Briefly: outlook for the stock market is sideways-to-bearish in the short-term, and then sideways-to-bullish for the following weeks and especially months.

Welcome to this week's Stock Investment Update.

Friday's session added a new wrinkle to the bulls, and especially its close is a fly in the ointment for Thursday's encouraging signs. I anticipated the sideways-to-down period to arrive in July - but aren't we at its doorstep already? The narratives haven't changed one bit - there are the corona second wave fears coupled with the Fed's cautious tone against the data pointing that the recovery is on and new stimulus is underway.

The bulls' interpretations have been winning earlier in the week before the bears took initiative. How serious is this crack in the dam, enough to derail the stock bull market? I don't think it will succeed in doing that, but rougher times for stock bulls might very well be knocking on the door already. In what I think will turn out to be summer doldrums in stocks, I stand by my call that we're going to see quite higher S&P 500 prices in December than is the case now.

S&P 500 in the Medium- and Short-Run

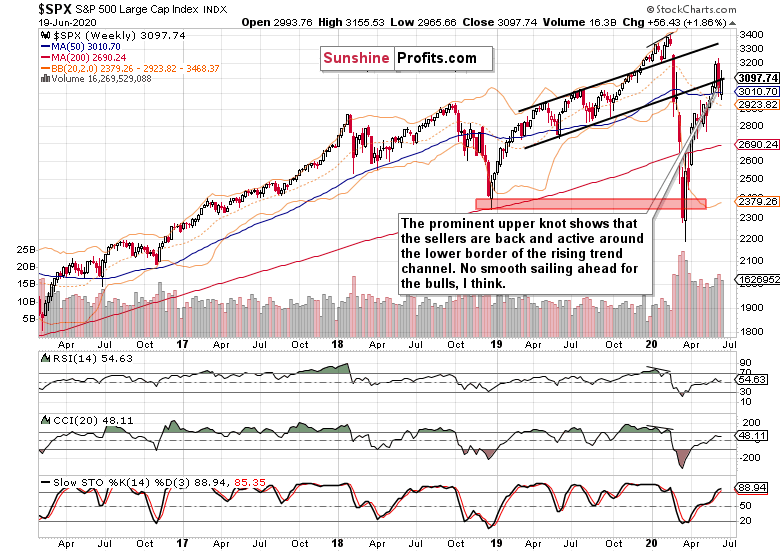

I'll start with the weekly chart perspective (charts courtesy of http://stockcharts.com ):

The weekly chart shows last week's battle precisely. After reversing prior week's selloff on Monday and Tuesday, stocks stalled on Wednesday and Thursday. Friday's session opened encouragingly, and it appeared the bulls will close the week decently. Yet despite two intraday rebounds, the sellers proved to be in the driving seat.

This week's candle got a bearish flavor as a result. The lower volume isn't as concerning as the upper shadow is. The extended weekly indicators are whispering caution here as well, regardless of being still fit to power one or a few weeks of more upside before consolidating.

Either way, the last three weeks have shown that volatility is rising again, giving us sizable swings both ways. The steep recovery of the March 23 lows that came with its own fits and starts in April and May, appears to be entering a similar period now, and as the days and weeks go by, it might very well turn out that the risks would get skewed rather to the downside than to the upside.

The week just over is a first one of its kind in another way too - not only the Fed's balance sheet increases have been moderating prior, but we just got a first week of balance sheet contraction since the corona crisis hit. This is a piece of the puzzle that no stock bull can ignore - it's less new money to help drive stocks (and whatever else is viewed as an anti-dollar play at that moment) higher, and helping the greenback recover.

On one hand, the Fed stands ready to support the real economy's recovery, on the other hand, the toying around with yield curve control doesn't do much good to financial stocks. We all know that the recovery will be a long and thorny event spanning not merely quarters, and I suspect it could easily be years in some aspects. By some, I mean e.g. airlines, cruise ship operators, leisure and hospitality, your usual suspects.

But these are anecdotal, because I view the corona hit as having a potential for creative destruction. The emphasis goes on creative and creativity. I mean that corona is an accelerator of trends, a trigger for an overdue clean-up - for example in retail. Also, many companies are getting used to operating long-term with remote workforce, which hits the commercial real estate.

Globalization and supply chains are being reassessed. Mergers and acquisitions are marching on, and the consolidations are moving us closer to oligopolistic structures, which means less competition and better margins for companies. What we see as an extended P/E ratio now, might not be as extended more than a few quarters down the road.

That's bringing me back to the Fed, and especially the source of upcoming stock market gains. While the central bank's engine is sputtering in the short run (remember those implied calls that the fiscal policy has to step up to the plate? What chances does Trump's $1T infrastructure bill stand vs. the Democrat's $3T wish list?) and election uncertainties will creep in increasingly more, it's the real economy's actual performance that will be driving further stock gains. Along with the earnings recovery (also note that so many stocks are trading below their book value currently), whose not only source I hinted at above.

It will be a bumpy ride. On one hand, latest non-farm payrolls coming in above expectations is an understatement, and strong retail sales or Philly Fed manufacturing with building permits support that. On the other hand, continuing claims are sticky - little wonder with their disincentive to work through overly generous benefits at times.

Meanwhile corona is surging in the Sun Belt states, raising fears of another series of lockdowns and disruptions to economic activity. Little wonder if you look at what's going on in Beijing. And the Red States would find it hard to reconcile with that after reopening - not that it were easier in Michigan. The virus is still here, and a reasonable coexistence must be achieved in the now - stocks seem to me more worried about the actual recovery, monetary and fiscal policy steps than another corona headache nationwide.

That's why I think that Friday's intraday reversal was more driven by the Fed's guarded tone, Apple store closures (indicative for the rest of the crowd) and simply less fresh money available.

But can the Fed be tightening here? After the hockey stick since March? I see it rather as a trial balloon - will anything start to disintegrate? It's not in their (and their mandate's) interest to try to do that too hard. When exactly did Powell say "We are not even thinking about raising rates"? Once this event of sticking it to freeloading Europe (EUR/USD rising, which is helping the eurozone sell its balance sheet expansion plans) while keeping the US as afloat as can be, is over, I fully expect the balance sheet to keep on expanding throughout this year - given the fundamental circumstances we're in, it can't really be any other way.

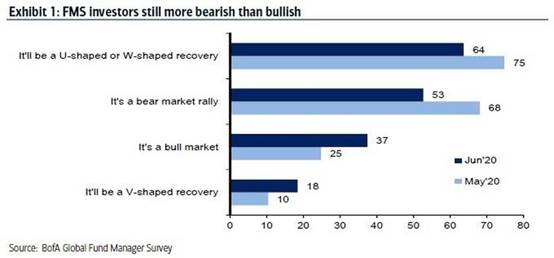

The new money taking place of the deflationary corona black hole, is bound to lift all boats, stocks including. Yet, it's not yet etched into the fund managers' consciousness. Take a look at the following graph (tough to make an attribution, so let's name them all: Bank of America, Zero Hedge and Wealth Research Group):

I've been in the minority since calling this S&P 500 a new bull markets so many weeks ago, and while I have reservations about a V-shaped recovery, it's nonetheless encouraging to see both hypotheses becoming ever more broadly accepted during the last 30 days.

These sentiment figures just show you that there's plenty of doubters and money on the sidelines to deploy. This doesn't take away from the short- and medium-term signs of deterioration I'll tell you about next, but illustrates that a lot of fire powder is still dry.

While stocks can take a hit, the sentiment is still too bearish to take us back into a bear market. Remember, bull markets end when there's no one left to buy - and I see quite a few potential buyers here.

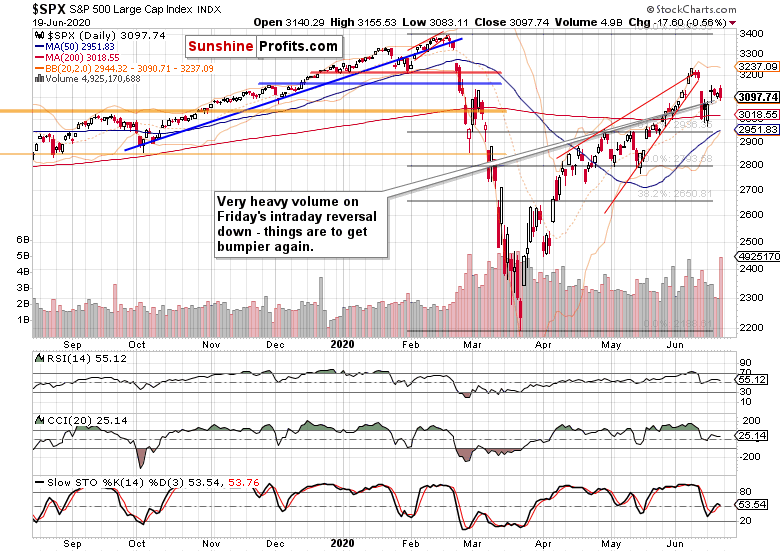

Does the daily chart really paint such a cautious tone that I am striking for the coming weeks?

It does, and not only because of the extraordinary Friday's volume. Going into the open with a solid bullish gap and extending gains, was what I had been looking for based on Thursday's action. But the selling pressure throughout the day was gradually picking up steam, and the above mentioned headlines (Powell, Clarida, Quarles and Apple) served as useful catalysts.

It's the market that decides to either ignore or place a certain weight on an event, story or soundbite. And the Fed didn't say anything really unknown and out of the blue, which is why the reaction (selling pressure) is making me worried. It might be that regardless of corona not disrupting the reopening on a large scale yet (that's why I earlier wrote that it's too early to sweat this one in mid-June), the sands are shifting a few weeks earlier than I thought they would. In other words, the market's sensitivities are on the move already.

Even the daily chart as such warrants caution here. Will follow through selling strike well before we wake up to the regular session on Monday? I don't rule out this possibility entirely but don't view it yet as highly probable. The daily indicators are in no-man's land.

If it comes that far, will the 61.8% Fibonacci retracement hold again, or can we carve out a local bottom way about this key support? Or is this just an isolated tremor in the protracted base building after Monday's Fed move?

I wrote on Friday that with a pinch of salt, we've seen two daily inside candles. And Friday's trading also remained within the confines of Tuesday's wild swings. Are we building a bullish flag (poking fun here, can any buyer come up with a more bullish look at things)?

Let's turn to the credit markets, because they take away quite some froth from the bullish explanations.

The Credit Markets' Point of View

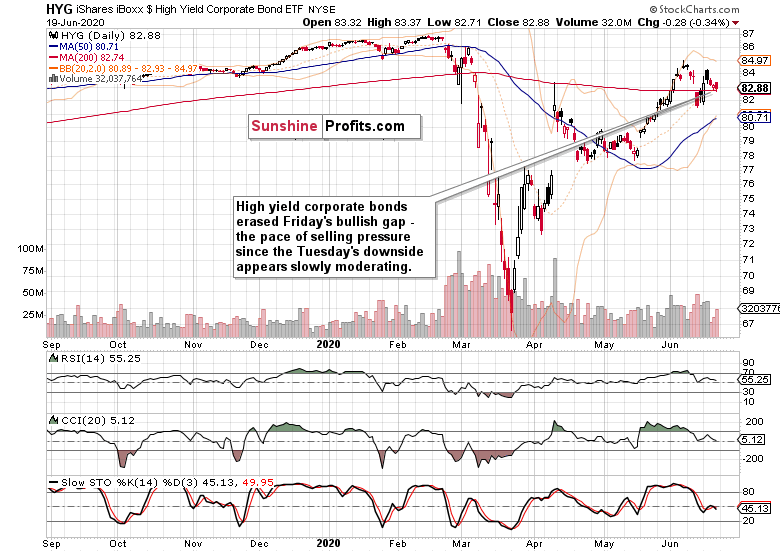

High yield corporate bonds (HYG ETF) came under pressure, and lost the opening bullish gap. Again, the positive signs from their Thursday's performance are short-term gone, and the bulls will have to reassert themselves after Friday's downside reversal.

Since their similar performance on Tuesday (another bullish gap coming under attack), the pace of decline has slightly moderated, but it's nothing the bulls could call home about - the best proof of an uptrend are rising prices, which we don't have currently (we have merely a solid potential for them).

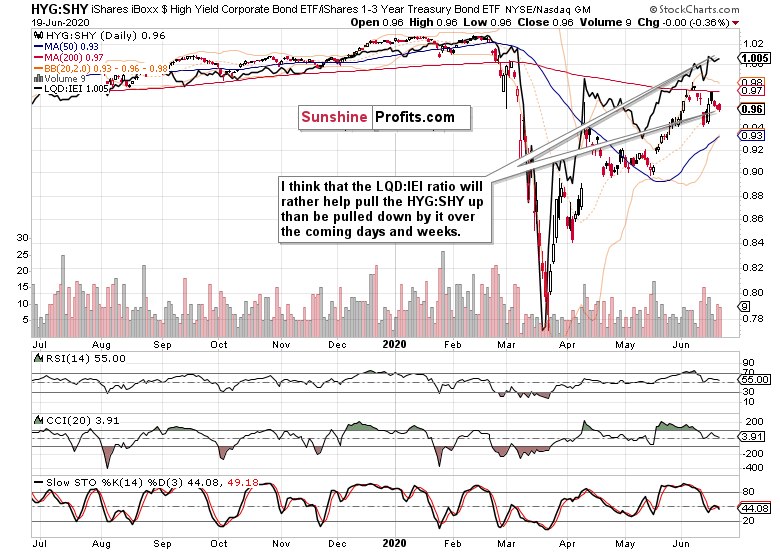

Investment grade corporate bonds to the longer-term Treasuries (LQD:IEI) ratio offers a positive hint. This is the less risk-on ratio than the high yield corporate bonds to short-term Treasuries (HYG:SHY), and it peeked higher on Friday in what could turn out to be a temporary weakness for its more risk-on counterpart.

It's important to note that none of these ratios is breaking down - only once they do that, the stocks can enter a period of true weakness. I made these fundamental outlook observations on Thursday, and they're still valid today:

(...) In short, the bond markets aren't questioning the recovery storyline, and are still more sensitive to the money spigots than hair-raising corona stories. I'm not arguing for a V-shaped recovery here, I just think that less bad is the new good as stocks are bought amid the prevailing real economy uncertainties (just when and how much will it rebound with some veracity?) and stimulus efforts as far as eye can see.

The money spigots are in a slowdown mode on a weekly basis, but I think that the Fed is just making a point that it's not the world's central bank ready to bail out everyone (right now). Will the markets try to test that, and will that show up in stock prices? To answer, I'll just say that it's been less than a week since the Fed has shown that it's willing and ready to support the U.S. economy. And just this Friday, Fed Vice Chair Clarida said that the central bank can and will do more to support the U.S. economy.

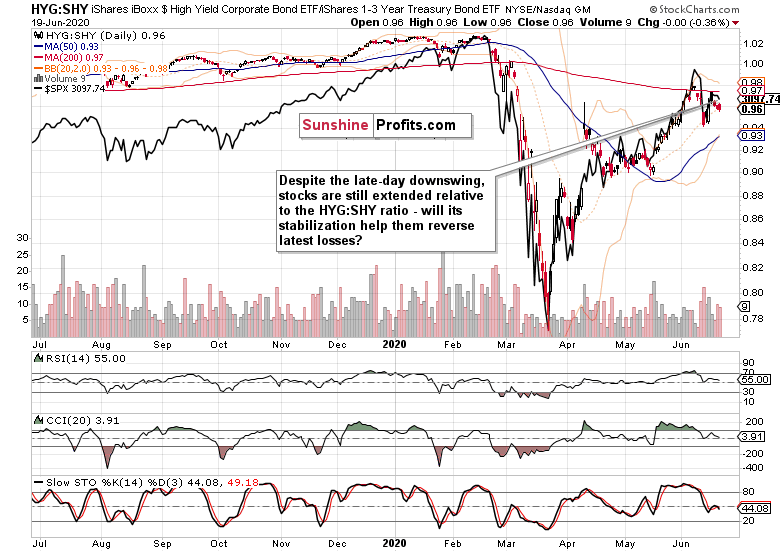

The HYG:SHY ratio with overlaid S&P 500 prices shows that the current price action and closeness of mutual relationship of these two metrics, isn't out of the ordinary. Right now, stocks are no longer trading that extended relative to the HYG:SHY ratio.

What we're seeing currently, could very well turn out to be a consolidation on par with the April-May one. My Thursday's observations still ring true today (we're not in a period where the markets decided to take on the Fed):

(...) Take a look instead at the sizable early April gap and the trading action that followed next. There were some downside moves, yet amid generally rising stocks. And what about the mid-May non-confirmation as the HYG ETF moved lower while stocks more than held ground? While we're not at such an advanced stage of Monday's Fed move digestion, it pays to remember that lesson already.

If one credit market ratio spells caution, it's this one - high yield corporate bonds against corporate bonds (PHB:$DJCB). As the junk corporate bonds aren't compared to Treasuries, but instead to the corporate bond universe, this metric reveals the willingness to take on more risk within corporate bonds - and the short-term picture isn't all that pretty.

It's true that in mid-May, stocks also traded elevated compared to the ratio testing its rising support line made by the April intraday lows. Right now, the ratio isn't that far off that line (reinforced by the mid-May test too) either.

The bearish takeaway from the ratio's daily indicators is more pronounced than in HYG:SHY, indicating more risk aversion within the corporate bond space. And that can have negative consequences for the stock bulls. I mean in the short run, because the ratio isn't breaking down and pulling stocks along right now.

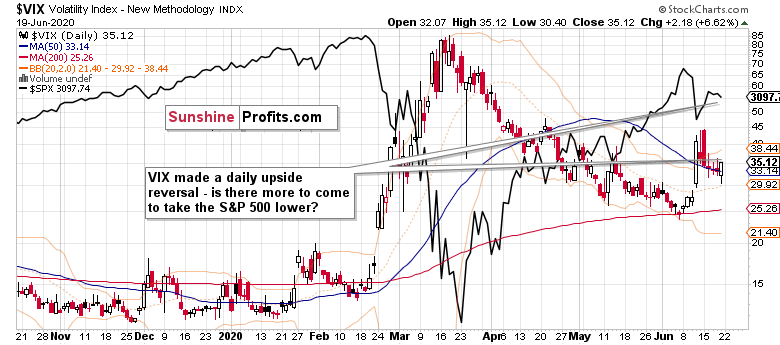

Rising volatility ($VIX) is another short-term sign of caution. Its consolidation with a downside bias just couldn't carry on anymore on Friday. Is it ready to march higher again relentlessly? Not necessarily, but it isn't likely to immediately budge down either. In short, we appear to be on the doorstep of the bumpier ride ahead for stocks.

Smallcaps are still lagging behind, and the picture isn't improving in the very short-term either. Barring an uptake in risk-on sentiment, I don't see them likely to catch up in the short run. This also goes to highlight the risks the S&P 500 faces right now.

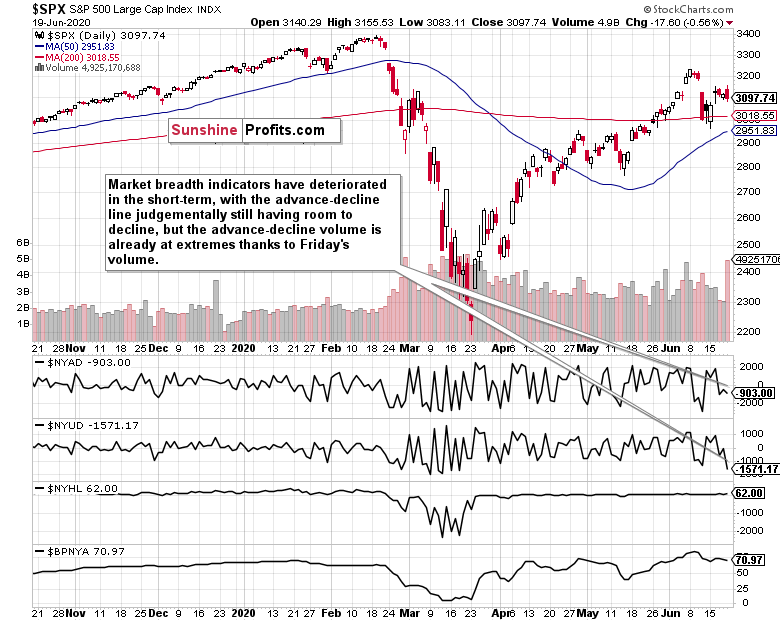

But the S&P 500 market breadth shows that we're quite far into the current weakness - the advance-decline volume is at its recent extremes already. But that's the result of Friday's extraordinary volume - the advance-decline line still has some room before it reaches its own extreme zone, meaning that we might very well be meeting lower stock prices before long.

From the Readers' Mailbag

Q: what is your opinion about gold and what do you think about Brent crude making impact on markets ?

A: I don't follow gold on a daily basis, but it's common knowledge that gold loves money printing. It has also been rather steadily rising since the Fed made its U-turn and went off its tightening plans many quarters ago. While the yellow metal hasn't risen as strongly during the repo crisis (autumn 2019), it had been consolidating similarly to spring 2019.

Corona brought us a deflationary episode in March, and gold went sharply down. If you compare that to the pre-Lehman times, it had been weakening since mid-July 2008. The Lehman collapse (mid-September 2008) helped put a short-term floor below it, and gold rallied. But what was the Fed-Treasury response back then, was it convincing enough for the markets to turn around? No, both gold and the S&P 500 went on to make new lows (the king of metals did so in October 2008 while stocks only in March 2009).

Fast forward to today - we're seeing the events play out much faster than back then. The quantitative easing announcement (let alone its volume) came much earlier this time (end of November 2008 was when QE1 was launched), and the market didn't really question the authorities since. Now, the Fed's balance sheet is over $7T, and the expansion has been the fastest ever.

Obviously, this is driving inflation expectations higher, but we are not yet seeing inflation on the ground meaningfully spiking. Yet, gold is reacting as if it were the case already. Right now, gold is not signaling another true deflationary event on the horizon or the Fed truly changing its rhetoric and behavior. But this doesn't mean it's safe from a short-term downside, especially if inflation keeps coming in weak. The yellow metal has a great future ahead and I expect higher prices in the quarters and years to come.

The oil part of your question ties in to gold as well, in what I think will turn out two great surprises for the markets later on. The first will be inflation rearing its head, and the other one would be higher oil prices. I say so despite the oil demand destruction that will take much patience to recover. Both of these factors will become very apparent well before the end of 2020 in my opinion, and stocks will like that.

Q: What's your prediction for Russell 2000 in 3 months? I read small businesses usually boom after a recession more than big ones.

A: You're asking about a time point that could very well mean the peak uncertainty about the election results. Take a look what happened in 2016 - smallcaps were not willing to rise much and were taking a dive since October 2016. Something similar could play out this time as well, but we're not seeing smallcaps outperforming in the runup from the panic lows. That's a watchout against being too bullish on the smallcaps right now.

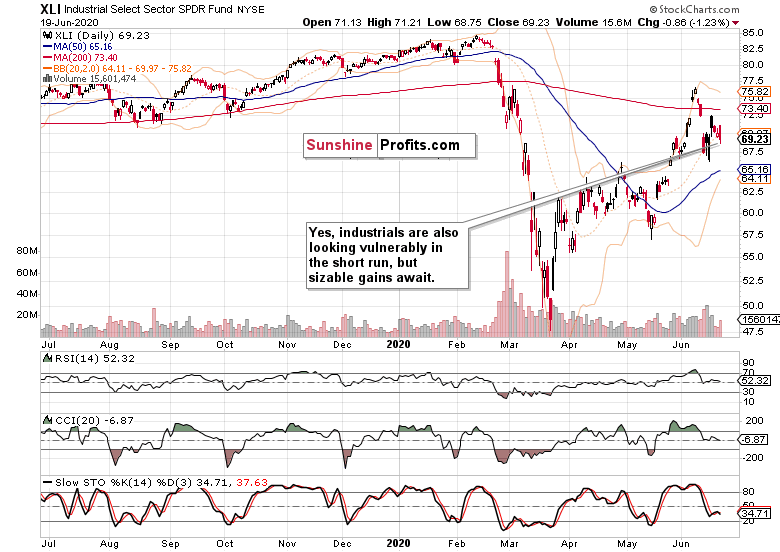

Q: I've recently bought industrials (XLI ETF) and want to profit on the stock upswing. How do you view the chances for the sector to appreciate?

A: I think industrials are a great choice within the bull markets' early recovery stage - they're leading the way higher, similarly to materials (XLB ETF).

Have we seen their top? I don't think so - there is ample room for appreciation as the recovery gets increasingly recognized as being on track. The incoming manufacturing data help to paint a bright picture too. If your investment horizon is long enough (end of 2020 as a minimum), you're set in for really nice gains in my opinion.

Q: I am curious about your thoughts on bank stress reports coming out on Thursday and the Fed not wanting banks to respond till after the markets close.

A: While this could in theory turn out a catalyst for a sizable stock move, I think it wouldn't be a great surprise to the markets - unless accompanied by a shift in the Fed's narrative, which I don't expect. Yes, they're taking the punch bowl away on a very short-term basis, but will it last long? I don't think so. Similarly, I think that the banks' comments won't push markets down in the aftermarket session. Of course, should I feel about that differently after Wednesday's closing prices, I'll highlight that.

Q: I'm interested in your short- and very short-term view on the AEX and DAX indices. Would appreciate your comment/analysis on this one.

A: I deal primarily with U.S. stock indices but a little international perspective certainly won't hurt as different national stock markets aren't moving totally independently of each other.

The S&P 500 has been more resilient that the DAX (or other eurozone indices) since the corona crisis hit, and I think the relative valuation is at an interesting point currently. I look rather at the U.S. to outperform than underperform next (we're at the 200-day moving average support here), and the U.S. outperformance will get into a true limelight once the election uncertainty is removed. Before that, it's a tough call, but I still slightly favor the U.S.

Fundamentally, much depends upon how the U.S. - China trade deal and globalization sentiment (supply chains reset) goes - should these tensions go into overdrive, export-dependent Germany with its stock market would suffer.

Summary

Summing up, the risk-on sentiment took it on the chin with Friday's reversal, and while no key supports were broken, the short-term outlook has deteriorated. The credit markets' performance is sturdier than is the case with stocks, and will set the tone for the S&P 500 amid the mixed short-term picture the index is sending. The summer doldrums for stocks that I anticipated in July, might be making an appearance already - time to buckle up, continuously assess whether stocks are or aren't getting ahead of themselves relatively speaking, and expect more risk-off environment in the weeks ahead.

Very short-term outlook for the stock market (our opinion on the next 2-3 weeks):

Sideways-to-bearish.

Short-term outlook for the stock market (our opinion on the next 2 months): Sideways-to-bearish.

Medium-term outlook for the stock market (our opinion on the period between 2 and 6 months from now): Sideways-to-bullish.

Long-term outlook for the stock market (our opinion on the period between 6 and 24 months from now): Bullish.

Very long-term outlook for the stock market (our opinion on the period starting 2 years from now): Bullish.

As a reminder, Stock Investment Updates are posted approximately once per week. I'm usually posting them on Monday, but I can't promise that it will be the case each week.

Please note that this service does not include daily or intraday follow-ups. If you'd like to receive them, I encourage you to subscribe to my Stock Trading Alerts today.

Thank you.

Monica Kingsley

Stock Trading Strategist

Sunshine Profits: Analysis. Care. Profits.