Briefly: in our opinion, full (300% of the regular position size) speculative short positions in mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Today is Martin Luther King Jr. Day, and in honor of the important civil rights leader, the stock market is closed. However, we are publishing today’s analysis as an exception because we understand that readers are eagerly waiting to read our thoughts about last week’s closes and what may lie ahead.

Welcome to this week's flagship Gold & Silver Trading Alert. As we’ve promised you previously, in our flagship Alerts, we will be providing you with much comprehensive and complex analyses (approximately once per week), which will usually take place on Monday.

Predicated on last week’s price moves, our most recently featured outlook remains the same as the price moves align with our expectations. On that account, there are parts of the previous analysis that didn’t change at all in the earlier days, which will be written in italics.

Let’s start with a quick comparison of what happened in gold last week and how it compares to the news that hit the market. In short, the price of gold has declined further amid poor economic date and Biden’s fiscal stimulus, which is a bearish sign.

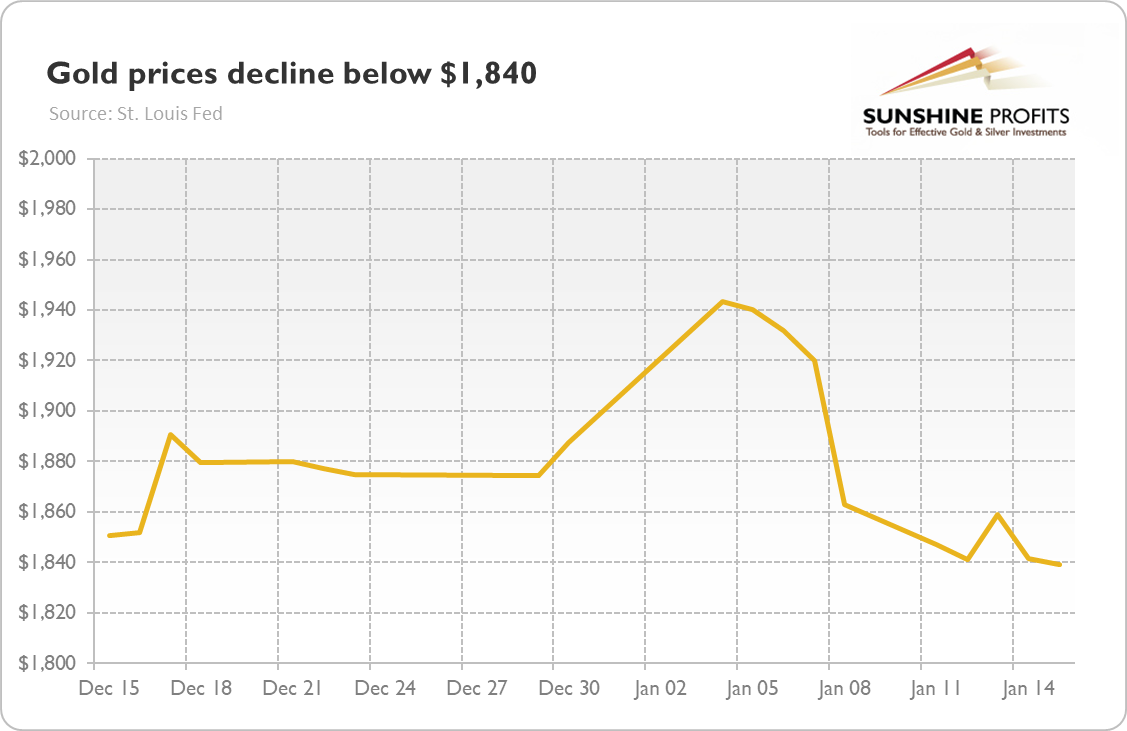

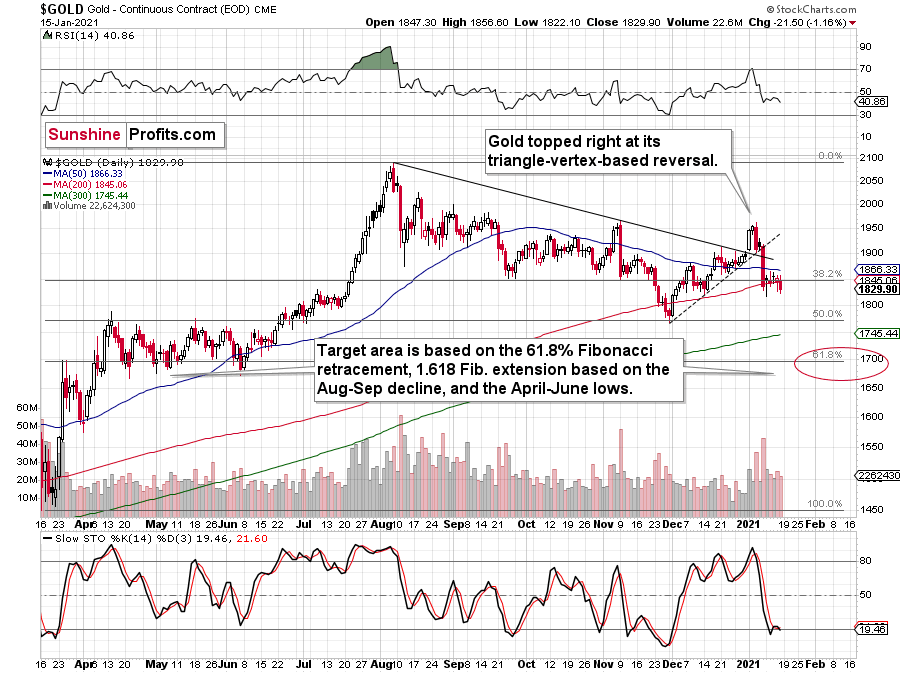

The weakness in the gold market continued last week. As the chart below shows, the London P.M. Fix declined below $1,840 on Friday (the price of the yellow metal declined later even further, i.e., below $1,830).

Figure 1

The downward trend is a bit disturbing given the poor economic data reported last week. First, the jobless claims increased from 784,000 on January 2 to 965,000 on January 9, 2021, as one can see in the chart below. The increase surpassed market expectations and indicates that there is a long way ahead for a full recovery in the U.S. labor market.

Figure 2

Second, U.S. retail sales declined 0.7 percent in December from the previous month. Importantly, the decrease was a larger than expected 0.1 percent drop. Third, the Empire State Index increased 3.5 percent in January. Although the index grew, it rose at a slower pace than in December and below expectations.

All these economic reports shows that the U.S. economy has slowed down, and we could see more stimulus coming in an effort to stimulate economic growth. Indeed, on Thursday (Jan. 14), Jerome Powell excluded any tapering of the quantitative easing in the near future, saying that he “expect[s] that the current pace of purchases will remain appropriate for quite some time”. The recent weak economic data that shows slack remaining in the labor market should only reassure the Fed that it ought to continue providing accommodation and not think about raising interest rates.

Moreover, on Thursday, President-elect Joe Biden unveiled a massive stimulus plan worth $1.9 trillion to support the economy amid the COVID-19 epidemic. The aid package, that would be on top of the $900 billion stimulus adopted by Congress in December, includes $1 trillion in direct checks to Americans, about $440 billion for small businesses (particularly those hit strongest by the epidemic), and about $415 billion to fight the coronavirus and speed up the distribution of the vaccinations.

The continuation of the dovish monetary policy and expansion of the easy fiscal policy should theoretically send the price of gold higher.

They should, but gold has gone south instead. Therefore, the drop in the gold prices amid poor economic data, Powell’s remarks, and Biden’s announcement is a bearish signal.

However, it might also be the case that we see a replay of March, when the first wave of the pandemic has initially hit the precious metals market. Investors were stocking up on cash then, selling both equities and gold. We observed a similar pattern on Friday (Jan. 15), so we could see a reversal after some time.

Moreover, if Biden’s fiscal aid is adopted, it would increase U.S. government spending, budget deficit and public debt even further. As a reminder, the federal government spent a record $6.5 trillion in fiscal 2020, while the national debt has already risen by almost $7.8 trillion during Trump’s presidency. According to an early January projection from the Committee for a Responsible Federal Budget, the U.S. fiscal deficit would total $2.3 trillion for fiscal 2021. However, with Biden’s new stimulus, it would be much larger and could even surpass the record deficit of $3.1 trillion for the last fiscal year.

So, the ballooning fiscal deficits and debts, together with a recession caused by the pandemic and the Great Lockdown, should be sufficient reasons to be cautious and hold part of one’s portfolio (the insurance part) in safe-haven assets such as gold. Yet many investors are still turning a blind eye to the negative effects of fiscal stimulus. But just because they cover their eyes, the elephant will not disappear from the room. Indeed, the gold elephant – and gold bull, his cousin – will not disappear, although they may hide for a while.

All in all, there are multiple fundamental reasons why gold is likely to soar in the upcoming years. However, even the most profound bull markets can’t move up in a straight line, and some corrections will likely take place. After the big rallies, we will probably witness significant corrections, and in the case of the precious metals market, one is long overdue.

To clarify, the significant correction in the precious metals market is already underway, but it seems that it’s not over yet, and it’s probably before its biggest and most important part.

Triggers for the decline in the precious metals market are not necessary – the market might collapse on its own or as a result of some lone random trigger that normally wouldn’t cause any major action. However, a trigger would speed things up. The less likely trigger might come from the general stock market – after all, it fell sharply together in the first half of this year.

S&P 500 (SPX) Signals

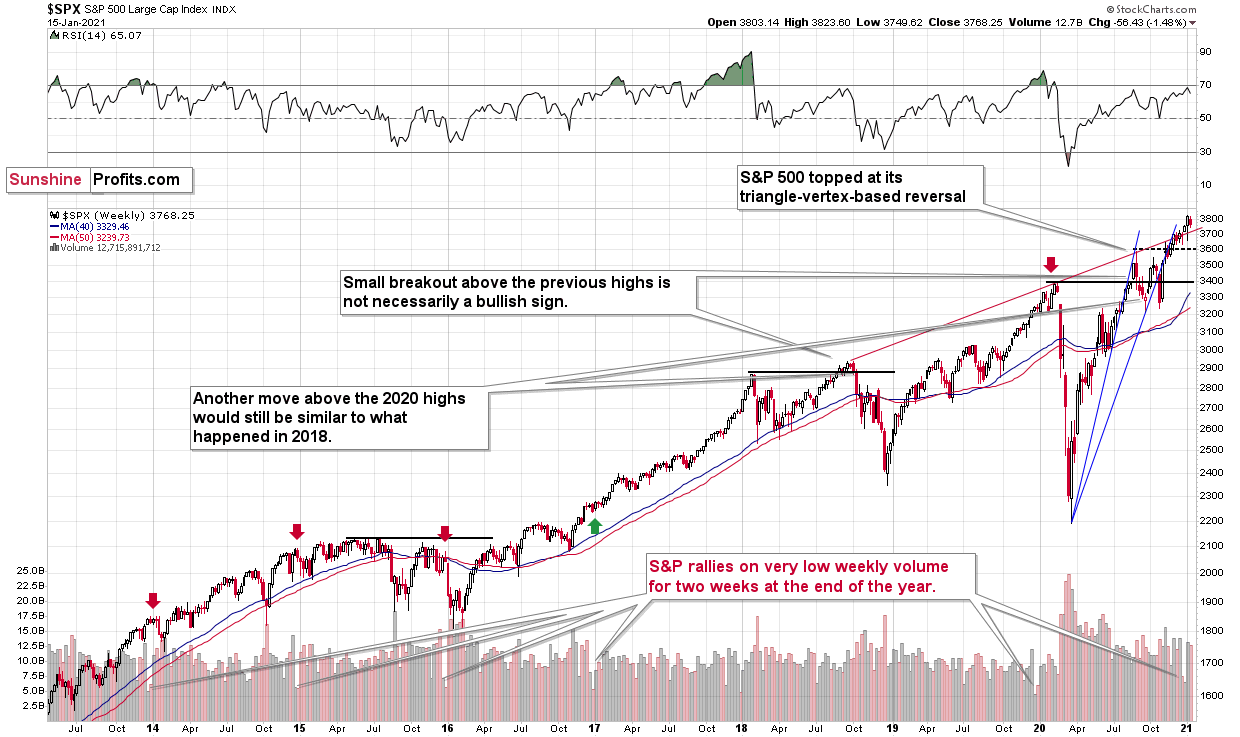

After coming within a whisker of 70 on the RSI (Relative Strength Index), the S&P 500 ran out of gas on Thursday and Friday (Jan. 14/15). And as a few creaks lead to larger repairs, its RSI is signaling that the SPX is about to break down.

Preceding six meaningful pullbacks since 2018, each time the SPX’s RSI approached (or exceeded) 70, a significant drawdown occurred.

Please see below:

Figure 3 – S&P 500 Index

And while it’s still too early to call a definitive top, the moody music of equities isn’t so sanguine anymore.

Beyond the technicals, valuations have also gone from excessive to extreme.

On Monday (Jan. 11), the NASDAQ (4.17x), S&P 500 (2.85x) and Russell 2000 (1.49x) all traded at their highest price-to-sales (P/S) ratios ever.

Please see below:

Figure 4 – (Source: Bloomberg/ Liz Ann Sonders)

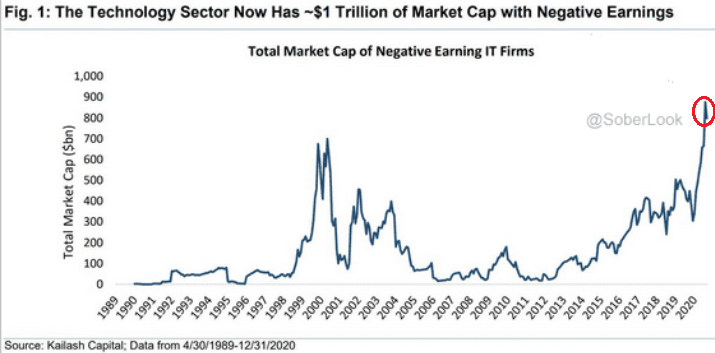

In addition, 2020 ended with U.S. investors granting the highest-ever combined market cap to technology companies with negative earnings.

Figure 5

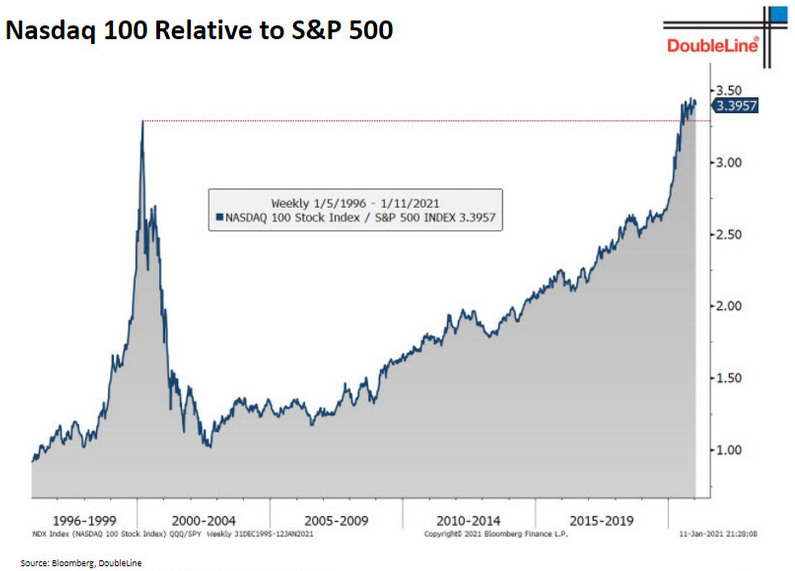

And making three of a kind, this record-setting feat also coincided with the NASDAQ 100 reaching its highest-ever relative outperformance of the S&P 500.

Figure 6

To explain, I wrote (Jan. 14):

The chart above plots the ratio of the NASDAQ 100’s price relative to the S&P 500’s price. When the line rises, it means that the NASDAQ 100 is outperforming and when the line falls, it means that the S&P 500 is outperforming. As you can see, the current value already exceeds the dot-com bubble peak.

More importantly though, the six largest companies in the NASDAQ 100 – Apple, Microsoft, Amazon, Tesla, Facebook and Alphabet – are also the six largest constituents of the S&P 500. Thus, if technology’s outperformance reverts back to its historical average, both indices will be slaughtered.

And how could this affect the precious metals?

Well, considering the interconnectedness of financial markets, a collapse of equities will shake the foundation of the PMs. As you read above, gold, silver and the HUI Index have 250-day (roughly one year) correlations with the S&P 500 of 0.64, 0.84 and 0.64 (For context, the closer they are to +1, the more often they move in the same direction.)

Thus, with recent equity strength helping to support the PMs, a reversal of this trend could lead to an even bigger decline for the PMs once it unfolds.

As a reminder, a decline in stocks is not required for the PMs to decline. However, given their moderate-to-strong correlations with the S&P 500, a break in the former could easily trigger a sell-off in the latter. And as history has shown, silver and the miners will be the hardest hit.

Goodbye 2020, Welcome 2021

With a December to remember already a January to forget, gold has started the New Year with two straight weekly declines (Also noteworthy, the yellow metal is down by more than $65 from its 2019 close.) And after last week’s muted response to Joe Biden’s $1.90 trillion stimulus package, the downtrend is poised to continue.

As 2020 quickly draws to a close and the champagne corks pop, precious metals investors have January 2021 on their mind and how gold will fare just after the New Year. Let’s take a quick look at what the previous years tell us.

In a nutshell, gold didn’t just “soar” in previous Januaries, but rather reversed at the end of the year and then moved in the opposite direction in January – canceling the December moves. “New year – new me” sounds cliché, but that’s what gold has actually been adhering to instead of simply soaring.

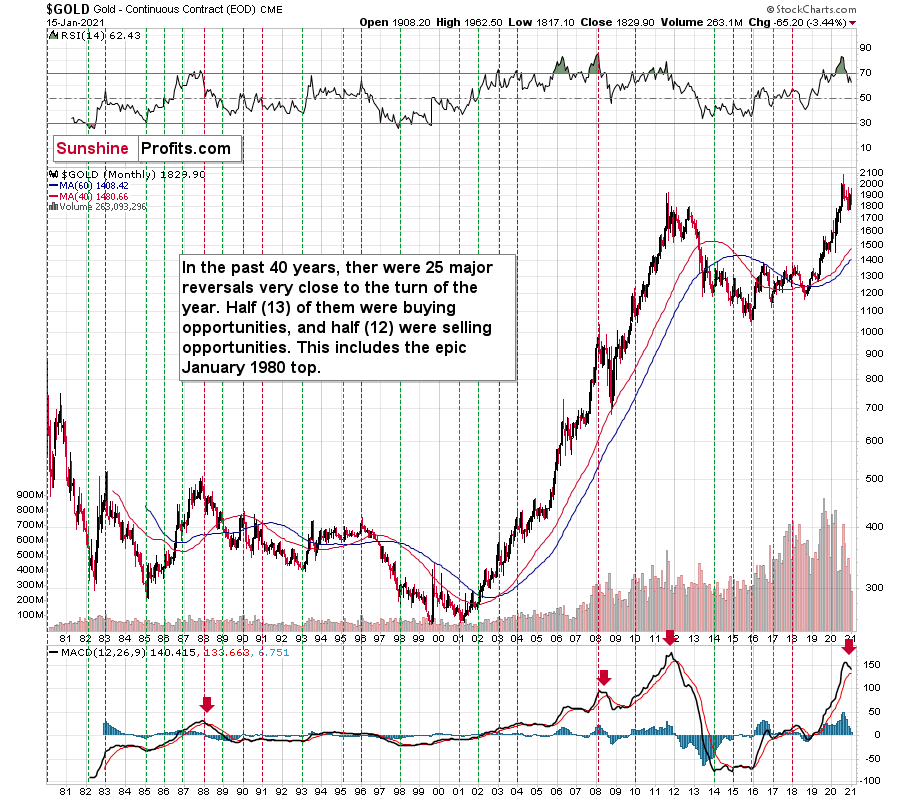

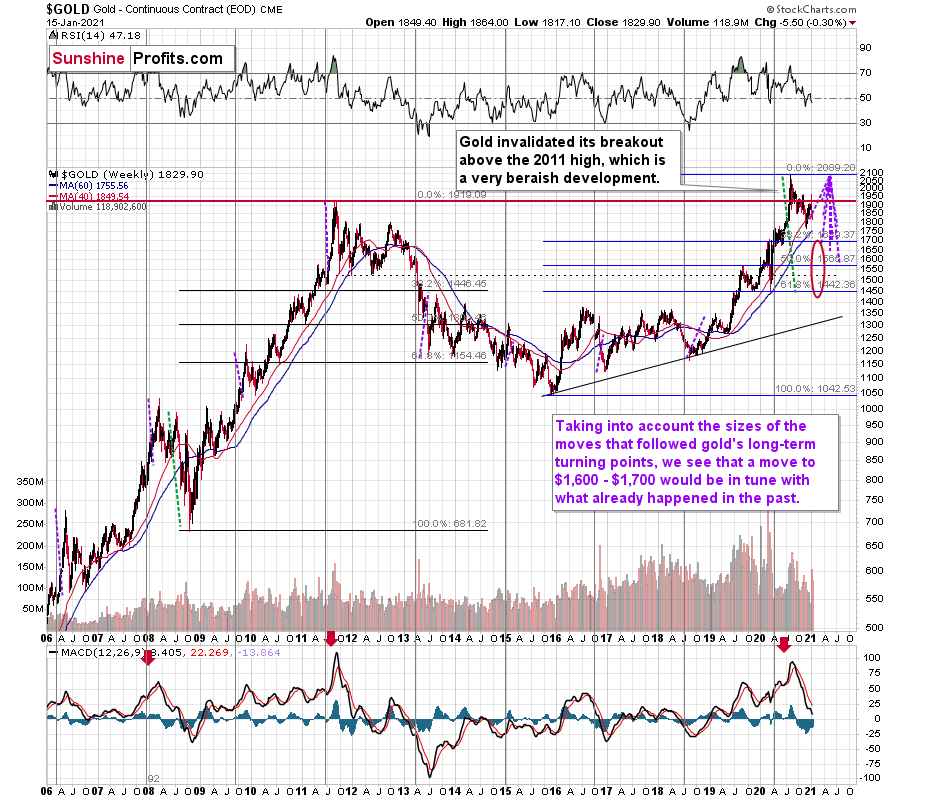

Let’s take a look at gold’s very long-term chart for details.

Figure 7 - Gold Continuous Contract Overview, GOLD and Moving Average Convergence Divergence Chart (MACD) Comparison

The above chart covers the past 40 years. The green vertical lines represent cases when (approximately) the turn of the year was a great buying opportunity. The red lines represent cases when (approximately) the turn of the year was a great selling opportunity.

There were 25 cases when gold visibly reversed close to the end of the year or the beginning of the new year – so that’s what happens in most cases.

In 13 of the cases, those were buying opportunities.

In 12 of the cases, those were selling opportunities.

Since the number of turning points is not divisible, the 13-12 breakdown is the closest that it can get to 50/50.

So, while it’s true that in most past cases, the turn of the year was positive for gold, it’s also true that the gold price forecast for January 2021 is not necessarily going to be bullish. The context is important, since:

- Gold has been rallying in December 2020

- Gold tends to reverse at the turn of the year

The implications of the 0 becoming a 1 at the end of the date are actually bearish for the yellow metal.

Moreover, please take a look at the lower part of the above chart. It features the MACD indicator based on the monthly gold prices. There were very few cases when this indicator moved up significantly and then clearly declined. This happened only four times in the previous four decades. Once in the late 1980s, once in early 2008, once in 2011, and once recently. In all previous cases, it heralded months of declines.

This does not bode well for the price of the yellow metal at all, especially considering that it recently invalidated its breakout above the 2011 high.

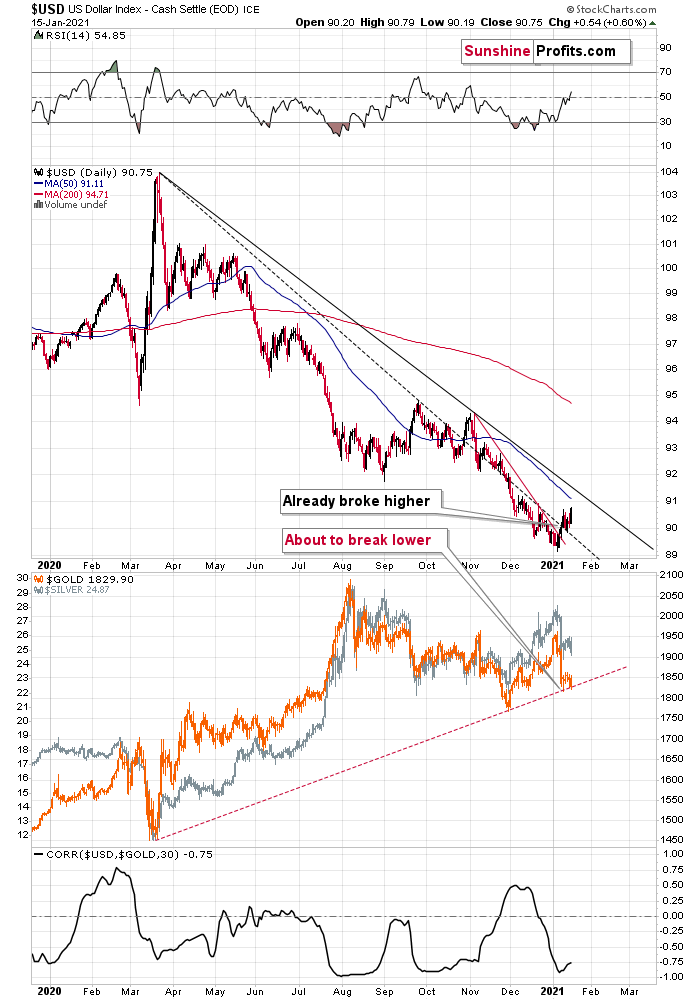

The USD Index (USDX)

Just over a week ago, the USD Index fell below 89.50, while gold traded above $1,954. Eight trading days later, the USDX has ripped to 90.75, while gold has fallen below $1,830.

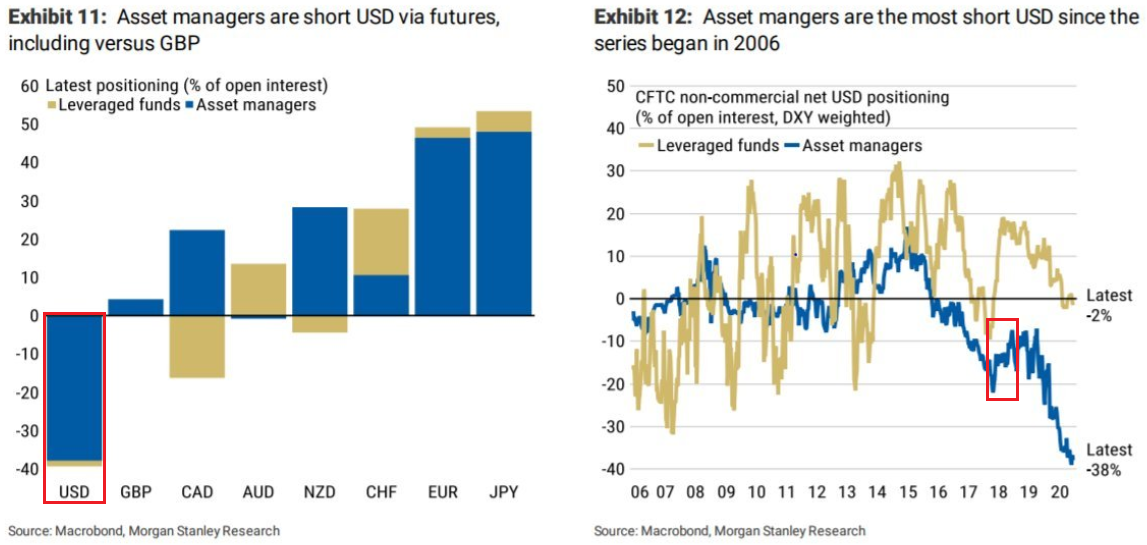

Warning about a potential USDX uprising, I wrote on Dec. 29 that we may be on the cusp of one of the biggest short-squeezes ever.

Please see the chart below:

Figure 8 – Net-short futures positions

If you analyze the second red box (on the right side), you can see that the 2018 top in net-short futures positions ended with a violent short-covering rally, which propelled the USDX nearly 11% higher from trough to peak.

And like a messy divorce, the USDX and gold continue to go their separate ways. On Friday (Jan. 15) the USDX rallied above its dashed resistance line (the dotted line below), confirming the breakout I highlighted previously. Moreover, the greenback’s next target is ~91.30 (the solid line below).

But as the rally unfolds, gold is hanging on for dear life. With its rising support line likely to break (the dotted line in the second chart below), gold will likely hit ~$1,700, consolidate, and then continue its downtrend trend. (For context, the call only changes if the yellow metal demonstrates sustained strength and rallies alongside the USDX.)

Figure 9

In addition, the USDX’s current flight may only be an appetizer to the main course. With the SPX showing cracks in its foundation, a potential drawdown of U.S. equities could put even more upward pressure on the USDX.

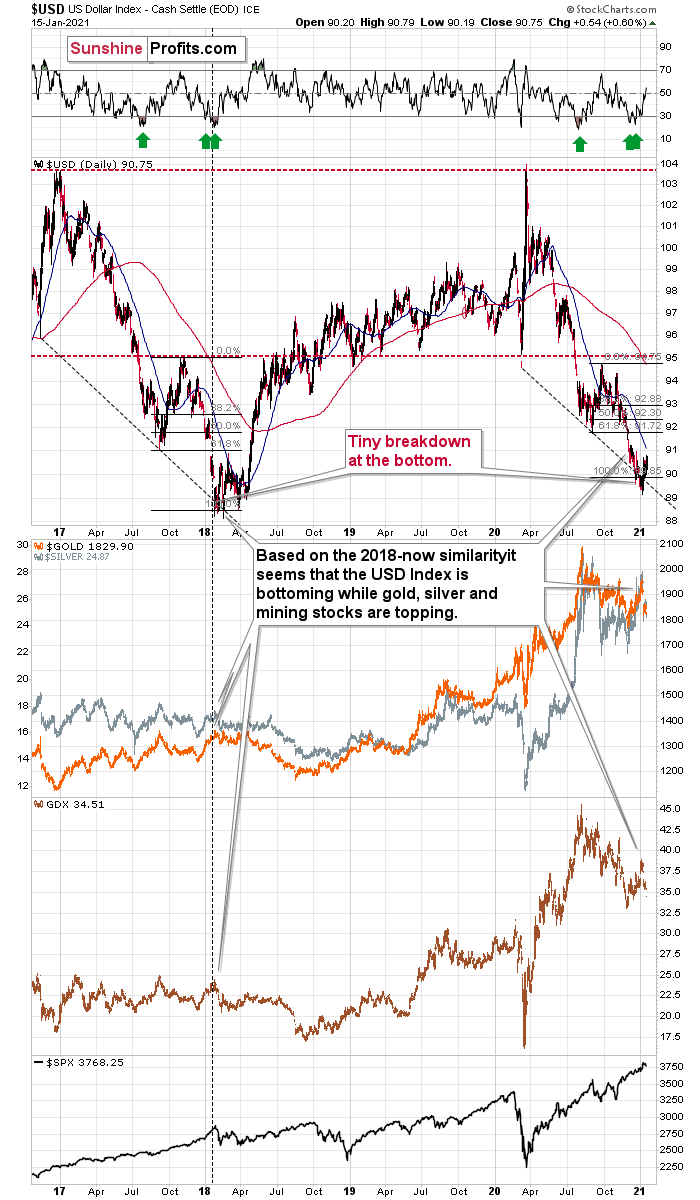

Also increasing the likelihood of a sustained bounce, the USDX’s RSI (Relative Strength Index) mirrors the double-bottom pattern seen in 2017-2018 (the green arrows on the below chart). As the initial pattern emerged (with the RSI below 30 in 2017), it preceded a significant rally, with the USDX’s RSI surging to nearly 70. And just like the chorus from your favorite song, the pattern repeated in 2018 with nearly identical results.

And today? Well, the choir is gearing up for its third act.

If you look at the pattern at the top-right of the chart below (Figure 10 - the green arrows), the USDX’s RSI bounced off identical oversold levels and is now trading north of 50.

Figure 10

For more on the USDX’s 2017-2018 analogue, I wrote previously:

It appears that the USD Index is repeating its 2017 – 2018 decline to some extent. The starting points of the declines (horizontal red line) as well as the final high of the biggest correction are quite similar. The difference is that the recent correction was smaller than it was in 2017.

And what happened to gold, silver and the gold miners in 2017-2018?

In short, they moved just a little higher after the USDX’s breakdown. I marked the moment when the U.S. currency broke below its previous (2017) bottom with a vertical line, so that you can easily see what gold, silver, and GDX (proxy for mining stocks) were doing at that time. They were just before a major top. The bearish action that followed in the short term was particularly visible in the case of the miners.

And as we move forward (and the USDX’s RSI continues its uprising), there are also several other catalysts to keep the momentum going:

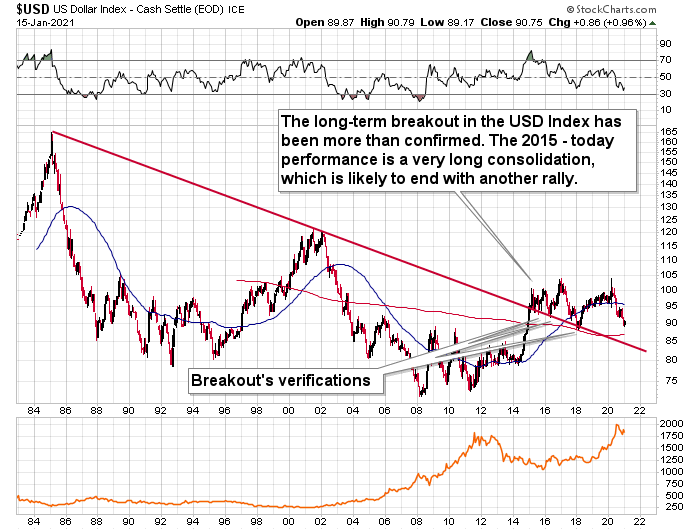

First, the USD Index is after a long-term, more-than-confirmed breakout. This means that the long-term trend for the U.S. currency is up.

Second, the amount of capital that was shorting the USD Index was excessive even before the most recent decline.

Third, a significant drawdown of the SPX could propel the USDX to levels similar to what we saw in March (If you analyze the chart above, you can see that the USDX bottom coincided with the SPX top.)

And rounding out the Four Horsemen of the Apocalypse?

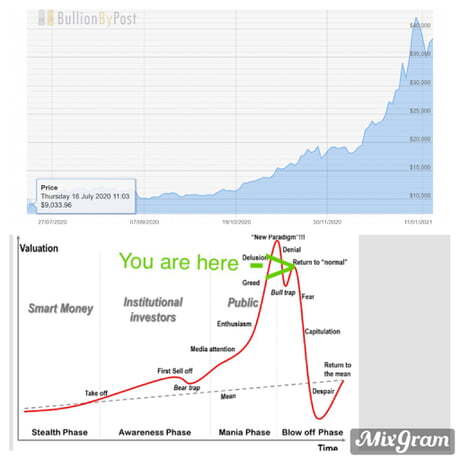

Bitcoin

On Jan. 6, I warned that a bubble was brewing. And after falling by more than 20% from its ~$40,000 peak, Bitcoin’s bubble may have already burst. If you analyze the visuals below, I want you to focus on the green arrow. Like 12 steps to sobriety, a return to ‘normal’ isn’t without fear. And once fear gives way to capitulation, the March-like fervor could ignite the USDX back to its previous highs. Even a smaller rally in the latter would likely trigger a huge sell-off in the precious metals, though. After all, the USDX rallied by only 0.86 so far this year (taking Friday’s closing price into account), but gold is down by over $65.

Figure 11

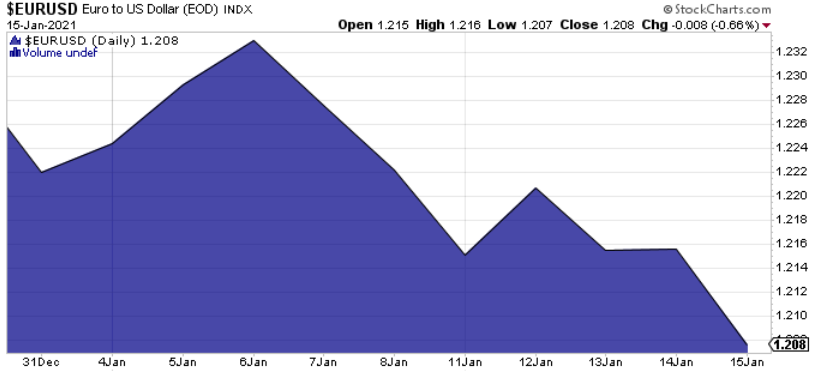

Turning to fundamentals, the EUR/USD is also starting to wobble (Remember, the EUR/USD accounts for nearly 58% of the USDX’s movement.) The currency pair has fallen by 2% over the last seven trading days and I’ve been raising the alarm about deteriorating Eurozone fundamentals.

On Dec. 28, I wrote:

The Eurozone economy is in free-fall.

Remember, currencies trade on a relative basis. Thus, a less-bad U.S. economy is good news for the U.S. dollar.

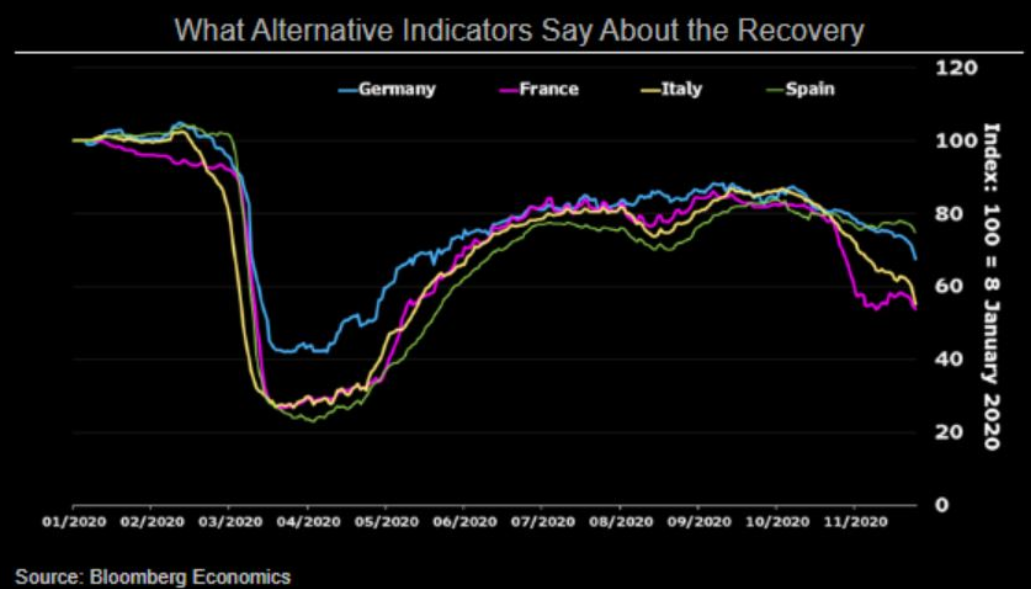

Please see below:

Figure 12 – Alternative Economic Indicators in 2020 for Germany, France, Italy, and Spain

Across Europe’s largest economies – Germany, France, Italy and Spain – economic activity is rolling over (To explain the chart, alternative economic indicators are high-frequency data like credit card spending, indoor dining traffic, travel activity and location information.)

And underpinning the irrationality, the deceleration is happening as the euro is strengthening.

Make sense?

Then, on Jan. 12, I wrote:

Beginning the New Year in style, the USD Index’s four-day rally is starting to shift sentiment.

I wrote previosuly that the EUR/USD is ground zero in the USDX’s battle for redemption. And whether its retail sales, consumer inflation, monetary spending (relative to GDP) or alternative economic indicators, the euro is inching ever-closer to surrender.

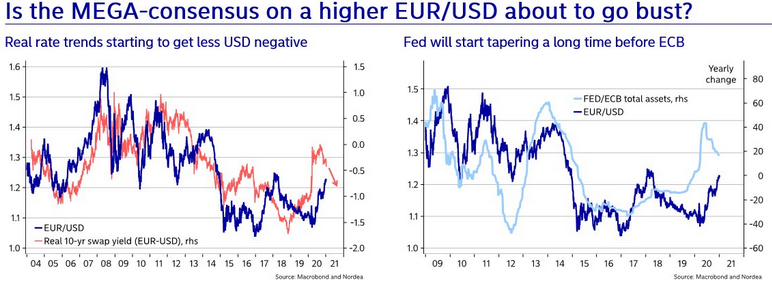

Please see below:

Figure 13

If you analyze the first chart (Figure 13 - on the left), it highlights another issue that I’ve been discussing for some time. On Monday (Jan. 11), the U.S. 10-Year real yield rose to an intraday high of – 0.912%, delivering a 0.168% spread increase in just five trading days. And if you look at the orange line on the chart, you can see that EUR/USD (the dark blue line) tends to follow the direction of real interest rate differentials (the orange line). Thus, if U.S. real yields keep rising (relative to Europe), EUR/USD’s four-day losing streak will likely continue.

Turning to the second chart (Figure 13 - on the right), notice how the EUR/USD tracks the FED/ECB ratio? To explain, the ratio (the light blue line) is calculated by dividing the U.S. Federal Reserve’s (FED) balance sheet by the European Central Bank’s (ECB) balance sheet. Essentially, its direction tells you which monetary authority is printing more money. If you analyze the EUR/USD (the dark blue line), it trades higher when the FED is out-printing the ECB (the light blue line is rising) and trades lower when the ECB is out-printing the FED (the light blue line is falling). The key takeaway? With the light blue line falling, it means that the ECB is outprinting the FED. And if this dynamic continues, the EUR/USD (the dark blue line) should move lower as well.

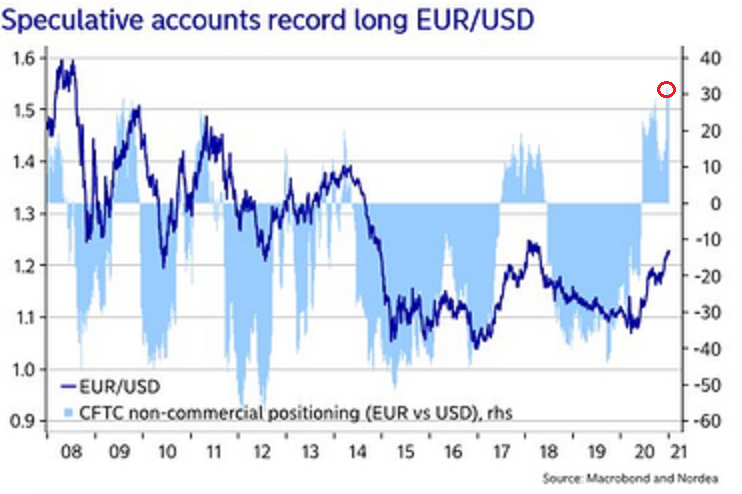

Making three of a kind, (and like I mentioned at the beginning), futures positioning could be the scream that starts the avalanche.

Please see below:

Figure 14

To explain, the light blue bars (Figure 7) represent the net-positioning of non-commercial futures traders (speculators), while the dark blue line is the movement of EUR/USD. Please focus on the red circle at the top-right of the chart: right now, bullish futures bets on EUR/USD are at their highest level since before the financial crisis.

More importantly, notice how one-sided positioning (in both directions) often leads to a sharp reversal?

If you analyze the 2009 to 2011 period, you can see that the EUR/USD plunged almost immediately after speculative futures positioning approached (or hit) the 30-level (using the vertical scale on the right side of the chart). And with today’s positioning already exceeding 30 (the red circle), there is plenty of room for the EUR/USD to move lower.

The bottom line?

The euro’s pain is the USDX’s gain. And after Wednesday’s (Jan. 13) revelation that Italy’s government is on the brink of collapse (Italy being the Eurozone’s third-largest economy that also has the second-highest debt-to-GDP in the Eurozone), political instability is the latest fundamental variable foretelling a weaker euro.

For more on a potential uprising, please see the USDX’s long-term breakout in 2015:

Figure 15 – USD Index Futures Contract (ICE)

The duration of the move, the multiple breakouts, and the five-year consolidation signals a move higher for the USDX. This remains the path of least resistance (perhaps to the ~120 level).

Please note that the consolidation that preceded the previous rally to 120 that took place between 1997 and 2000 happened when the USD index was trading at relatively similar price levels – approximately between 90 and 105.

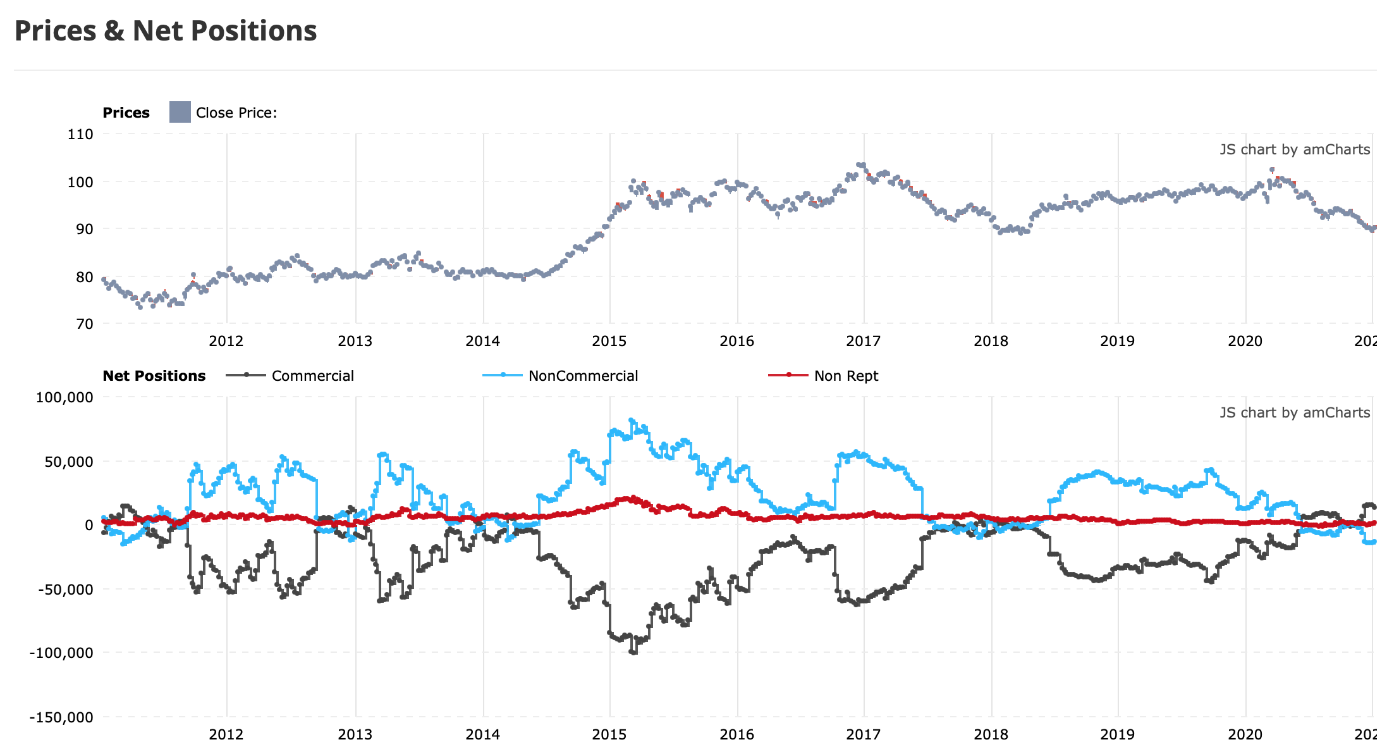

A second major factor is extreme USDX bearishness within the futures market. A contrarian indicator, net-short USDX futures positions remain excessively high.

Figure 16 – Commitment of Traders Report

To explain, there is an extreme divergence between commercial traders (the dark blue line) and non-commercial traders (the light blue line). For context, commercial traders are gold producers (miners), while non-commercial traders are speculators (hedge funds, prop traders).

Knowing the difference is extremely important, because the two parties have differing views on where the precious metals are headed.

On Jan. 6, I wrote:

Since Jun. 15, the two parties have drawn opposite lines in the sand. While speculators increased their long positions, producers took the other side of the trade. And despite the yellow metal leaping above $2,000 soon after (mainly momentum driven), gold topped less than two months later and fell by 15.4% before reaching a bottom on Nov. 30 (intraday peak to trough).

Regarding silver, the results are identical. However, producers’ timing was much more prescient.

Since Aug. 17, producers and speculators have traded in opposite directions. In September, with speculators still buying, the white metal rallied to an intraday high of $29.24 (on Sept. 1). However, in just over three weeks, silver plunged by 25.4% before bottoming on Sep. 24.

The key takeaway?

Commercial traders (producers) study the market more intently than speculators. And because they have more to lose than just the trigger of a stop-loss, producers are usually on the right side of the trade.

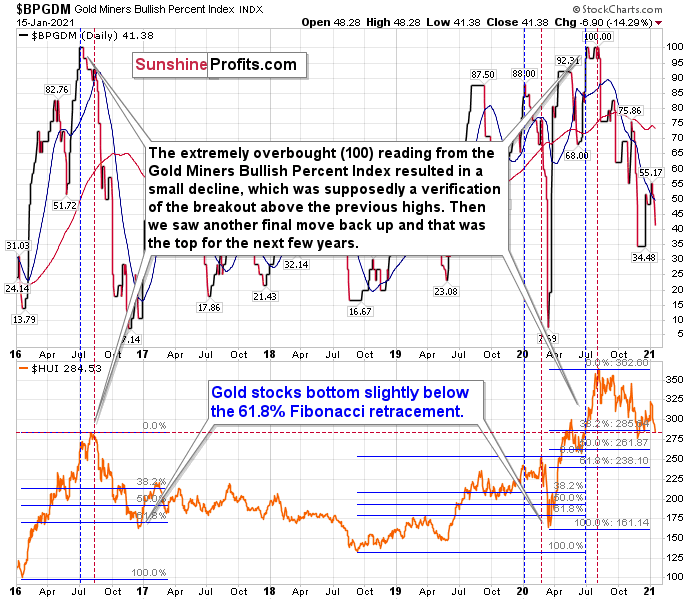

Sentiment Indicators

After last week’s lull, the Gold Miners Bullish Percent Index ($BPGDM) sunk to 41. However, the index is still more than 30 points above its 2016 and 2020 lows.

On Dec. 14, I wrote:

Back in 2016 (after the top), and in March 2020, the buying opportunity didn’t present itself until the $BPGDM was below 10.

Thus, with sentiment still elevated, it will take a lot more negativity for gold to find a bottom.

Figure 17 - Gold Miners Bullish Percent Index ($BPGDM) and NYSE Arca Gold BUGS Index (HUI) Comparison

I wrote previously:

The excessive bullishness was present at the 2016 top as well and it didn’t cause the situation to be any less bearish in reality. All markets periodically get ahead of themselves regardless of how bullish the long-term outlook really is. Then, they correct. If the upswing was significant, the correction is also quite often significant.

Please note that back in 2016, there was an additional quick upswing before the slide and this additional upswing had caused the $BPGDM to move up once again for a few days. It then declined once again. We saw something similar also in the middle of this year. In this case, the move up took the index once again to the 100 level, while in 2016 this wasn’t the case. But still, the similarity remains present.

Back in 2016, when we saw this phenomenon, it was already after the top, and right before the big decline.

Based on the decline from above 350 to below 280, we know that a significant decline is definitely taking place. But has it already run its course?

Let’s consider two similar cases when gold miners declined significantly after the $BPGDM was very high: the 2016 decline and early-2020 decline.

In both cases, the HUI Index continued to decline until it moved slightly below its 61.8% Fibonacci retracement level. This means that if the history is to repeat itself, we shouldn’t expect any major turnaround until the gold miners decline to 220 - 230 or so. Depending on how things are developing in gold, the above might or might not be the final bottom, though.

Please note that the HUI already declined below its 2016 high. This breakdown is yet another bearish sign.

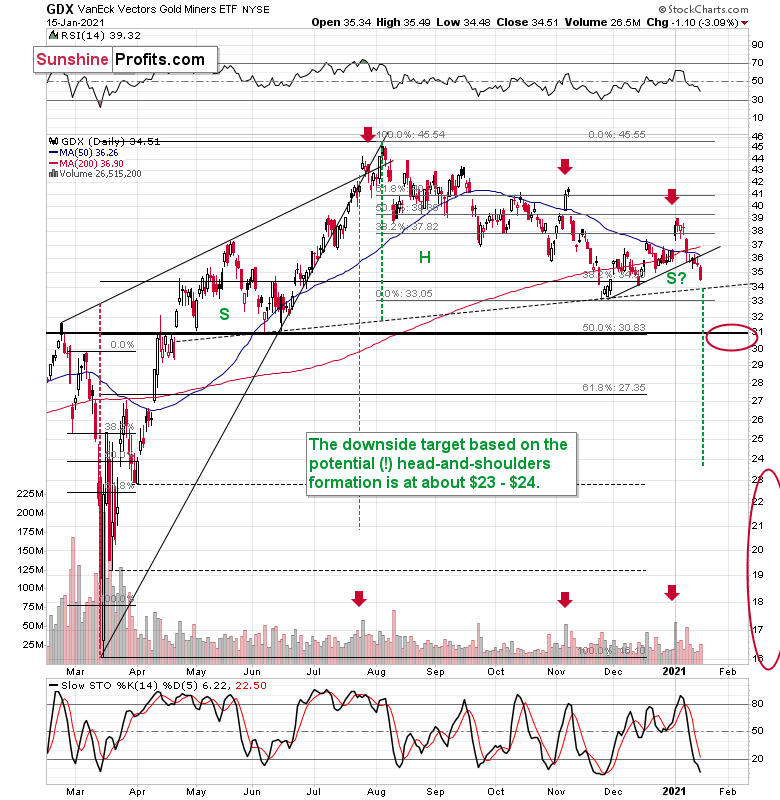

The Gold Miners

With prior support now having changed to resistance, the walls are closing in on the GDX ETF. After recording three consecutive closes below its rising support line (plus the weekly close), the price action confirmed the bearish breakdown.

Moreover, Friday’s (Jan. 15) close was the lowest of the year and the GDX ETF continues to form the right shoulder of its potential head and shoulders pattern. If the bearish prospect becomes reality, we could see a decline to the $24 to $23 range.

Please see the chart below:

Figure 18 - VanEck Vectors Gold Miners ETF (GDX), GDX and Slow Stochastic Oscillator Chart Comparison – 2020

To explain, I wrote on Jan. 11:

If you analyze the chart above, the area on the left (marked S) represents the first shoulder, while the area in the middle (H) represents the head and the area on the right (second S) represents the potential second shoulder.

Right now, $33.7-$34 is the do-or-die area. If the GDX breaks below this (where the right shoulder forms) it could trigger a decline back to the $24 to $23 range (measured by the spread between the head and the neckline; marked with green).

Since there’s a significant support at about $31 in the form of the 50% retracement based on the 2020 rally, and the February 2020 high, it seems that we might see the miners pause there. In fact, it wouldn’t be surprising to see a pullback from these levels to about $33, which could serve as the verification of the completion of the head-and-shoulder pattern. This might take place at the same time, when gold corrects the decline to $1,700, but it’s too early to say with certainty.

Foretelling the New Years’ massacre – with the GDX ETF moving lower in eight out of 2021’s 10 trading session – I warned about bearish developments in previous Gold & Silver Trading Alerts.

I cited:

- A huge volume spike in the first session of 2021 was very similar to what we saw at the November 2020 and July 2020 tops – this heralded declines.

- The GDX’s stochastic oscillator bounced above 80, mirroring similar readings that preceded five pullbacks since September.

- Arguably the most important indication that keeps on flashing the very bearish signals , the GDX’s underperformance relative to gold remained intact.

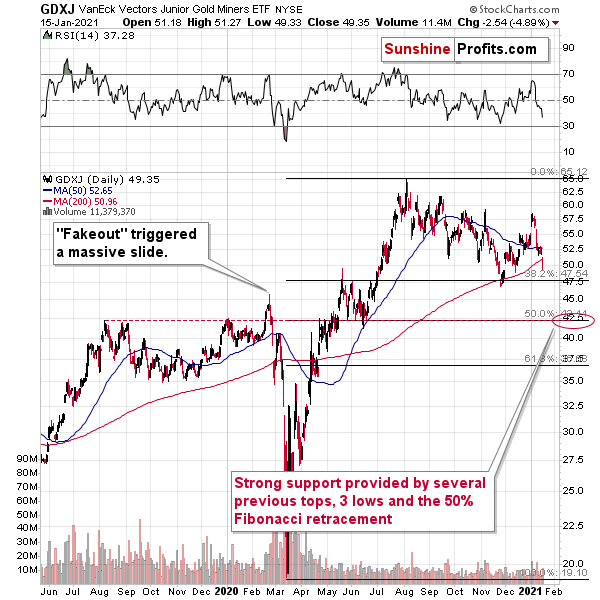

Moving on to the GDXJ ETF (a proxy for the junior gold miners), the little brother is also sending ominous signals. Poised to re-test the ~$42.50 range, the GDXJ ETF (just like GDX) put in several tops and three previous bottoms at the 50% Fibonacci retracement level.

If you analyze the chart below, you can see that the GDXJ ETF put in three adjacent tops in 2019/2020 and put in a similar bottom in June of 2020. This makes the proximity of $42.5 a strong support and something that’s likely to trigger at least a corrective upswing after a profound decline.

Figure 19

Thus, if the forecast proves prescient (and given the size of the potential move), the GDXJ ETF is likely to underperform the GDX ETF over the next few weeks (i.e. decline more than GDX on a relative basis).

Please see below:

Figure 20

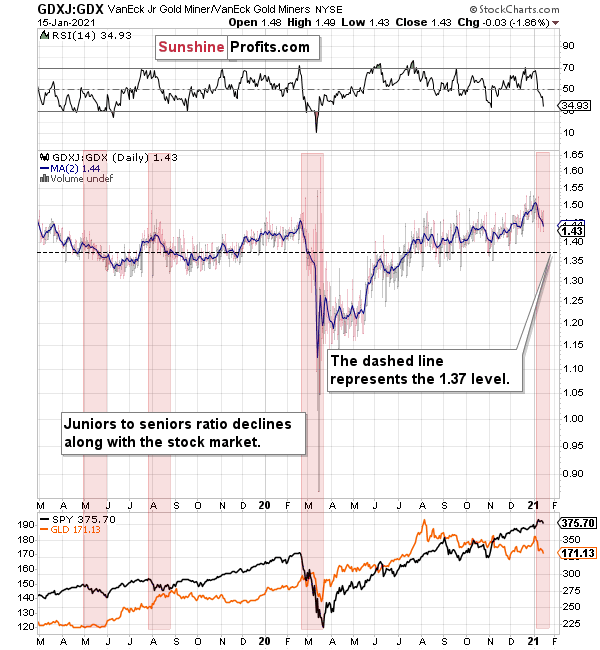

To explain, the above chart depicts the ratio of the GDX ETF’s price relative to the GDXJ ETF’s price (the dark blue line above). When the line is rising, it means that the GDXJ ETF is outperforming the GDX ETF. Conversely, when the line is falling, it means that the GDX ETF is outperforming the GDXJ ETF. If you analyze the right-half, you can see that the GDXJ ETF has massively outperformed since late May.

However, once the calendar turned (to 2021), the ratio has made a vertical move lower. Thus, if both ETFs reach their 50% Fibonacci retracement levels ($42.50 and $31 respectively), the ratio above should drop from 1.43 to 1.37. As a result, the GDXJ ETF will incur a swifter drawdown. Given the pace at which the ratio has been declining so far this year, the above is easily achievable – the pace of decline would simply have to continue.

Also supporting the underperformance, the GDXJ ETF’s high-beta nature (and stronger correlation with the S&P 500) means that as the SPX falls, more damage is being done to the GDXJ ETF. Please note how closely linked the declines were in case of the GDXJ/GDX ratio and the general stock market (black line in the lower part of the chart). This also explains why the juniors to seniors ratio moved higher since the March bottom.

Thus, if the S&P 500 hits a wall (like I mentioned above), the GDXJ/GDX ratio should continue its free fall.

In addition, I wrote previously:

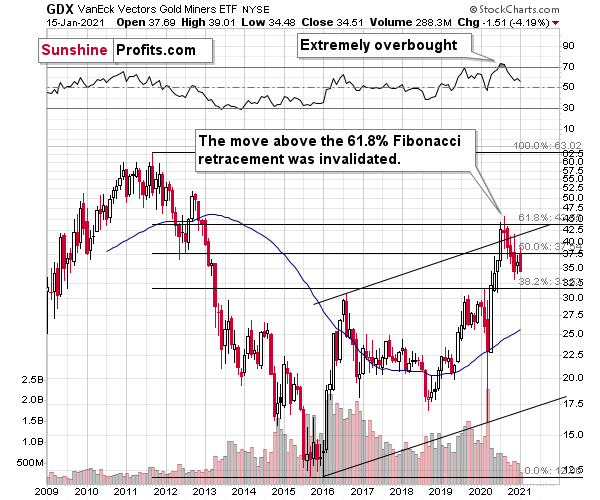

Let’s not forget that the GDX ETF has recently invalidated the breakout above the 61.8% Fibonacci retracement based on the 2011 – 2016 decline.

Figure 21 - GDX VanEck Vectors Gold Miners ETF (2009 – 2020)

When GDX approached its 38.2% Fibonacci retracement, it declined sharply – it was right after the 2016 top. And miners’ inability to move above the 61.8% Fibonacci retracement level and their invalidation of the tiny breakout is a bearish sign. The same goes for miners’ inability to stay above the rising support line – the line that’s parallel to the line based on the 2016 and 2020 lows.

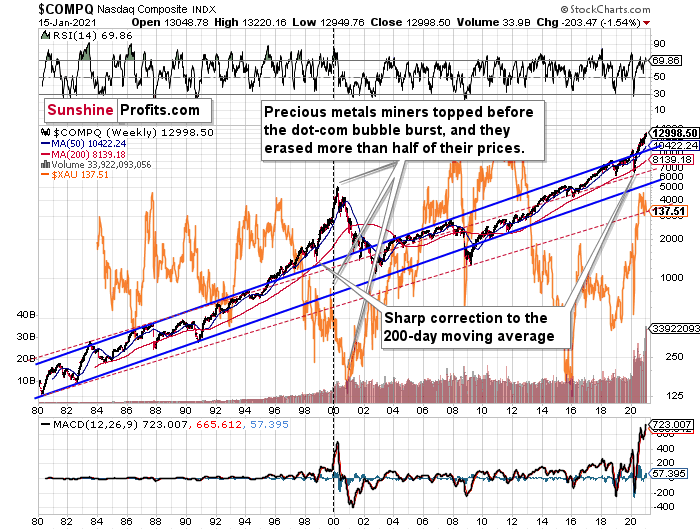

As icing on the cake, irrational exuberance across the NASDAQ (which I also highlighted above), could lead to a violent ending for the gold miners. Back in 2000 – when the dot-com bubble burst – the gold miners lost more than half of their value.

Please see below:

Figure 22

To explain, the two long-term channels above (the solid blue and red dashed lines), show that the NASDAQ is trading well above both historical trends.

Please note that the final part of the huge upswing materialized after the NASDAQ quickly declined to its 200-day moving average which was also slightly above the upper border of the rising trend channel marked with red dashed lines. We saw exactly the same thing in the first half of 2020.

The similarity between these two periods is also evident if one looks at the MACD indicator. There has been no other, even remotely similar, situation where this indicator would soar so high.

Furthermore, and because the devil is in the details, the gold miners’ 1999 top actually preceded the 2000 NASDAQ bubble bursting. It’s clear that miners (the XAU Index serves as a proxy) are on the left side of the dashed vertical line, while the tech stock top is on its right side. However, it’s important to note that it was stocks’ slide that exacerbated miners’ decline. Right now, the mining stocks are already declining, and the tech stocks continue to rally. Two decades ago, tech stocks topped about 6 months after miners. This might spoil the party of the tech stock bulls, but miners topped about 6 months ago…

Gold

After incoming U.S. President Joe Biden unveiled his $1.90 trillion stimulus package, crickets were heard across the gold market. The once boisterous crowd yawned with boredom, as rising U.S. yields and a resurgent U.S. dollar soaked up all of the attention (and the liquidity).

But preceding the despair, gold’s fate was sealed when it reached its triangle-vertex-based reversal point after a short-term rally (a topping indicator that I warned about previously). And now, with the miners’ underperformance prophesying a much steeper decline, fireworks could be on display in the coming weeks.

Please see below:

Figure 23 - Gold Continuous Contract Overview and Slow Stochastic Oscillator Chart Comparison

Gold is after a significant decline and also a pause that immediately followed. This means that it can slide once again any day (or hour) now. The tiny buy signal from the Stochastic indicator (lower part of the above chart) was already nullified by a sell signal. A similar occurence resulted in declines in late November.

Interestingly, please note that back in November, gold’s second decline (second half of the month) was a bit bigger than the initial (first half of the month) slide that was much sharper. The January performance is very similar so far, with the difference being that this month, the initial decline that we saw in the early part of the month was bigger.

This means that if the shape of the price moves continues to be similar, the next short-term move lower could be bigger than what we saw so far in January and bigger than the decline that we saw in the second half of November. This is yet another factor that points to the proximity of $1,700 as the next downside target.

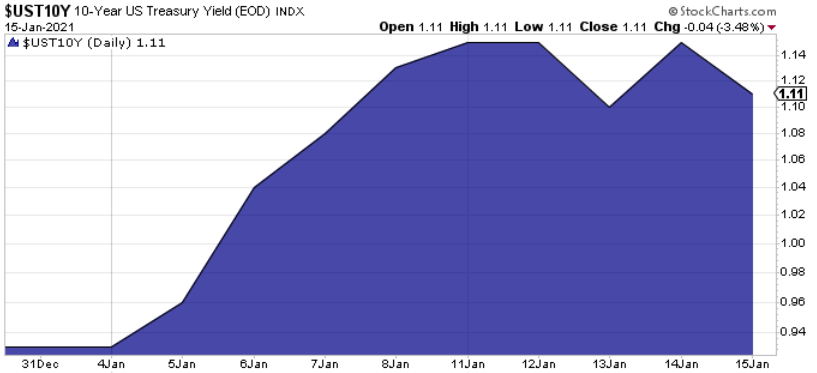

In addition, fundamentals are also starting to take effect. The U.S. 10-Year yield has surged by more than 19% since the New Year, and despite Friday’s (Jan. 15) pullback, it still closed above Wednesday’s (Jan. 13) low.

Figure 24

And like a double-edged sword, the rising 10-year yield is accelerating the EUR/USD’s 2021 fall from grace (another development that’s hurting gold’s short-term prospects). And because the EUR/USD accounts for nearly 58% of the movement in the USD Index, a continuation of the trend could spell trouble for gold (As I mentioned on Jan. 15, gold’s 250-day correlation with the USDX is – 0.80.)

Figure 25

In summary, lower gold prices remain the path of least resistance. Until the miners start pulling their weight, gold is stuck in limbo. And because bearish technicals and fundamentals support another move lower for the GDX ETF, gold is unlikely to buck the trend. However, once the dynamic reverses, it will provide an attractive opportunity to profit from the eventual upswing.

Before moving on, I want to reiterate my previous comments and explain why gold is likely to bottom at roughly $1,700:

One of the reasons is the 61.8% Fibonacci retracement based on the recent 2020 rally, and the other is the 1.618 extension of the initial decline. However, there are also more long-term-oriented indications that gold is about to move to $1,700 or lower.

(…) gold recently failed to move above its previous long-term (2011) high. Since history tends to repeat itself, it’s only natural to expect gold to behave as it did during its previous attempt to break above its major long-term high.

And the only similar case is from late 1978 when gold rallied above the previous 1974 high. Let’s take a look at the chart below for details (courtesy of chartsrus.com)

Figure 26 - Gold rallying in 1978, past its 1974 high

As you can see above, in late 1978, gold declined severely right after it moved above the late-1974 high. This time, gold invalidated the breakout, which makes the subsequent decline more likely. And how far did gold decline back in 1978? It declined by about $50, which is about 20% of the starting price. If gold was to drop 20% from its 2020 high, it would slide from $2,089 to about $1,671.

This is in perfect tune with what we described previously as the downside target while describing gold’s long-term charts:

Figure 27 - Relative Strength Index (RSI), GOLD, and Moving Average Convergence Divergence (MACD) Comparison

The chart above shows exactly why the $1,700 level is even more likely to trigger a rebound in gold, at the very minimum.

The $1,700 level is additionally confirmed by the 38.2% Fibonacci retracement based on the entire 2015 – 2020 rally.

There’s also a good possibility that gold could decline to the $1,500 - $1,600 area or so (50% - 61.8% Fibonacci retracements and the price level to which gold declined initially in 2011), but based on the size of the recent upswing, we no longer think that this scenario is the most likely one.

Before looking at the below chart, please note the – rather obvious – fact. Gold failed to break above its 2011 highs. Invalidations of breakouts are sell signals, and it’s tough to imagine a more profound breakout that could have failed. Thus, the implications are extremely bearish for the next several weeks and/or months.

Figure 28 - RSI, GOLD, and MACD Comparison

The odd thing about the above chart is that I copied the most recent movement in gold and pasted it above gold’s 2011 – 2013 performance. But – admit it – at first glance, it was clear to you that both price moves were very similar.

And that’s exactly my point. The history tends to rhyme and that’s one of the foundations of the technical analysis in general. Retracements, indicators, cycles, and other techniques are used based on this very foundation – they are just different ways to approach the recurring nature of events.

However, every now and then, the history repeats itself to a much greater degree than is normally the case. In extremely rare cases, we get a direct 1:1 similarity, but in some (still rare, but not as extremely rare) cases we get a similarity where the price is moving proportionately to how it moved previously. That’s called a market’s self-similarity or the fractal nature of the markets. But after taking a brief look at the chart, you probably instinctively knew that since the price moves are so similar this time, then the follow-up action is also likely to be quite similar.

In other words, if something looks like a duck, and quacks like a duck, it’s probably a duck. And it’s likely to do what ducks do.

What did gold do back in 2013 at the end of the self-similar pattern? Saying that it declined is true, but it doesn’t give the full picture - just like saying that the U.S. public debt is not small. Back then, gold truly plunged. And before it plunged, it moved lower in a rather steady manner, with periodic corrections. That’s exactly what we see right now.

Please note that the above chart shows gold’s very long-term turning points (vertical lines) and we see that gold topped a bit after it (not much off given their long-term nature). Based on how gold performed after previous long-term turning points (marked with purple, dashed lines), it seems that a decline to even $1,600 would not be out of ordinary.

Finally, please note the strong sell signal from the MACD indicator in the bottom part of the chart. The only other time when this indicator flashed a sell signal while being so overbought was at the 2011 top. The second most-similar case is the 2008 top.

The above-mentioned self-similarity covers the analogy to the 2011 top, but what about the 2008 performance?

If we take a look at how big the final 2008 decline was, we notice that if gold repeated it (percentage-wise), it would decline to about $1,450. Interestingly, this would mean that gold would move to the 61.8% Fibonacci retracement level based on the entire 2015 – 2020 rally. This is so interesting, because that’s the Fibonacci retracement level that (approximately) ended the 2013 decline.

History tends to rhyme, so perhaps gold is going to decline even more than the simple analogy to the previous turning points indicates. For now, this is relatively unclear, and my target area for gold’s final bottom is quite broad.

Silver

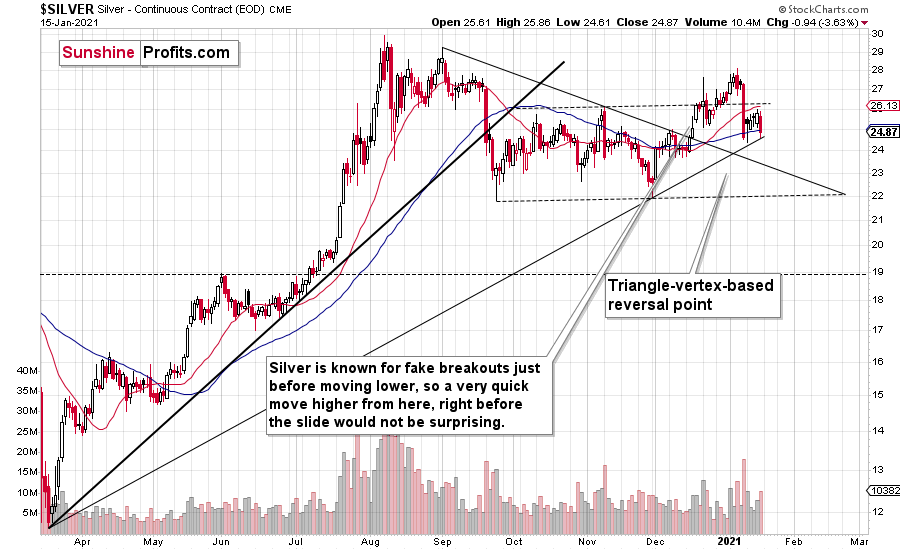

Like a Formula One racer lining up for the Tour de France, silver continues to leave gold and the gold miners in the dust.

But over the last few weeks, I’ve highlighted silver’s reputation for deception. During the final parts of the rally, silver usually outperforms both the GDX and gold, while gold outperforms the GDX (and – ideally – underperforms relative to the USD Index). And after the previous Friday’s (Jan. 8) 9.63% plunge, traders learned this lesson the hard way.

Figure 29 - COMEX Silver Futures

Still unsure of its next move, silver remains in consolidation mode. However, once the dam breaks, silver’s downward flood will likely outpace gold and the gold miners. If you analyze the chart above, you can see that silver is trading right at its medium-term rising support line (which begins at the bottom left corner of the chart). And with a breakdown likely to cause a tsunami of selling, the first wave could be fast and furious. If not the first wave, then the second – after the post-breakdown consolidation.

And when should we expect this climax? Quite likely soon, as miners have already broken below their declining support line. When will silver start declining more than the miners? It’s a tough call. It seems that we are not yet in the final part of the decline, so “not yet” seems the best reply at this time.

The white metal has its next triangle-vertex-based reversal in the second half of February, around Feb. 23. That’s when we might see the next reversal in the precious metals market.

Please note that the above could take the form of a bottom or a top. We’ll know more once we get closer to this date.

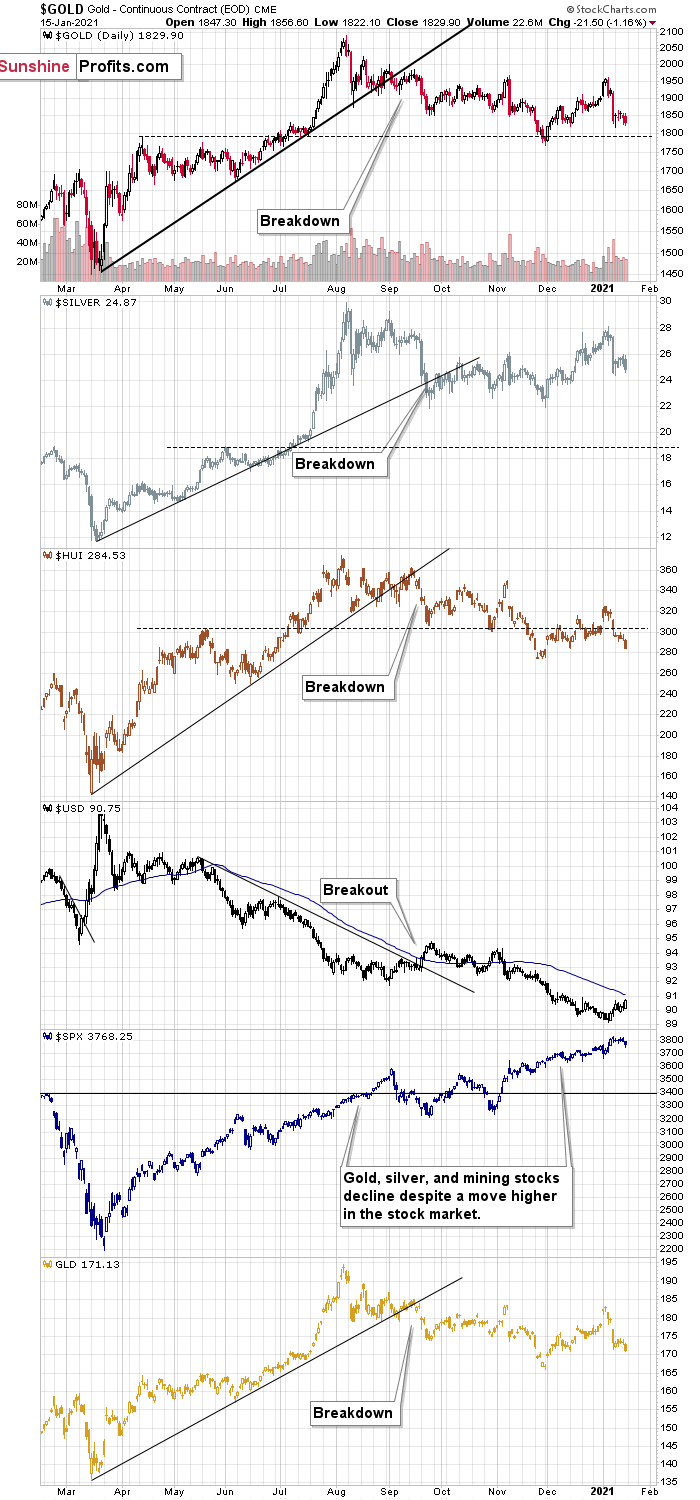

For more insight, let’s analyze the relative performance of gold, silver and the gold miners, and compare how they’re impacted by the USDX and the SPX. If you analyze the chart below, you can see that the precious metals all broke down in September after the USDX broke above resistance.

Figure 30 - GOLD, SILVER, HUI, USD, SPX, GLD Comparison

And like traffic lights flashing red, notice how the HUI Index (proxy for gold stocks) is trading well below its early 2020 highs? In stark contrast (and similar to last week), gold remains moderately above its early 2020 highs, while silver is significantly above its early 2020 highs. The misaligned performance – with silver outperforming and gold miners underperforming – puts a bow on this bearish package.

The bottom line?

It is not only the case that silver was strong and miners were weak in the last several days – it’s been the case over the past several months as well. The implications are bearish.

Also troubling is that the stock market that’s soaring in the medium term, hasn’t shined its light upon the PM market. Contrasting the mantra that ‘a rising tide lifts all boats,’ equity market strength hasn’t triggered a sustainable rally in silver or the gold miners. And this “should have” been the case – both are more connected to stocks than gold is. Gold stocks because they are, well, stocks. Silver, due to multiple industrial uses.

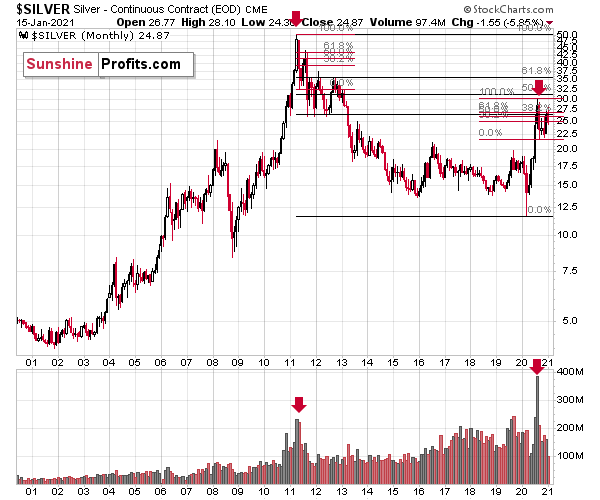

Additionally, the implications coming from silver’s long-term chart are also bearish for the next several weeks (perhaps even months) due to the size of the volume that accompanied the recent monthly rally.

Figure 31 - COMEX Silver Futures

If you look at the monthly silver volume levels, it seems likely that the next sizable downswing has already begun. The previous substantial monthly volume in silver accompanied the 2011 top. The analogy doesn’t get more bearish than this. Ok, it would, if there were multiple key tops confirmed by huge monthly volume. But the 2011 top was so significant that other tops are not comparable, except for the most recent one. Thus, the implications are bearish.

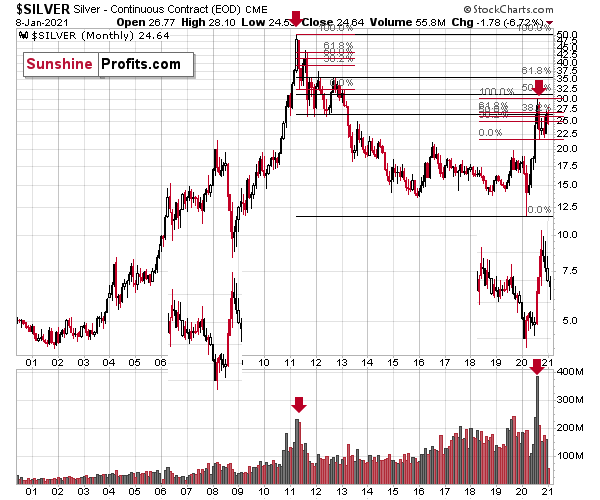

Moreover, please keep in mind that while gold moved to new highs, silver – despite its powerful short-term upswing – didn’t manage to correct more than half of its 2011 – 2020 decline.

In fact, silver has already invalidated its move above the lowest of the classic Fibonacci retracement levels (38.2%), which is not something that characterizes extraordinarily strong markets.

Just like in 2011, silver initially spiked on high volume, before rolling over and making a vertical move lower. Then it corrected slightly more than 61.8% of the preceding decline and then it truly plunged – much more than it had declined initially. We already saw the initial slide and the corrective upswing slightly above the 61.8% retracement. If the history is to rhyme (and this appears likely) then we can expect to see a sizable slide in the white metal in the next several weeks to months.

Based on the above chart, it seems that silver is likely to move well above its 2011 highs, but it’s unlikely to do it without another sizable downswing first.

In addition, silver is showing an interesting pattern when analyzing its inverse price action. Nearly identical to the inverted formation that emerged from 2006 to 2009, today’s chart looks eerily similar to its predecessor.

Please see below:

Figure 32 - COMEX Silver Futures

While it’s more of a wild card, the above pattern shows that silver’s 2020 top plots nearly identical to the inverse of the 2006-2009 performance. I copied the 2006 – 2009 performance right below the regular price movement and I inverted it, and I also copied this inverted pattern to the last few years.

The similarity is quite significant. And whenever a given pattern has been repeated, the odds are that it could also repeat in the not-too-distant future. Of course, there is no guarantee for that, but once the same market has reacted in a certain way to a specific greed/fear combination, it can just as well do it again. And these similarity-based techniques work quite often. So, while it’s not strong enough to be viewed as a price-path-discovery technique on its own, it should make one consider some scenarios more closely. In particular, this means that the declines in the prices of silver, gold, and mining stocks could be bigger and take longer than it seems based on other charts and techniques.

The only thing that comes to my mind, which could – realistically – trigger such a prolonged decline would be a major drop in the general stock market. Given what I wrote above, the latter is quite possible, so I’ll be on the lookout for confirmations and invalidations of this scenario.

If history rhymes, silver could be in for a profound decline over the next few months (beyond my initial target). Moreover, the development would increase the duration of a precious metals’ bear market (also beyond my initial forecast).

After all, gold did invalidate its long-term breakout above the 2011 highs and the way gold reacted to a small upswing in the USD Index was truly profound…

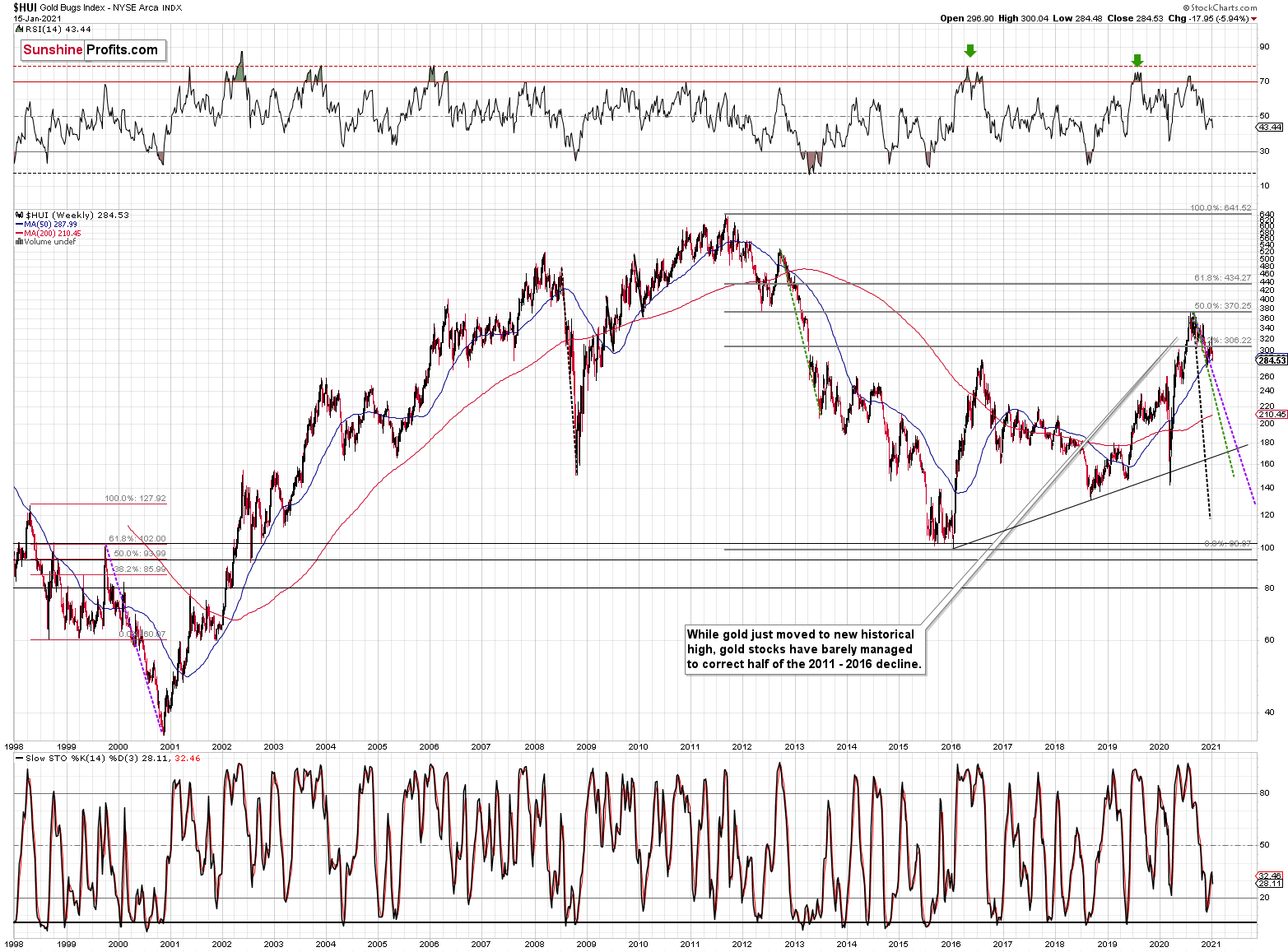

We are witnessing something similar in the HUI Index as well. The latter corrected half of its 2011 – 2016 decline and nothing more, while gold moved well above its 2011 high.

Figure 33 - NYSE Arca Gold BUGS Index (HUI) and Slow Stochastic Oscillator Chart Comparison

Showing historical precedent, the HUI Index is declining at a pace that’s similar to 1999-2000 and 2012-2013 (particularly bearish periods). And while it’s unclear which historical analogue the HUI Index will adopt, it’s still set up for a significant move lower (we’ll know a lot more about the shape of the decline once gold and the GDX ETF tip their hands).

The key takeaway?

The recent price action – even the short-term rallies - remain extremely bearish. Furthermore, the HUI Index is likely to revive its checkered past over the next few weeks and months.

And how will we spot a buying opportunity?

We view the price target levels as guidelines and the same goes for the Gold Miners Bullish Percent Index (below 10), but the final confirmation will likely be something else. Something that we already saw in March when gold bottomed.

We will be on a special lookout for gold’s strength against the ongoing USDX rally. At many vital bottoms in gold, that’s exactly what happened, including the March bottom.

Moving on to cross-asset correlations, gold and the USDX have been strongly negative over the medium-term (past year). And despite trading in similar directions for much of November, gold, silver and the HUI Index (relative to the USD) are now back to their usual divergences (30-trading-day correlations of – 0.79, – 0.92 and – 0.70).

Figure 34

Since gold, silver, and mining stocks have been strongly negatively correlated with the USD Index in the medium term, it seems likely that they will be negatively affected by the upcoming sizable USDX upswing.

…Until we see the day where gold reverses or soars despite the U.S. currency’s rally.

If that happens with gold at about $1,700, we’ll have a very good chance that this was the final bottom. If it doesn’t happen at that time, or gold continues to slide despite USD’s pause or decline, we’ll know that gold has further to fall.

Naturally we’ll keep you – our subscribers – informed.

To move forward, how does the GDX downside target compare to gold’s downside target? If, at the same time, gold moves to about $1,700 and miners are already after a ridiculously big drop (to $31-$32 in the GDX ETF, or lower), the binding profit-take exit price of your GDX ETF will become $32.02 (those with higher risk tolerance might lower it to $31.15 or so, but moving it lower seems just too risky).

At this time, the final GDX target (the one that would correspond to gold at $1,500 or so) is still unclear. The $17 - $23 area seems probable, especially if the general stock market slides once again. It’s too early to say with any significant level of certainty. Gold is providing us with a clearer final target, so that’s what we’ll focus on. And most importantly – we’ll focus on gold’s performance relative to the USD Index.

Letters to the Editor

Q: Please comment on the new ETNs, GDXD and GDXU, as suitable trading vehicles.

A: The suitability is an individual matter, so I won’t be able to tell if it’s suitable for *you*, but I can tell if they seem like a useful proxy for mining stock trades in general, and I’ll provide some extra comments as well.

In 2020, the popular highly-leveraged (3x) mining stock ETNs: NUGT, DUST, JNUG, and JDST had their leverage decreased from 3x to 2x. This was probably caused by outraged traders who lost their capital even though they were right in case of some market movements, and it was all likely (at least mostly) due to the fact that these ETNs don’t provide the said leverage over the course of the entire price move that one wants to bet on, but they do on a day-to-day basis – literally. This has some very important, but often overlooked consequences.

One of them is that if the underlying asset gets very volatile, the above-mentioned mechanism will “eat” quite visible amount of capital. Why?

Because losing 1% and then gaining 1% results in a person getting practically even (almost), but at the same time:

Losing 10% and then gaining 10% gets one 0.9 x 1.1 – 1 = 0.99 – 1 = minus 1% (loss of 1%)

Losing 50% and then gaining 50% gets one only 0.5 x 1.5 – 1 = 0.75 – 1 = minus 25% result (so a loss of 25%)

Losing 90% and then gaining 90% gets one only 0.1 x 1.9 – 1 = 0.19 – 1 = minus 81% result (so a loss of 81%).

A loss of 81% means that one’s capital is almost gone.

As you can see, the bigger the price moves, the stronger the effect becomes. Moreover, the bigger the leverage in case of an ETN, the stronger the effect as well.

As things got very volatile in 2020, the daily price moves in the underlying assets were wide, and thus over time, through the volatile day-to-day price moves, the value of traders’ portfolios declined. Consequently, the decision was made to limit the leverage – this would also limit the extent of the above-described effect.

However, as time passed, the volatility seems to have declined. Trader’s appetite for risk increased once again and the memory of the unpleasant price swings faded away. Consequently, the market was ready for the increase of the leverage once again. The leverage was not increased in the NUGT, DUST, JNUG, and JDST ETNs, which created an opportunity for someone else to provide the 3x leveraged ETN – and that’s exactly what happened.

There are GDXU (3x leveraged) and GDXD (inverse 3x leveraged) ETNs based on the mining stock ETFs: GDX and GDXJ.

The liquidity for these ETNs is not yet significant, but I expect that it will pick up in the following months. If not immediately, then eventually. Why? Because individual investors tend to get overleveraged and the 3x leveraged ETNs is an easy way to do so. The above is particularly dangerous when it’s combined with position sizes that are too big. Don’t get me wrong – leverage can be useful, when applied carefully, but it’s not for everyone, and the 3x leverage might not be appropriate for most traders.

Figure 35

On the above chart, you can see the phenomenon that I explained previously today. While both the GDX and the GDXJ (middle of the chart) are slightly above their mid-December lows, the GDXU is visibly below the analogous level.

For comparison, the NUGT ETN is also slightly above its mid-Dec. low.

Does the GDXU provide the bigger bang for the buck? Yes. But does it come at an extra price that might be too high for most people? Once again, yes. Will I use these instruments myself? I’m not using them right now, but I might consider using them on a temporary basis.

So, while the GDXU and GDXD might be useful for very short-term trades, I don’t recommend using these vehicles for most traders. The 2x leverage is usually enough or even more than enough for most people. In fact, no leverage is very often the best choice.

Consequently, I will not be providing the exit / stop-loss details for the GDXU and GDXD ETNs – these vehicles are not appropriate for beginning investors, and pros will have no trouble with coming up with these price levels based on my price levels for the unleveraged GDX / GDXJ targets.

By the way, it’s usually the case that when I’m discussing percentages and ETNs, I then receive a question about how can an inverse ETN make more than 100% gains if the underlying asset can’t lose more than 100% of value – so, I’ll comment on that right away. Once again, it’s a matter of focusing on the right period. The underlying asset can’t lose more than 100% of its starting value but it can lose 1% for even 300 days in a row and still have positive value. On the second day it doesn’t decline 1% of the starting value, but 1% of the value that it had on the second day. And so on.

Overview of the Upcoming Decline

- As far as the current overview of the upcoming decline is concerned, I think it has already begun.

- During the final part of the slide (which could end within the next 1-12 weeks or so), I expect silver to decline more than miners. That would align with how the markets initially reacted to the COVID-19 threat.

- The impact of all the new rounds of money printing in the U.S. and Europe on the precious metals prices is incredibly positive in the long run, which does not make the short-term decline improbable. Markets can and will get ahead of themselves and decline afterward – sometimes very profoundly – before continuing with their upward climb.

- The plan is to exit the current short positions in miners after they decline far and fast, but at the same time, silver drops just “significantly” (we expect this to happen in 1 – 5 weeks ). In other words, the decline in silver should be severe, but the decline in the miners should look “ridiculous”. That’s what we did in March when we bought practically right at the bottom . It is a soft, but simultaneously broad instruction, so additional confirmations are necessary.

- As a point of reference, given that the inverse pattern above mirrors today’s price action, the duration of the precious metals’ decline could last longer than my initial forecast. Keep in mind though, a prolonged bear market is not my base case; I’m merely indicating that the possibility exists.

- In absence, I expect a bottom to form with gold falling to roughly $1,700 - $1,750 . If – at the same time – gold moves to about $1,700 - $1,750 and miners are already after a ridiculously big drop (say, to $31 - $32 in the GDX ETF – or lower), we will probably exit the short positions in the miners and at the same time enter short positions in silver. However, it could also be the case that we’ll wait for a rebound before re-entering short position in silver – it’s too early to say at this time. It’s also possible that we’ll enter very quick long positions between those short positions.

- The precious metals market's final bottom is likely to take shape when gold shows significant strength relative to the USD Index . It could take the form of a gold’s rally or a bullish reversal, despite the ongoing USD Index rally.

Summary

Summing up, the outlook for gold and the rest of the precious metals market is bearish for at least the next few weeks. After topping at its triangle-vertex-based reversal, gold moved sharply lower and it just invalidated the breakout above its declining resistance line, while breaking below the rising support line. All this happened as the USD Index rallied visibly above its declining resistance lines and invalidated the breakdown below the 2020 lows. This creates a strongly bearish combination for the precious metals market.

The USD Index and cryptocurrencies suggest that we’re seeing the repeat of early 2018, when the USD Index bottomed. Given the current correlations between PMs and the USD Index, the rally in the USDX is likely to have very bearish implications for the precious metals market.

Despite a recent decline, it seems that the USD Index is going to move higher in the following months and weeks, in turn causing gold to decline. At some point gold is likely to stop responding to dollar’s bearish indications, and based on the above analysis, it seems that this is already taking place.

Naturally, everyone's trading is their responsibility. But in our opinion, if there ever was a time to either enter a short position in the miners or increase its size if it was not already sizable, it's now. We made money on the March decline, and on the March rebound, with another massive slide already underway.

After the sell-off (that takes gold to about $1,500), we expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money on the March decline and the subsequent rebound (its initial part) price moves (and we'll likely earn much more in the following weeks and months), but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in mining stocks is justified from the risk to reward point of view with the following binding exit profit-take price levels:

Senior mining stocks (price levels for the GDX ETF): binding profit-take exit price: $32.02; stop-loss: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the DUST ETF: $28.73; stop-loss for the DUST ETF: none (the volatility is too big to justify a SL order in case of this particular trade)

Junior mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $42.72; stop-loss: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the JDST ETF: $21.22; stop-loss for the JDST ETF: none (the volatility is too big to justify a SL order in case of this particular trade)

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway. In our view, silver has greater potential than gold does):

Silver futures downside profit-take exit price: unclear at this time - initially, it might be a good idea to exit, when gold moves to $1,703.

Gold futures downside profit-take exit price: $1,703

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief