-

Gold Approaches $1,900 amid FOMC Minutes and Crypto Sell-Off

May 20, 2021, 10:05 AMThe latest FOMC minutes were dovish, especially in light of the recent increase in inflation and elevated asset valuations. What does it mean for gold?

Yesterday, the FOMC published minutes from its last meeting in April. They’ve shown two things doing that: first, that some of the central bankers are worried about the inflation and elevated asset valuations; and, second, that the Fed is going to remain dovish despite all these concerns.

Indeed, some FOMC participants noted that the demand for labor had started to put some upward pressure on wages. Moreover, a number of them pointed out the protracted supply disruptions and the insufficient pre-emptive hawkish reaction from the Fed as potentially inflationary factors:

A number of participants remarked that supply chain bottlenecks and input shortages may not be resolved quickly and, if so, these factors could put upward pressure on prices beyond this year. They noted that in some industries, supply chain disruptions appeared to be more persistent than originally anticipated and reportedly had led to higher input costs. (…)

A couple of participants commented on the risks of inflation pressures building up to unwelcome levels before they become sufficiently evident to induce a policy reaction.

When it comes to financial stability and asset valuations, several FOMC members pointed out elevated risk appetite and very low credit spreads. And certain participants noted dangers related to the low interest rates and excessive risk-taking: if the risk appetite fades, the asset prices could decline with potentially harmful consequences for the financial sector and the economy:

Regarding asset valuations, several participants noted that risk appetite in capital markets was elevated, as equity valuations had risen further, IPO activity remained high, and risk spreads on corporate bonds were at the bottom of their historical distribution. A couple of participants remarked that, should investor risk appetite fall, an associated drop in asset prices coupled with high business and financial leverage could have adverse implications for the real economy. A number of participants commented on valuation pressures being somewhat elevated in the housing market. Some participants mentioned the potential risks to the financial system stemming from the activities of hedge funds and other leveraged investors, commenting on the limited visibility into the activities of these entities or on the prudential risk-management practices of dealers’ prime-brokerage businesses. Some participants highlighted potential vulnerabilities in other parts of the financial system, including run-prone investment funds in short-term funding and credit markets. Various participants commented on the prolonged period of low interest rates and highly accommodative financial market conditions and the possibility for these conditions to lead to reach-for-yield behavior that could raise financial stability risks.

So, given all these concerns about financial stability and higher inflation, the Fed should send some hawkish signals, right? Not at all! On the contrary, the US central bank reiterated its ultra-dovish stance, justifying that the economy was far from achieving full employment.

Participants commented on the continued improvement in labor market conditions in recent months. Job gains in the March employment report were strong, and the unemployment rate fell to 6.0 percent. Even so, participants judged that the economy was far from achieving the Committee's broad-based and inclusive maximum-employment goal. Payroll employment was 8.4 million jobs below its pre-pandemic level. Some participants noted that the labor market recovery continued to be uneven across demographic and income groups and across sectors.

After all, higher inflation would only be transitory, and when these short-term factors fade, inflation will decrease:

In their comments about inflation, participants anticipated that inflation as measured by the 12-month change of the PCE price index would move above 2 percent in the near term as very low readings from early in the pandemic fall out of the calculation. In addition, increases in oil prices were expected to pass through to consumer energy prices. Participants also noted that the expected surge in demand as the economy reopens further, along with some transitory supply chain bottlenecks, would contribute to PCE price inflation temporarily running somewhat above 2 percent. After the transitory effects of these factors fade, participants generally expected measured inflation to ease. Looking further ahead, participants expected inflation to be at levels consistent with achieving the Committee's objectives over time (…) Despite the expected short-run fluctuations in measured inflation, many participants commented that various measures of longer-term inflation expectations remained well anchored at levels broadly consistent with achieving the Committee's longer-run goals.

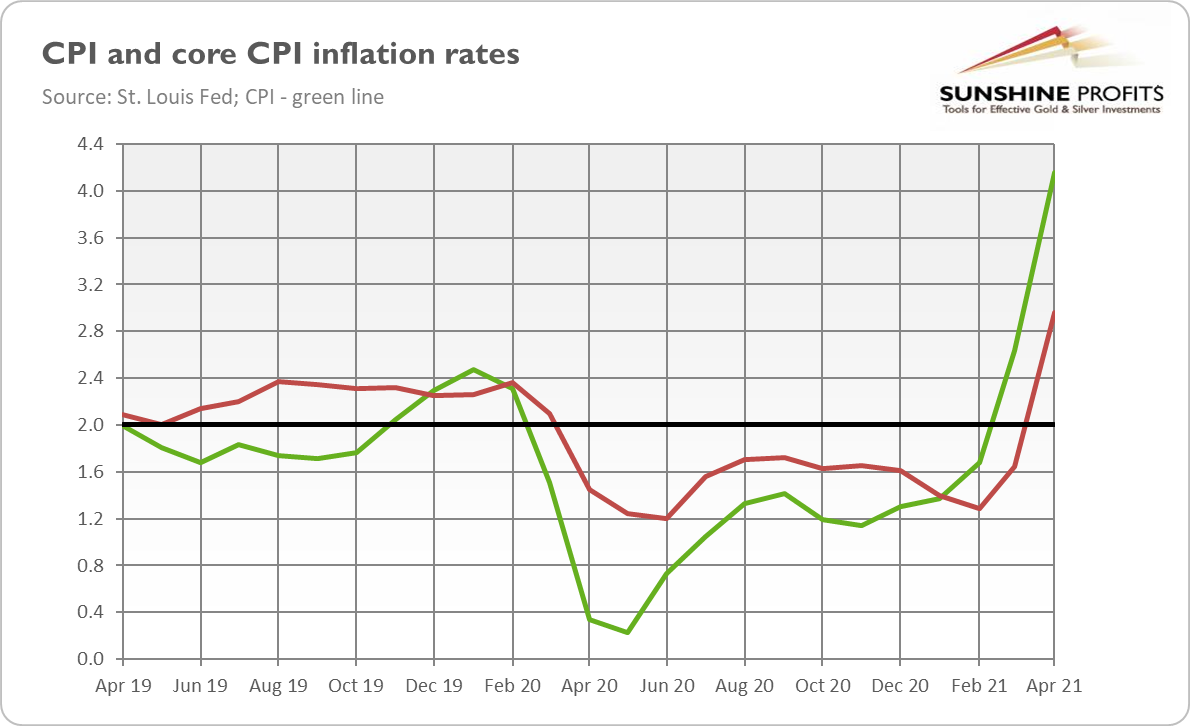

Yeah, sure, but why should we believe the Fed if they were surprised by the CPI readings in April? They anticipated inflation moving above 2 percent, and meanwhile the CPI inflation surged above 4 percent as the chart below shows!

But at least inflation expectations remain well-anchored, don’t they? Well, not exactly. As the chart below shows, the market-based expectations of inflation have significantly risen recently. Similarly, the University of Michigan’s index that measures inflation expectations for the next five years rose from 2.7 percent in April to 3.1 percent in May – it’s the highest level in a decade.

Interestingly, even the Fed staff doesn’t believe in transitory inflation. After all, they forecast that the actual GDP would be above its potential until 2022-2023:

With the boost to growth from continued reductions in social distancing assumed to fade after 2021, GDP growth was expected to step down in 2022 and 2023. However, with monetary policy assumed to remain highly accommodative, the staff continued to anticipate that real GDP growth would outpace that of potential over much of this period, leading to a decline in the unemployment rate to historically low levels.

Economics 101 teaches us that when the economy operates above its potential, it implies overheating and inflation that reflects more fundamental or lasting factors than base effects and short-term supply disruptions.

Implications for Gold

What do the recent FOMC minutes imply for gold? Well, the Fed remaining dovish despite all the inflationary risks and elevated asset valuations (many assets plunged yesterday, especially cryptocurrencies) is bullish for gold.

Sure, a few members became ready to start talking about tapering the quantitative easing and tightening the monetary policy:

A number of participants suggested that if the economy continued to make rapid progress toward the (policy-setting) Committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.

However, “a number” is not “the majority”, so we shouldn’t expect such a discussion in the mainstream anytime soon, especially in light of the disappointing April nonfarm payrolls and recent declines in the stock market.

The price of gold rose yesterday, approaching $1,900. It might have been due to the FOMC minutes, but also the sell-off in cryptocurrencies and the following outflow of money from them into old, good gold.

Given these shifts in the marketplace, it seems that Fed’s worries about fading risk appetite were justified. If risk appetite wanes further, gold should shine as a safe-haven asset.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Gold Rebounds After Fainting Due to Inflation Spike

May 18, 2021, 7:33 AMGold recovered after a downward response to the surge in inflation. What’s next for the yellow metal?

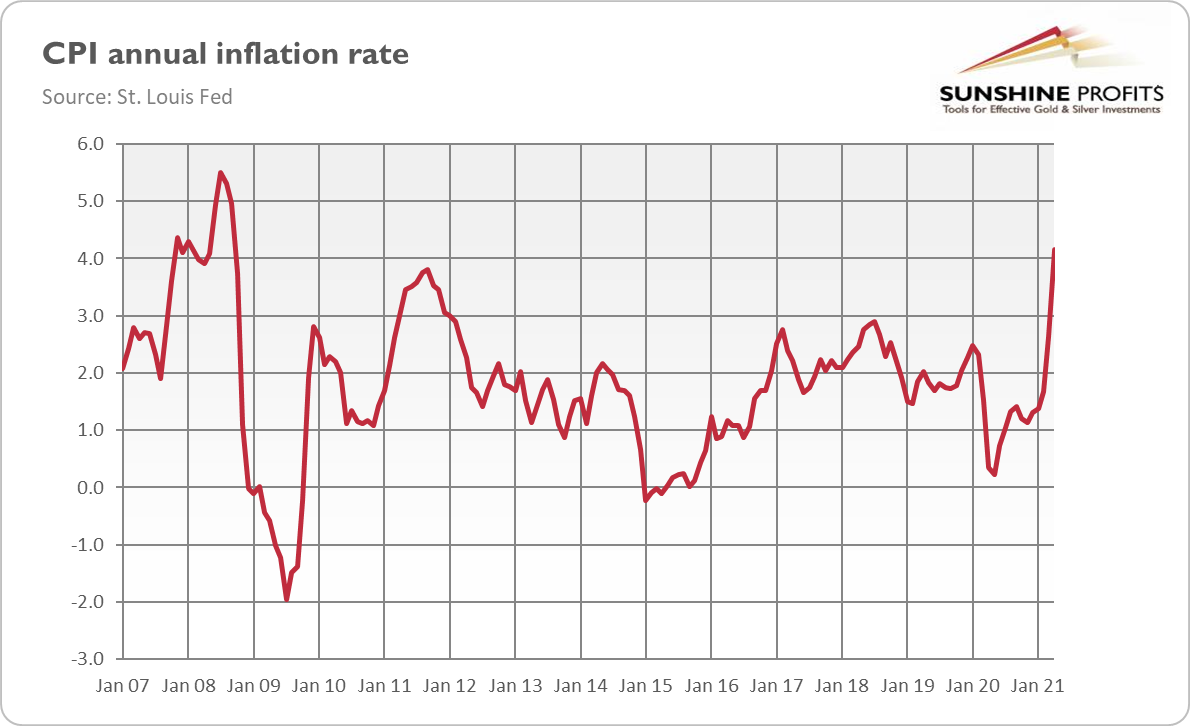

Gold rebounded after an initially bearish reaction to the BLS report showing that inflation soared 4.2% in April year-to-year. This means we have an inflation annual rate doubling the Fed’s target and the highest since the Great Recession as the chart below shows.

It might now seem counterintuitive, but traders worried that the jump in the CPI would force the Fed to tighten its monetary policy earlier than anticipated. However, it seems that the US central bank managed to convince the markets that it would remain dovish for a very long period and that April’s inflation reading wouldn’t accelerate the first hike of the federal funds rate.

Indeed, on Thursday, Federal Reserve Governor Christopher Waller said that the Fed would need “several more months of data” before considering modifications to its stance. He added “now is the time we need to be patient, steely-eyed central bankers, and not be head-faked by temporary data surprises.” So, don’t fight the Fed, interest rates will stay at zero for several months, thus supporting the yellow metal!

After all, the Fed’s narrative is that the current inflation is transitory. Of course, the April surge was partially caused by a 10% increase in the cost of new, as well as used cars and trucks – this accounted for a great part of the overall rise. Interestingly enough, the massive spike in car prices was in part generated by temporary supply-chain disruptions, i.e., the shortage of microchips used in automobile production.

However, one can almost always find an element without which inflation is smaller. But one can also almost always find an element without which inflation is higher. This is how the consumer baskets work: some goods are getting more expensive, others are getting cheaper, etc.

So, although May’s inflation reading will likely be smaller, inflation may be more lasting than many analysts believe. There are many arguments for this. First, the surge in the broad money supply. Second, rising producer prices in China, so there might be an import of inflation. Third, the realization of the pent-up demand. Fourth, the rising input prices and more room for passing them on consumers. Fifth, April’s sluggish job creation signals that wages will have to rise to entice people to return to work (all the recent unemployment benefits have made current wages less appealing). So, producers could try to pass these increases in wages on consumers, just as with rising input prices.

Implications for Gold

What does inflation imply for the gold market? Well, from the fundamental perspective, higher and more permanent inflation is positive for the yellow metal. Inflation lowers the real interest rates and the purchasing power of the greenback, supporting gold. Of course, the short-term relationship between inflation and gold is more complicated (and less bullish than in theory), especially when higher inflation translates into higher nominal bond yields and expectations of a more hawkish Fed.

However, gold is a proven long-term hedge against inflation, so “gold can be a valuable component of an inflation-hedging basket”, as the WGC’s Investment Update shows. What is important here is that the Fed has become more tolerant of higher inflation. Therefore, we will have an environment of higher inflation and dovish Fed behind the curve, which implies lower real interest rates and a weaker dollar.

Hence, gold should attract attention as a hedge against inflation – actually, it’s already happening, as market sentiment toward gold has recently improved, while outflows in gold ETFs have slowed. And, as the chart below shows, the price of gold has jumped this week above $1,850.

So, as I repeated several times earlier, although the threat of higher interest rates will remain, the second quarter of 2021 should be better than the first one, unless the Fed radically changes its stance.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Inflation Monster Rears Its Ugly Head. Will Gold Beat It?

May 13, 2021, 10:06 AMInflation surged 4.2% in April, but gold declined in response. What is happening?

Unbelievable! The “non-existent” inflation keeps getting stronger. The CPI increased 0.8% in April, after rising 0.6% in March. The pundits cannot blame energy prices for this jump, as the energy index decreased slightly. This shows that the surge in inflation wasn’t caused just by the base effect. Apart from energy, all major component indexes increased last month. In particular, the index for used cars and trucks rose 10.0%, which was the largest monthly increase since the series began in 1953.

As a result, the core CPI, which excludes food and energy, soared even stronger in April, i.e., 0.9%, following a 0.3% jump in March. It was the largest monthly increase since April 1982. But still, there is no inflationary pressure in the economy…

And now for the best part, the true crème de la crème of the recent BLS report on inflation: As the chart below shows, the overall CPI surged 4.2% over the 12 months ending in April, while the core CPI jumped 3.0%. These annual rates followed, respectively, 2.6% and 1.6% increases in March.

So, there was a huge acceleration in inflation last month! The last occurrence of such high inflation was in 2008 during the Great Recession. The quickening was a surprise for many analysts, but not for me. When analyzing the March CPI report, I wrote that it wasn’t an outlier:

What’s important is that the recent jump in inflation is not a one-off event. We can expect that high inflation will stay with us for some time, or it can accelerate further next month.

And indeed, inflation escalated in April. In May, however, inflation could be softer, but it will remain relatively elevated, in my view.

Implications for Gold

What does the hastening in inflation imply for the precious metals market? Well, the London P.M. Gold Fix has barely moved, as the chart below shows. What’s more, the New York spot gold prices have decreased in the aftermath of the April report on the CPI.

What happened? Shouldn’t gold have reacted more positively to the surprising speeding up of inflation? As an inflation hedge – it should. But this is far more complicated. First, the bond yields have increased to reflect higher inflation, as traders started to bet that the Fed would have to hike interest rates faster than previously expected.

But the April CPI report won’t force the U.S. central bank to alter its monetary policy and adopt a more hawkish line. After all, they expected acceleration in inflation, and they will simply describe it as a transitory development. As a reminder, the Fed focuses now more on the labor market than price stability – and with employment still more than 8 million short of the pre-pandemic level, the Fed will likely maintain its dovish stance.

Indeed, Fed Vice Chair Richard Clarida reiterated that the U.S. central bank is far away from tightening its monetary policy and confirmed that higher inflation than anticipated won’t alter the Fed’s course, as it would prove to be temporary:

The economy remains a long way from our goals, and it is likely to take some time for substantial further progress to be achieved (…) This is one data point, as was the labor report (...) We have been saying for some time that reopening the economy would put some upward pressure on prices.

What’s more, although traders focused initially on the implications of higher inflation on the federal funds rate and the U.S. monetary policy, in the longer-term gold should come into more favor as a hedge against higher inflation or even stagflation – after all, in April, we witnessed surprisingly disappointing nonfarm payrolls and a surge in inflation. Of course, single reports are not enough, but inflationary risks have definitely risen recently, and we could see some portfolio rebalancing toward gold later this year.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Gold Jumps above $1,800. What’s Next?

May 11, 2021, 10:27 AMGold jumped above $1,800, and it’s the disappointing jobs data that added fuel to the fire.

The gold market is a funny place. On Thursday (May 6), I complained that the yellow metal couldn’t surpass $1,800:

The price of gold has been trading sideways recently as it couldn’t break out of the $1,700-$1,800 price range. This inability can be frustrating, but the inflationary pressure could help the yellow metal to free itself from the shackles.

And voilà, just later that day, the price of gold finally jumped above $1,800, as the chart below shows. Hey, maybe I have to complain about gold more often?

But jokes aside. The move is a big deal, as gold has finally broken above the key resistance level. What’s important here is that the breakthrough wasn’t caused by some negative geopolitical or economic shock, but rather by fundamental and sentiment factors.

So, what happened? First, there is a weakness in the US dollar. With global economic recovery progressing, the safe-haven appeal of the greenback is simply vanishing. Another issue here is – and I pointed this out in the Fundamental Gold Report dedicated to the latest ECB’s meeting – that the pandemic in the Eurozone has reached its peak. So, the worst is already behind the euro area, and it can catch up with the US now, supporting the euro and gold against the dollar.

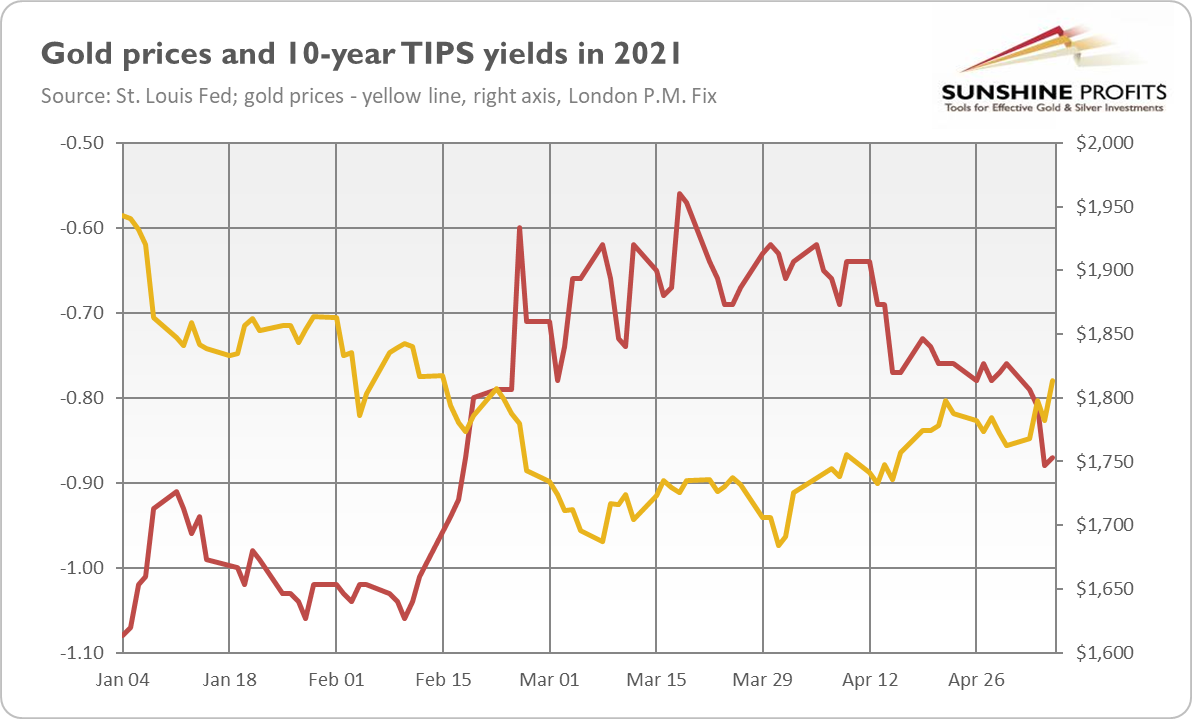

Second, the bond yields have been heading lower recently. As one can see in the chart below, the real interest rates have corrected significantly since their peak in March. In early May, the 10-year TIPS yields slid further, returning to almost -0.90 percent.

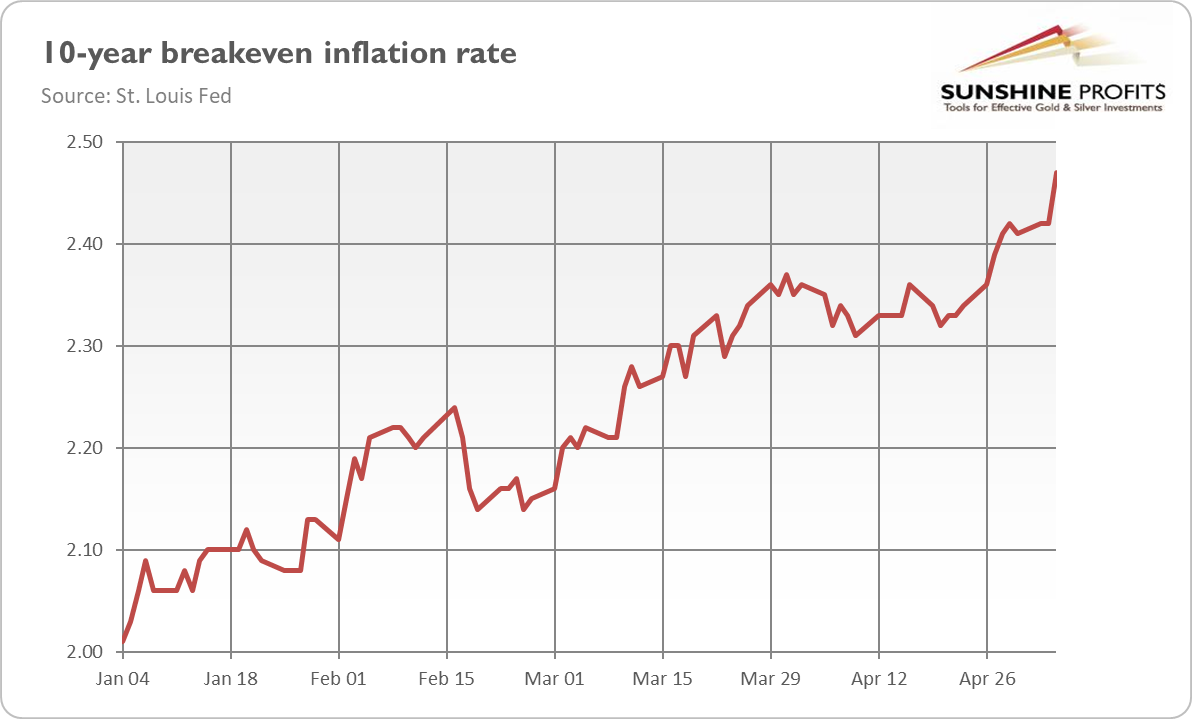

What is noteworthy here, the real interest rates declined more than the nominal interest rates. It resulted from the increase in the expected inflation. Indeed, as the chart below shows, the 10-year breakeven inflation rate jumped in early May. As a reminder, I wrote on Thursday that “the inflationary pressure could help the yellow metal to free itself from the shackles” and this is exactly what happened.

Implications for Gold

What does gold’s jump above $1,800 imply for its future? Well, the crossing of an important obstacle is always a positive development. The decline in the interest rates, coupled with the weakness in the US dollar, means that the markets are convinced that the Fed would remain very dovish, even despite the rising inflation.

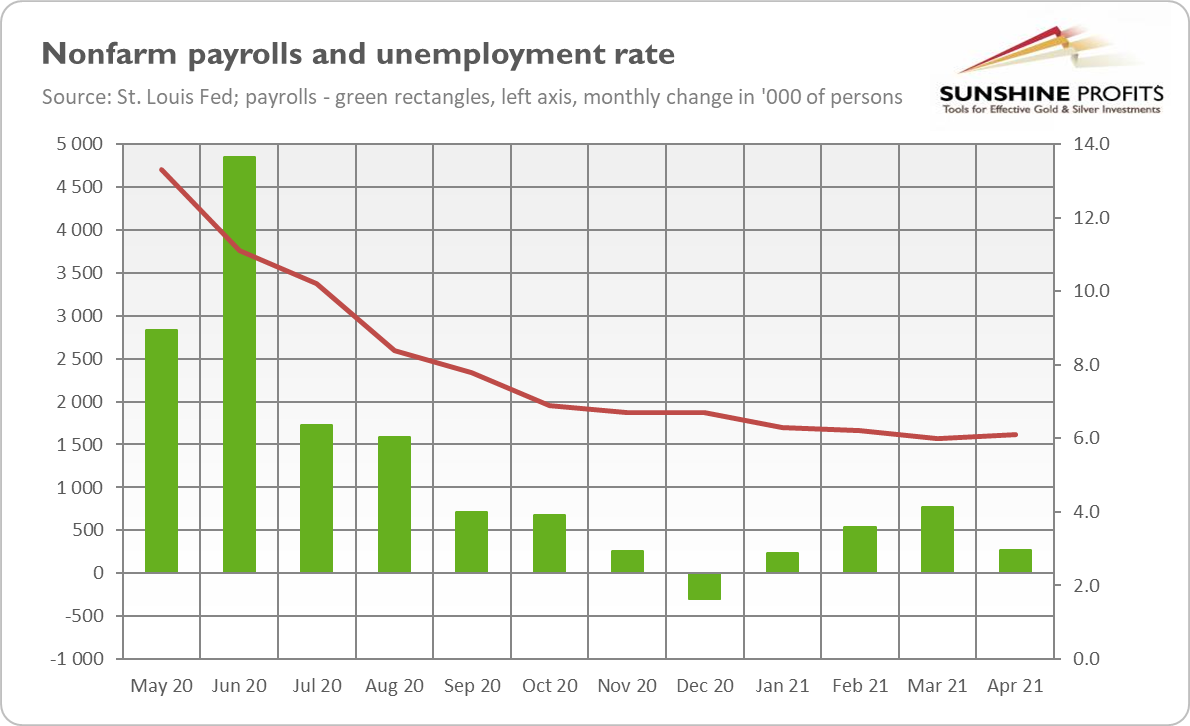

Other positive news for the gold market is April’s nonfarm payrolls that came in below the forecasts. The US economy added only 266,000 jobs last month (see the chart below), although many analysts and even the FOMC members expected a nearly 1 million increase in employment. Such a disappointment made traders slash the bets on the pace of the Fed’s monetary tightening. A softer expected path of the federal funds rate is a fundamentally positive factor for gold.

In other words, the weak employment report relieves a lot of the pressure put on the Fed to tighten its monetary policy. So, the US central bank will continue to provide monetary support, despite all the progress observed in the economy, and that easy stance will stay with us for longer than previously expected. In that sense, April’s disappointing jobs data may be a game-changer for gold, and it could add fuel to the recent rally that started on Thursday.

Of course, one weak employment number doesn’t erase the impressive economic recovery. Moreover, I would like to see that gold hold the recent gains through the coming days before organizing a party for the gold bulls. However, it seems that I was right in saying that the second quarter would be much better than the first one. Gold is indeed gaining momentum! And, what’s really important, the yellow metal started to rise amid a strong economic recovery – it implies that we can be observing important, bullish shifts in the market sentiment towards gold.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Lumber and Copper Are Surging. Will Gold Join the Party?

May 6, 2021, 9:20 AMThere’s no inflation… None at all. Only, completely by accident, lumber prices are skyrocketing. Gold is likely to remain silent, but it may catch up later.

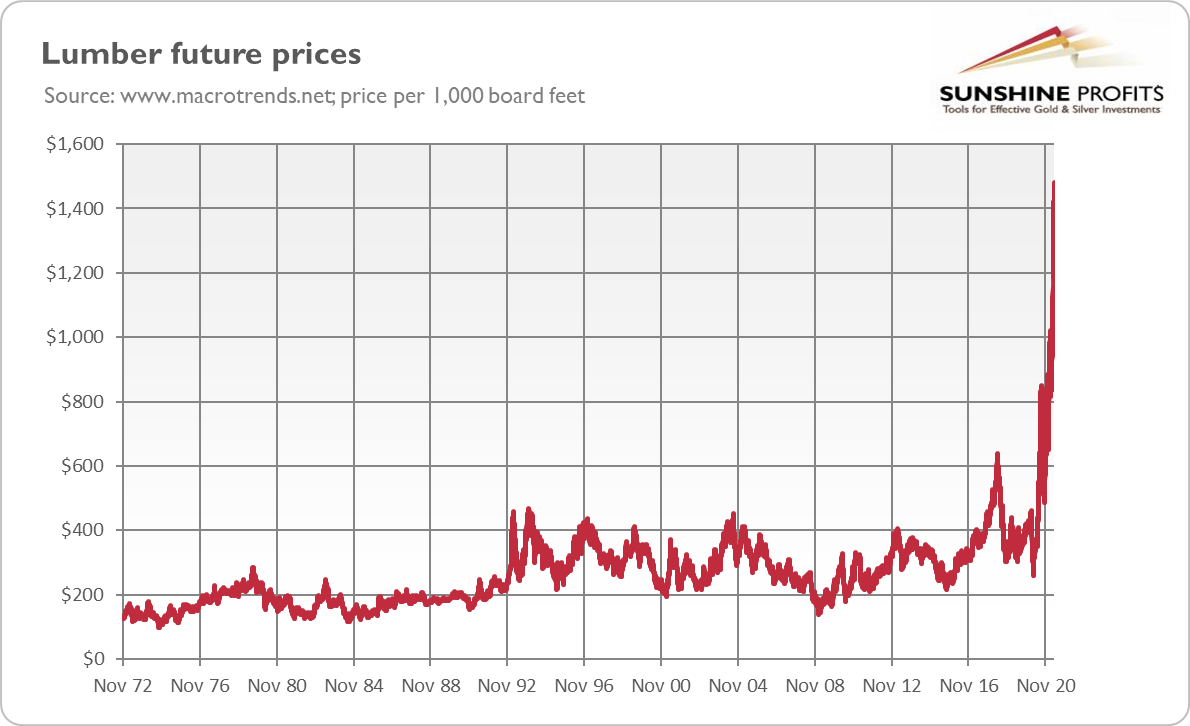

The rise in lumber prices can be seen in the chart below:

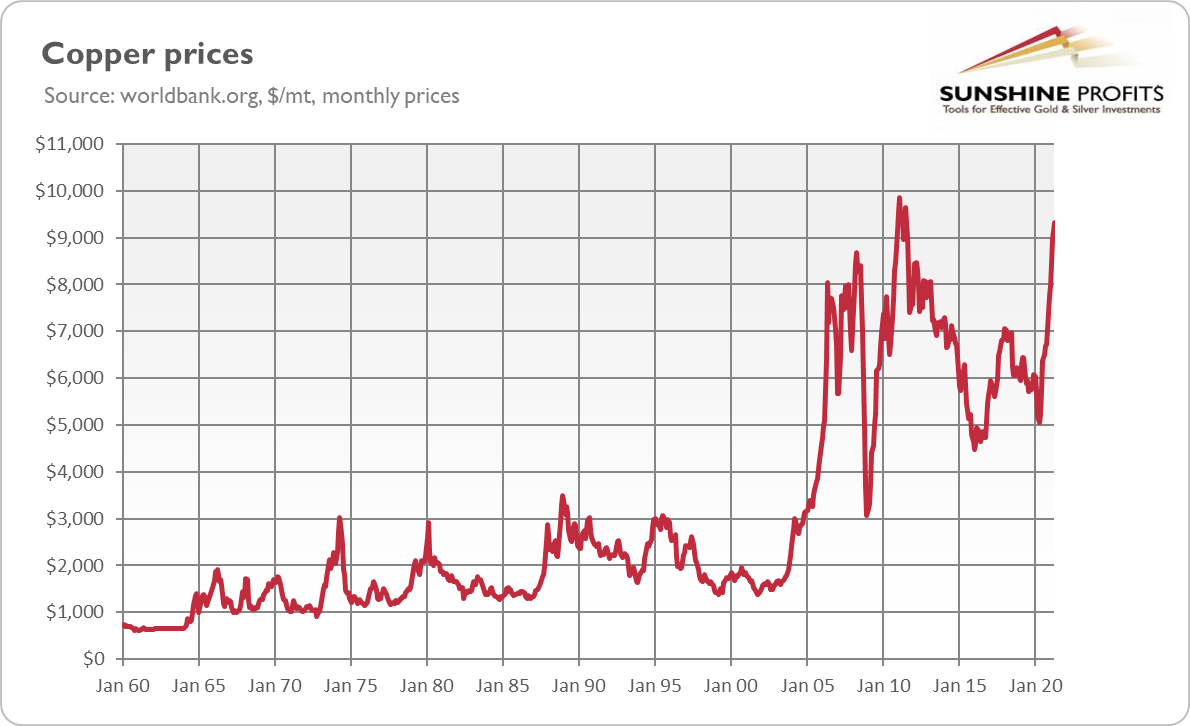

What a surge! It happened because of the limited supply and strong demand for new houses. But it’s not just lumber. Many raw commodities are rallying too. The price of copper, for example, has just approached its record height (from February 2011), as the recovery of the global economy boosted demand. Just take a look at the price below.

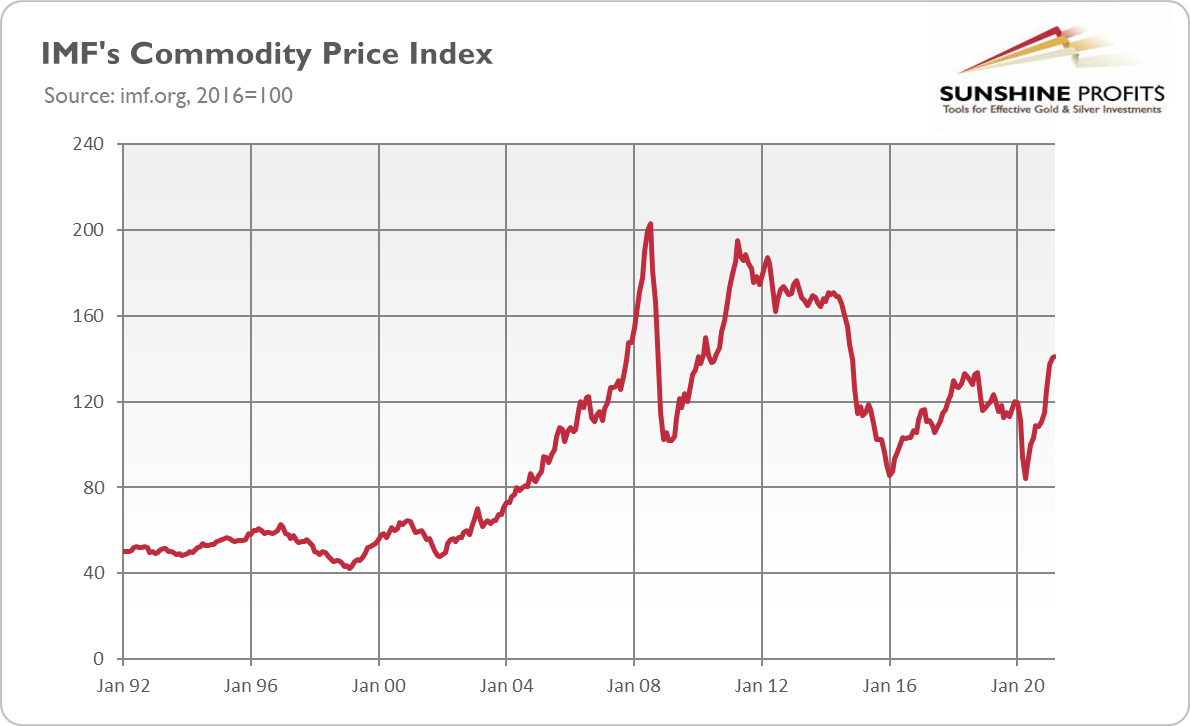

Indeed, the trend is up. Commodity prices are on the rise as a whole as the chart below clearly shows. Even Warren Buffet warned investors against a “red hot” recovery, saying that his portfolio companies were “seeing very substantial inflation” amid shortages of raw materials.

Of course, commodity price inflation and consumer price inflation are quite different phenomena, as consumers don’t buy lumber or copper directly but only finished products made from these materials. However, at least part of this producer price inflation may translate into higher consumer prices, as producers’ ability to pass higher costs on consumers has recently increased – people have a large holding of cash and are willing to spend it.

Implications for Gold

What do rallying commodity prices imply for the precious metals? Well, rising commodity prices signal higher inflation, which should increase the demand for gold as an inflation hedge. Of course, there might be some supply disruptions and bottlenecks in a few commodities. However, the widespread character and the extent of the increase in prices suggest that monetary policy is to blame here and that inflation won’t be just transitory as the Fed claims.

What’s more, the commodity boom is usually a good time for precious metals. As the chart below shows, there is a strong positive correlation between the broad commodity index and the precious metals index.

There was a big divergence during the pandemic when commodities plunged, while gold at the same time shined brightly as a safe-haven asset. So, the current lackluster performance of the yellow metal is perfectly understandable during the economic recovery.

Indeed, the rebound in gold has been weak, and gold hasn’t even crossed $1,800 yet, although it was close this week, as the chart below shows.

There was a rally on Monday (May 3) amid a retreat in the US dollar, but we were back in the doldrums on Tuesday, amid Yellen’s remarks about higher bond yields. She said that interest rates could rise to prevent the economy from overheating:

It may be that interest rates will have to rise somewhat to make sure that our economy doesn't overheat, even though the additional spending is relatively small relative to the size of the economy

However, Yellen clarified her statements later, explaining that she was not recommending or predicting that the Fed should hike interest rates. Additionally, several FOMC members made their speeches, presenting the dovish view on the Fed’s monetary policy. For example, Richard Clarida, Fed Vice Chair, said that the economy was still a long way from the Fed’s goals and that the US central bank wasn’t thinking about reducing its quantitative easing program.

Anyway, the price of gold has been trading sideways recently as it couldn’t break out of the $1,700-$1,800 price range. This inability can be frustrating, but the inflationary pressure could help the yellow metal to free itself from the shackles. The bull market in gold started in 2019, well ahead of the commodities. Now, there is a correction, but gold may join the party later. It’s important to remember that reflation has two phases: the growth phase when raw materials outperform gold and the inflation phase when gold catches up with the commodities. So, we may have to wait for a breakout a little longer, but once we get it, new investors may flow into the market, strengthening the upward move.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

Gold Reports

Free Limited Version

Sign up to our daily gold mailing list and get bonus

7 days of premium Gold Alerts!

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM