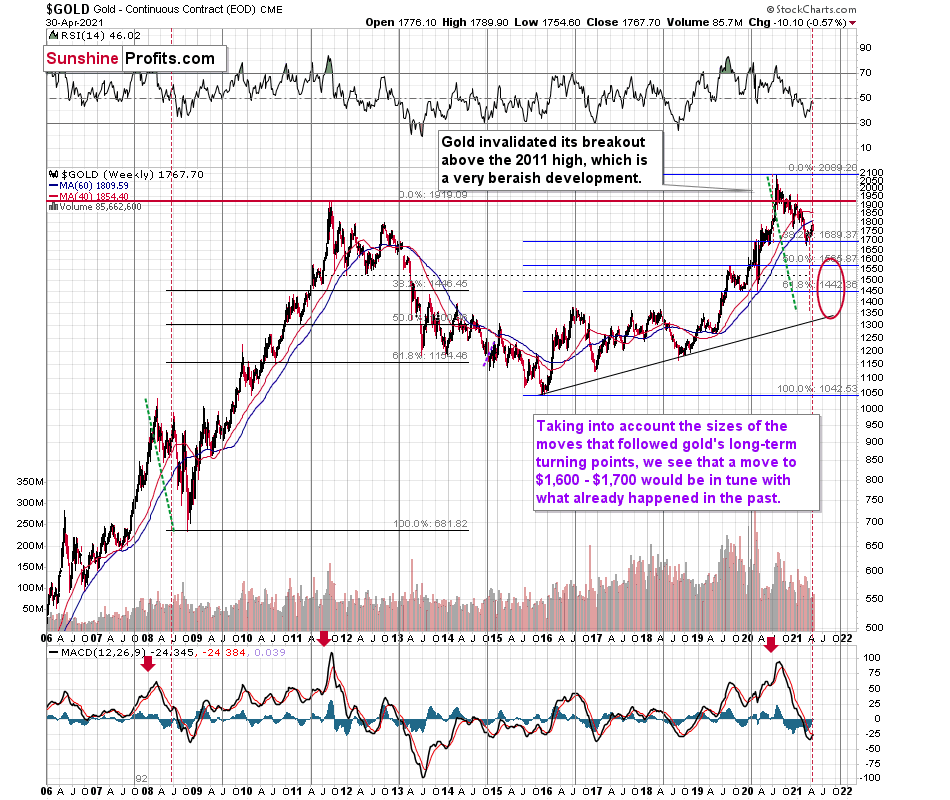

Remember though: this is only an interim target. Over the medium term, the yellow metal will likely form a lasting bottom in the ~$1,450 to $1,500 range.

And why is that?

Well, if you analyze the long-term chart below, you can see that the yellow metal has invalidated the breakout above its 2011 high. More importantly, though, with its rising support line (on the right side of the chart) also coinciding with the 61.8% Fibonacci retracement level and the 2019 and 2020 lows, ~$1,450 to $1,500 is the most prudent medium-term price target.

Conversely, if the 2008 analogue repeats – and a crisis of confidence erupts across U.S. equities – the PMs could move substantially lower. When combining an equity shock with an USD Index’s resurgence, the yellow metal could bottom at roughly $1,400 (or even ~$1,350). Similarly, while the MACD indicator (on gold’s 40-year chart near the top of today’s edition) signals a bottom in the ~$1,200 to ~1,350 range, to be perfectly clear, ~$1,450 to $1,500 is the most likely outcome.

If you analyze the red arrow in the lower part of the above chart (the weekly MACD sell signal), today’s pattern is similar not only to what we saw in 2011, but also to what we witnessed in 2008. Thus, if similar events unfold – with the S&P 500 falling and the USD Index rising (both seem likely for the following months, even if these moves don’t start right away) – the yellow metal could plunge to below $1,350 or so. The green dashed line shows what would have happened to the gold price if it had not declined as much as it did in 2008.

In addition, relative to 2011-2013, today’s price action is also a splitting image. For starters, gold invalidated the breakout above its 2011 highs. Invalidations of breakouts are sell signals, and it’s tough to imagine a more profound breakout that could have failed.

Furthermore, if you analyze the right side of the chart above (the bottom section), you can see that the MACD indicator has sprouted a tiny weekly buy signal. However, it’s important to remember that the same signal emerged in mid-2008 – which confirmed the previous rally but had no bullish implications for the future. Case in point: following the reading in 2008, gold’s volatility increased, and the yellow metal suffered several declines before finding a lasting bottom in 2009. Thus, the recent reading is nothing to write home about. I marked both cases with red, dashed lines.

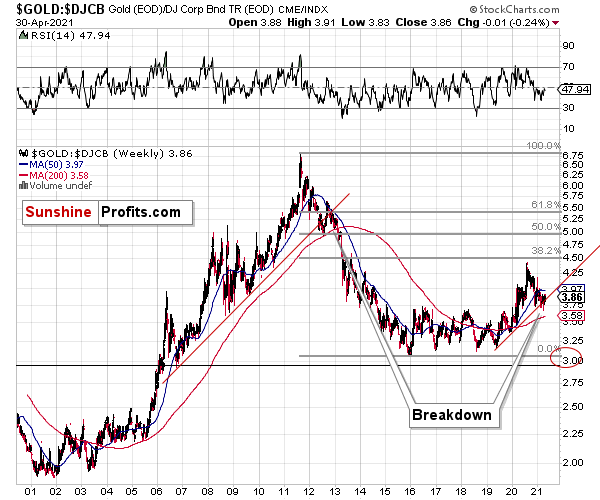

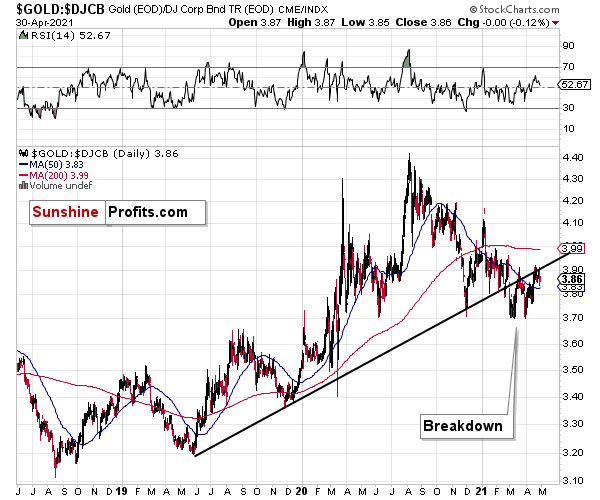

To that point, the yellow metal continues to demonstrate weakness in the face of rising bond yields. Analyzing from a long-term perspective, the gold/ Dow Jones Corporate Bond Index (Total Return) ratio suffered significant resistance near the 38.2% Fibonacci retracement level. Moreover, the ratio has also fallen below its 50-week moving average (the blue line) and broken below its rising support line (the upward-sloping red line on the right side of the chart).

On top of that, sandwiched between its 50-week MA and its 200-week MA, the ratio is mirroring its pre-plunge behavior from 2012. And following right along, the 2012 swoon also coincided with a sharp decline in gold, silver and mining stocks.

What’s more, if we zoom in for a closer look, the bearish breakdown is even more visible. If you analyze the right side of the chart, you can see that despite two attempts to break above its rising support line, rejection has left the ratio in no man’s land. The bottom line? The yellow metal was recently swimming upstream against an extremely powerful current.

Silver

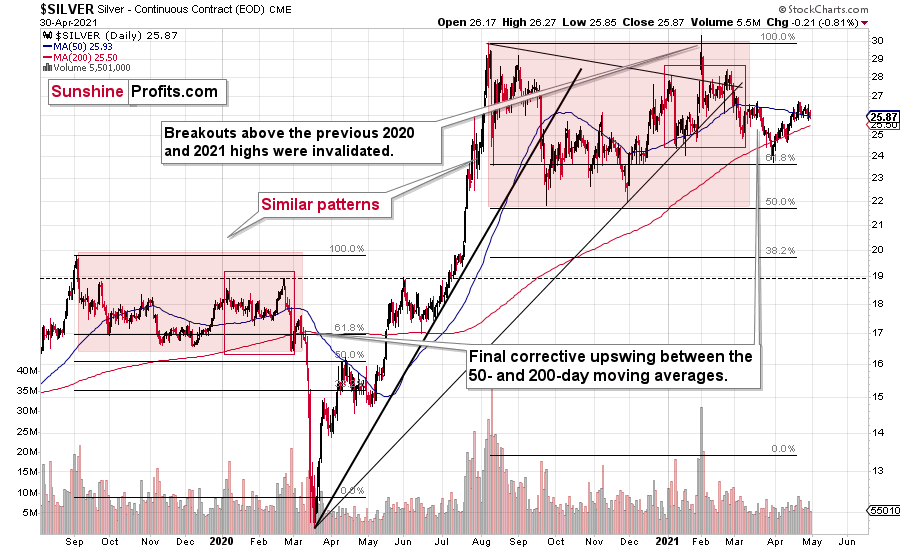

While silver’s daily dance above and below its 50-day moving average contradicts the price action from early 2021, the white metal is essentially trading one bearish analogue for another. If you analyze the left side of the chart below, you can see that silver’s failed attempt to break above its 50-day MA was followed by a material drawdown in early 2021. However, after falling below its 50-day MA last week, the white metal has only gone deeper into its time machine.

Please see below:

To explain, with its current behavior mirroring 2008 – where silver fell below and then rallied back above its 50-day MA before plunging – the white metal is embarking on a journey of self-destruction. Moreover, with silver matching the NASDAQ Composite’s inability to conquer new heights, new lows could soon be on the horizon.

For context, I wrote previously:

If we zoom in on the white metal’s price action in 2008, you can see that an immaterial bounce also occurred right before silver fell off a cliff.

The final corrective upswing of early 2020 took place in very late February and early March, while the two – normal – tops that created the red-line rectangle formed more or less at the turn of the year and in late February. This year, it’s all taking place at almost exactly the same time of the year.

Let’s be realistic - so far, the analogy might seem too unclear to be viewed as a reliable base for making a silver forecast.

But what if… What if there was a very similar pattern in the past that also preceded a massive decline? This would greatly increase the reliability of the above self-similarity.

There was indeed such a pattern!

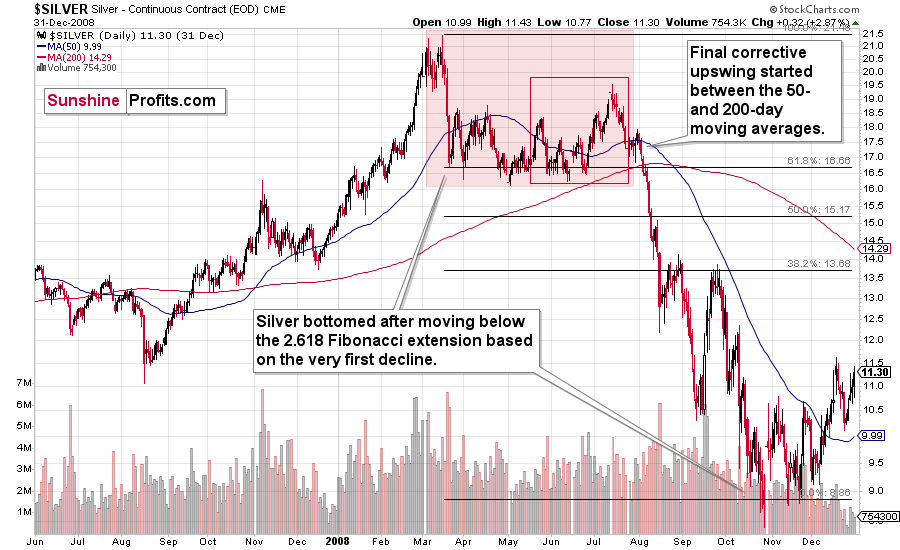

That’s what silver did in 2008 before it declined.

The August 2007 – March 2008 rally (please note the interim top in November 2007 that was followed by a zigzag decline, more or less in the middle of the rally) is similar to the March 2020 – August 2021 rally (please note the interim top in June 2020 that was followed by a zigzag pattern, more or less in the middle of the rally).

Afterwards, we saw a double top in both cases that was followed by a sizable slide. Then silver formed a specific U-shaped broad top, where the final top was below the initial one (exception: in this case the forum-based rally took silver slightly above the previous high, but due to the specific / random nature of the move, it “doesn’t count” as something that invalidates the analogy).

After the top, silver declined, and the final corrective upswing took place approximately between the 50- and 200-day moving averages.

Please note that in both previous (2008 and 2020) cases silver then truly plunged, and it kept on declining until it moved below the 2.618 Fibonacci extension based on the initial downswing. The above charts illustrate that by showing the first decline at the 38.2% retracement (1 / 0.382 = approximately 2.618). Applying the same to the current situation (the initial decline took silver from below $30 to below $24) provides us with the minimum decline target at about $13.50. Will silver really decline as low? In my view, it’s imperative to watch other markets for indications as they might have more reliable targets (for instance gold), but I wouldn’t say that this target (or lower price levels) is out of the question. Of course, that’s just on a temporary basis – silver will likely soar in the following months and years (after this decline).

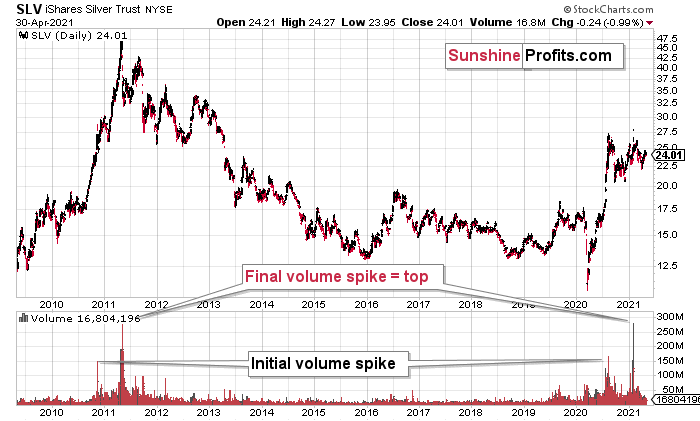

Highlighting the effect of WallStreetBets’ #SilverSqueeze, the SLV ETF’s volume spikes in 2020/2021 were nearly identical to the surges that we witnessed ~10 years ago. If you analyze the chart below, you can see that the massive inflows at the end of 2012 were not the beginning of a medium-term upswing. In fact, they coincided with silver’s final bounce before the white metal suffered a major decline.

Please see below:

To explain, I wrote previously:

If you analyze the volume spikes at the bottom of the chart, 2021 and 2011 are a splitting image. To explain, in 2011, an initial abnormal spike in volume was followed by a second parabolic surge. However, not long after, silver’s bear market began.

SLV-volume-wise, there's only one similar situation from the past - the 2011 top. This is a very bearish analogy as higher prices of the white metal were not seen since that time, but the analogy gets even more bearish. The reason is the "initial warning" volume spike in this ETF. It took place a few months before SLV formed its final top, and we saw the same thing also a few months ago, when silver formed its initial 2020 top.

The history may not repeat itself to the letter, but it tends to be quite similar. And the more two situations are alike, the more likely it is for the follow-up action to be similar as well. And in this case, the implications for the silver price forecast are clearly bearish.

Based on the above chart, it seems that silver is likely to move well above its 2011 highs, but it’s unlikely to do it without another sizable downswing first.

Similarly, silver’s inverse price action also has bearish implications. Nearly identical to the inverted formation that emerged from 2006 to 2009, today’s chart looks eerily similar to its predecessor.

While it’s more of a wild card, the above pattern shows that silver’s 2020 top plots are nearly identical to the inverse of the 2006-2009 performance. I copied the 2006 – 2009 performance right below the regular price movement and inverted it. I also copied this inverted pattern to the last few years.

The similarity is quite significant. And whenever a given pattern has been repeated, the odds are that it could also repeat in the not-too-distant future. Of course, there is no guarantee for that, but once the same market has reacted in a certain way to a specific greed/fear combination, it can just as well do it again. And these similarity-based techniques work quite often. So, while it’s not strong enough to be viewed as a price-path-discovery technique on its own, it should make one consider some scenarios more closely. In particular, this means that the declines in the prices of silver, gold, and mining stocks could be bigger and take longer than it seems based on other charts and techniques.

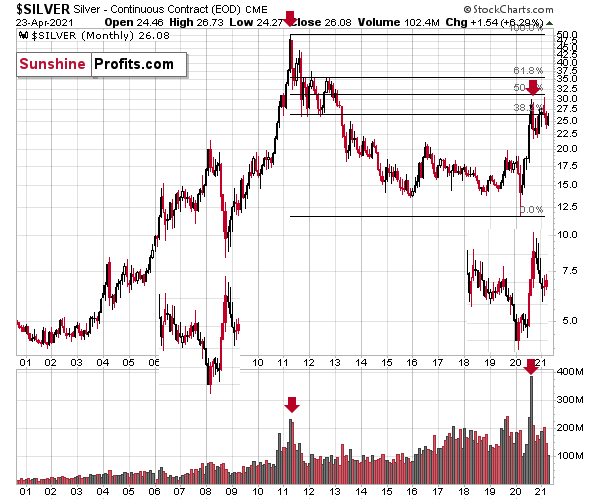

The above is also in tune with the implications of the sell signal from the MACD indicator on the monthly gold chart.

The only thing that comes to my mind which could – realistically – trigger such a prolonged decline would be a major drop in the general stock market. Given what I wrote above, the latter is quite possible, so I’ll be on the lookout for confirmations and invalidations of this scenario.

If history rhymes, silver could be in for a profound decline over the next few months (beyond my initial target). Moreover, the development would increase the duration of precious metals’ bear market (also beyond my initial forecast).

After all, gold did invalidate its long-term breakout above the 2011 highs, and the way gold reacted to a small upswing in the USD Index was truly profound…

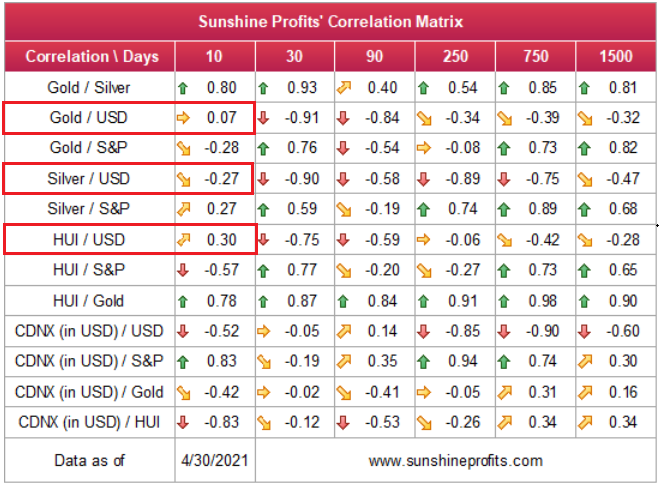

Turning to cross-asset correlations, gold, silver and the HUI Index’s 10-day correlations have become scrambled once again. With a higher U.S. 10-Year Treasury yield distracting the PMs from the movement of the USD Index, they’ve been unable to capitalize on the latter’s recent weakness. However, still exhibiting strong negative relationships with the U.S. dollar over the medium term, the USD Index’s likely ascension is poised to haunt the PMs over the course of the next several months.

For more context, I wrote previously:

Since gold, silver, and mining stocks have been strongly negatively correlated with the USD Index in the medium term, it seems likely that they will be negatively affected by the upcoming sizable USDX upswing.

…Until we see the day where gold reverses or soars despite the U.S. currency’s rally.

If that happens with gold at about $1,700, we’ll have a very good chance that this was the final bottom. If it doesn’t happen at that time, or gold continues to slide despite USD’s pause or decline, we’ll know that gold has further to fall.

Naturally, we’ll keep you – our subscribers – informed.

To move forward, how does the GDX downside target compare to gold’s downside target? If, at the same time, gold moves to about $1,700 and miners are already after a ridiculously big drop (to $31-$32 in the GDX ETF, or lower), the binding profit-take exit price of your GDX ETF will become $32.02 (those with higher risk tolerance might lower it to $31.15 or so, but moving it lower seems just too risky).

At this time, the final GDX target (the one that would correspond to gold at $1,500 or so) is still unclear. The $17 - $23 area seems probable, especially if the general stock market slides once again. It’s too early to say with any significant level of certainty. Gold is providing us with a clearer final target, so that’s what we’ll focus on. And most importantly – we’ll focus on gold’s performance relative to the USD Index.

Overview of the Upcoming Part of the Decline

- It seems likely to me that the corrective upswing was already completed . Consequently, it seems that the next big move lower is already underway.

- After miners slide once again in a meaningful and volatile way, but silver doesn’t (and it just declines moderately), I plan to switch from short positions in miners to short positions in silver (this could take another 1-2 weeks to materialize). I plan to exit those short positions when gold shows substantial strength relative to the USD Index, while the latter is still rallying. This might take place with gold close to $1,450 - $1,500 and the entire decline (from above $1,700 to about $1,475) would be likely to take place within 1-12 weeks, and I would expect silver to fall hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold – after gold has already declined substantially) is likely to be the best entry point for long-term investments, in my view. This might happen with gold close to $1,475, but it’s too early to say with certainty at this time. In other words, the entire decline could take between 1 and 12 weeks, with silver declines occurring particularly fast in the final 1-2 weeks.

- If gold declines even below $1,500 (say, to ~$1350 or so), then it could take another 10 weeks or so for it to bottom, but this is not what I view as a very likely outcome.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector would be likely to bottom about three months after the general stock market tops. If the last week’s highs in the S&P 500 and NASDAQ were the final highs, then we might expect the precious metals sector to bottom in the middle of the year – in late July or in August

- The above is based on the information available today, and it might change in the following days/weeks.

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Letters to the Editor

Q: You have mentioned the "winter part of the Kondratiev cycle" several times. Can I assume you think this will result in a dramatic decline in the stock market? Do you think the winter part could occur within the next twelve months?

A: The comment to the first sentence is “yes”, the answer to your first question is “yes”, and the answer to your second question is also “yes”.

What I would like to add is that I’m no longer as certain as I used to be if we are definitely entering “Winter” here. It could actually be “Summer” that is about to start, but the implications for stocks and gold are identical. Gold is likely to perform very well, but not necessarily initially, when the stock market slides.

Q: As a follow-up, gold has strengthened and reversed the majority of its move down in the past 24 hrs and this is in the face of the DXY, dollar strength and rising above the resistant line. Gold is showing strength and does not want to decline. Gold should have moved considerably lower this morning but instead moved up. Gold wants to go up and this appears to be a reversal in direction. Comments? Could it be that there is just too much Fed Intervention now to assume Gold will go down if the DXY/USD strengthens? 4-30-2021

A: Not really, as one swallow doesn’t make a summer. Seeing something like this for many days would likely indicate that the sentiment has indeed changed. For now, it’s way too early to say that, in light of how many opposite signs we got in the previous days.

Q: What are your thoughts regarding the short supply of physical silver and gold?

(The question also included an extra explanation that it was about the shortage of physical coins and bullion products)

A: It’s something relatively normal when we see sizable declines or are close to them. The same happened with regard to the shortage of physical silver and gold coins when PMs were falling in 2013. The physical prices lagged the futures prices, but when it was all said and done and the dust settled, the physical premium decreased, which means that the physical market caught up (not 100%, but to a significant extent) with the futures prices. It’s kind of similar to how the premium on call options won’t decline as much as it “should” based on a volatile decline in prices. The reason is the volatility, which makes people think (and algorithms “think”) that such a move is only temporary and therefore it will or might be quickly reversed.

In short, there are myriads of reasons why gold is likely to soar in the upcoming years, but the one about “physical shortage of coins” is not one of the particularly valid ones. Yes, the demand is significant, but this is what we’ve already seen in the not-too-distant past, and it didn’t result in significantly higher prices, especially in the short term.

Q: The euro is a flawed currency. I expect it to fail within a few years. This would cause the dollar to skyrocket. And gold to collapse initially... Do you see any hope for the euro?

A: I too expect the euro to fail as a currency in the long run. I don’t see it being around two decades from now, perhaps it won’t even last a decade or even several years. The currency was under pressure during the sovereign debt crisis, and while it survived it, I’m not convinced if it’s going to be able to take on another massive crisis like that. And it’s quite easy to tell what could ruin it – the upcoming slide in the general stock market and the overall crisis that follows. After all, the European economies are not really integrated enough for them to have a common currency. That piece of news has been around for many years, and yet the currency held its ground. However, during particularly bad times, it might not be the case.

Would it cause the dollar to skyrocket? Most likely, yes.

Would it cause gold to collapse initially? It’s a tough call. If it happened overnight, then gold would probably soar because this turmoil would likely trigger panic safe-haven buying. However, if the euro’s demise were preceded by a steadier decline in its value, then gold would likely suffer, at least initially.

Q: Many thanks for your analyses. You were spot on with all the moves in the precious metals complex. Really amazing considering that you seem to be the only analyst who is able to do so.

Having said that, I am a bit worried about the timing. For quite some time now, you have been predicting that the final slide would take 1-12 weeks. Based on this timeframe, I took a position in (June 18) JDST options and have been holding this for several months now. I read in your last Gold Alert that you are not positioned in options, but perhaps I'm not the only one of your subscribers who is.

I'm currently deep in the red, but I have a lot of faith in your analysis, and I'm confident that GDXJ will start its slide this week. However, as nothing goes down in a straight line, it seems reasonable to expect it to rebound again halfway, perhaps from half May to early June, after which the slide may continue. But as you may understand, I am getting worried about my June 18 options. The whole slide seems to take longer than originally anticipated, and if the final part of the slide takes again several weeks and GDXJ rebounds in mid-June, my whole position could turn out to be worthless.

So as I see it, I have a choice to make whether or not to close my position early, after the first part of the upcoming slide (perhaps within the next 10 days) or hope for a further slide before mid-June.

I understand you cannot give individual investment advice, but I would be grateful for your views and further insights regarding the (short-term) timing of the upcoming slide.

Many thanks for all your great work.

A: Thank you for the kind words and for the question. As it’s written above, this reply is not an individual investment advice, but rather my opinion in general on a situation in case of such an instrument. Everyone should apply their own specific risk-tolerance levels and other circumstances before making any investment decision.

So, in case of options that expire in mid-June, I would focus on exiting the position when gold moves close to $1,600. That seems to be the likely interim stop for the yellow metal. It’s unclear which of the target areas in GDXJ (and thus JDST) will be at hand at that time, but it’s quite likely that miners will be bottoming a bit before gold, so when gold is just about to reach $1,600, miners will likely already be very close or at their short-term bottom. Of course, this is based on what seems likely to me, not what’s inevitable. It could even be the case that there is no pause at $1,600 in gold, but this seems to be the most likely outcome for the next month – 1.5 months or so.

Summary

To summarize, the PMs’ medium-term decline is well underway, and based on the recent performance of the USD Index, gold and mining stocks, it seems that the corrective upswing is already over. The confirmed breakout in the USD Index is yet another confirmation of the bearish outlook for the precious metals market, and the same goes for the symmetric nature of the potential broad head-and-shoulders in gold and in gold stocks.

After the sell-off (that takes gold to about $1,450 - $1,500), we expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and this March, and it seems that we’re about to make much more on the upcoming decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

By the way, we’re currently providing you with a possibility to extend your subscription by a year, two years or even three years with a special 20% discount. This discount can be applied right away, without the need to wait for your next renewal – if you choose to secure your premium access and complete the payment upfront. The boring time in the PMs is definitely over and the time to pay close attention to the market is here. Naturally, it’s your capital, and the choice is up to you, but it seems that it might be a good idea to secure more premium access now, while saving 20% at the same time. Our support team will be happy to assist you in the above-described upgrade at preferential terms – if you’d like to proceed, please contact us.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $24.12; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $39.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $94.87; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures upside profit-take exit price: unclear at this time - initially, it might be a good idea to exit, when gold moves to $1,512.

Gold futures upside profit-take exit price: $1,512.

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief