tools spotlight

-

Does Gold Have a Friend in the USD?

February 9, 2021, 7:48 AMGold can thank a weaker dollar for its most recent jump, but have the yellow metal’s fundamentals changed or is it simply counter trending?

Do you remember the Beatles’ song With A Little Help from My Friends? Well, gold is getting a slight boost from its friend, the U.S. dollar. Ok, it’s a love and hate relationship, and gold is singing out of tune, as the fundamentals and overall outlook have not changed. Gold should be thinking “what will happen when the USD stands up and walks out on me?”

Gold moved higher yesterday (Feb. 8), and so did silver and miners. At the same time, the USD Index moved lower. Did the above change anything in the outlook? Let’s check.

Figure 1 - USD Index

In yesterday’s analysis, I commented on the USD Index’s performance in the following way:

Again, because assets don’t move in a straight line, it’s plausible that the USD Index retests its declining resistance line, while gold retests its rising support line. If this occurs, the USDX is likely to decline to the 90.6 range, while gold will receive a short-term boost. Remember though: the outcome does not change their medium-term trends and the above confirmations signal that the USDX is heading north and gold is heading south.

The part that I put in bold is exactly what is being realized right now. The USDX is correcting after the breakout, likely verifying the previous resistance as support.

Unless the USDX breaks back below the declining medium-term support line in a meaningful way, the bullish implications for the following weeks will remain intact.

So, nothing really changed from this perspective. The USD Index could actually move a bit lower and the overall outlook would not change.

But gold rallied – didn’t it change anything?

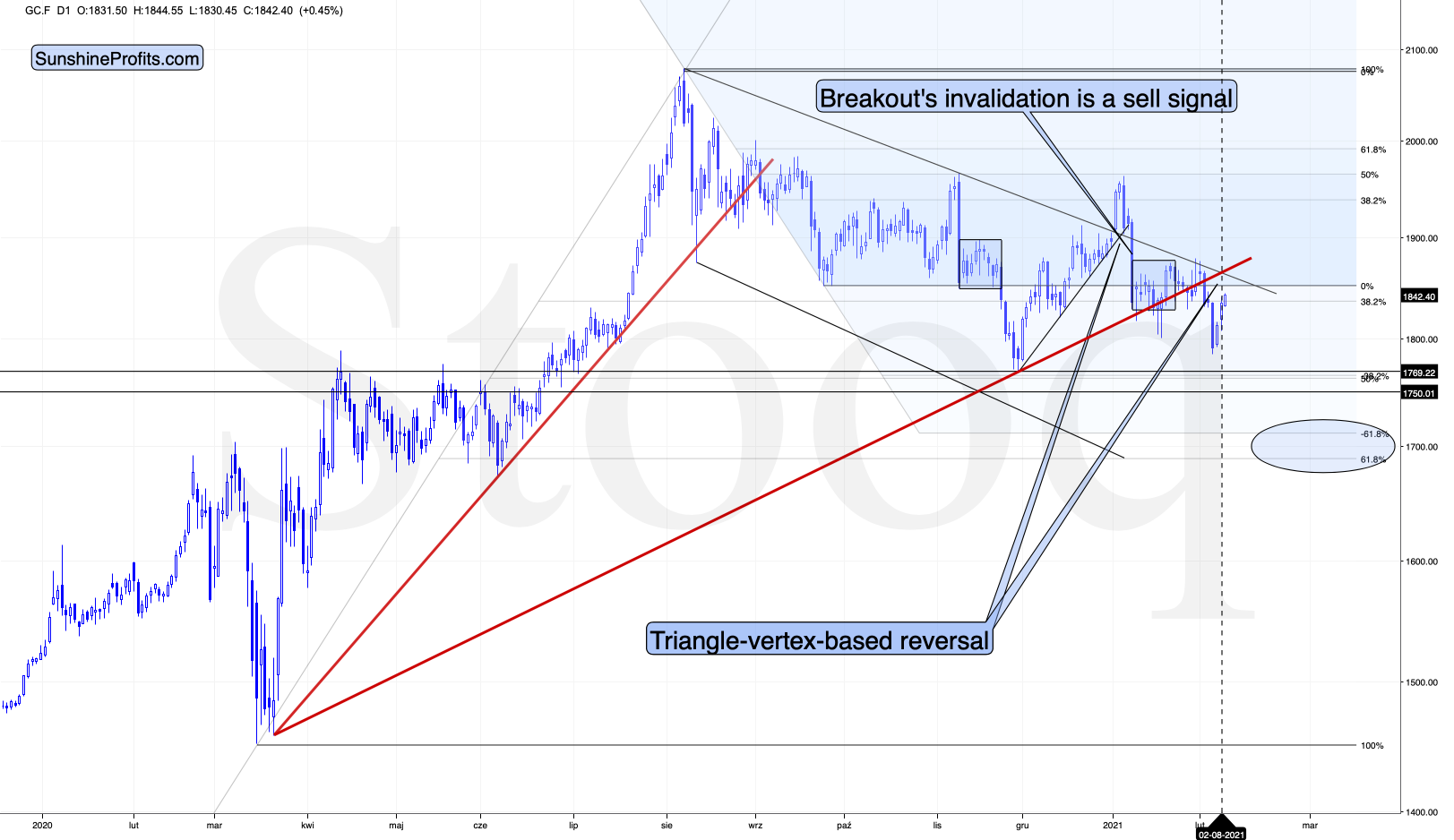

Figure 2 - COMEX Gold Futures

Not really. Once again, let’s quote what I wrote in the previous days (on Feb. 4):

In yesterday’s analysis, I wrote that the yellow metal’s breakdown below the rising red support line was not yet confirmed, but that the situation had already become more bearish. Gold closed below this line for the second day yesterday and given today’s decline, it seems that it’s going to close below it for the third consecutive day. This means that the breakdown is almost confirmed, and the implications are strongly bearish.

Now, given the proximity of the triangle-vertex-based reversal, I wouldn’t rule out a quick comeback and then another downturn within the next several days.

Theoretically, it’s possible that gold slides to $1,700 shortly and reverses there, but we wouldn’t bet the farm on this happening this or the next week. However, it is very likely to take place in February (more likely) or in March (less likely).

That’s exactly what we saw – a quick comeback. Gold is currently approximately at its triangle-vertex-based reversal, which means that it’s likely to reverse and decline any day or hour now.

So, again, nothing changed with regard to the outlook and nothing would likely change if gold moves a little higher from here as well (in analogy to the USD Index moving a little lower). What we’re seeing is either normal during a bigger upswing (post-breakout verification in the USD Index) or its direct consequence that fits other technical signs (gold’s quick comeback).

What about silver, did the white metal change anything?

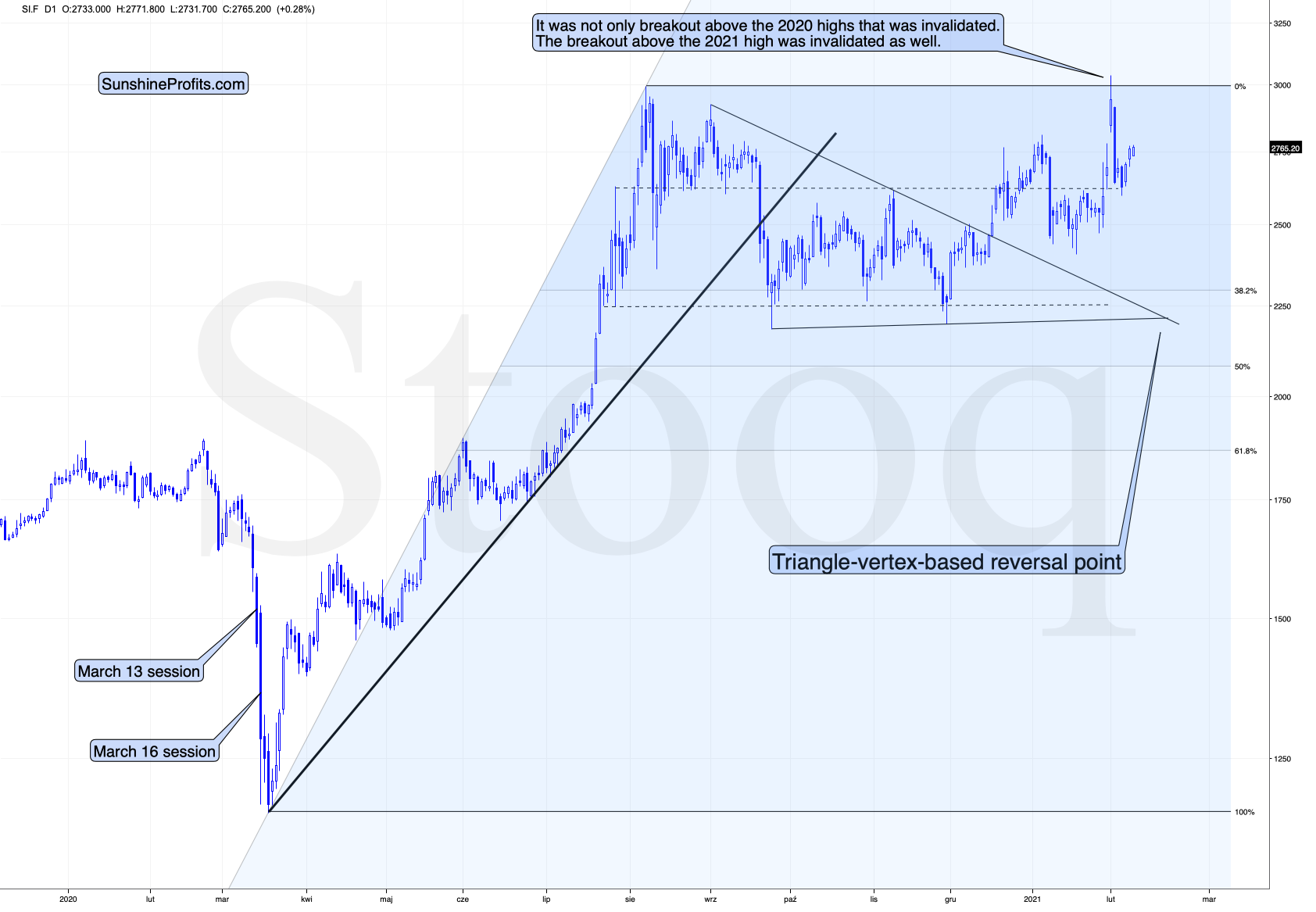

Figure 3 - COMEX Silver Futures

Not really. Just like gold, silver is taking a breather after the increased volatility. This is normal.

And the miners?

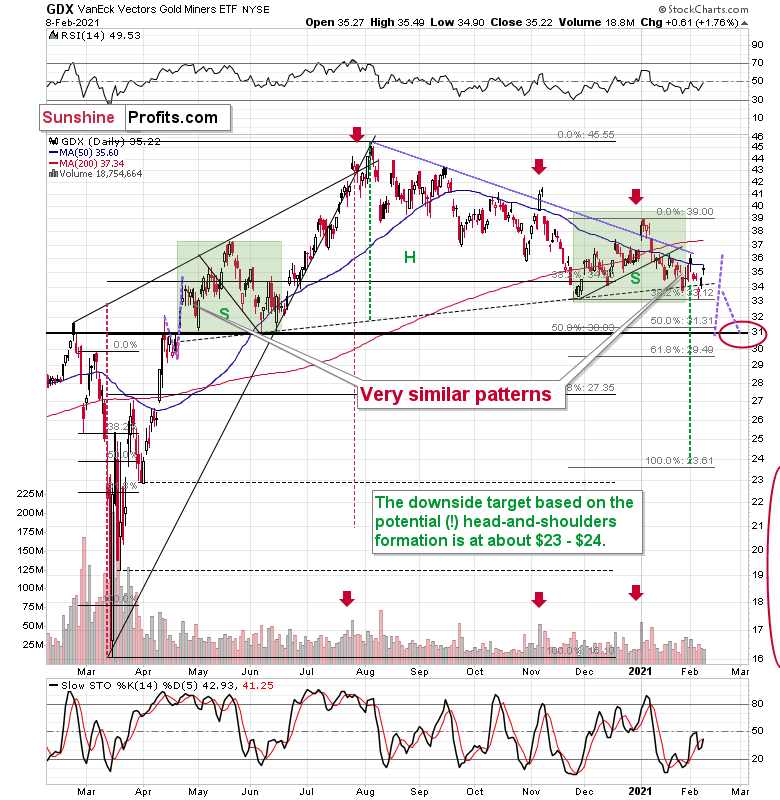

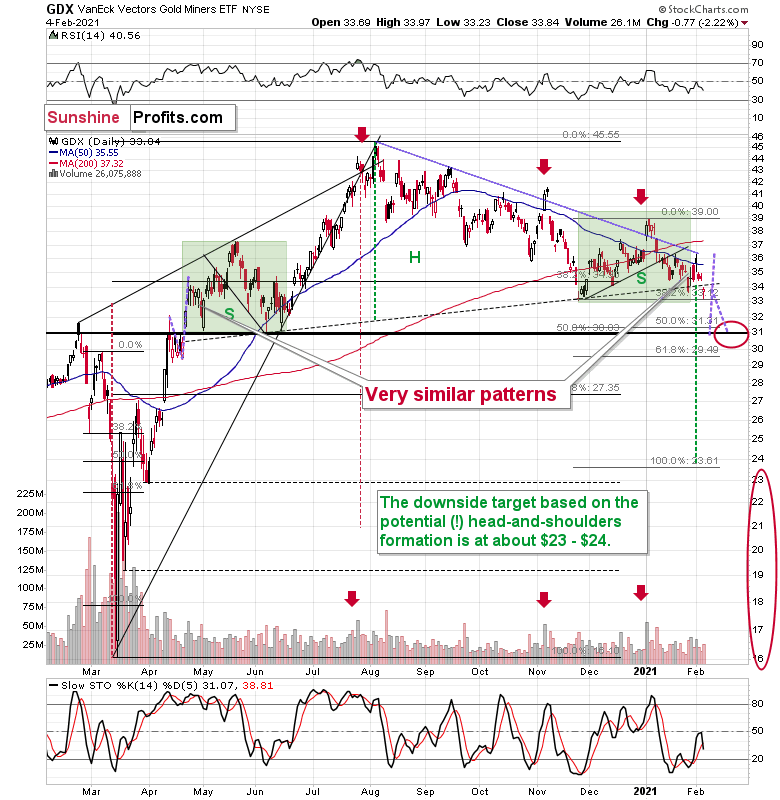

Figure 4 - VanEck Vectors Gold Miners ETF (GDX)

Mining stocks are declining in a relatively regular manner as well. After their early January top, they declined profoundly, and since that time they have also been declining, but at a slower pace. We’ve been seeing lower highs and lower lows in the past month or so, and yesterday’s upswing fits this pattern very well.

Ever since the mid-September breakdown below the 50-day moving average, the GDX ETF was unable to trigger a substantial and lasting move above this MA. The times when the GDX was able to move above it were also the times when the biggest short-term declines started.

So, did anything change yesterday? Not really.

The most recent move higher only made the similarity of this shoulder portion of the bearish head-and-shoulders pattern to the left shoulder (figure 4 - both marked with green) bigger. This means that when the GDX breaks below the neck level of the pattern in a decisive way, the implications are likely to be extremely bearish for the next several weeks or months.

Due to the uncanny similarity between the two green rectangles, I decided to check what happens if this mirror-similarity continues. I used purple, dashed lines for that. There were two important short-term price swings in April 2020 – one shows the size of the correction and one is a near-vertical move higher.

Copying these price moves (purple lines) to the current situation, we get a scenario in which GDX (mining stocks) moves to about $31 and then comes back up to about $34. This would be in perfect tune with what I wrote previously. After breaking below the head-and-shoulders pattern, gold miners would then be likely to verify this breakdown by moving back up to the neck level of the pattern. Then, we would likely see another powerful slide – perhaps to at least $24.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

What’s Next for the Silver Roller Coaster?

February 8, 2021, 9:52 AMAfter a frenzy of Reddit induced activity that captivated everyone, silver painfully gave back what it gained. What’s next for the white metal?

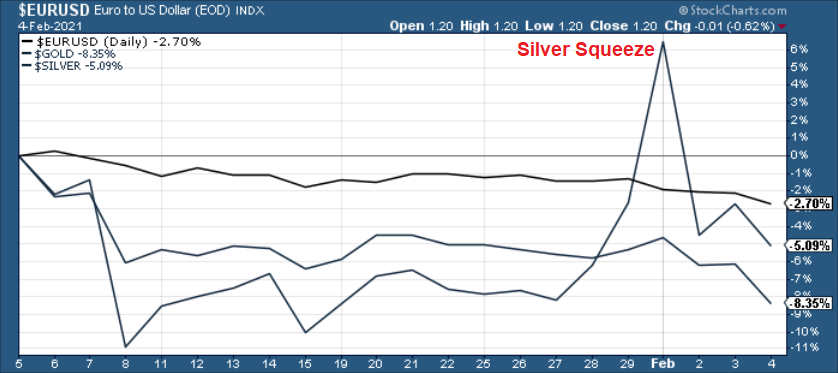

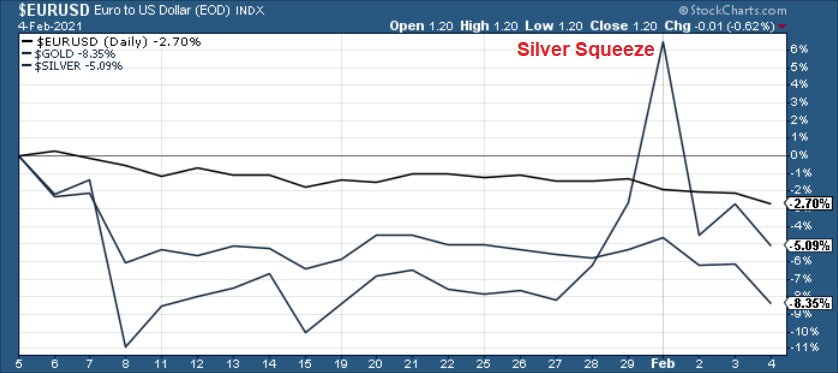

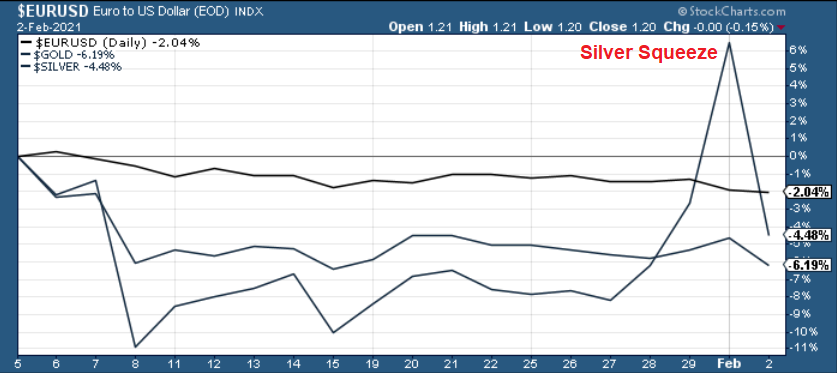

As the precious metals’ version of moral hazard, silver tipped over the flowerpot, and left gold to clean up the mess. After silver’s short squeeze mania ended in tears on Feb. 2, the white metal gave back 97% of its squeeze-induced gains. Conversely, bearing the brunt of the market’s wrath, gold gave back 237% of the momentum-induced gains.

Please see below:

Figure 1

As a result, silver is doing what it normally does near market tops: outperforming among comments regarding silver shortage.

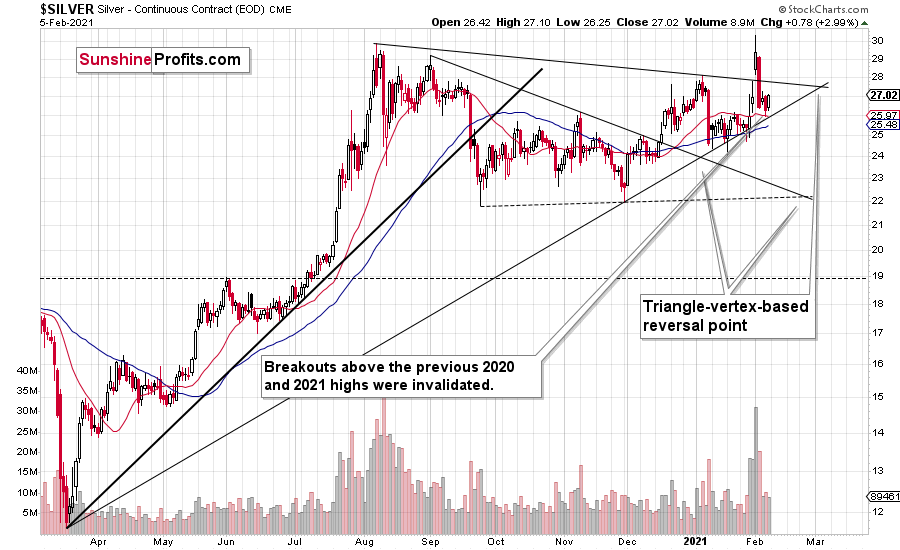

Positioning itself for an epic blow-off top, silver’s Feb. 1 surge ended in less than 24 hours. In addition, silver is approaching two triangle-vertex-based reversal points – which could come to a head by the end of February or early March. However, given the two set ups, they could be signaling one climactic reversal or two separate reversals of differing magnitudes. As it stands today, it’s still too early to tell.

Figure 2 - COMEX Silver Futures

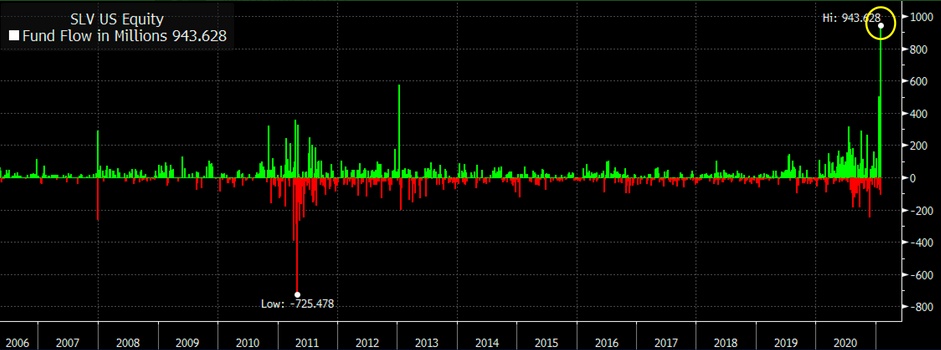

However, supporting the argument of a single blow-off top, I mentioned last week that the iShares Silver Trust ETF (SLV) took in nearly $1 billion in daily inflows on Jan. 29. For context, that was nearly double the previous record.

Please see below:

Figure 3 - Source: Bloomberg/Eric Balchunas

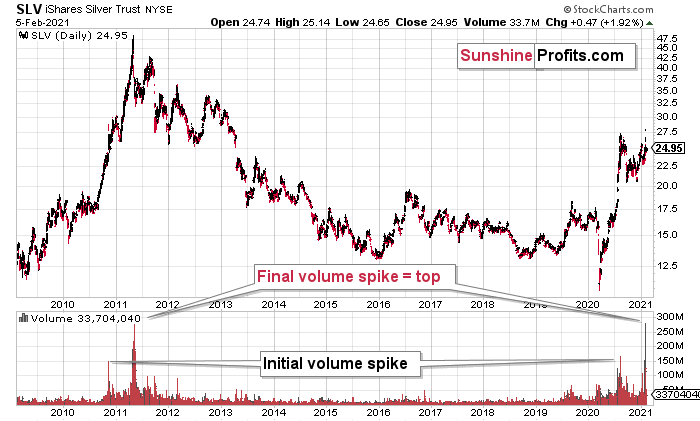

But because too much of a good thing can often be bad, the frantic buying mirrored an ominous period in SLV’s history.

Please see below:

Figure 4 - COMEX Silver Futures

If you analyze the volume spikes at the bottom of the chart, 2021 and 2011 are a splitting image. To explain, in 2011, an initial abnormal spike in volume was followed by a second parabolic surge. However, not long after, silver’s bear market began.

SLV-volume-wise, there's only one similar situation from the past - the 2011 top. This is a very bearish analogy as higher prices of the white metal were not seen since that time, but the analogy gets even more bearish. The reason is the "initial warning" volume spike in this ETF. It took place a few months before SLV formed its final top, and we saw the same thing also a few months ago, when silver formed its initial 2020 top.

The history may not repeat itself to the letter, but it tends to be quite similar. And the more two situations are alike, the more likely it is for the follow-up action to be similar as well. And in this case, the implications for the silver price forecast are clearly bearish.

Based on the above chart, it seems that silver is likely to move well above its 2011 highs, but it’s unlikely to do it without another sizable downswing first.

In conclusion, if silver meets its maker, the white metal is likely to lead gold and the miners to slaughter. Moreover, silver is well known for its false breakouts and its relative strength is often a precursor to substantial declines. As a result, last week’s short squeeze was much more semblance than substance. In contrast, once the metals rebase and trade at more appropriate levels, an attractive buying opportunity will emerge.

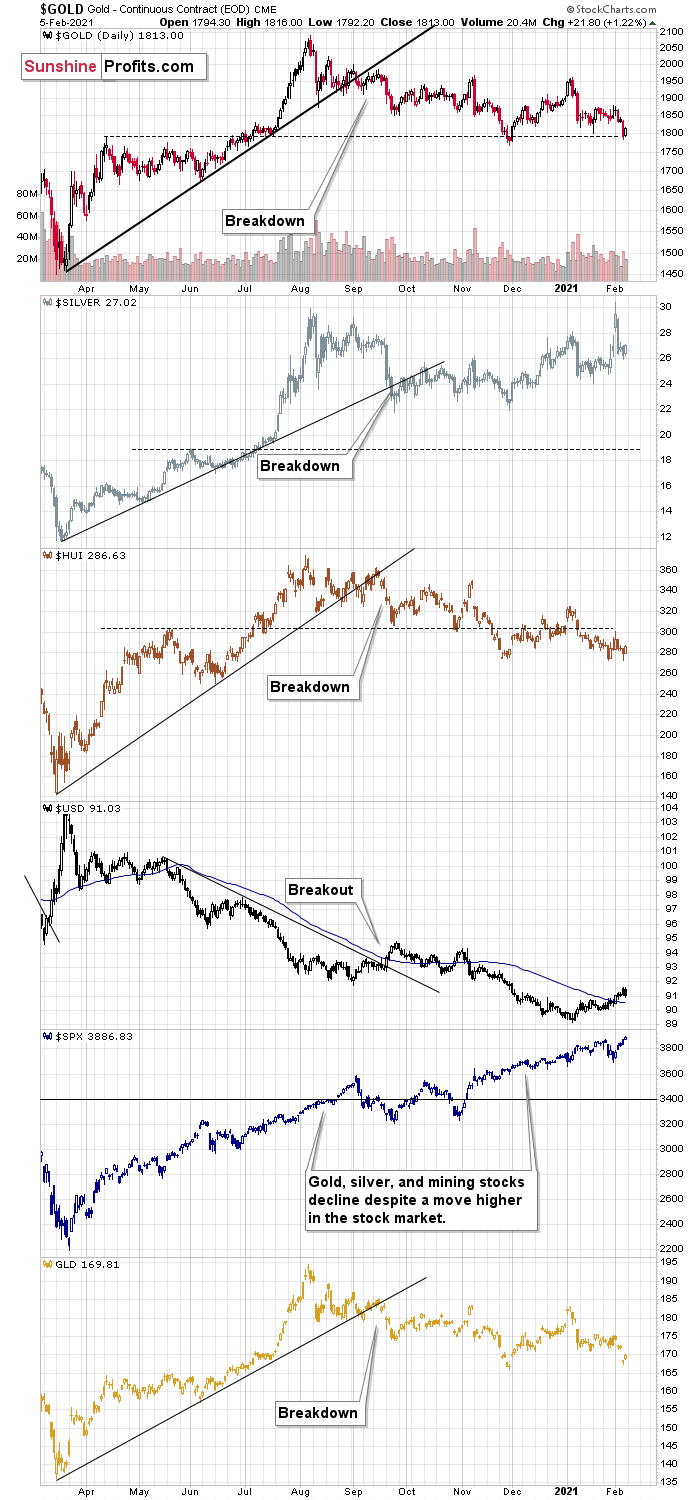

For more insight, let’s look at the relative performance of gold, silver and the gold miners, and compare how they’re impacted by the USDX and the SPX. If you analyze the chart below, you can see that the precious metals all broke down in September, after the USDX broke above resistance.

Figure 5

To explain, I wrote on Jan. 18:

Like traffic lights flashing red, notice how the HUI Index (proxy for gold stocks) is trading well below its early 2020 highs? In stark contrast, gold remains moderately above its early 2020 highs, while silver is significantly above its early 2020 highs. The misaligned performance – with silver outperforming and gold miners underperforming – puts a bow on this bearish package.

The bottom line?

It is not only the case that silver was strong and miners were weak in the last several days – it’s been the case over the past several months as well. The implications are bearish.

Also troubling is that the stock market that’s soaring in the medium term, hasn’t shined its light upon the PM market. Contrasting the mantra that ‘a rising tide lifts all boats,’ equity market strength hasn’t triggered a sustainable rally in silver or the gold miners. And this “should have” been the case – both are more connected to stocks than gold is. Gold stocks because they are, well, stocks. Silver, due to multiple industrial uses

All in all, based on what we saw in silver recently, it doesn’t seem that we’re likely to see much higher precious metals prices without seeing a major decline first.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

How Europe’s Underperformance May Hurt Gold

February 5, 2021, 9:24 AMGold most recently dipped below $1800 and it’ll be testing new lows in the days and weeks ahead. How does the European connection place even further downward pressure on the precious metals?

We’ve recently written quite a bit about the importance of the EUR/USD pair and how the precious metals are tied to it, and we’ll delve further into this matter today, but before we do, let’s take a look at mining stocks, using the GDX ETF as a proxy for them.

Figure 1 – VanEck Vectors Gold Miners ETF (GDX)

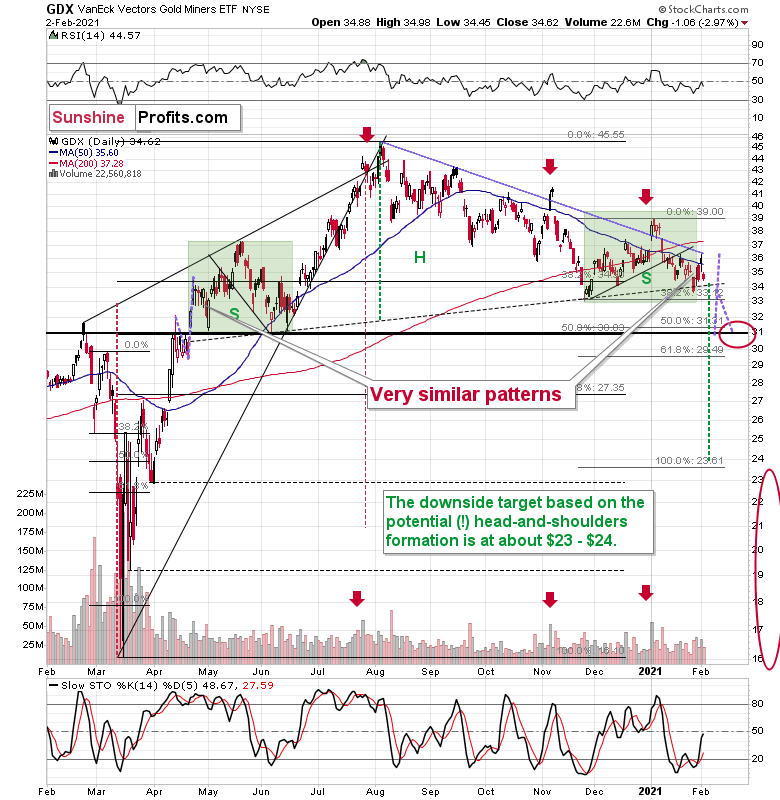

Miners declined decisively yesterday (Feb. 4), and they once again closed below the neck level of the head-and-shoulders pattern. The final pause before the slide seems to be over.

Are miners weak right now? Of course, they are weak. It was not only silver that got attention recently, but also silver stocks. The GDX ETF is mostly based on gold stocks, but still, silver miners’ performance still affects it. And… GDX is still trading relatively close to the yearly lows. Silver moved a bit above its 2020 highs – did miners do that as well? Absolutely not, they were only able to trigger a tiny move higher.

And based on Wednesday’s decline, most of the recent run-up was already erased.

Interestingly, the most recent move higher only made the similarity of this shoulder portion of the bearish head-and-shoulders pattern to the left shoulder (figure 2 - both marked with green) bigger. This means that when the GDX breaks below the neck level of the pattern in a decisive way, the implications are likely to be extremely bearish for the next several weeks or months.

Due to the uncanny similarity between the two green rectangles, I decided to check what happens if this mirror-similarity continues. I used purple, dashed lines for that. There were two important short-term price swings in April 2020 – one shows the size of the correction and one is a near-vertical move higher.

Copying these price moves (purple lines) to the current situation, we get a scenario in which GDX (mining stocks) moves to about $31 and then comes back up to about $34. This would be in perfect tune with what I wrote previously. After breaking below the head-and-shoulders pattern, gold miners would then be likely to verify this breakdown by moving back up to the neck level of the pattern. Then, we would likely see another powerful slide – perhaps to at least $24.

All in all, it seems that silver’s run-up was just a temporary phenomenon and the next big medium-term move in the precious metals and mining stocks is going to be to the downside.

There’s something more about those big head-and-shoulders patterns that you should know, and it’s not something minor.

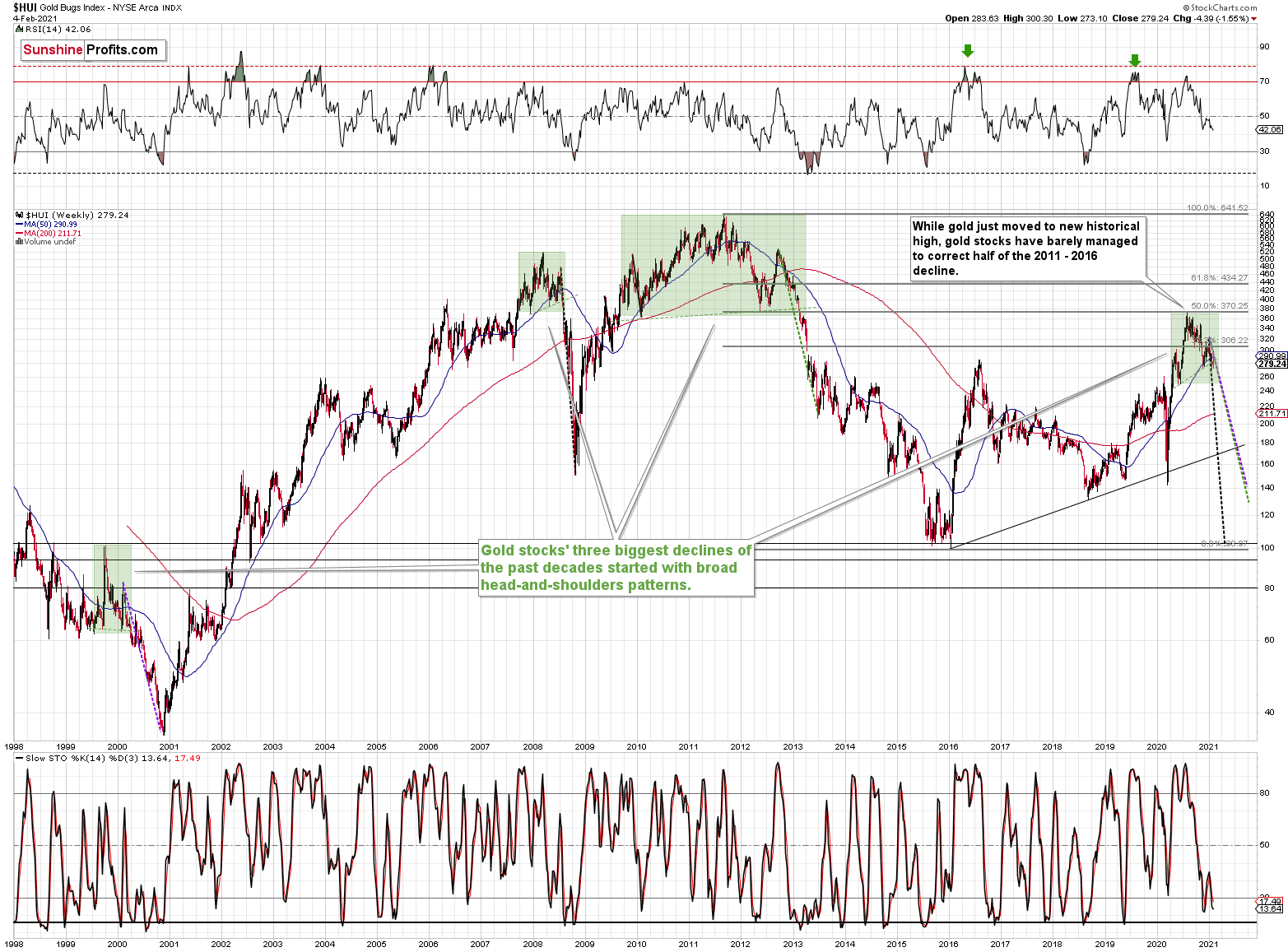

Figure 2

The thing is – the three of the biggest declines in the mining stocks (I’m using the HUI Index as a proxy here), all started with broad, multi-month head-and-shoulders patterns.

And now we’re seeing this pattern all over again. The above picture should make it clear why I was putting “at least” in bold, when describing the targets based on the head-and-shoulders patterns.

In all three cases, the size of the decline exceeded the size of the head of the pattern. This means that the $24 target on the GDX ETF chart is likely conservative.

Can we see gold stocks as low as we saw them last year? Yes.

Can we see gold stocks even lower than at their 2020 lows? Again, yes.

Of course, it’s far from being a sure bet, but the above chart shows that it’s not irrational to expect these kind of price levels before the final bottom is reached.

The dashed lines starting at the 2020 top are copies of sizes of the declines that started from the right shoulder of the previous patterns. If things develop as they did in 2000 and 2012-2013, gold stocks are likely to bottom close to their 2020 high. However, if they develop like in 2008 (which might be the case, given the extremely high participation of the investment public in the stock market and other markets), gold stocks could re-test (or break slightly below) their 2016 low.

I know, I know, this seems too unreal to be true… But wasn’t the same said about silver moving below its 2015 bottom in 2020? And yet, it happened.

Having said that, let’s go to Europe and take a look at the markets from the fundamental point of view.

Down Where We Belong

For weeks, I’ve been warning that the Eurozone economy and the EUR/USD were on a collision course. And with Europe’s fundamental underperformance accelerating at a drastic pace, we may have just had impact.

On Feb. 4, the EUR/USD hit its lowest level since Nov. 30.

Please see below:

Figure 3

Along for the ride, the EUR/USD’s pain has not been the PMs gain. Because of their strong correlation, it’s no surprise that the euro’s downfall is making waves across the precious metals’ market.

Figure 4

Foretelling the decline, I warned that the EUR/GBP was about to crack. And given the EUR/USD’s strong correlation with the EUR/GBP, the latter’s collapse was an early warning sign.

On Monday (Jan. 25), I wrote that Janet Yellen’s pledge to “act big” on the next coronavirus relief package ushered the EUR/GBP back above critical support.

However, on Tuesday (Jan. 26), the key level broke again.

Please see below:

Figure 5

More importantly though, a break in the EUR/GBP could be an early warning sign of a forthcoming break in the EUR/USD.

Figure 6

If you analyze the chart above, ~20 years of history shows that the EUR/GBP and the EUR/USD tend to follow in each other’s footsteps. As a result, if the EUR/GBP retests its April low (the next support level), the EUR/USD is likely to tag along for the ride (which implies a move back to ~1.08).

And living up to its billing, the EUR/GBP is racing toward its April low.

Please see below:

Figure 7

And if the April low breaks, it could be lights out for the EUR/USD. Already, the currency pair has broken below its long-term declining resistance line. And if the technical damage continues and the EUR/USD breaks below the 1.16/1.17 level, its long-term support (roughly 1.05) is well within the range of its April low (roughly 1.08).

Figure 8

To make the fundamental case for a lower EUR/USD, the U.S. Treasury revealed on Feb. 1 that it plans to borrow $274 billion in the first quarter of 2021. In stark contrast to its November estimate of $1.127 trillion, the massive 76% reduction (the red box below) is the result of stimulus gridlock in Washington.

Figure 9 - Source: The U.S. Department of the Treasury

From a currency perspective, the about face is extremely bullish for the U.S. dollar. With the European Central Bank’s (ECB) printing press working 24/7, the FED/ECB ratio has already declined by 0.26% week-over-week. And now, with the U.S. Treasury reducing its Q1 borrowing, the ratio should continue to move lower.

To explain, the U.S. Treasury raises money by selling bonds to the general public. And to keep interest rates low, the FED purchases these bonds on the secondary market. The two claim that they don’t collaborate, however, the end result is always the same: the more bonds the Treasury issues, the more purchases that the FED has to make to keep interest rates low. Conversely, the less bonds the Treasury issues, the less purchases that the FED has to make to keep interest rates low.

As a result, the Treasury’s latest projection adds more wind to the greenback’s sails.

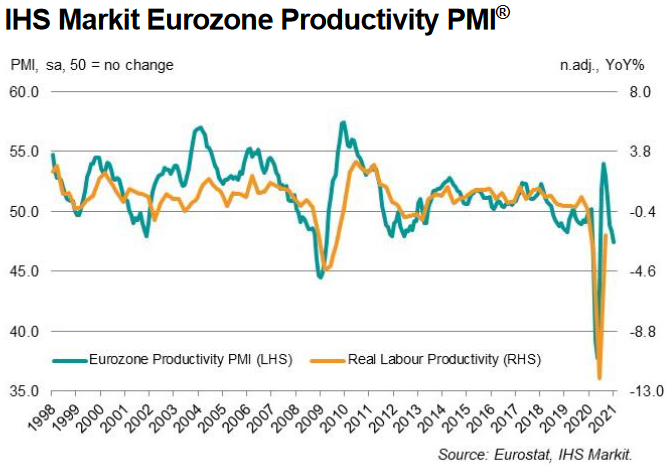

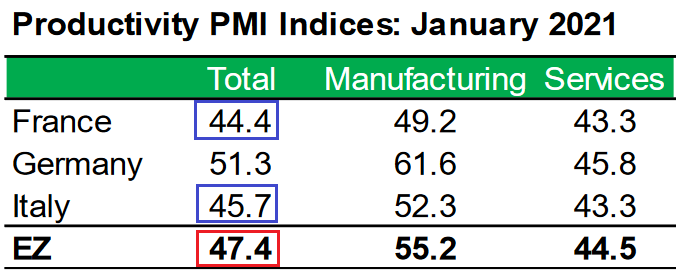

Also supportive of a weaker EUR/USD, the Eurozone economy remains on life support. On Feb. 4, IHS Markit revealed that its Eurozone Productivity PMI fell for a third-straight month (to 47.4 in January) and that the latest decline occurred at the quickest pace since June.

Please see below:

Figure 10

To explain the term, I wrote previously:

PMI (Purchasing Managers’ Index) data is compiled through a monthly survey of executives at more than 400 companies. A PMI above 50 indicates business conditions are expanding, while a PMI below 50 indicates that business conditions are contracting (the scale on the left side of the chart).

Even more insightful, service sectors in France and Italy (Europe’s second and third-largest economies) led the PMI decline, as both countries (figure 15 – the blue boxes below) underperformed the bloc average (figure 15 – the red box below).

Figure 11 - Source: IHS Markit

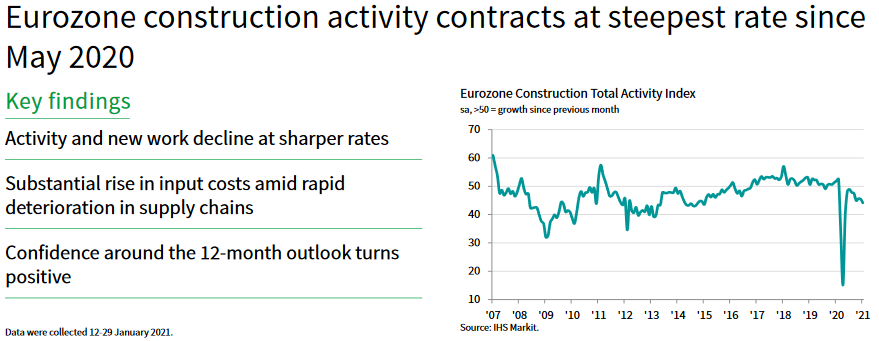

To make matters worse, Eurozone construction activity has fallen off a cliff. The IHS Markit Eurozone Construction PMI recorded its sharpest decline since May and an excerpt from the release read:

“The decline in construction output across the Eurozone was driven by falls in each of the three largest economies in the region. France posted the steepest rate of contraction, followed by Germany, with both countries seeing rates of contraction quicken since December. Italy meanwhile recorded a drop in construction activity for the third time in the past four months, albeit one that was only mild.”

But the one saving grace? 12-month confidence in Europe turned positive.

Please see below:

Figure 12

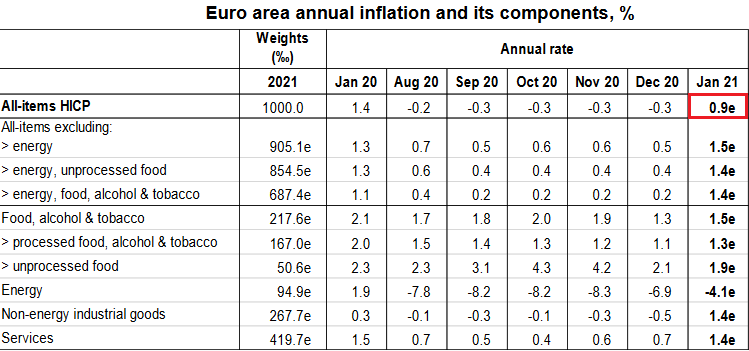

Indicating superficial strength, Eurozone inflation also rose by 0.90% in January (the red box below).

Figure 13 - Source: Eurostat

And while the positive January print ended a streak of seven-straight months of negative inflation, it’s not a cause for celebration. Previously, I wrote that higher inflation is a precursor to higher interest rates; and higher interest rates are a precursor to a stronger currency.

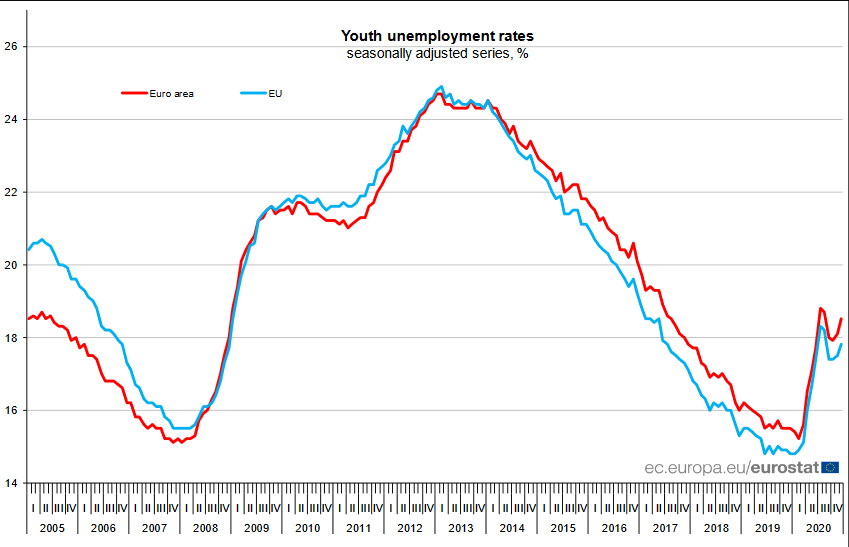

However, in the Eurozone, inflation is rising alongside deteriorating economic fundamentals. If you combine everything above with the fact that the youth unemployment rate (persons under 25) in Europe increased from 18.1% to 18.5% month-over-month in December, the region could be headed for stagflation.

Please see below:

Figure 14

To explain the term, stagflation occurs when a region has high inflation and high unemployment. In a nutshell: it’s the worst possible outcome for an economy, as monetary and/or fiscal easing becomes a double-edged sword.

Further supporting the possibility, the overall Eurozone unemployment rate has barely moved since September. Despite the best efforts of Europe’s governments and central bank, progress has become a slow process.

Figure 15 - Source: Eurostat

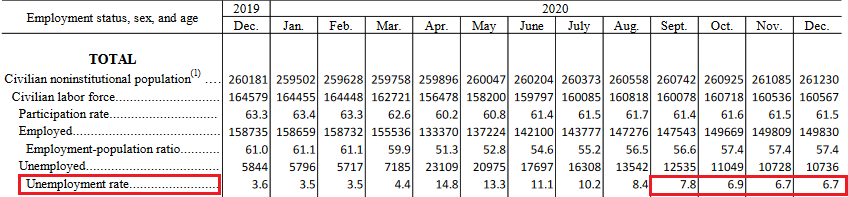

Conversely, the U.S. unemployment rate has fallen by 1.1 points since September – delivering yet another data point of relative outperformance.

Figure 16 - Source: U.S. Bureau of Labor Statistics (BLS)

In conclusion, the EUR/USD remains destined for devaluation. The Eurozone economy is drastically underperforming the U.S. and market participants are finally starting to accept this reality. As a result, the PMs are likely to remain under pressure. Given their strong correlation with the currency pair, a weaker EUR/USD is likely to drop the hammer on the metals. However, once the technical and fundamental damage is complete, the PMs will shine once again.

Letters to the Editor

Q: You have introduced a glittering array of charts and data to support your macro thesis, which is playing out, albeit in slow motion. I was in wealth management my entire career and I have never seen ANYTHING as comprehensive as what you produce. Not wanting to jump the gun, but I gather that the GDX tends to outperform in the early stages of a recovery and then the GDXJ tends to take over... then silver becomes a later runner. Do you see any reason why the forthcoming recovery will not follow this? To make it simpler... would it be fair to concentrate on gold mining stocks initially and to avoid SILJ in the early months? Finally have you heard of JGLD? It’s a new PROPER JUNIOR MINING EFT. GDXJ is mainly mid-tier stocks these days. I thought other readers would be interested.

A: It’s great to hear compliments from a professional – thank you!

As far as the relative performance is concerned, the above is indeed what’s often taking place, but I would like to emphasize (for those who might be reading my analysis for the first time today) that this outperformance doesn’t mean a situation where one market stops rallying and then only the other market is moving. No, it means that they all move in the same direction, but one of them is providing a bigger bang for the buck at a given time. Senior miners tend to do that at first (along with junior miners to some extent), then junior miners start to perform a bit better than seniors and silver is often strongest in the final parts of a given rally.

I wouldn’t use the word “avoid” with regard to SILJ in the early months of the next medium-term upswing, as it might imply that it’s bad ETF or one that would trigger losses even though the rest of the precious metals market moves higher. I’d use “prefer” or “use mostly for diversification purposes”. If you look at the SILJ to SIL ratio, you see that after the bottom silver juniors didn’t really lag the silver seniors, initially, but they did outperform about 2 months after the bottom.

Figure 17

Then again, if one followed the “seniors first, then juniors, and then silver” rule, they would still likely be happy with the results.

As far as JGLD is concerned – thank you for mentioning it. I haven’t previously commented on it. I agree that there are not as many juniors in the GDXJ junior ETF as there should be and that’s its more similar to the GDX than it should, and that the JGLD does solve this problem by having mostly low-cap juniors. However, it seems to me that it’s too early to use this ETF as it was launched only about two months ago and the liquidity in it is still very low. If it increases substantially before the time comes to focus on junior miners (as above), then this might be my unleveraged junior miner ETF of choice. Some people will likely still prefer the leveraged ones, though.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

Will Gold Chart New Lows as USD Rises?

February 4, 2021, 10:12 AMAs the silver craze subsides and the USD rises - partly due to a better-than-expected U.S. jobless report - gold and the precious metals will be testing deeper waters.

While silver stole the spotlight recently, I’ve been emphasizing the importance of what’s happening in the USD Index and gold. Developments in both markets had bearish implications for the precious metals market overall, and we didn’t have to wait long for the results.

Namely, gold moved lower once again in today’s pre-market trading and it’s currently testing its 2021 lows.

Figure 1

In yesterday’s analysis, I wrote that the yellow metal’s breakdown below the rising red support line was not yet confirmed, but that the situation had already become more bearish. Gold closed below this line for the second day yesterday and given today’s decline, it seems that it’s going to close below it for the third consecutive day. This means that the breakdown is almost confirmed, and the implications are strongly bearish.

Now, given the proximity of the triangle-vertex-based reversal, I wouldn’t rule out a quick comeback and then another downturn within the next several days.

Theoretically, it’s possible that gold slides to $1,700 shortly and reverses there, but we wouldn’t bet the farm on this happening this or the next week. However, it is very likely to take place in February (more likely) or in March (less likely).

Why is this move likely to happen soon? Because of what happened in the USD Index.

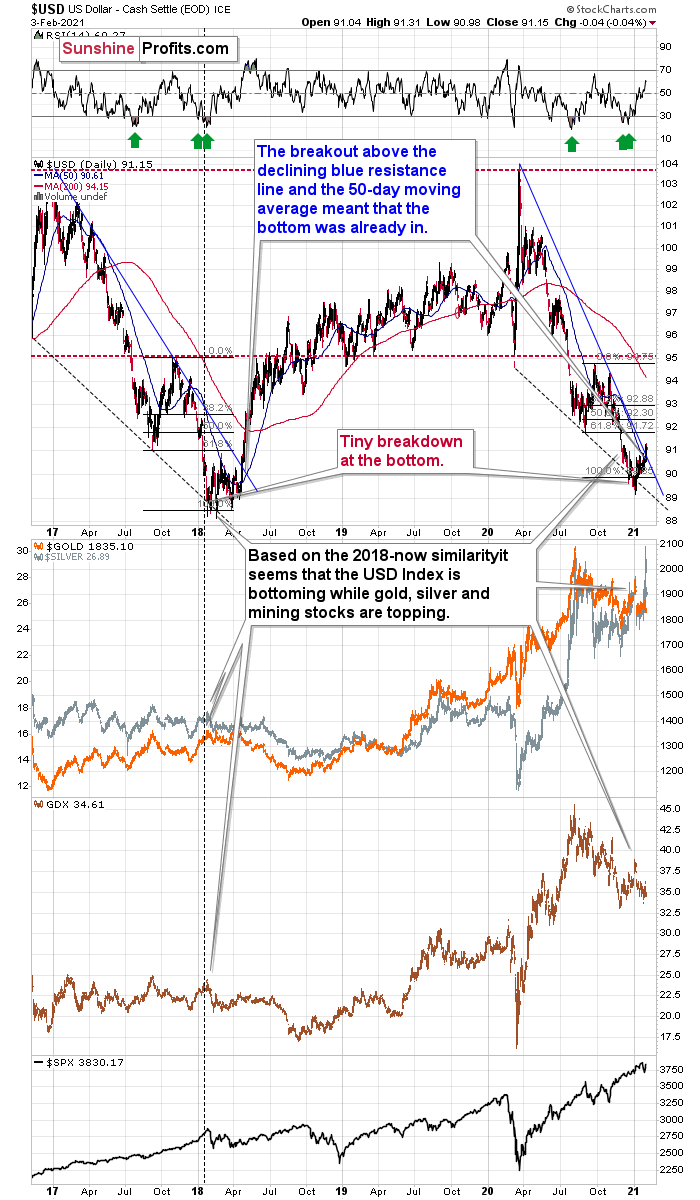

Figure 2

The U.S. currency just confirmed two important breakouts:

- Breakout above the neck level of the inverse head-and-shoulders pattern

- Breakout above the declining medium-term resistance line based on the March 2020 and November 2020 highs.

The above is important also due to another – even more critical – reason.

Figure 3

Based on the remarkable similarity to early 2018 (also in bitcoin and dogecoin, and most likely also in stocks to some extent), the breakout above the declining resistance line (and the 50-day moving average) is likely to mark the start of a big, sharp upswing.

Back in 2018, the rally continued until the USD Index moved to its previous medium-term high. Afterwards, it started to move in a more moderate manner.

If the history rhymes once again (the similarity has been uncanny in the previous months), then the next temporary stop for the USD Index is a bit below 95, as that’s when the USDX topped in September 2020. Precisely, that was 94.80, so to be conservative, we can say that the next particularly significant resistance for the USD Index is at about 94.5.

Will this level correspond to gold at $1,700? This might be the case, but it could also be the case that gold declines to $1,700 even sooner. Given the current gold-USD dynamics, I don’t expect to see the USD Index at about 95 without seeing gold decline to at least $1,700.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief -

EUR and Silver: Going Down a One-Way Street

February 3, 2021, 10:28 AMSince the precious metals like to ride along with the EUR/USD, and the latest Eurozone data looks grim, what are the implications for the PMs?

Just when everyone and their brother thought that silver was going straight to the moon… it plunged. And that’s not the end of the decline.

Figure 1 – COMEX Silver Futures

I previously emphasized that silver’s volatile upswing is likely just temporary, and I discussed the Kondratiev cycle which implies much higher gold prices but not necessarily right away, because the value of cash (USD) would be likely to soar as well. The latter would likely trigger a temporary slide in gold – and silver.

Well, was silver’s rally just temporary?

This seems to have been the case. The white metal declined back below not only the 2020 highs, but also back below this year’s early high. Please remember that invalidations of breakouts have immediately bearish implications and we just saw more than one in case of silver.

So far today (Feb. 3), silver is quiet, but let’s keep in mind that back in September, it took only a few sessions for the white precious metal to move from approximately the current price levels to about $22.

Will silver slide as much shortly? This is quite likely, although the downswing doesn’t have to be as quick as it was in September.

Terms like the silver shortage, the size of the silver market and silver manipulation became incredibly popular in the last couple of days, which - together with huge SLV volume, and this ETF’s inflows - confirms the dramatic increase in interest in this particular market. This is exactly what happens close to market tops: silver steals the spotlight while mining stocks are weak. I’ve seen this countless times, and in most cases, it was accompanied by multiple voices of people “feeling” that the silver market is about to explode. For example, please consider what happened in early September 2020 on both (above and below) charts. Silver jumped and almost reached its August 2020 high, while the GDX was unable to rally even to (let alone above) its mid-August high.

Don’t get me wrong, I think that silver will soar in the following years and I’m not shorting silver (nor am I suggesting this) right now and in fact I haven’t been on the short side of the silver market for months. In fact, I expect silver to outperform gold in the final part of the next massive upswing, but… I don’t think this massive upswing has started yet.

Gold had it’s nice post-Covid panic run-up, but it didn’t manage to hold its breakout above the 2011 highs, despite multiple dovish pledges from the Fed, the open-ended QE, and ridiculously low interest rates. Plus, while gold moved above its 2011 highs, gold stocks have barely corrected half of their decline from their 2011 highs. Compare that to when the true bull market started about two decades ago – gold miners were soaring and multiplying gold’s gains in the medium run.

Let’s take a look at mining stocks, using the GDX ETF as a proxy for them.

Figure 2 – VanEck Vectors Gold Miners ETF (GDX)

Are miners weak right now? Of course, they are weak. It was not only silver that got attention recently, but also silver stocks. The GDX ETF is mostly based on gold stocks, but still, silver miners’ performance still affects it. And… GDX is still trading relatively close to the yearly lows. Silver moved a bit above its 2020 highs – did miners do that as well? Absolutely not, they were only able to trigger a tiny move higher.

And based on yesterday’s decline, most of the recent run-up was already erased.

Interestingly, the most recent move higher only made the similarity of this shoulder portion of the bearish head-and-shoulders pattern to the left shoulder (figure 2 - both marked with green) bigger. This means that when the GDX breaks below the neck level of the pattern in a decisive way, the implications are likely to be extremely bearish for the next several weeks or months.

Due to the uncanny similarity between the two green rectangles, I decided to check what happens if this mirror-similarity continues. I used purple, dashed lines for that. There were two important short-term price swings in April 2020 – one shows the size of the correction and one is a near-vertical move higher.

Copying these price moves (purple lines) to the current situation, we get a scenario in which GDX (mining stocks) moves to about $31 and then comes back up to about $34. This would be in perfect tune with what I wrote previously. After breaking below the head-and-shoulders pattern, gold miners would then be likely to verify this breakdown by moving back up to the neck level of the pattern. Then, we would likely see another powerful slide – perhaps to at least $24.

All in all, it seems that silver’s run-up was just a temporary phenomenon and the next big medium-term move in the precious metals and mining stocks is going to be to the downside.

Having said that, let’s take a look at the markets from the fundamental point of view.

EUR-on to Something

For weeks, I’ve been warning that the fundamental disconnect between the U.S. and Eurozone economies could pressure the EUR/USD.

And on Jan. 29, I wrote:

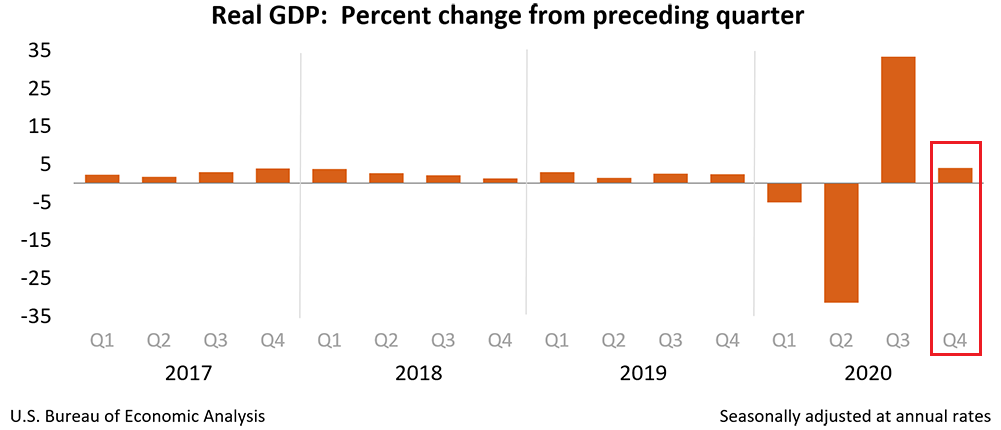

The economic divergence between Europe and the U.S. continues to widen. On Jan. 28, the U.S. Bureau of Labor Statistics (BLS) revealed that U.S. GDP (advanced estimate) likely expanded by 4.0% in the fourth-quarter.

Figure 3

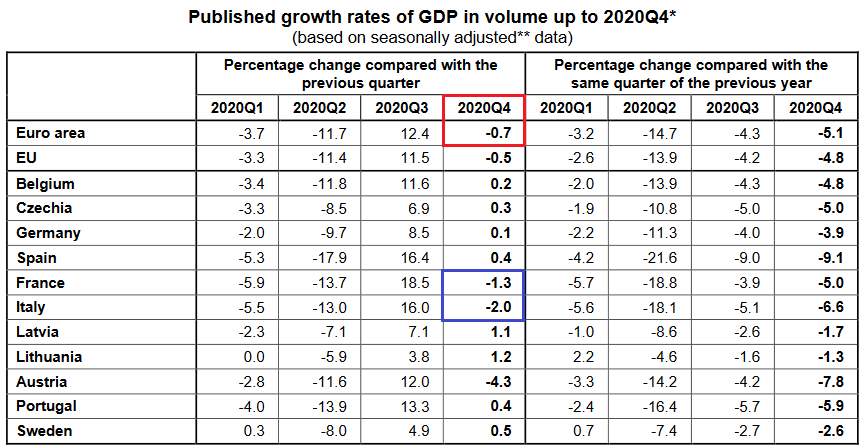

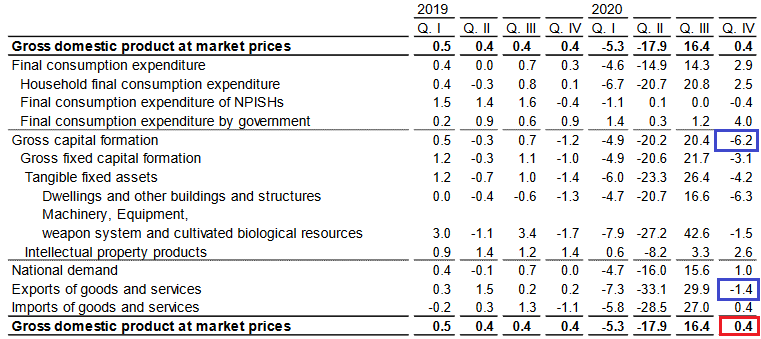

Making its counter move, Eurozone fourth-quarter GDP was released on Feb. 2, revealing that the European economy shrank by 0.7% (the red box below). Even more revealing, France and Italy – Europe’s second and third-largest economies – underperformed the bloc average, contracting by 1.3% and 2.0% respectively (the blue box below).

Figure 4 - Source: Eurostat

In addition, German retail sales (released on Feb. 1) declined by 9.6% in December – well below the 2.6% contraction expected by economists. And why is this relevant? Because the month-over-month decline was the largest since 1956 and speaks volumes coming from Europe’s largest economy.

Please see below:

Figure 5

If that wasn’t enough, Spain’s (Europe’s fourth-largest economy) Q4 GDP inched up by only 0.40% (the red box below). And not only did the figure come in well below the Spanish government’s December estimate (of an increase of 2.40%), the country’s exports declined by 1.4%, while business investment plunged by 6.2% (the blue boxes below).

Figure 6 - Source: Instituto Nacional de Estadística (Spain’s National Statistics Institute)

Moreover, as the fiscal situation worsens across Europe’s four-largest economies, the European Central Bank (ECB) has no choice but to pick up the slack. As of Feb. 2, the ECB’s balance sheet now totals more than 70% of Eurozone GDP (up from 69%). More importantly though, the figure is more than double the U.S. Federal Reserve’s (FED) 34.5% (down from 35%).

Please see below:

Figure 7

Thus, while the ECB’s money printer works overtime relative to the FED’s, the dominoes are lining up for a material fall:

- The ECB’s relative outprinting causes the FED/ECB ratio to decline

- A declining FED/ECB ratio causes the EUR/USD to decline

- A declining EUR/USD causes the precious metals to decline

To explain, please see below:

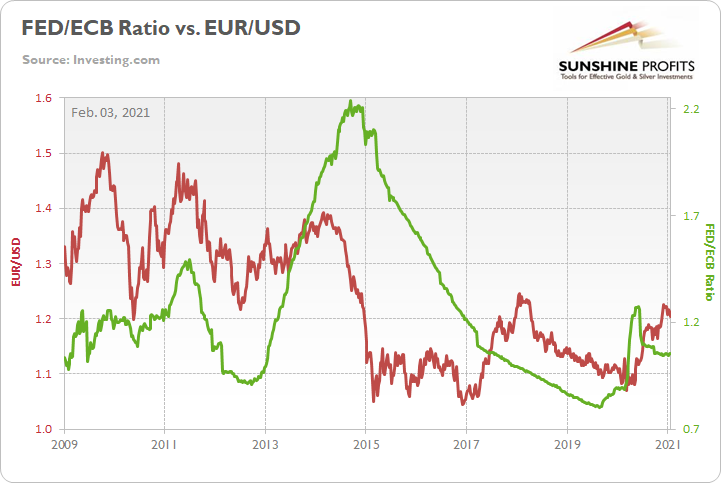

Figure 8

The red line above depicts the movement of the EUR/USD, while the green line above depicts the FED/ECB ratio. As you can see, when the green line rises (the FED is outprinting the ECB), the EUR/USD also tends to rise. Conversely, when the green line falls (the ECB is outprinting the FED), the EUR/USD tends to fall.

As it stands today, the FED/ECB ratio has declined by 0.26% week-over-week and is down by nearly 18% since June. And if you analyze the right side of the chart, you can see that the EUR/USD is starting to notice. As the FED/ECB ratio tracks lower, the EUR/USD is starting to roll over. And if history is any indication, the EUR/USD has plenty of catching up to do.

Also signaling a profound EUR/USD decline, I warned on Jan. 27 that the EUR/GBP could be the canary in the coal mine.

On Monday (Jan. 25), I wrote that Janet Yellen’s pledge to “act big” on the next coronavirus relief package ushered the EUR/GBP back above critical support.

However, on Tuesday (Jan. 26), the key level broke again.

Please see below:

Figure 9

More importantly though, a break in the EUR/GBP could be an early warning sign of a forthcoming break in the EUR/USD.

Figure 10

If you analyze the chart above, ~20 years of history shows that the EUR/GBP and the EUR/USD tend to follow in each other’s footsteps. As a result, if the EUR/GBP retests its April low (the next support level), the EUR/USD is likely to tag along for the ride (which implies a move back to ~1.08).

As it stands today, the wheels are already in motion. On Feb. 2, the EUR/GBP made another fresh low and the initial support level is all but gone.

Figure 11

Furthermore, notice how the EUR/USD is tracking the EUR/GBP lower? Despite being a fair distance from the ~1.08 level, the euro’s weakness relative to sterling is a sign that the Eurozone calamity is finally starting to weigh on its currency.

If you analyze the chart below, you can see that the EUR/USD has already broken below its December and January support.

Figure 12

More importantly though, we could be approaching a point of no return.

Figure 13

Barely breaking out of a roughly 12-year downtrend, the EUR/USD has yet to invalidate the declining long-term resistance line. As a result, and with the EUR/USD already rolling over, a break below the 1.16/1.17 level puts ~1.08 well within the range of the 2015/2016 lows.

And how could this affect the PMs?

Well, notice how they like to tag along for the EUR/USD’s ride?

Figure 14

Despite silver’s short squeeze providing a short-term reprieve, it’s no surprise that the EUR/USD’s weakness has been met with angst by the PMs.

Please see below:

Figure 15

As a result, the floundering euro is ushering the PMs down a one-way street. And while they may veer off to view the scenery from time to time, they all remain on a path to lower prices. Thus, yesterday’s sell-off highlights the superficiality of Monday’s (Feb. 1) surge. But while finding a true bottom requires time and patience, once it occurs, the PMs long-term uptrend will resume once again.

Thank you for reading our free analysis today. Please note that the above is just a small fraction of the full analyses that our subscribers enjoy on a regular basis. They include multiple premium details such as the interim targets for gold and mining stocks that could be reached in the next few weeks. We invite you to subscribe now and read today’s issue right away.

Sincerely,

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Gold Investment News

Delivered To Your Inbox

Free Of Charge

Bonus: A week of free access to Gold & Silver StockPickers.

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM