Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

The precious metals sector has not been doing much recently, and yesterday’s session was no exception. Gold, silver, and mining stocks were down yesterday, but they are a bit up in today’s pre-market trading. Overall, nothing really changed.

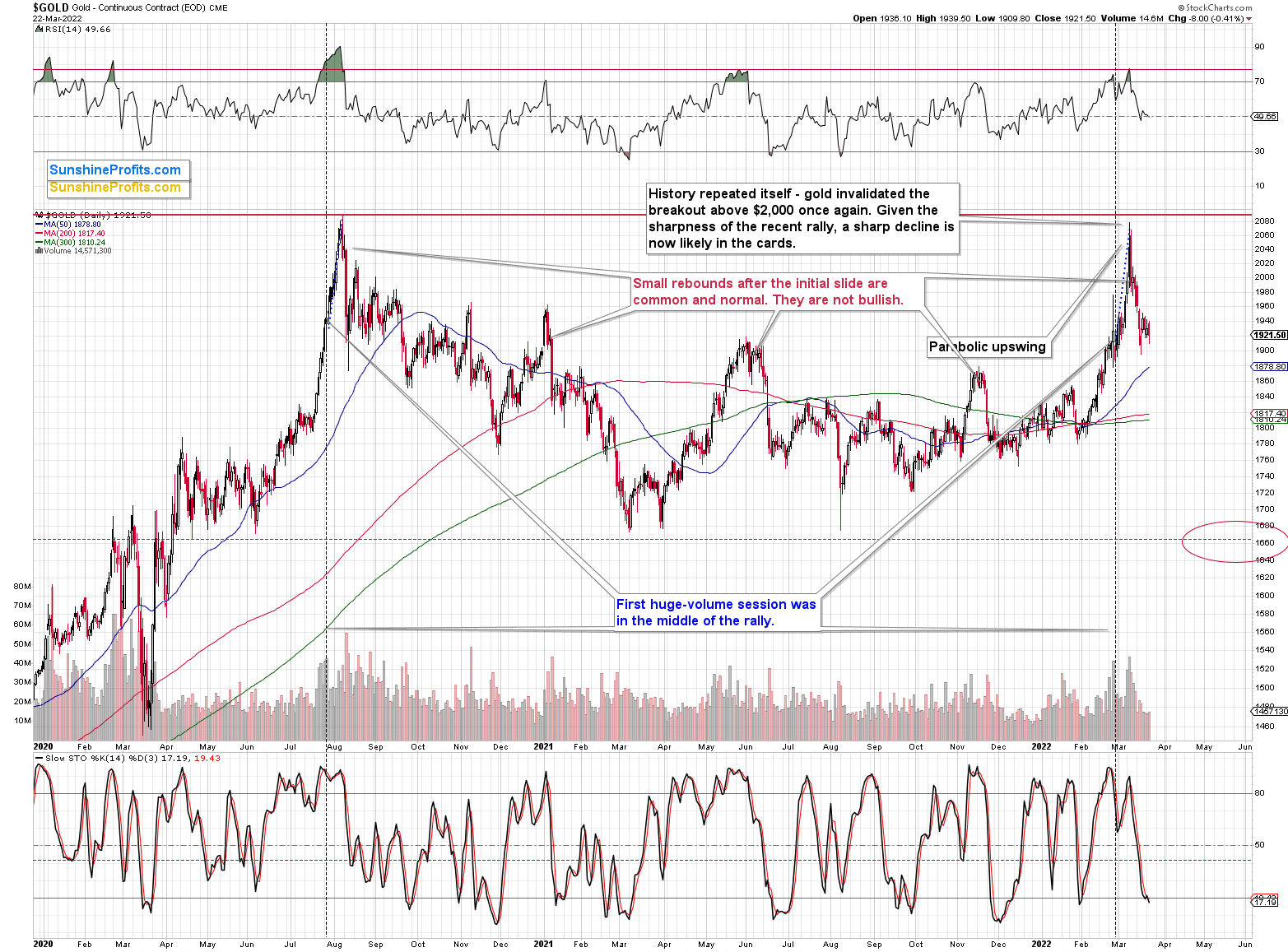

Gold is moving back and forth after a powerful decline, and it’s taking place on relatively low volume, suggesting that it’s just a pause within the slide.

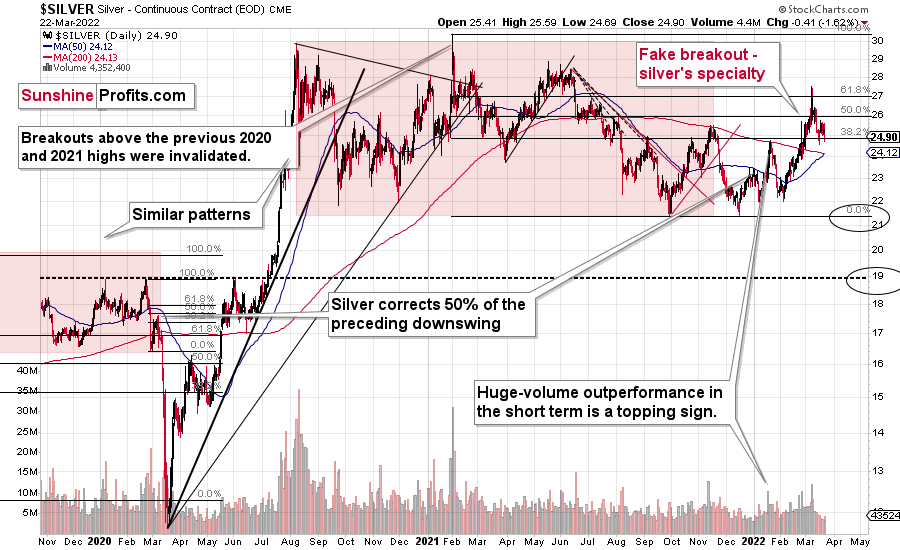

We see the same thing in silver…

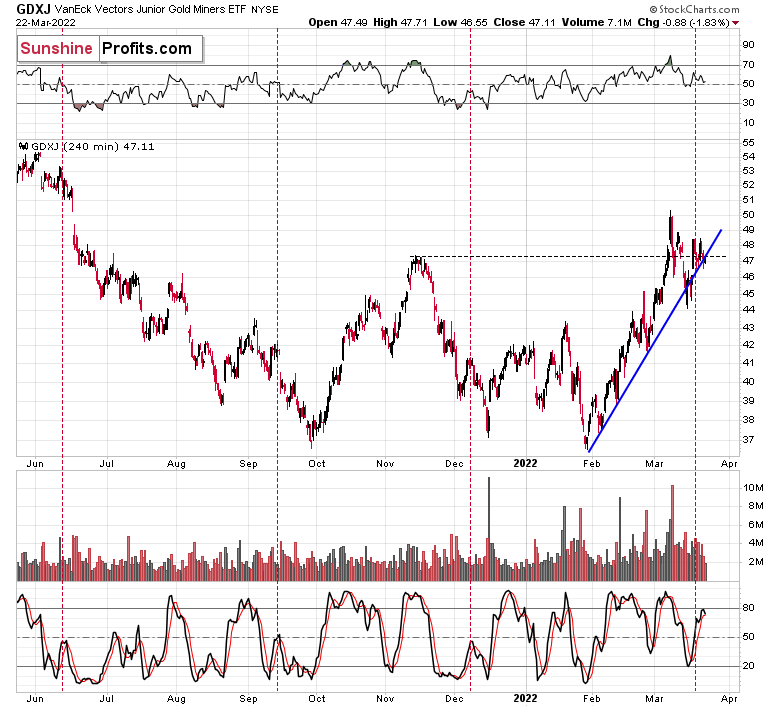

…and in junior mining stocks.

However, there are two interesting facts about yesterday’s session.

The first one is that the GDXJ (a proxy for junior miners) closed the day slightly below the rising short-term support line, so we saw a small (but still) breakdown.

The second one is that the GDXJ closed the day below the highest close that we saw in late-2021, which means that we witnessed a breakdown below this level as well. The move below it was not significant, but it happened.

None of the above events are anything to write home about, but they do indicate somewhat that perhaps the time for this consolidation is over, or about to be over.

After all, let’s keep in mind where the RSI is and what happened when it was trading at similar levels after similar moves. That’s what the red vertical dashed lines represent.

In all three previous cases, similar consolidations were the final chance to exit long positions and/or enter short ones in order to profit on the upcoming declines, which were either significant or very significant. Based on the above, right now would be exactly the wrong time to give up on this sector and/or to stop paying attention to it. Patience here is likely to be extremely well rewarded.

All in all, the technical picture for the precious metals market remains bearish and my previous comments on it remain up-to-date. If you haven’t read my Monday analysis, I encourage you to do so today. Yesterday’s issue (where I focused on silver) is up-to-date too.

Having said that, let’s take a look at the market from a more fundamental point of view.

Falling on Deaf Ears

An epic battle is unfolding across the financial markets as the Fed warns investors about its looming rate hike cycle and the latter ignores the ramifications. However, with perpetually higher asset prices only exacerbating the Fed's inflationary conundrum, a profound shift in sentiment will likely occur over the next few months.

To explain, I highlighted in recent days how the Fed has turned the hawkish dial up to 100. Moreover, I wrote on Mar. 22 that it's remarkable how much the PMs' domestic fundamental outlooks have deteriorated in recent weeks. Yet, prices remain elevated, investors remain sanguine, and the bullish bands continue to play.

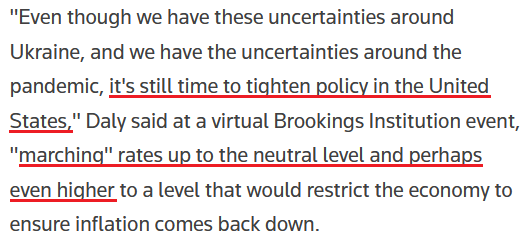

However, with inflation still rising and the Fed done playing games, the next few months should elicit plenty of fireworks. For example, with another deputy sounding the hawkish alarm, San Francisco Fed President Mary Daly said on Mar. 22: "Inflation has persisted for long enough that people are starting to wonder how long it will persist. I'm already focused on letting make sure this doesn't get embedded and we see those longer-term inflation expectations drift up."

As a result, Daly wants to ensure that the "main risk" to the U.S. economy doesn't end up causing a recession.

Please see below:

Source: Reuters

Source: Reuters

Likewise, St. Louis Fed President James Bullard reiterated his position on Mar. 22, telling Bloomberg that “faster is better,” and that “the 1994 tightening cycle or removal of accommodation cycle is probably the best analogy here.”

Please see below:

Source: Bloomberg

Source: Bloomberg

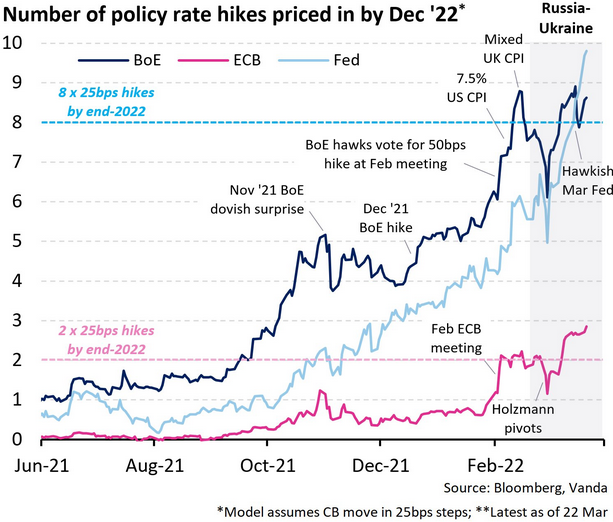

To that point, while investors seem to think that the Fed can vastly restrict monetary policy without disrupting a healthy U.S. economy, a major surprise could be on the horizon. For example, the futures market has now priced in nearly 10 rate hikes by the Fed in 2022. As a result, should we expect the hawkish developments to unfold without a hitch?

Please see below:

To explain, the light blue, dark blue, and pink lines above track the number of rate hikes expected by the Fed, BoE, and ECB. If you analyze the right side of the chart, you can see that the light blue line has risen sharply over the last several days and months. For your reference, if you focus your attention on the material underperformance of the pink line, you can see why I’ve been so bearish on the EUR/USD for so long.

Also noteworthy, please have a look at the U.S. 2-Year Treasury yield minus the German 2-Year Bond yield spread. If you analyze the rapid rise on the right side of the chart below, you can see how much short-term U.S. yields have outperformed their European counterparts in 2021/2022.

Source: Bloomberg/ Lisa Abramowicz

Source: Bloomberg/ Lisa Abramowicz

More importantly, though, with Fed officials’ recent rhetoric encouraging more hawkish re-pricing instead of talking down expectations (like the ECB), they want investors to slow their roll. However, investors are now fighting the Fed, and the epic battle will likely lead to profound disappointment over the medium term.

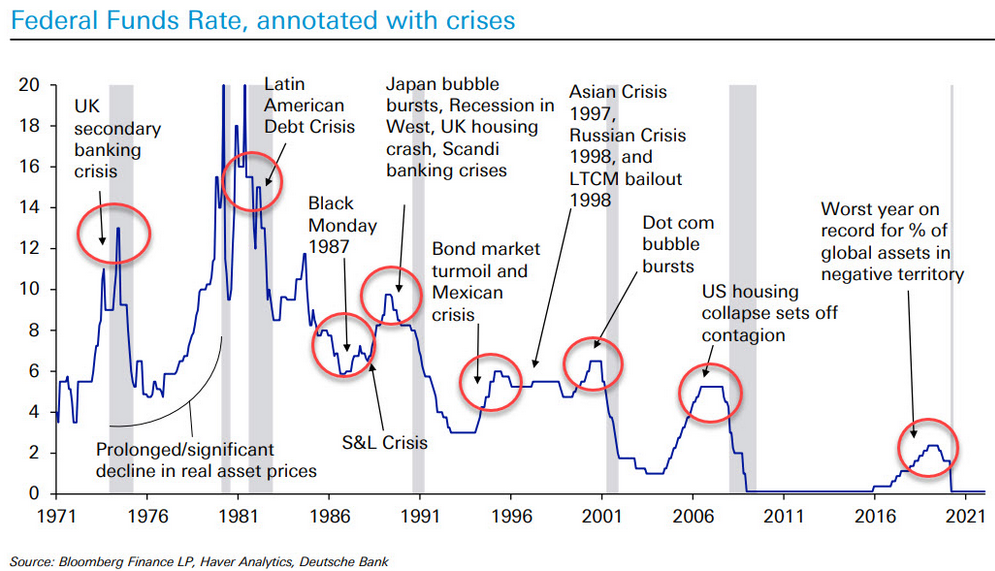

Case in point: when Fed officials dial up the hawkish rhetoric, their “messaging” is supposed to shift investors’ expectations. As such, the threat of raising interest rates is often as impactful as actually doing it. However, when investors don’t listen, the Fed has to turn the hawkish dial up even more. If history is any indication, a calamity will eventually unfold.

Please see below:

To explain, the blue line above tracks the U.S. federal funds rate, while the various circles and notations above track the global crises that erupted during the Fed’s rate hike cycles. As a result, standard tightening periods often result in immense volatility.

However, with investors refusing to let asset prices fall, they’re forcing the Fed to accelerate its rate hikes to achieve its desired outcome (calm inflation). As such, the next several months could be a rate hike cycle on steroids.

To that point, with Fed Chairman Jerome Powell dropping the hawkish hammer on Mar. 21, I noted his response to a question about inflation calming in the second half of 2022. I wrote on Mar. 22:

"That story has already fallen apart. To the extent it continues to fall apart, my colleagues and I may well reach the conclusion we'll need to move more quickly and, if so, we'll do so."

To that point, Powell said that “there’s excess demand" and that "the economy is very strong and is well-positioned to handle tighter monetary policy." As a result, while investors seem to think that Powell’s bluffing, enlightenment will likely materialize over the next few months.

Please see below:

Source: Reuters

Source: Reuters

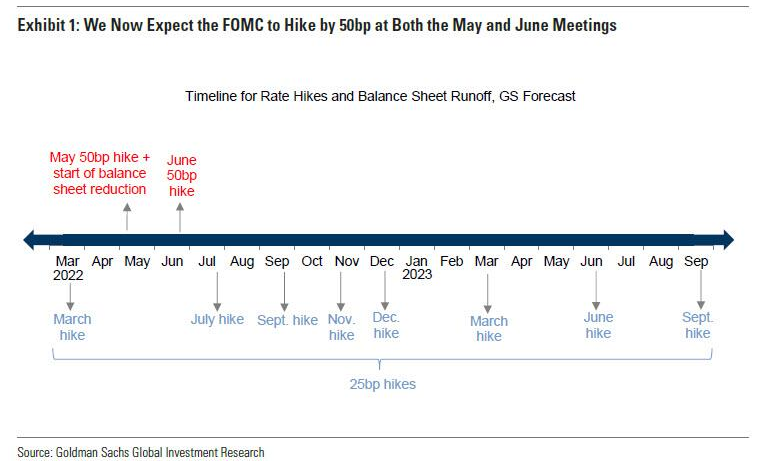

Furthermore, with Goldman Sachs economists noting the shift in tone from “steadily” in January to “expeditiously” on Mar. 21, they also upped their hawkish expectations. They wrote:

“We are now forecasting 50bp hikes at both the May and June meetings (vs. 25bp at each meeting previously). The level of the funds rate would still be low at 0.75-1% after a 50bp hike in May, and if the FOMC is open to moving in larger steps, then we think it would see a second 50bp hike in June as appropriate under our forecasted inflation path.”

“After the two 50bp moves, we expect the FOMC to move back to 25bp rate hikes at the four remaining meetings in the back half of 2022, and to then further slow the pace next year by delivering three quarterly hikes in 2023Q1-Q3. We have left our forecast of the terminal rate unchanged at 3-3.25%, as shown in Exhibit 1.”

Please see below:

In addition, this doesn’t account for the Fed’s willingness to sell assets on its balance sheet. For context, Powell said on Mar. 16 that quantitative tightening (QT) should occur sometime in the summer and that shrinking the balance sheet “might be the equivalent of another rate increase.” As a result, investors’ lack of preparedness for what should unfold over the next few months has been something to behold. However, the reality check will likely elicit a major shift in sentiment.

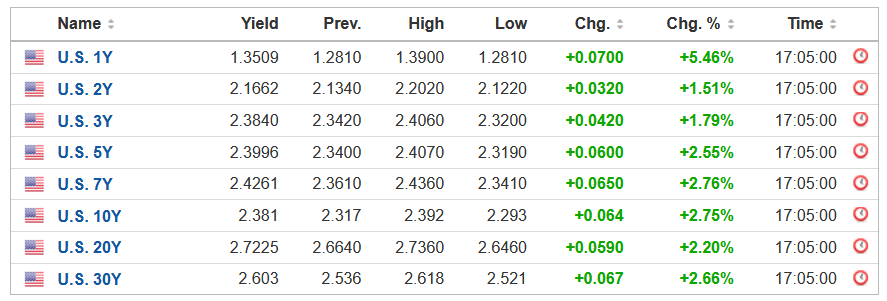

In contrast, the bond market heard Powell’s message loud and clear, and with the U.S. 10-Year Treasury yield hitting another 2022 high of ~2.38% on Mar. 22, the entire U.S. yield curve is paying attention.

Please see below:

Source: Investing.com

Source: Investing.com

Finally, the Richmond Fed released its Fifth District Survey of Manufacturing Activity on Mar. 22. With the headline index increasing from 1 in February to 13 in March, the report cited “increases in all three of the component indexes – shipments, volume of new orders, and number of employees.”

Moreover, the prices received index increased month-over-month (MoM) in March (the red box below), while future six-month expectations for prices paid and received also increased (the blue box below). As a result, inflation trends are not moving in the Fed’s desired direction.

Please see below:

Source: Richmond Fed

Source: Richmond Fed

Likewise, the Richmond Fed also released its Fifth District Survey of Service Sector Activity on Mar. 22, nd while the headline index decreased from 13 in February to -3 in March, current and future six-month inflationary pressures/expectations rose MoM.

Source: Richmond Fed

Source: Richmond Fed

The bottom line? While the Fed is screaming at the financial markets to tone it down to help calm inflation, investors aren't listening. With higher prices resulting in more hawkish rhetoric and policy, the Fed should keep amplifying its message until investors finally take note. If not, inflation will continue its ascent until demand destruction unfolds and the U.S. slips into a recession. As such, if investors assume that several rate hikes will commence over the next several months with little or no volatility in between, they're likely in for a major surprise.

In conclusion, the PMs declined on Mar. 22, as the sentiment seesaw continued. However, as I noted, it's remarkable how much the PMs' domestic fundamental outlooks have deteriorated in recent weeks. Thus, while the Russia-Ukraine conflict keeps them uplifted, for now, the Fed's inflation problem is nowhere near an acceptable level. As a result, when investors finally realize that a much tougher macroeconomic environment confronts them over the next few months, the shift in sentiment will likely culminate in sharp drawdowns.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is now over or very close to being over , and that gold, silver, and mining stocks are now likely to continue their medium-term decline.

- It seems that the first (bigger) stop for gold will be close to its previous 2021 lows, slightly below $1,800 . Then it will likely correct a bit, but it’s unclear if I want to exit or reverse the current short position based on that – it depends on the number and the nature of the bullish indications that we get at that time.

- After the above-mentioned correction, we’re likely to see a powerful slide, perhaps close to the 2020 low ($1,450 - $1,500).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place, and if we get this kind of opportunity at all – perhaps with gold close to $1,600.

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold close to $1,350 - $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,375, but at the moment it’s too early to say with certainty.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector is likely to bottom about three months after the general stock market tops.

- The above is based on the information available today, and it might change in the following days/weeks.

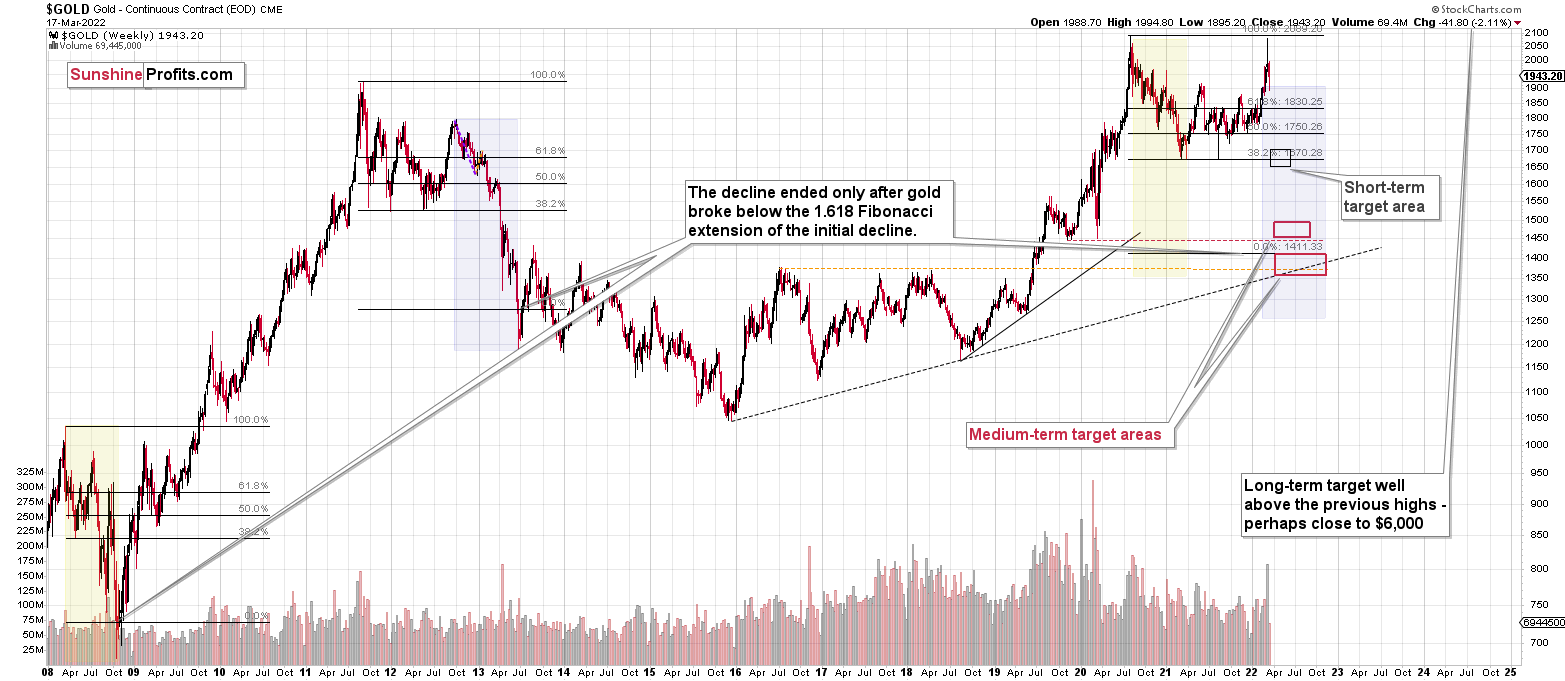

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Summary

Summing up, despite the recent rally in gold, the outlook for junior mining stocks remains exactly as I described previously.

Crude oil’s extreme outperformance, the stock market’s weakness, and critical medium-term resistance levels reached by gold (all-time high!) and junior mining stocks, all indicate that the tops are at hand or have just formed. The huge-volume reversals in gold and (especially) mining stocks, along with silver’s short-term outperformance, all point to lower precious metals prices in the following days/weeks. It seems that the top is in.

Investing and trading are difficult. If it was easy, most people would be making money – and they’re not. Right now, it’s most difficult to ignore the urge to “run for cover” if you physically don’t have to. The markets move on “buy the rumor and sell the fact.” This repeats over and over again in many (all?) markets, and we have direct analogies to similar situations in gold itself. Junior miners are likely to decline the most, also based on the massive declines that are likely to take place (in fact, they have already started) in the stock markets.

From the medium-term point of view, the two key long-term factors remain the analogy to 2013 in gold and the broad head and shoulders pattern in the HUI Index. They both suggest much lower prices ahead.

It seems that our profits from short positions are going to become truly epic in the coming months.

After the sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and this March, and it seems that we’re about to make much more in the upcoming decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $34.63; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $14.98; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $25.48; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $19.12

SLV profit-take exit price: $17.72

ZSL profit-take exit price: $38.28

Gold futures downside profit-take exit price: $1,683

HGD.TO – alternative (Canadian) inverse 2x leveraged gold stocks ETF – the upside profit-take exit price: $11.79

HZD.TO – alternative (Canadian) inverse 2x leveraged silver ETF – the upside profit-take exit price: $29.48

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief