-

Powell Didn’t Come to Gold’s Rescue – What Now?

June 24, 2021, 10:25 AMPowell’s testimony to Congress failed in generating a rebound in gold prices; thus, the bearish trend could continue.

On Tuesday (June 22) the Fed Chair testified before the Select Subcommittee on the Coronavirus Crisis, U.S. House of Representatives. Before Powell’s appearance in Congress, there were some hopes that he would soften the Fed’s hawkish signals from the previous week. However, these hopes only partially materialized.

This is because Powell’s testimony was basically a confirmation of the last FOMC meeting. In particular, he reiterated the view that higher inflation would be transitory, as “a substantial part or perhaps all of the overshoot in inflation are from categories directly affected by reopening.”

Actually, some of his remarks were quite hawkish, as he said that the price pressures “don't speak to a broadly tight economy, but these effects have been larger and may persist longer than expected”. The admission that strong inflationary pressure could last longer than expected suggests that Powell is more worried about inflation than several months ago. He even explicitly admitted that “5% inflation is not acceptable.”

Luckily for the gold bulls, there were also some dovish comments. In particular, Powell said that the Fed wouldn’t hike the federal funds rates too quickly based only on inflationary worries:

We will not raise interest rates preemptively because we fear the possible onset of inflation. We will wait for evidence of actual inflation or other imbalances.

Of course, it doesn’t make any sense, as actual inflation is already 5%, more than twice the target, and the Fed hasn’t reacted. The US central bank remains passive because it believes that inflation will prove to be transitory. However, it means that it actually acts based on expectations, not the current data, contrary to what the Fed is saying when justifying its ultra-dovish stance.

And Atlanta Fed President Raphael Bostic also sent some dovish signals in an interview with National Public Radio’s Morning Edition he gave the next day after Powell’s testimony. He adhered to the view about temporary inflation, but he explained that the time horizon of this temporariness would be longer than previously thought:

The recent jump in prices will prove temporary, but "temporary is going to be a little longer than we expected initially... Rather than it being two to three months it may be six to nine months.

However, Bostic didn’t mention the necessity to hike in the face of prolonged high inflation. On the contrary, he pointed out that the Fed shouldn’t announce the victory in the jobs battle too quickly: “We have to make sure our policies don't pivot in ways that make it look like we are declaring victory prematurely.”

Implications for Gold

What does all this mean for the yellow metal? Well, theoretically, more lasting high inflation with unchanged dovish stance of the US central bank should be positive for gold prices, as an unresponsive Fed implies lower real interest rates, which usually support the yellow metal.

However, gold hardly reacted to either Powell’s or Bostic’s comments. As the chart below shows, contrary to some hopes, Powell’s testimony failed in sending strong dovish signals that would be able to overwrite the hawkish turmoil triggered by the recent dot-plot. So, there was no rebound in gold prices. Instead, the price of the yellow metal merely stabilized at about $1,775.

The lack of any rebound is a bad sign, indicating gold’s weakness (especially given that some other assets rebounded a bit this week after the post-FOMC turmoil ). This suggests that gold prices have room for further declines. It seems that gold would need a very dovish surprise from the Fed to go the other way, which is not likely without some kind of economic crisis or at least an influx of significantly negative economic data.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Will Gold Survive Hawkish Fed?

June 22, 2021, 9:33 AMThe recent Fed’s hawkish turn is fundamentally negative for gold prices but there is still some hope.

The hawkish counter-revolution within the Fed continues. On Friday, St. Louis Fed President James Bullard said that the recent FOMC shift towards a faster tightening of monetary policy was a natural response to faster economic growth and higher inflation than anticipated:

We were expecting a good year, a good reopening, but this is a bigger year than we were expecting, more inflation than we were expecting, and I think it's natural that we've tilted a little bit more hawkish here to contain inflationary pressures.

Bullard also noted that “Powell officially opened the taper discussion this week”. Indeed, in my Friday edition of the Fundamental Gold Report, I focused on the changed dot-plot, which suggested that FOMC members were ready to hike interest rates twice in 2023. However, the second major shift in the stance of the US central bank was that the Fed officials started to “talk about talking about” tapering.

In his prepared remarks for the press conference, Powell said:

At our meeting that concluded earlier today, the Committee had a discussion on the progress made toward our goals since the Committee adopted its asset purchase guidance last December. While reaching the standard of “substantial further progress” is still a way off, participants expect that progress will continue. In coming meetings, the Committee will continue to assess the economy’s progress toward our goals. As we have said, we will provide advance notice before announcing any decision to make changes to our purchases.

In plain English, it means that the Fed could announce tapering at any of its future meetings, depending on the assessment of the incoming data. However, to avoid a replay of the taper tantrum, the Fed will “give advance notice before announcing any decision”. So, September is the first probable date of a hawkish announcement about tapering of quantitative easing, which could be preceded by some clues as early as in July:

That is, you know, the process that we're beginning now at the next meeting. We will begin, meeting by meeting, to assess that progress and talk about what we think we're seeing, and just do all of the things that you do to sort of clarify your thinking around the process of deciding whether and how to adjust the pace and composition of asset purchases.

Another hawkish shift in the Fed’s thinking, which is worth pointing out, is that it dropped the phrase in the statement saying that the pandemic is weighing on the economy. So, although it’s still cited as a risk, Powell and his colleagues officially ceased to see the pandemic as a constraint on economic activity. It means that, as I already wrote earlier in my reports, the US economy has returned to the pre-epidemic level or has shifted from the recovery to the expansion phase.

Implications for Gold

What does it all mean for the yellow metal? Well, the Fed triggered some panic selling in the gold market last week. Actually, on Thursday, there was the largest one-drop of 2021 in response to the more hawkish stance of the US central bank, as the chart below shows.

The bearish reaction is understandable, as the Fed’s readiness to reduce its asset purchases and end the policy of zero interest rates is fundamentally negative for the yellow metal. More hawkish FOMC implies higher real interest rates and a stronger dollar, the two most important drivers of gold prices. Furthermore, when the US central bank becomes more hawkish, it means that it’s more confident in the economy – and gold struggles when the economy is strong.

However, some analysts claim that the selloff was exaggerated. After all, the Fed still maintains that higher inflation is transitory; but transitory inflation doesn’t mix with earlier interest rate hikes. So, we will have either more lasting high inflation (but the Fed is slow to admit it), or the Fed doesn’t really want to increase its interest rates substantially. In both cases, gold should benefit, either from higher inflation and lower real interest rates, or from more dovish Fed than it’s currently perceived.

So, the bullish case for gold is not dead yet, but if the Fed really becomes more hawkish and determined to tighten its monetary policy (while high inflation turns out to be transitory), gold may struggle during the upcoming tightening cycle, unless it triggers some economic turmoil.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

FOMC Sees Two Rate Hikes in 2023. Gold Didn’t Like It!

June 18, 2021, 11:19 AMThe newest Fed’s statement and dot-plot indicated a much more hawkish tone among the FOMC members than the markets expected, and gold dropped.

On Wednesday (June 16, 2021), the FOMC has published its newest statement on monetary policy. The statement was barely changed. The main alteration is that the Fed has ceased saying that “the pandemic is causing tremendous human and economic hardship across the United States and around the world”. Furthermore, with the CPI annual rate jumping to 5% in May, the US central bank acknowledged that inflation is not any longer “running persistently below this longer-run goal”. Hence, both modifications are slightly hawkish, as the Fed noticed an improvement in the epidemiological situation, as well as higher inflation. Bad news for gold.

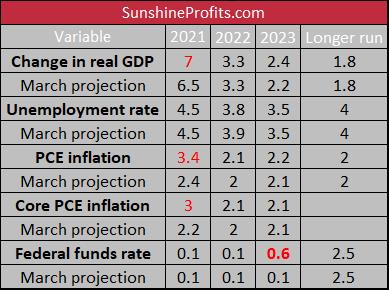

However, the statement was only slightly changed, so the investors focused more on the accompanying dot-plot and Powell’s press conference instead. According to the fresh economic projections, the Fed forecasts higher GDP growth and higher inflation this year, as the table below shows.

As one can see, the FOMC expects that the GDP will soar 7% in 2021, compared to a 6.5% rise expected in March. They also assume that the pace of economic growth will be slightly higher in 2023. Meanwhile, the Fed officials believe now that the PCE inflation (core PCE) will jump to 3.4% (3%) this year, compared to 2.4% (2.2%) seen in March. They also forecast a slightly lower unemployment rate in 2022.

But the most impactful change occurred in the expected path of the federal funds rate. The FOMC members now forecast that the US policy rate will be 0.6% at the end of 2023, an important upward change from 0.1% projected in March. In other words, the US central bankers believe that two interest rate hikes will be appropriate in 2023. It means that they started to think about tapering, which is fundamentally negative for gold prices.

Indeed, Powell said during his post-meeting press conference that we can “think of this meeting that we had as the talking about talking about meeting [at which the Fed will start tapering], if you like”.

Implications for Gold

What does the recent FOMC meeting imply for the gold market? Well, the Fed struck again. As a result, the price of gold plunged. As the chart below shows, the London P.M. Fix slid from about $1,865 on Tuesday to $1779 on Thursday.

The reason is simple: the fresh dot-plot shows that a majority of the Fed officials currently forecasts two quarter-point rate hikes in 2023. 13 of 18 FOMC members see some interest rate increases in 2023 compared to just 7 members in March. Moreover, 7 participants now predict some upward moves next year. These changes lifted market expectations of future interest rates. In consequence, the bond yields increased, which raised the opportunity costs of holding non-yielding bullion. Furthermore, the more hawkish stance of the Fed strengthened the US dollar, creating downward pressure on gold prices. In other words, the new economic outlook revealed some hawks among the FOMC members and that there might be less tolerance toward higher inflation than previously thought.

However, the bullish case for gold is not over yet. After all, the Fed maintained its very accommodative monetary policy, and it will not hike interest rates this year and probably not also in 2022. Additionally, the dot-plot is not the official projection of the future path of the federal funds rate, so it should be taken with a grain of salt. A lot may happen by 2023. Also, the Fed leadership seems to be more dovish than many of the regional Fed presidents.

Last of all, Powell repeated that inflation is merely transitory. But why hike interest rates if inflation is merely transitory and federal debt is ballooning? Hence, it might be the case that the Fed is testing the markets. High inflation is still with us, and it may be more lasting than the Fed believes. Even with two interest rate hikes, the real interest rates should stay negative.

Having said that, the hawkish Fed’s statement and hawkish economic projections are fundamentally negative for the yellow metal in the medium term. The chances of a replay of 2013 have increased. It seems that gold may struggle without an inflationary turmoil, stagflation, the dovish counter-strike at the Fed, or a debt crisis.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Inflation Soars 5%! Will Gold Skyrocket?

June 15, 2021, 9:29 AMWith the CPI annual inflation rate spiking 5% in May, gold could have gained a lot in response. However, it rallied only $20. Should we prepare for more?

Whoa! Inflation soared 5% in May – quite a lot for a nonexistent (or transitory) phenomenon! But let’s start from the beginning. The CPI rose 0.6% in May, after increasing 0.8% in April. Meanwhile, the core CPI, which excludes food and energy, soared 0.7%, following a 0.9% jump in April. So, given that the pace of the monthly inflation rate decelerated, we shouldn’t worry about inflation, right? Well… we should.

First of all, inflation was higher than expected, as the consensus forecast was a 0.4% increase. Inflation surprised pundits once again, but not me. Last month, I wrote in the Fundamental Gold Report that “Inflation escalated in April. In May, however, inflation could be softer, but it will remain relatively elevated, in my view” – and this is exactly what happened. However, the unexpected rise in inflation is positive news for gold, as such a surprise should decrease the real interest rates.

Second, pundits cannot blame energy prices for this jump, as the energy index was flat. Apart from energy and medical care services, which decreased slightly, all index components increased last month. In particular, the index for used cars and trucks soared again (7.3%). Also, the indexes for new vehicles and apparel surged in May, which shows that inflationary pressure is broad-based.

Last but definitely not least, the latest BLS report on inflation reveals that the overall CPI skyrocketed 5% for the 12 months ending May (before seasonal adjustment), followed by a 4.2% spike in April. For context, the annual inflation rate has been trending up every month since January, when the 12-month change was just 1.4%. Therefore, we’ve just seen the largest move since a 5.4% jump for the period ending in August 2008, just one month before the bankruptcy of Lehman Brothers that triggered the global financial crisis and deflationary Great Recession.

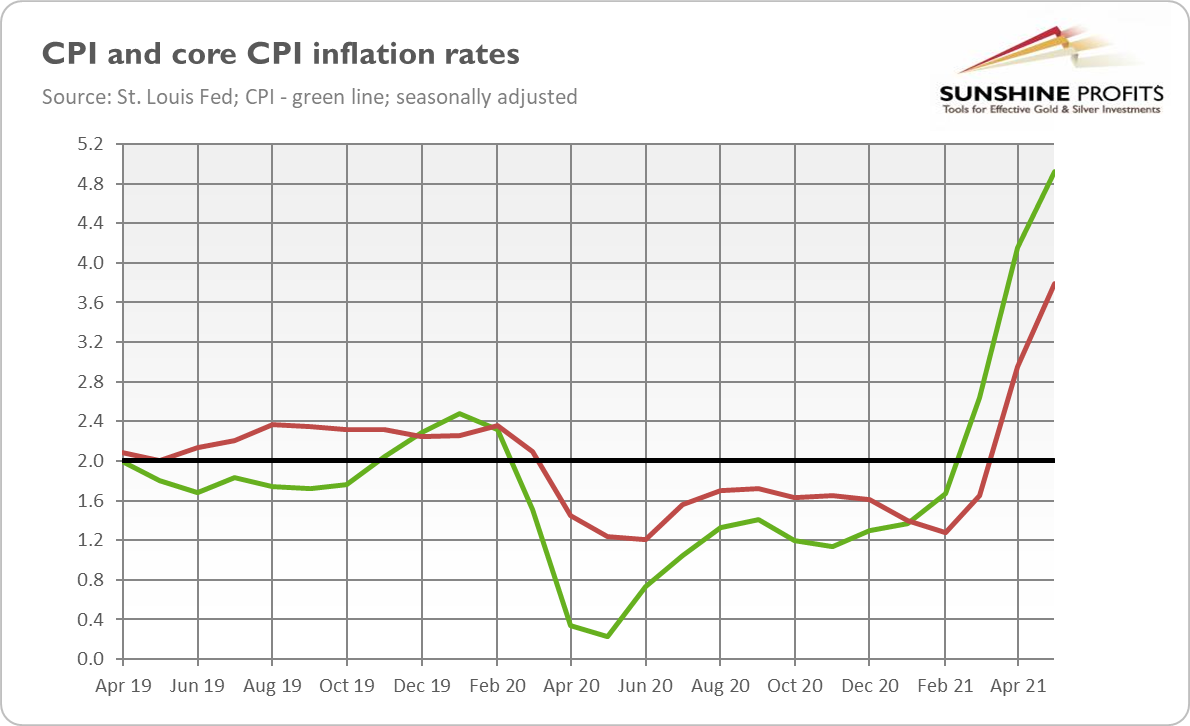

But that’s not all! The annual core CPI rate soared 3.8% last month after rising 3% in April, as the chart below shows. It was the fastest pace since June 1992. So, the Fed cannot by any manner of means blame higher inflation on food or energy prices.

Supply disruptions are not a credible explanation either, as the inflation acceleration is broad-based. How likely would it be, that the production of virtually all goods and services would face supply bottlenecks at the same time and extent? Indeed, a significant boost in the broad money supply is a much more convenient explanation for widespread price increases.

Implications for Gold

What does accelerating inflation imply for the gold market? Well, on the one hand, higher inflation should be positive for the yellow metal, as it means a stronger demand for gold as an inflation hedge. Additionally, higher inflation could lower the real interest rates, also supporting gold prices. And indeed, the price of gold has risen from about $1,870 to $1,890 in a response to the inflation spike.

On the other hand, some analysts point out that stronger inflation could be rather negative for the yellow metal, as the Fed would have to tighten its monetary policy, taper its quantitative easing and hike the federal funds rate to contain inflation. After all, the overall CPI annual rate is more than twice as high as the Fed’s target. Moreover, the mediocre gold’s reaction to the surge in inflation suggests that investors are worried about a normalization of the ultra-dovish monetary policy.

However, the Fed has recently become more tolerant of higher inflation, and Powell is likely to continue claiming that inflation is merely transitory. Also, on Thursday, the European Central Bank held its regular monetary policy meeting and maintained its elevated flow of stimulus, even though recovery takes hold. And the Fed may do the same, i.e., nothing, tomorrow.

Nevertheless, the relaxed stance of the ECB and the Fed could come out as incorrect. We have the economy operating above potential, with big fiscal injections along with a very easy monetary policy. Such a combination could bring us to an environment of higher and more lasting inflation, which could disrupt the market later in the future.

After all, many indicators suggest that financial markets believe in the narrative of “transitory” inflation. But if inflation proves to be more permanent than expected, there could be some turmoil in the markets – and gold could benefit from it. Gold is not always a good inflation hedge, and it could suffer somewhat if the nominal interest rates increase; however, it should prosper if the real interest rates decline further.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Will Gold Rally Continue in the Upcoming Months?

June 10, 2021, 8:52 AMMay was certainly a positive month for the yellow metal. Gold could keep its momentum later this year, but a lot depends on the Fed and inflation.

We left May in the rearview mirror, and as the chart below shows, it was the second positive month in a row for the yellow metal. Gold rose 7% last month – this is 12.3% since the local bottom on March 31, 2021. The jump was driven mainly by inflation fears, a weak greenback and a decrease in real interest rates.

Hence, I was right: the second quarter has been so far much better for the shiny metal than the first one, in which it declined by 11%. Gold even jumped temporarily above $1,900 at the turn of May and June. Since then, it has been fluctuating around this level. All this means that the yellow metal fully recovered its Q1 losses, finishing last month virtually flat year-to-date.

Now, the key question is: what’s next for gold? Outlooks are, as always, divided. Some analysts point out that gold’s struggle to move decisively north above $1,900 amid all the increase in the money supply, public debt and inflation is disturbing and has bearish implications for the future. For instance, the French bank Société Générale still believes that we will see $2,000 per ounce by the end of the year, but its conviction towards this forecast has weakened. I have to admit – the lack of a stronger rally in gold is something I also worry about.

But on the other hand, some believe that gold is still in a long-term bull trend. For instance, the World Gold Council, in its latest Gold Market Commentary, points out that sentiment towards gold became more bullish in May, as net positioning on COMEX futures rose to its highest level since February. Moreover, not only gold ETFs recorded their first monthly inflows since January 2021, but also the highest ones since September 2020.

Furthermore, the WGC’s 2021 Central Bank Gold Reserves Survey reveals a slightly stronger conviction towards gold, as there is a growing recognition among central banks of gold’s performance during periods of economic crises. The report notes that 21% of central banks expect to increase their gold reserves within the next year (value relatively unchanged from last year’s survey) and that no central bank expects to sell gold this year – down from 4% in 2020.

Also, Commerzbank remains bullish on gold despite recent volatility. Although the German bank expects that the Fed will start tapering its quantitative easing by the fourth quarter, it’s forecasting rising inflation. As a result, nominal interest rates will stay below the inflation rate leaving real bond yields significantly below zero.

Implications for Gold

What does all this imply for the gold market? Well, there are both downside and upside risks for gold in the future. Possible drawbacks are the unwinding of the Fed’s bond-buying program and the new tightening cycle. Strengthening expectations of asset purchases tapering and normalization of the ultra-dovish monetary policy could trigger an increase in the interest rates and outflows from the gold market.

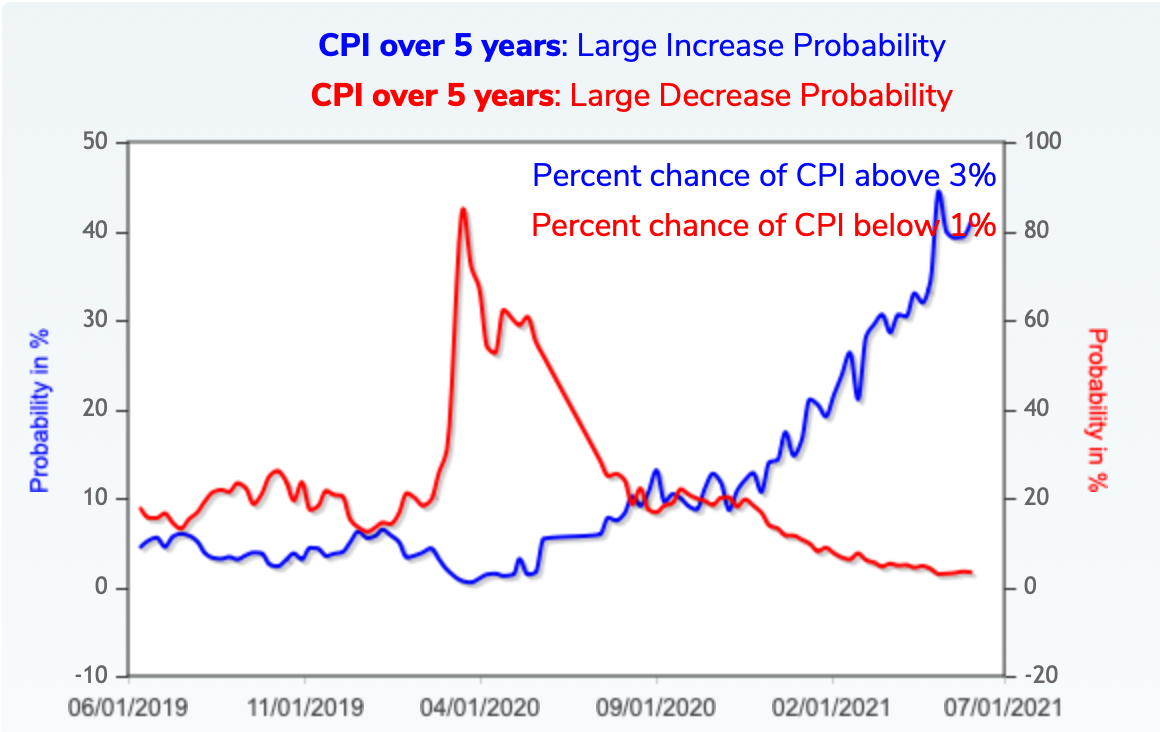

To the other group of factors, I would include higher inflation. After all, we have never seen such coexistence of dovish monetary policy and easy fiscal policy. Not surprisingly, investors started to worry about record-breaking inflation. As the chart below shows, market-based probabilities derived from options (calculated by the Minneapolis Fed, which computes probabilities from option prices) show that the previous expectations of the CPI annual rate above 3% over five years have significantly increased recently. Higher inflation would increase demand for gold as an inflation hedge and decrease real interest rates, supporting gold prices.

So, gold’s future depends on the Fed’s reaction to rising inflation, or whether or not investors will focus on nominal and real interest rates. If the US central bank stays behind the inflation curve, real interest rates will stay in the negative territory, supporting the price of gold. However, if the Fed tightens its monetary policy decisively, or if investors focus on rising nominal bond yields in a response to inflation, the yellow metal may go down.

To that point, the most recent changes in the Fed’s framework, comments from the FOMC members and disappointing data about the US labor market suggest that we are far away from any serious tightening. So, gold has room for moving higher.

Having said that, it seems that gold needs more negative events (or even a kind of financial crisis) to rally decisively further. So far, the US economy remains in the boom phase and higher inflation doesn’t seem to significantly disrupt the functioning of the markets. Perhaps gold bulls will have to wait a bit longer until we move from reflation to stagflation. Today’s report on inflation and upcoming FOMC meeting could provide more clues about gold’s future – stay tuned!

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

Gold Reports

Free Limited Version

Sign up to our daily gold mailing list and get bonus

7 days of premium Gold Alerts!

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM