The markets closed the week at record highs and booked weekly gains for the fourth time in five weeks. This comes despite a disappointing U.S. jobs report.

News Recap

- The Dow Jones gained 248 points, or 0.83, the S&P 500 gained 0.9%, and the Nasdaq advanced 0.7%. All three indices posted both intraday and closing record highs. Meanwhile, the small-cap Russell 2000 also closed at a record high and once again led the markets with gains of 2.2%.

- The November jobs report grossly disappointed and came well short of estimates. The report stated that the U.S. added 245,000 jobs compared to the consensus estimate of 440,000.

- November’s unemployment rate matched expectations and fell to 6.7% from 6.9%.

- The US trade deficit widened to $63.1 billion in October from a revised $62.1 billion. Market expectations placed this number at $64.8 billion.

- New data was encouraging for US factory orders. New orders for US manufactured goods beat expectations and jumped 1% from a month earlier. This marks the 6th consecutive month of rising factory orders.

- As COVID-19 numbers continue to reach record highs in new infections, single-day deaths, and hospitalizations, a report from Thursday that Pfizer may have issues rolling its vaccine out was quite concerning. Judging by the markets’ performance on Friday, however, investors are not overly concerned.

- Stimulus talks continued for another day as Republicans and Democrats attempt to break a stalemate and pass a relief package before the end of the year.

- Chevron and Caterpillar each rose 3.9% and 4.3%, respectively, and led the Dow higher.

- Energy was the best-performing S&P 500 sector, gaining 5.4%.

- Friday’s jump led to the major indices booking their fourth weekly gain in five weeks. The Dow rose 1%, the S&P 500 gained 1.7%, and the Nasdaq rallied 2.2%. The Russell 2000 also gained over 2% this week.

In the short-term, there will be optimistic days where investors rotate into cyclicals and value stocks, and pessimistic days where there will be a broad sell-off or rotation into “stay-at-home” names. On other days like Friday, the markets will broadly rise without any one specific catalyst.

In the mid-term and long-term, there is certainly a light at the end of the tunnel. Once this pandemic is finally brought under control and vaccines are mass deployed, volatility will surely stabilize, and optimism and relief will permeate the markets. In fact, CNBC personality Jim Cramer said that beating COVID-19 would feel like “the end of prohibition.” Stocks especially dependent on a rapid recovery and reopening such as small-caps should thrive.

Markets will continue to wrestle with the negative reality on the ground and optimism for an economic rebound in 2021. While more positive vaccine news continues to trickle in day by day, there is still discouraging COVID-19 news, economic news, and geopolitical news to consider. Amidst the current fears of a double-dip recession with further COVID-19-related shutdowns and no stimulus, it is very possible that short-term downside persists. However, it’s encouraging that Democrats and Republicans are speaking again, and if a stimulus deal passes before the end of the year, it could mean more market gains.

Due to this tug of war between good news and bad, any subsequent move downwards will likely be modest in comparison to the gains since the bottom in March and since the start of November. It is truly hard to say with conviction that another crash or bear market will come. If anything, the constant wrestling match between sentiments will keep markets relatively sideways.

Therefore, to sum it up:

While there is long-term optimism, there is short-term pessimism. A short-term correction is very possible. But it is hard to say with conviction that a big correction will happen.

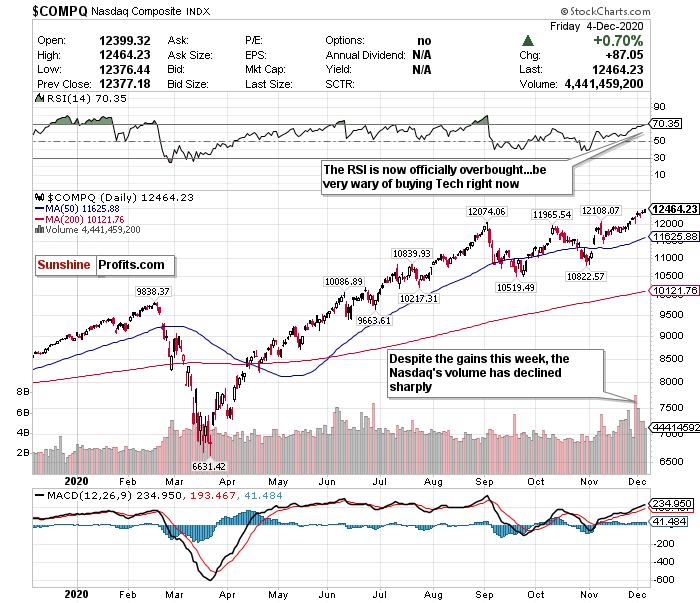

Tech Valuations Have Reached Concerning Levels...Buyer Beware

Despite initially lagging behind cyclicals and value stocks during the initial vaccine rallies of November, the NASDAQ has outperformed both the Dow and S&P for two consecutive weeks.

However, there are some serious concerns of overheating. Tech valuations have now reached astoundingly inflated levels. According to this chart, there are some things to be very concerned about as well.

Despite gaining 2.2% this week, the NASDAQ’s sharp decline in volume since the beginning of the week is fairly alarming. Additionally, the RSI has now officially exceeded the overbought level of 70. While an RSI of 70 doesn’t automatically mean a trend reversal, it is something to take note of.

On pessimistic days, having NASDAQ exposure is certainly a good thing because of all the “stay-at-home” stocks that trade on the index. However, positive vaccine news always induces the risk of downward pressure on tech names - both on and off the NASDAQ.

It is very hard to say with conviction to sell your tech shares. However, all of the signs are pointing to an eventual sell off and correction sooner rather than later. If anything, just tread lightly. For now, the NASDAQ gets a HOLD call. But if it keeps surging, it will simply not be sustainable.

For an ETF that attempts to directly correlate with the performance of the NASDAQ, the Invesco QQQ ETF (QQQ) is a good option.

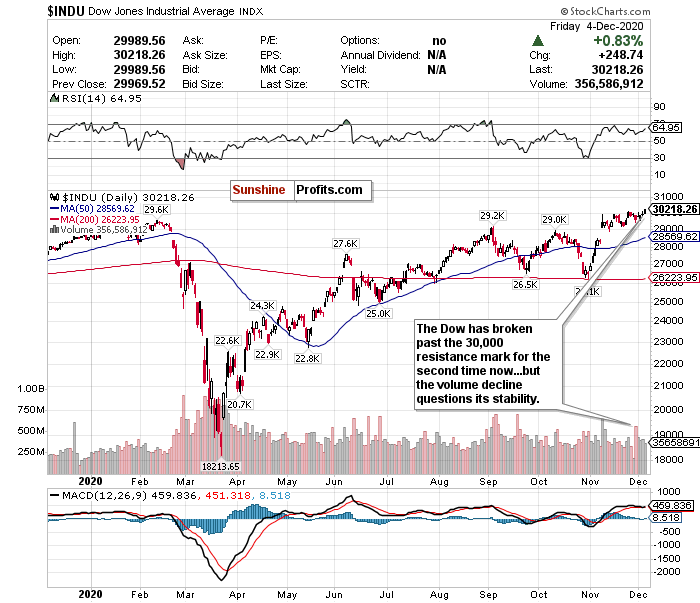

Can the Dow Remain Above 30,000?

The Dow Jones may be the major index most vulnerable to news and sentiment at this time. After breaking past the 30,000 level for the second time on Friday while volume sharply declined, doubts on the sustainability of the rally are no longer only sentiment based- they are technical based as well.

While the RSI still remains firmly in hold territory, the call on the Dow stays a HOLD.

On pessimistic “sell the news” kinds of days, the Dow will have more downside pressure than other indices. Many cyclical stocks that depend on a strong economic recovery trade on this index, and any change in sentiment can adversely affect their performances.

Comparably to the call on the S&P, it is hard to say with conviction that a drop in the index will be strong and sharp relative to the gains since March - let alone November. Just be very mindful that we have nearly reached overbought euphoria. For now, though, I believe that we could be in a sideways pattern for the near-term. For an ETF that attempts to directly correlate with the performance of the Dow, the SPDR Dow Jones ETF (DIA) is a strong option.

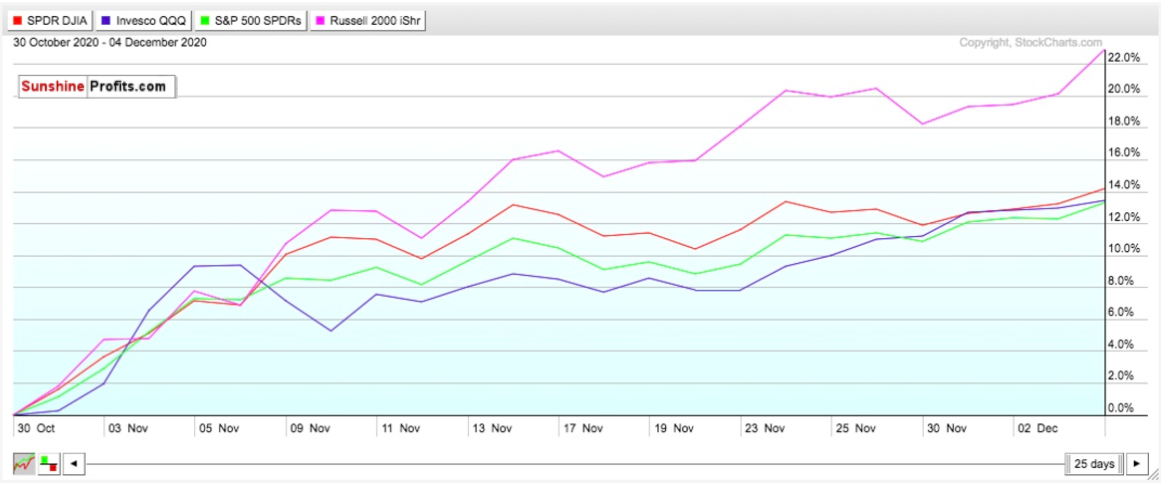

Can Small-caps Own December Too?

The Russell 2000 small-cap index once again outperformed the other indices on Friday. After gaining another 2.2% and closing at yet another record high, the Russell’s surge since November continued. Just look how the iShares Russell 2000 ETF (IWM) compares to the ETFs tracking the Dow, S&P, and Nasdaq in that time frame. Since November, the Russell has risen over 22%. This is nearly 7-8% higher than all the other major indices. Much of this can be attributed to the amount of cyclical stocks in the index that are dependent on the recovery of the broader economy.

If the last 9 months have shown us anything, it’s that Russell stocks will surge on optimistic days, and drop more on pessimistic days. In the long-term, however, small-caps may be the best opportunity to bet on an economic recovery in 2021. However, in the short-term, small-cap stocks may be the most volatile of them all and are a HOLD.

Mid-Term

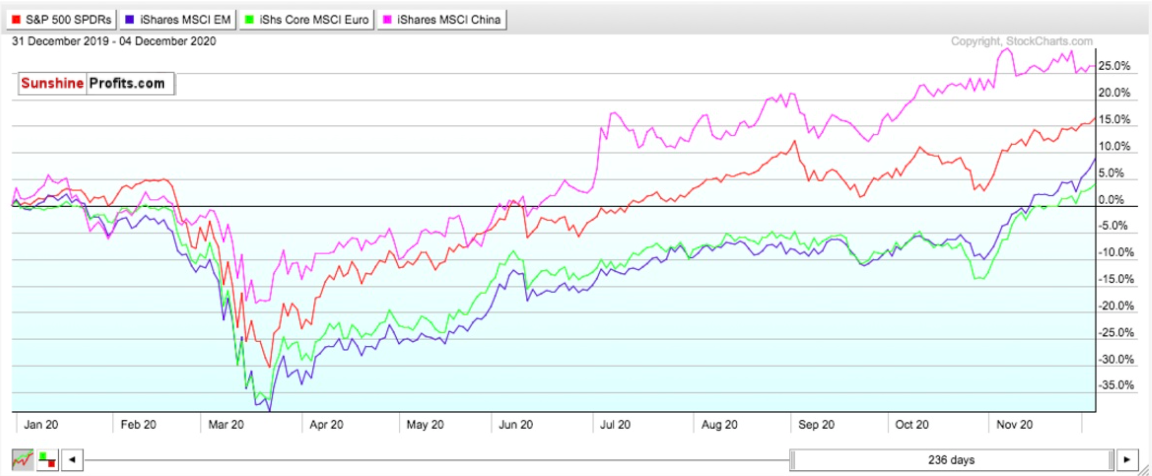

China Remains the Best Bet In Emerging Markets Over the Mid-Term

Investors remain bullish on emerging markets in both the short-term and medium-term. However, in the short-term it really depends on the region. China, for example, is by far the largest presence in emerging market indices, but it lagged significantly behind other global indices in November.

While China could outperform once again in December, there are renewed geopolitical tensions to worry about. Earlier in the week, Reuters reported on the possible blacklisting of a few Chinese companies, and President-elect Biden said that he would not remove tariffs on China- at least not early on in his administration. The House also passed a bill that could bar Chinese companies from listing on American exchanges if they do not adhere to U.S. auditing standards.

If you look at returns from December 31, 2019 to Friday’s close, and compare the performance of the iShares MSCI China ETF to the iShares MSCI Emerging Markets ex-China ETF, SPDR S&P ETF, and iShares Core Europe ETF the comparison is stunning. The only ETF that comes close to the China ETF’s returns is the SPDR S&P ETF- and the China ETF outperformed that by nearly 10%. Additionally, the ex-China ETF has only now begun to approach a 10% return while the Europe ETF has only now approached a 5% gain.

China has handled the pandemic better than other countries and continues to demonstrate its ability to handle COVID’s economic shocks. In fact, China’s GDP in Q3 this year outperformed its GDP in Q3 last year. China is also on pace to end the year with a net positive growth rate- despite its record plunge at the start of the pandemic.

For broad exposure to Emerging Markets, you will want to BUY the iShares MSCI Emerging Index Fund (EEM), for exposure to China you will want to BUY the iShares MCHI ETF (MCHI), and for exposure to a regional economic power without the geopolitical risks of China, you will want to BUY the iShares MSCI Taiwan ETF (EWT). Consider the iShares MSCI Indonesia ETF (EIDO) as well for another growing regional economy.

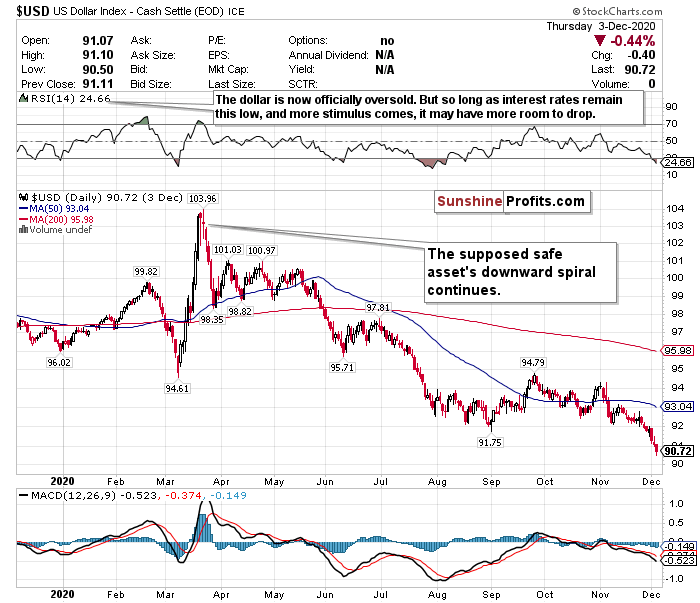

….and the Dollar Continues to Tank

The US Dollar continued its downward spiral on Friday, dropping another .44%. The dollar keeps hitting 2-year lows and has witnessed a staggering plunge in excess of 11% since March. I have been calling this dollar weakness all week despite the low level and expect it to continue.

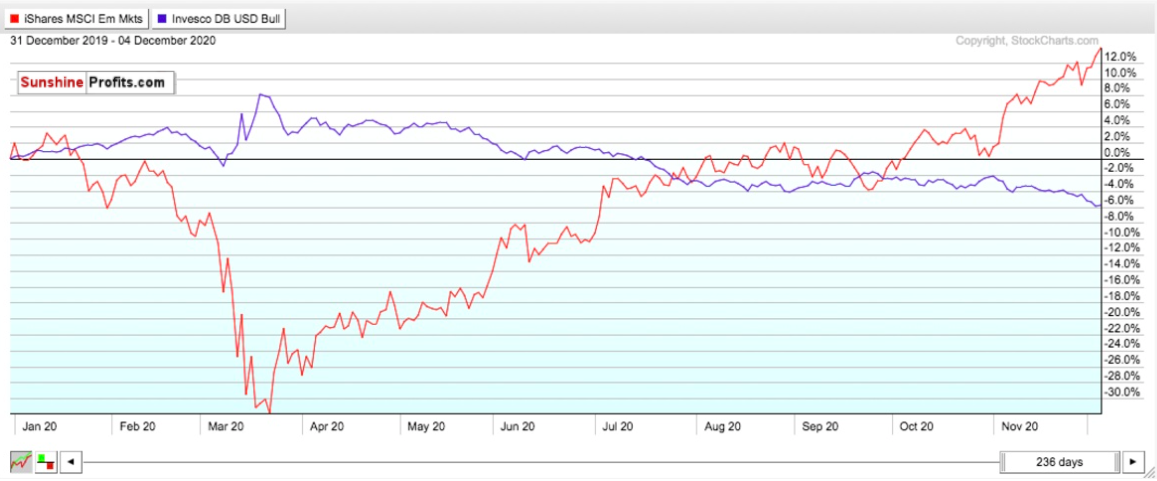

Further illustrating the dollar’s decline relative to emerging markets has been the performance of the iShares MSCI Emerging Market ETF (EEM) compared to the Invesco DB USD IDX Bullish ETF (UUP) since January.

Many believe that the dollar could fall further as well due to a multitude of headwinds.

If the world returns to relative normalcy within the next year, investors may be more “risk-on” and less “risk-off,” meaning that the dollar’s value will decline further.

Additionally, because of all of the economic stimulus that has been pumped into the markets thus far, combined with record low-interest rates, the dollar’s value has been hurt and could be further hurt. Please remember that the Fed does not plan on raising interest rates for at least another two years. This is an eternity for the dollar’s value.

As the world’s reserve currency, this plunge in value is concerning both in the short-term and mid-term for the US economy. A declining dollar means the strengthening of other foreign currencies such as the Yen or Yuan. Although US Treasuries have somewhat recovered, this could mean bad things for their values as well.

The plunge of the dollar has been so severe that it is currently trading below both its 50-day and 200-day moving averages. Furthermore, its 200-day moving average is considerably higher than its 50-day, further illustrating the sharp decline.

While the dollar may have more room to fall, according to its RSI, it is comfortably in oversold territory. This MAY be a good opportunity to buy the world’s reserve currency at a discount. But I just have too many doubts on the effect of interest rates this low, government stimulus, strengthening of emerging markets, and inflation to be remotely bullish on the dollar’s prospects over the next 1-3 years.

For now, HEDGE OR SELL USD exposure where possible.

Pay Very Close Attention to Inflation

Pay very close attention to the possible return of inflation within the next 6-12 months. The Fed has said it will allow the GDP to heat up, and it may overshoot in the medium-term as a result. Although JP Morgan and Goldman Sachs have cut their GDP growth estimates for Q1 2021, pay close attention to what happens in Q2 and Q3 once vaccines begin to be rolled out on a massive scale. It is only inevitable that inflation will return with the Fed’s policy and projected economic recovery by mid-2021.

If you are looking to the future to hedge against inflation, look into TIPS, commodities, gold, and potentially some REITS.

In the mid-term, I have BUY calls on the SPDR TIPS ETF (SPIP), the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC), the SPDR Gold Shares ETF (GLD), and the iShares Cohen & Steers REIT ETF (ICF).

Long-Term

While the surging spread of COVID-19 and resulting economic shutdowns may drive some short-term concerns, the progress made on the vaccine/treatment front poses significant optimism for 2021 and beyond. Although the news of Pfizer’s supply chain and distribution issues are concerning, and the November jobs report disappointed, the long-term outlook for equities, namely value stocks, and cyclicals, could be very positive.

Summary

We are thankfully in the home stretch of 2020- a tumultuous year filled with turmoil and pain. However, hopefully there is finally a light at the end of the tunnel, and we can enter 2021 with some optimism. But until COVID-19 is brought under control or is eradicated, there will be a continuous tug of war between vaccine optimism and health/economic pessimism.

Please keep in mind that markets are forward looking instruments and are investment vehicles that look 6-12 months down the road. However, it is very plausible that there could be some short-term uncertainty and volatility mixed in. But also remember how sharp and swift the rally was after the crashes in March. Since markets bottomed on March 23rd this is how the ETFs tracking the indices have performed: Russell 2000 (IWM) up 86.15%. Nasdaq (QQQ) up 79.08%. S&P 500 (SPY) up 65.86%. Dow Jones (DIA) up 63.02%. Markets long-term always end up going up and are focused on the future rather than the present.

If everything goes well with the vaccines, and the virus can be somewhat contained, the short-term volatility may be worth monitoring for opportunities before the eventual mid-term and long-term reality turns positive and stable in 2021.

To sum up all our calls, in the short-term I have a HOLD call for:

- the SPDR S&P ETF (SPY),

- Invesco QQQ ETF (QQQ)- (but consider trimming gains and/or selling),

- SPDR Dow Jones ETF (DIA), and

- iShares Russell 2000 ETF (IWM).

However, I am more bullish for these ETFs in the long-term.

In the mid-term, I suggest avoiding the US Dollar. Try gaining exposure in emerging markets instead.

I have BUY calls on:

- The iShares MSCI Emerging Index Fund (EEM),

- the iShares MSCI China ETF (MCHI),

- the iShares MSCI Taiwan ETF (EWT), and

- the iShares MSCI Indonesia ETF (EIDO)

Additionally, because I foresee inflation returning as early as mid to late 2021…

I also have BUY calls on:

- The SPDR TIPS ETF (SPIP),

- the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC)

- the SPDR Gold Shares ETF (GLD), and

- the iShares Cohen & Steers REIT ETF (ICF)

Thank you.

Matthew Levy, CFA

Stock Trading Strategist