Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

Gold miners ended yesterday’s session higher, even though gold didn’t – is this a bullish sign of strength?

Not really, at least not yet, and there are two good reasons for it.

I described the first in yesterday’s analysis, commenting on GDXJ’s 4-hour chart in the following way:

Now, if we zoom in even further, we’ll see that miners moved to their very short-term rising support line.

This means that it won’t be that odd if we see some kind of breather right now, before the decline continues.

Given that the Fed’s interest rate decision and the following press conference are scheduled for Wednesday, it would be rather normal to see the markets’ hesitation on Tuesday. There might be some immediate-term volatility, but the big moves might wait for the interest rate decision.

Whatever that decision is, when the dust settles, junior miners are likely to decline further.

Indeed, we saw the market’s hesitation – they bounced back.

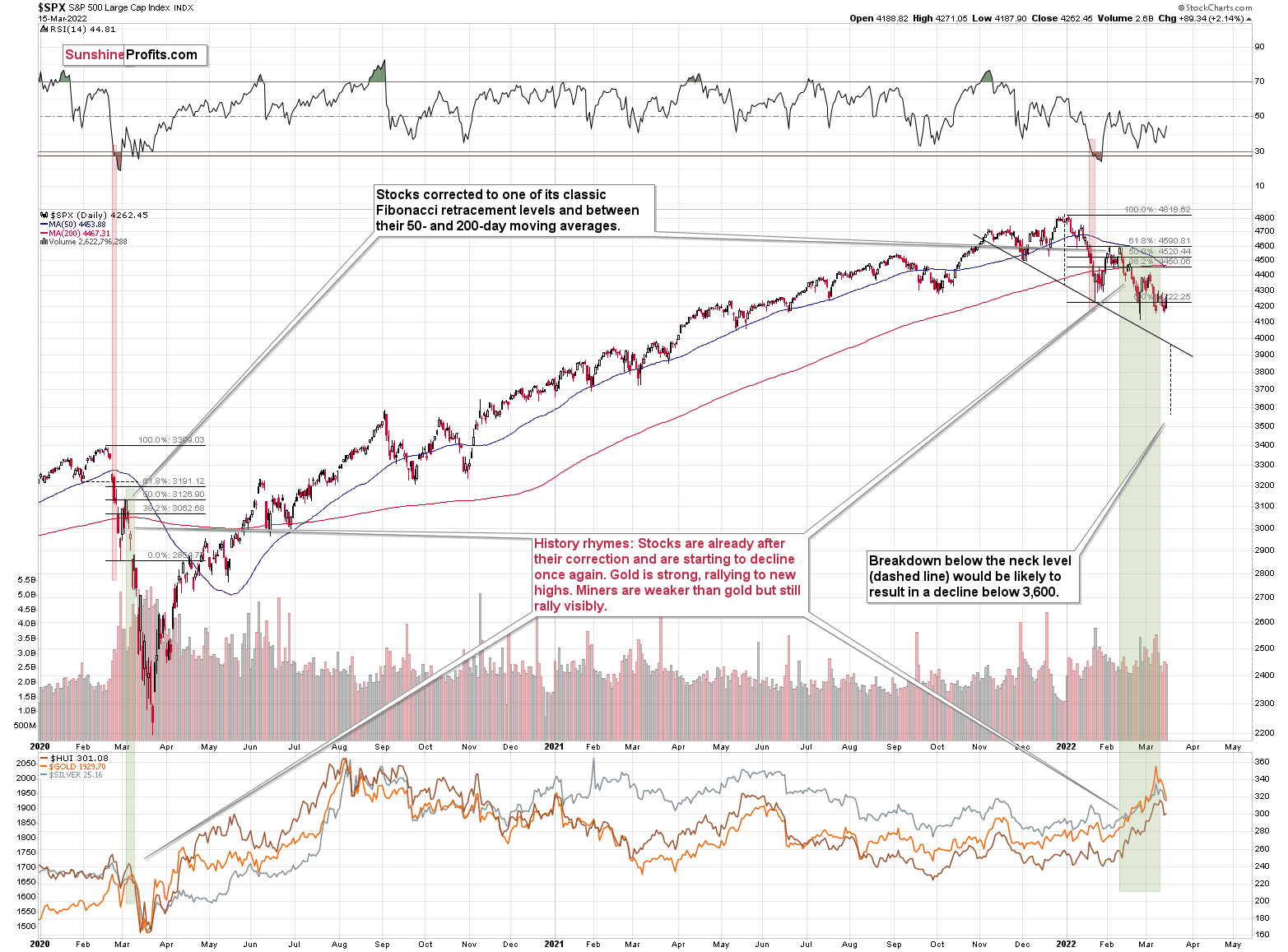

The second reason is what we saw in the general stock market: a daily rally.

This 2%+ daily rally didn’t change anything in the grander scheme of things, but it seems to have been enough to trigger a similar kind of reaction – a daily rally – in mining stocks.

As a reminder, every now and then, miners tend to take the lead of other stocks, focusing on the fact that they are “stocks” and kind of “forgetting” that their revenues ultimately depend on the price of the metal that they are producing or looking for.

This is not concerning because the general stock market is likely to slide after this brief pause, and because the bullish impact that stocks could have on miners could be just temporary, even if stocks don’t slide in the near term.

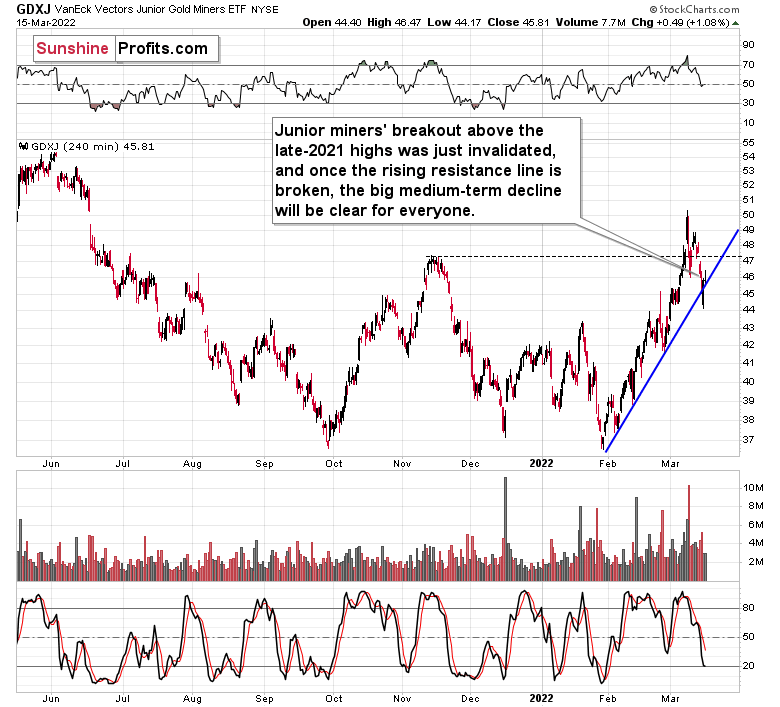

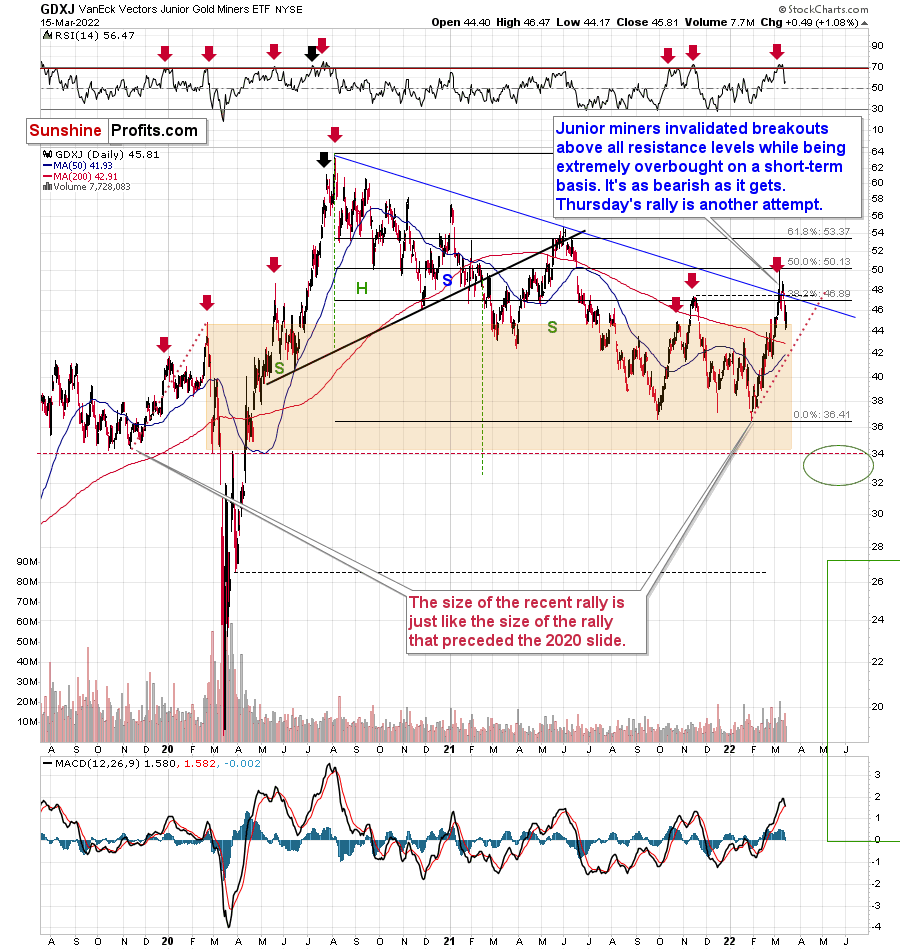

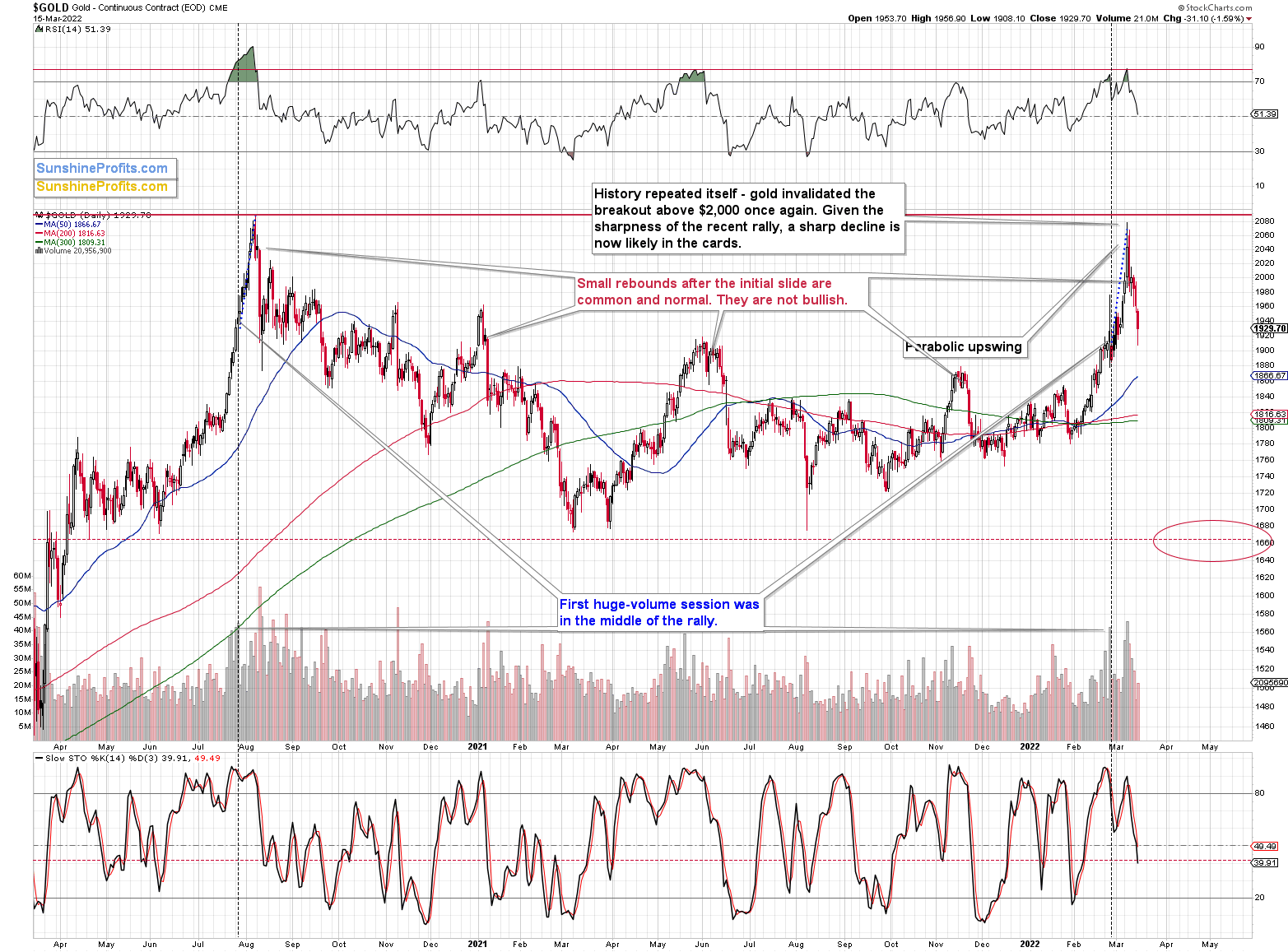

Besides, despite yesterday’s ~1% rally, the GDXJ ETF is still below its late-2021 highs, which means that the breakout above them was invalidated.

This means that my yesterday’s description of the above chart remains up-to-date:

In the case of junior miners, we also saw a decisive move – and a daily close – below the declining medium-term resistance line.

It’s also the invalidation of a move above the 38.2% Fibonacci retracement based on the 2020-2022 decline.

Yes, all those invalidations are bearish. This is particularly the case, since the RSI just moved below 70, which is one of the things that usually confirms that the final top for a given rally is already in.

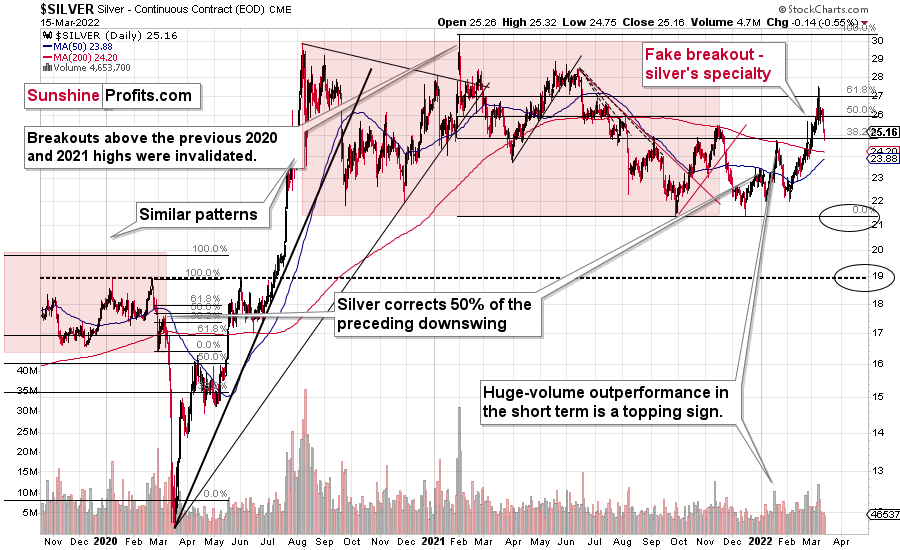

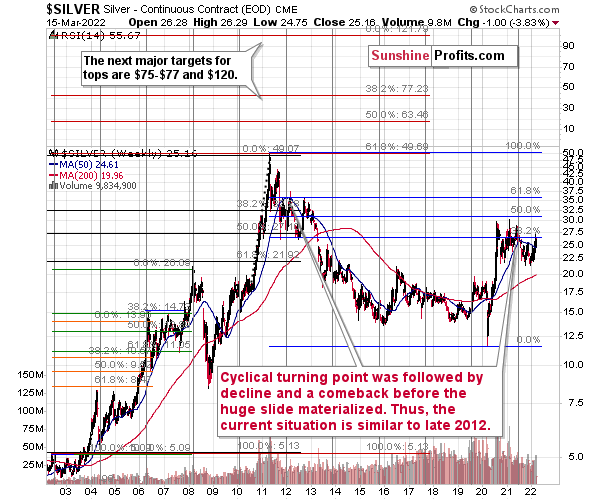

Silver didn’t move back above its late-2021 highs either.

In other words, the breakout above this level was invalidated. This is a strong bearish confirmation from the white metal.

The white metal just invalidated the move above its 61.8% and 50% Fibonacci retracements.

That’s bearish on its own, but let’s keep in mind that it happened right after silver outperformed gold.

Last Tuesday, the GDXJ ETF was up by less than 1%, gold was up by 2.37%, and silver was up by 4.57%. Silver’s outperformance and miners’ underperformance is what we tend to see right at the tops. That’s exactly what it was – a top. Silver declined profoundly, and the attempt to break above its 61.8% Fibonacci retracement level will soon be just a distant (in terms of price) memory.

On a medium-term basis, silver was simply weak relative to gold, but we saw short-term outperformance. In short, that was and continues to be bearish.

Silver reversed, but the volume on which that happened was relatively low, so it’s not a bullish sign – confirmation from the volume is important as it emphasizes that bullish overpowered bears. In the case of low volume, it’s not fair to say that this was the case, so the implications are not bullish.

Gold declined and closed the day below the intraday high that it reached when Russian forces were entering Ukraine.

The situation is worse than it was back then – on Feb. 24 – but it’s more well known what’s happening and the fear of the world regarding the way the events could unfold has declined.

This is normal and in tune with what I described as the aftermath of the previous military invasions (U.S. invasion of Afghanistan, U.S. invasion of Iraq, Russia’s invasion of Crimea), and in tune with how gold reacts to geopolitical events in general. The short-term rally appears to be over, and now prices can get back to their previous patterns.

The previous patterns were that gold and gold stocks were repeating their 2011-2013 performance. Based on the recent price movement, it turned out that silver was also repeating its 2011-2013 performance, and the recent top seems to be analogous to the 2012 top in the above-mentioned markets.

I recently commented on silver’s self-similar pattern in the following way:

As far as silver’s big picture is concerned, please note that it also provides us with a confirmation of the analogy between 2012 and now.

At the turn of the year in 2011/2012, there was a cyclical turning point in silver, and we saw a sizable decline in silver shortly thereafter. The same happened in 2021, after silver’s cyclical turning point.

Back in 2012, silver declined more or less to its previous lows and then rallied back up, but it didn’t reach its previous top. It more or less rallied to its 50-week moving average and then by about the same amount before topping.

Recently, we saw exactly the same thing. After the initial decline, silver bottomed close to its previous lows, and most recently it rallied to its 50-week moving average and then by about the same amount before topping – below the previous high.

Thus, the situation is just like what it was during the 2012 top in all three key components of the precious metals sector: gold, silver, and mining stocks.

We have a situation in the general stock market that points to an even quicker slide than what we saw in 2012-2013. If stocks slide sharply and significantly just like in 2008, then the same fate may await the precious metals sector – just like in 2008. In this case, silver and mining stocks (in particular, junior mining stocks) would be likely to fall in a spectacular manner.

All the above was confirmed by silver’s invalidation of its breakout above the late-2021 high. Not only has the medium-term outlook been bearish, but now the short-term outlook for silver is bearish too.

All in all, technicals favor a decline in the precious metals sector either soon, or very soon, depending on today’s interest-rate decision and the following comments. It seems to me that we’ll see some sizable downswings soon.

Having said that, let’s take a look at other fundamental matters.

The Sentiment Unwind

While the PMs were the belle of the ball when the Russia-Ukraine conflict erupted, I warned that investors are often the most bearish at the bottom and the most bullish at the top. With the S&P Goldman Sachs Commodity Index (S&P GSCI) following in the footsteps of the ARK Innovation ETF, commodities' fervor has cooled materially in recent days.

For context, the S&P GSCI contains 24 commodities from all sectors: six energy products, five industrial metals, eight agricultural products, three livestock products, and two precious metals. However, energy accounts for roughly 54% of the index's movement.

More importantly, though, while the index declined by another 3.22% on Mar. 16 and helped diminish gold's sentiment, the S&P GSCI still remains materially disconnected from its 20-month moving average. Furthermore, the more than 150-point peak-to-trough decline has done little to reduce the overbought conditions showcased on its monthly RSI (~74).

As a result, there is plenty of room for further downside, and the PMs should suffer if the mean reversion continues.

Please see below:

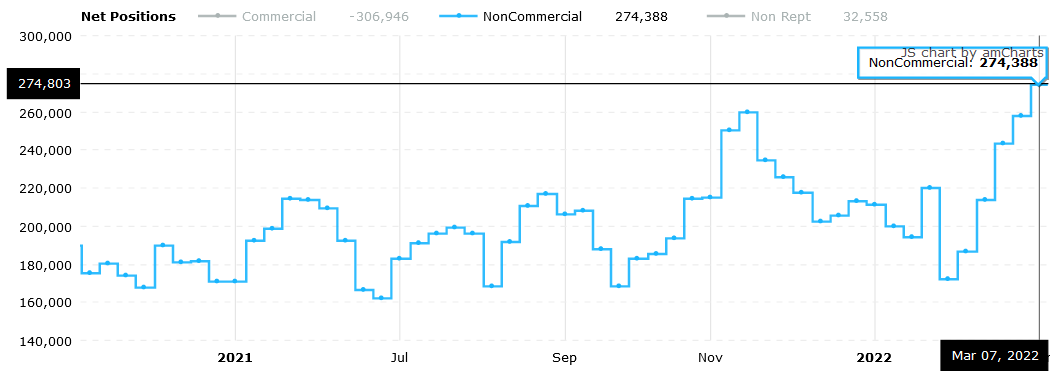

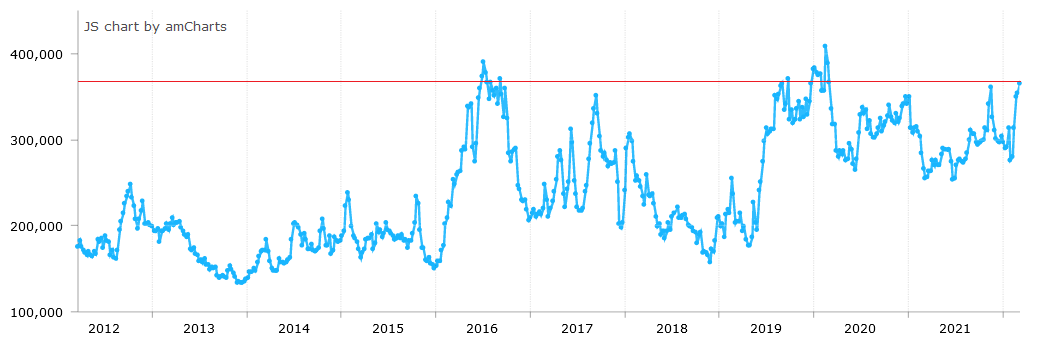

To that point, with investors known for their herd mentality, I noted on Mar. 15 that speculators’ love affair with gold was bearish, not bullish. I wrote:

It’s clear that human nature never changes. If you analyze the chart below, you can see that non-commercial (speculative) futures traders were all-in on gold at the end of last week (the latest data available).

Source: COT report

Source: COT report

Moreover, with speculative long positions increasing materially in recent weeks and the crowd often the most bullish at the top, it’s another contrarian indicator that supports lower gold prices over the medium term.

Please see below:

Source: COT report

Source: COT report

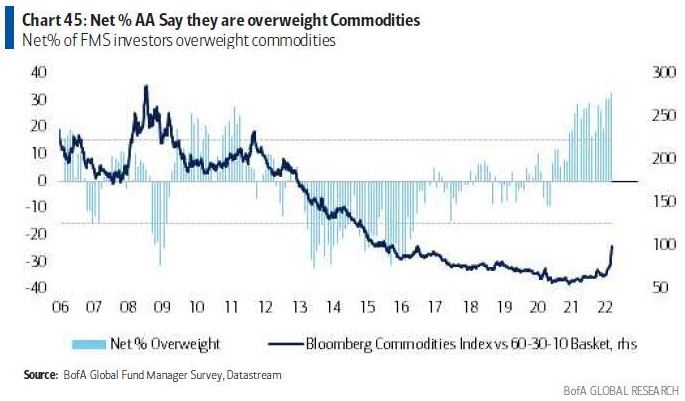

Likewise, with Bank of America releasing its latest Global Fund Managers Survey on Mar. 15, the net percentage of institutional investors overweight commodities is the highest in more than 16 years.

Please see below:

To explain, the dark blue line above tracks a variation of the Bloomberg Commodities Index, while the light blue bars above track the net percentage of respondents that are overweight on commodities. If you analyze the right side of the chart, you can see that allocations shot to new heights in the latest survey.

Moreover, with large dispersions often followed by large reversions, what’s popular today may not be so popular next week or next month. With price often a major driver of sentiment, the recent decline in the S&P GSCI could spark a positioning shift. If this occurs, the outcome is bearish for the PMs.

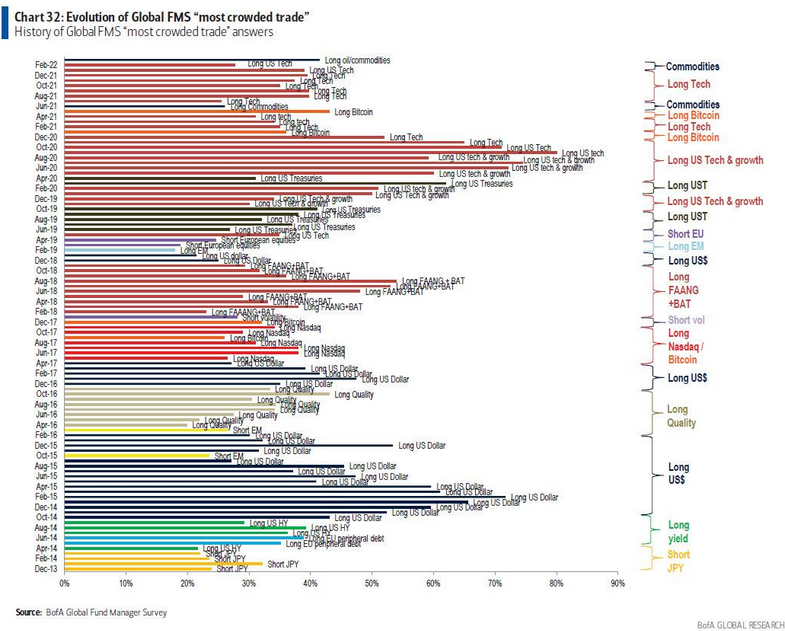

As further evidence, the Bank of America noted that long commodities are the most crowded trade on Wall Street.

Please see below:

To explain, the various horizontal bars above track the most popular positions of institutional investors each month. If you analyze the dark blue bar at the top, you can see that long commodities have gained immense popularity.

However, please note the length of the horizontal red bars from Jun 20 to Oct 20. Notice anything interesting? Well, with long tech captivating investors during that period, they chased ever-higher prices. However, if you analyze the second bar from the top, you can see that long tech positioning is roughly half of what it was then. As a result, it indicates how quickly sentiment can shift.

For context, I wrote about the similarities between commodities and high-growth tech on Mar. 8:

The unabated optimism rivals what we saw with SPACs, IPOs, and the ARK Innovation ETF in 2020. Yet, this time is different, and $2,500 gold is on the horizon?

Please see below:

When its RSI mirrored the behavior and the ARK Innovation ETF outperformed its 20-month MA by more than 115% in 2020, an epic collapse eventually unfolded. As of the Mar. 7 close, the ETF had suffered a 64% peak-to-trough decline.

To that point, with sentiment as a powerful force, investors’ emotions often cloud their judgment. When this occurs, fundamentals are powerless to stop the momentum. As a result, that’s why financial markets often overshoot on the upside and the downside.

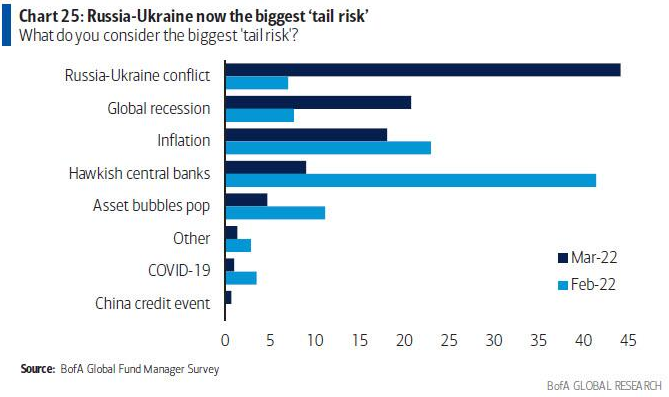

Moreover, with institutional investors’ heightened anxiety about the Russia-Ukraine conflict and the potential for a global recession impacting their decision-making, gold provides them comfort as a natural safe haven.

For example, if you analyze the chart below, you can see that fear over both developments rose to the top spots in March. However, with “hawkish central banks” going from big deal to no deal in a span of the month, it signals how quickly sentiment can shift.

Please see below:

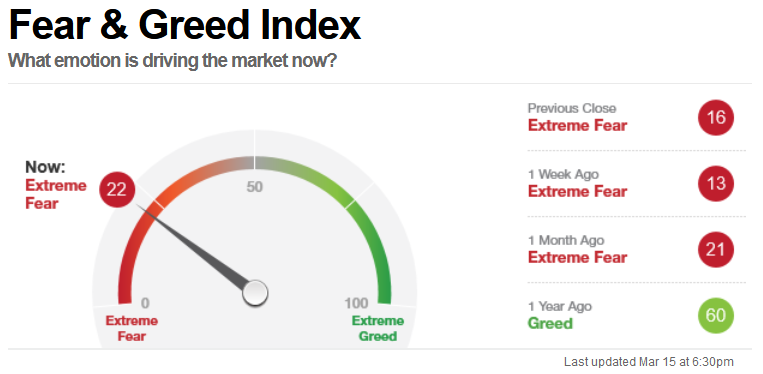

Furthermore, with fear helping to underwrite the PMs’ recent ascent, the S&P 500’s relief rally on Mar. 15 did little to quell investors’ trepidation. As evidence, CNN’s Fear & Greed Index is still firmly in the red.

Please see below:

Source: CNN

Source: CNN

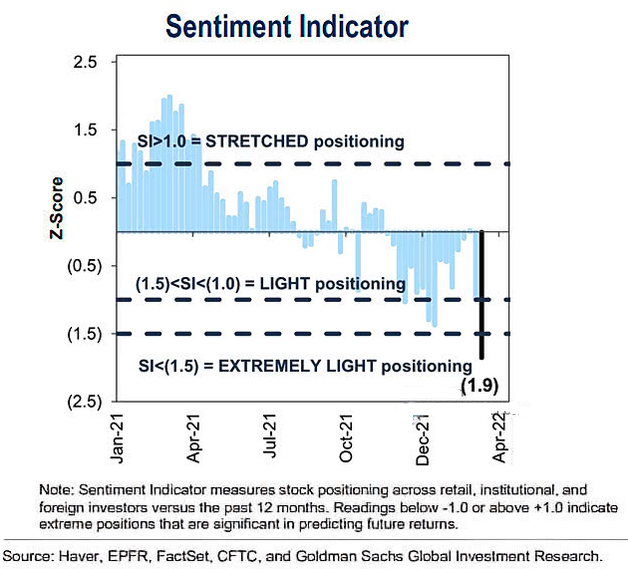

On top of that, Goldman Sachs’ sentiment indicator hit 1.9 standard deviations below the average on Mar. 14.

Please see below:

To explain, Goldman Sachs considers z-scores of -1 or +1 to indicate “extreme” positioning. If you analyze the right side of the chart, you can see that the latest reading (the dark blue bar) is sharply negative. As a result, with skittish investors often flocking to gold during periods of uncertainty, a normalization of sentiment will likely hurt the PMs.

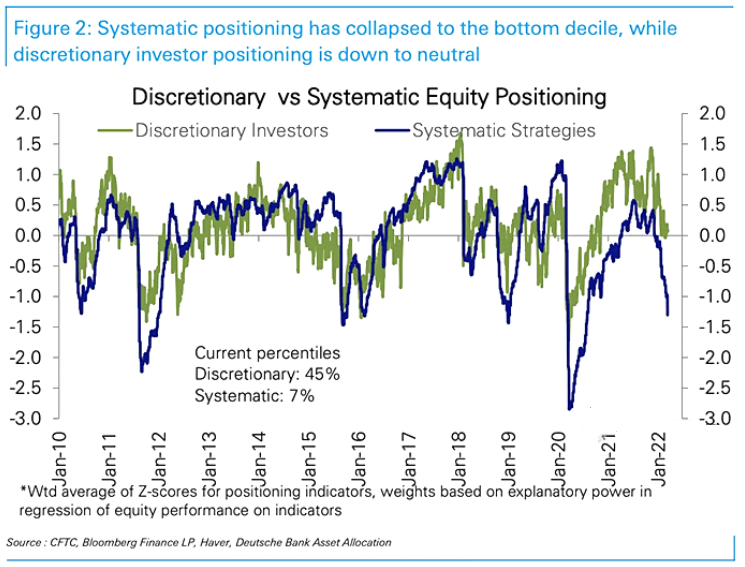

Expanding on that point, data from Deutsche Bank shows that systematic equity positioning is in the 7th percentile. For context, this metric tracks the positioning of algorithmic and quantitative investors. Moreover, if they’re not buying stocks or bonds, the PMs are strong candidates to fill the void.

Please see below:

To explain, the green and blue lines above track discretionary and systematic investors’ equity positioning. If you analyze the right side of the chart, you can see that the latter has declined significantly. Moreover, with a reading in the 7th percentile implying that 93% of the time, systematic investors have more equity exposure, the void opened the door for more commodities investments. As a result, the PMs benefited from ‘the most crowded trade on Wall Street.’

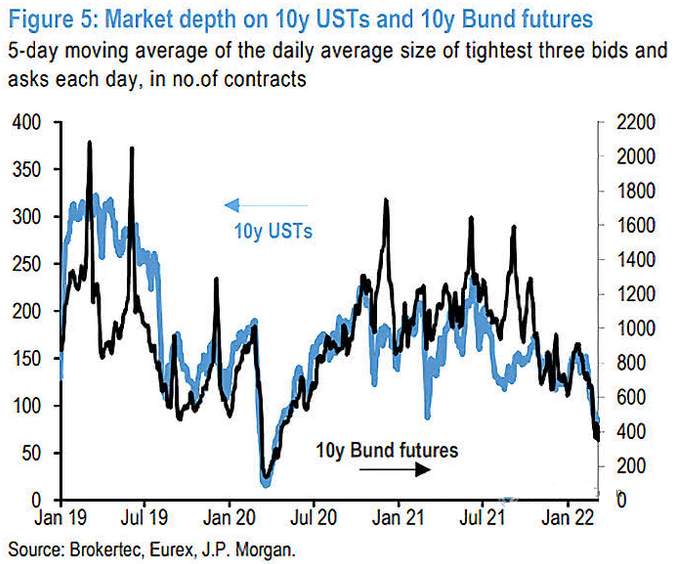

Finally, the U.S. 10-Year Treasury yield rallied again on Mar. 15 and closed at another 2022 high of 2.15%. Moreover, with liquidity in the futures market continuing to deteriorate, more yield spikes could be on the horizon.

Please see below:

To explain, the black and blue lines above track the market depth for 10-Year Treasury and Bund (German bonds) futures. If you analyze the right side of the chart, you can see that the five-day moving average of the tightest bid-ask settlements continues to decline. As a result, a shallow market has resulted in more contracts being settled with wider bid-ask spreads.

In turn, this creates liquidity risk, as buyers may not be there when large sellers want to unwind 10-Year Treasury futures positions. Due to that, yields often spike when sellers outweigh buyers. As such, the more the blue line declines, the more it increases the chance of a taper-tantrum-like event.

The bottom line? While the Russia-Ukraine conflict allowed the PMs to ignore bearish domestic fundamentals, sentiment is starting to shift, and while the PMs retreat from their 2022 highs, the USD Index has barely budged. As a result, while the Russia-Ukraine drama helped elicit a bid for the greenback, its strong fundamentals are in place despite the conflict. Moreover, with U.S. Treasury yields seeking higher ground alongside the USD Index, it’s an extremely bearish sign for the PMs.

In conclusion, the PMs were mixed on Mar. 15, as mining stocks sidestepped the negativity. However, with their fundamental outlooks worsening and the Fed poised to raise interest rates today, larger drawdowns should occur over the next few months. Moreover, if Russia and Ukraine reach a resolution, the sentiment unwind could occur at a rapid pace.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is now over or very close to being over , and that gold, silver, and mining stocks are now likely to continue their medium-term decline.

- It seems that the first (bigger) stop for gold will be close to its previous 2021 lows, slightly below $1,700. Then it will likely correct a bit, but it’s unclear if I want to exit or reverse the current short position based on that – it depends on the number and the nature of the bullish indications that we get at that time.

- After the above-mentioned correction, we’re likely to see a powerful slide, perhaps close to the 2020 low ($1,450 - $1,500).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place, and if we get this kind of opportunity at all – perhaps with gold close to $1,600.

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold close to $1,350 - $1,400. I expect silver to fall the hardest in the final part of the move. This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,375, but at the moment it’s too early to say with certainty.

- As a confirmation for the above, I will use the (upcoming or perhaps we have already seen it?) top in the general stock market as the starting point for the three-month countdown. The reason is that after the 1929 top, gold miners declined for about three months after the general stock market started to slide. We also saw some confirmations of this theory based on the analogy to 2008. All in all, the precious metals sector is likely to bottom about three months after the general stock market tops.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding or clear enough for me to think that they should be used for purchasing options, warrants or similar instruments.

Summary

Summing up, despite the recent rally in gold, the outlook for junior mining stocks remains exactly as I described previously.

Crude oil’s extreme outperformance, the stock market’s weakness, and critical medium-term resistance levels reached by gold (all-time high!) and junior mining stocks, all indicate that the tops are at hand or have just formed. The huge-volume reversals in gold and (especially) mining stocks, along with silver’s short-term outperformance, all point to lower precious metals prices in the following days/weeks. It seems that the top is in.

Investing and trading are difficult. If it was easy, most people would be making money – and they’re not. Right now, it’s most difficult to ignore the urge to “run for cover” if you physically don’t have to. The markets move on “buy the rumor and sell the fact.” This repeats over and over again in many (all?) markets, and we have direct analogies to similar situations in gold itself. Junior miners are likely to decline the most, also based on the massive declines that are likely to take place (in fact, they have already started) in the stock markets.

From the medium-term point of view, the two key long-term factors remain the analogy to 2013 in gold and the broad head and shoulders pattern in the HUI Index. They both suggest much lower prices ahead.

It seems that our profits from short positions are going to become truly epic in the coming months.

After the sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

Most importantly, please stay healthy and safe. We made a lot of money last March and this March, and it seems that we’re about to make much more in the upcoming decline, but you have to be healthy to enjoy the results.

As always, we'll keep you - our subscribers - informed.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $34.63; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged) and GDXD (3x leveraged – which is not suggested for most traders/investors due to the significant leverage). The binding profit-take level for the JDST: $14.98; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade); binding profit-take level for the GDXD: $25.48; stop-loss for the GDXD: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $19.12

SLV profit-take exit price: $17.72

ZSL profit-take exit price: $38.28

Gold futures downside profit-take exit price: $1,683

HGD.TO – alternative (Canadian) inverse 2x leveraged gold stocks ETF – the upside profit-take exit price: $11.79

HZD.TO – alternative (Canadian) inverse 2x leveraged silver ETF – the upside profit-take exit price: $29.48

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (like it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief