-

US Government Stimulus Went Wrong. How Will Gold React?

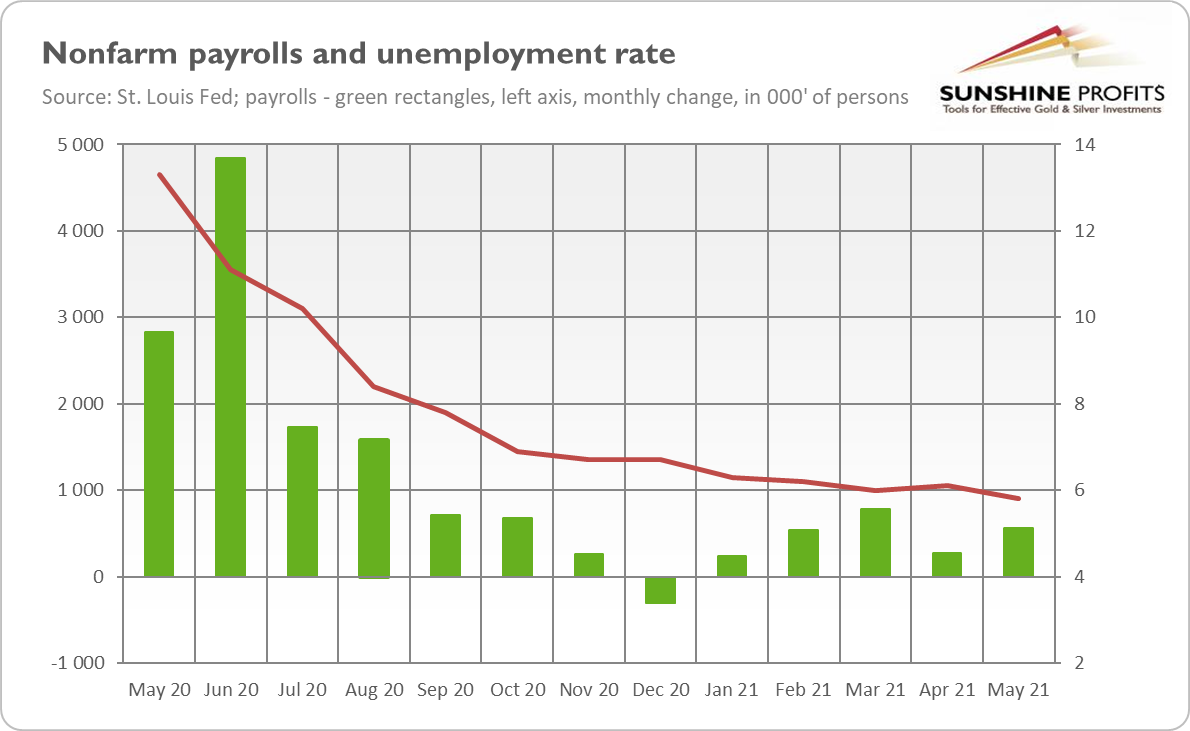

June 8, 2021, 12:51 PMGold may benefit from government money flooding households and people less willing to work – as evidenced by the low value of nonfarm payrolls.

According to the recent BLS Employment Situation Report, total nonfarm payrolls rose by 559,000 in May, following disappointing increases of 278,000 in April, as the chart below shows. What is disturbing here is that this time the US economy also added significantly fewer jobs than expected – economists surveyed by MarketWatch forecasted 671,000 additions. Moreover, labor force participation and employment-population rates were little changed, remaining significantly below the pre-pandemic levels.

On the positive side, the unemployment rate edged down from 6.1% to 5.8%, as the chart above shows. However, even though the number of unemployed people fell considerably from its recent high in April 2020, it remains well above the level seen before the Covid-19 epidemic. In February 2020, 5.7 million Americans were without a job, while now it is 9.3 million. It means that the labor market is still far from recovery. Or, actually, given all the generous unemployment benefit supplements introduced during the pandemic, the new equilibrium unemployment rate may be simply higher than in the past.

Implications for Gold

Anyway, the new employment situation report is positive for the gold market. May nonfarm payrolls report is disappointingly weak and missed expectations for the second month in a row. It means that the April report wasn’t just an accident, and the US labor market has to face some serious problems.

The sad truth is that Americans don’t want to work. Even the decline in the unemployment rate was caused to a large extent by the drop in the labor participation rate, as workers just left the labor market. This fact explains why employers report worker shortages despite an army of a few million unemployed people. According to the recent Fed’s Beige Book, many companies have difficulties finding new employees, so they had to boost their wages to attract candidates:

It remained difficult for many firms to hire new workers, especially low-wage hourly workers, truck drivers, and skilled tradespeople (…) A growing number of firms offered signing bonuses and increased starting wages to attract and retain workers.

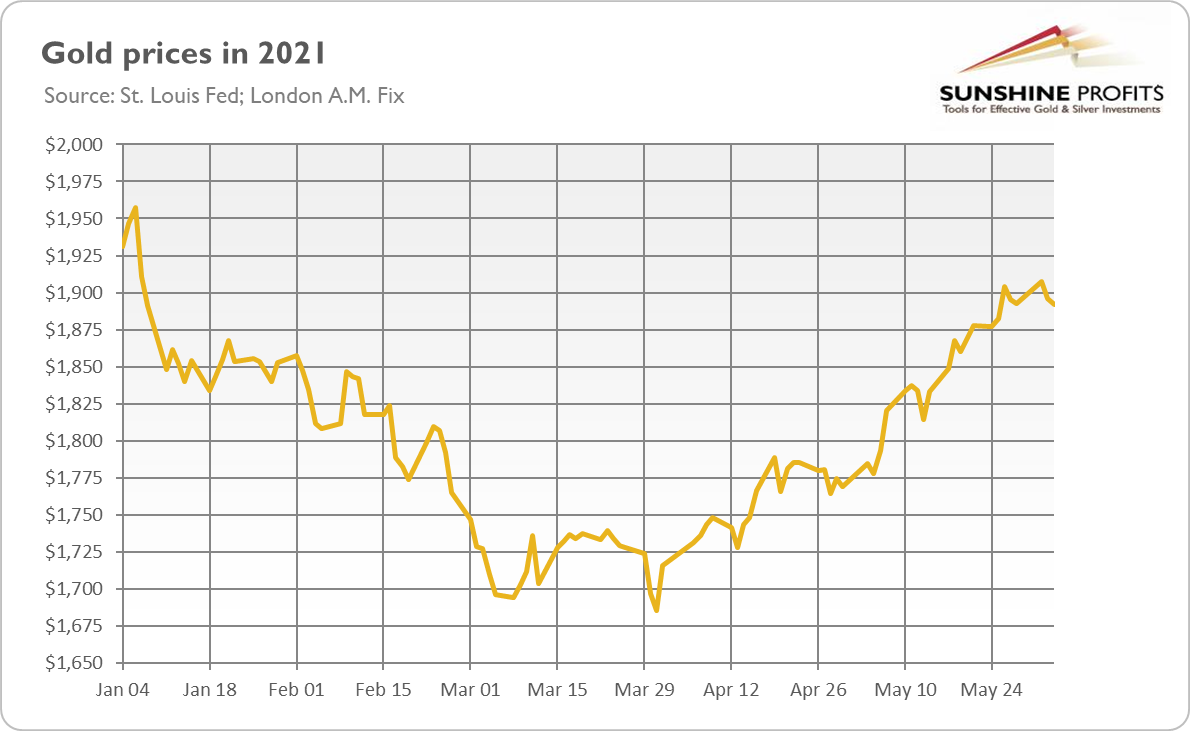

Even the BLS admitted that “rising demand for labor associated with the recovery from the pandemic may have put upward pressure on wages”. Indeed, wage increases accelerated to 2% in May year-over-year, up from just 0.4% in the previous month. They could add to the inflationary pressure or reduce companies’ margins and investments, reducing the pace of real economic growth. So, the jump in wages seems to be good for gold. Hence, the yellow metal could continue its long-term upward trend after the recent pullback below $1,900 (see the chart below).

Additionally, disappointing employment situation news will postpone tapering of the Fed’s quantitative easing. The weak nonfarm payrolls report gives a strong hand to the doves within the FOMC who don’t want to even start talking about talking about tapering. Hence, the US monetary policy should remain very dovish, with the real interest rates at ultra-low levels supporting gold prices. Indeed, the expected path of the federal funds rate, derived from the Fed Fund futures, has declined from the prior levels.

In other words, although May nonfarm payrolls report is an improvement when compared to April, the level of employment is still 7.6 million below its pre-pandemic peak. So, even if we see further improvement later this year (which is likely, as many states end the unemployment benefit supplements this month), it will take several more months to fully eliminate the slack in the labor market. The implication is clear: precious metals investors shouldn’t bet on a change in the Fed’s stance anytime soon. And as the yellow metal is very sensitive to tapering fears, this is positive news for gold bulls.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Gold Seems Stuck at $1900. Are Inflationary Fears Exaggerated?

June 3, 2021, 7:40 AMGold is fluctuating around $1,900 amid a sideways trend in real interest rates and a decline in inflationary expectations.

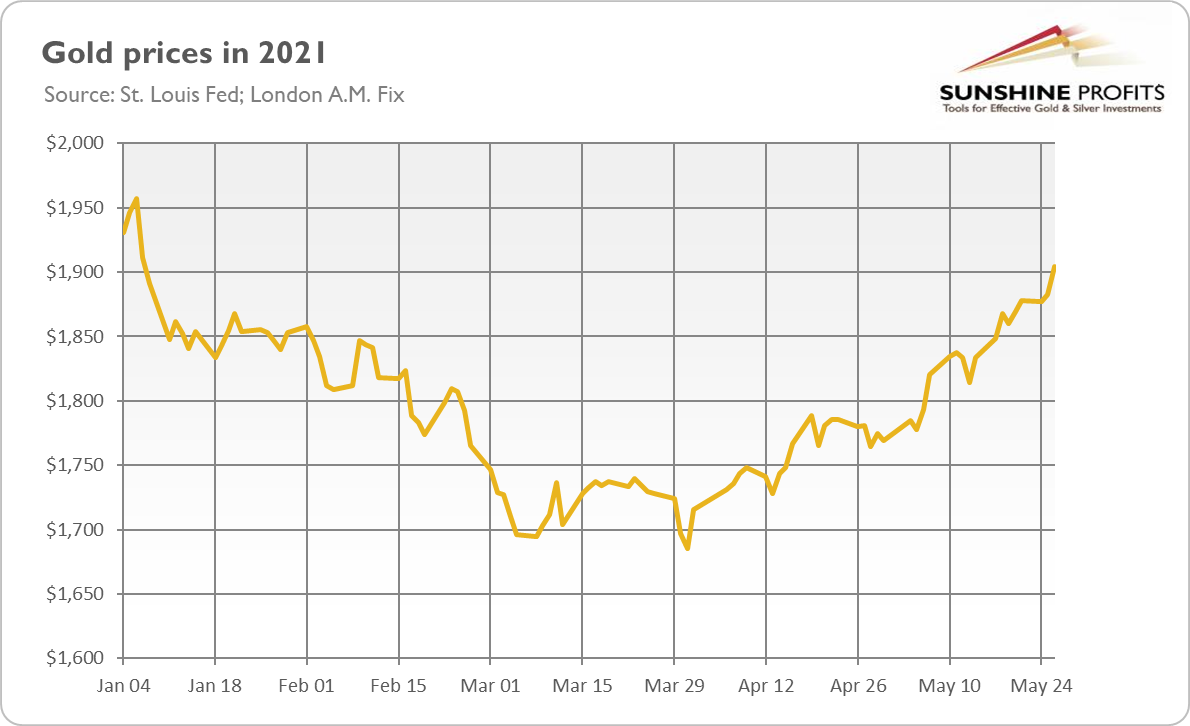

Gold surpassed $1,900 at the end of May. However, it has been struggling since then to rally decisively above this level. Instead, the price of the yellow metal has been oscillating around this level, as the chart below shows.

Why is that and what does it mean for the gold market? Well, on the one hand, we could say that the yellow metal is in a normal pause during an uptrend. However, the lack of more aggressive price appreciation amid high inflation, ultra-loose monetary policy, depreciating dollar and super easy fiscal policy could be seen as disturbing.

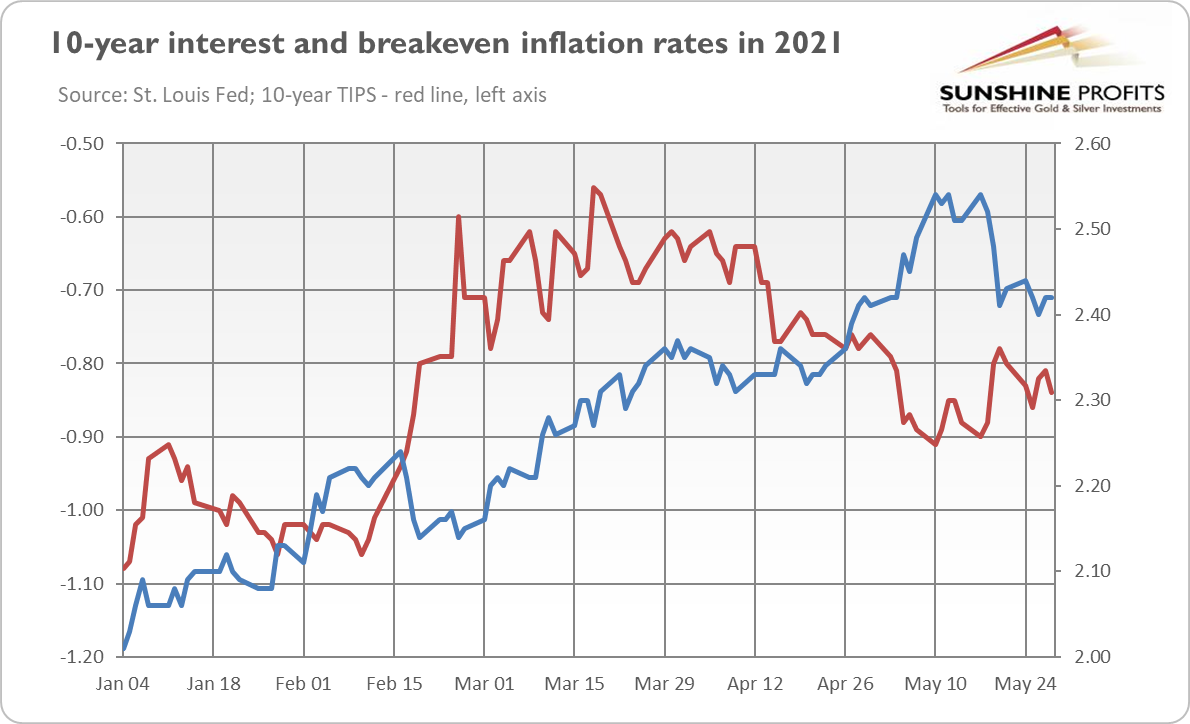

From a fundamental perspective, the timid price behavior of gold could be explained by a sideways trend in real interest rates. Their lackluster movement, in turn, could have resulted from the downward correction in long-term inflationary expectations (blue line), as the chart below shows.

Investors’ inflation bets have lost some steam, starting a debate about whether expectations of inflation have already peaked. After all, it might be the case that inflation fears have been exaggerated and investors have overshot, as they often do. In addition, some of the FOMC members signaled that it could be a good idea to begin discussing tapering quantitative easing.

If this was really the peak of inflationary expectations, the news would be bad for gold, which is seen as a hedge against inflation. However, many analysts expect that inflation expectations have room for further rises and could reach levels close to 3%.

Implications for Gold

What does all this mean for the price of gold? Well, market-based inflationary expectations have recently declined, dragging the real interest down and restraining gold from moving upward. However, inflation worries won’t disappear anytime soon. After all, the PCE inflation, the favorite Fed’s inflation gauge, jumped 3.1% in April, beating the expectations. Even in the Eurozone, where price pressure is usually lower than in the US, the inflation rate rose from 1.6% to 2% in May, which is the highest level since October 2018.

Furthermore, consumer-based inflationary expectations jumped from 3.4% to 4.6% in May, so inflation worries are still around. They could increase the uncertainty and increase the safe-haven demand for gold. Although higher uncertainty could limit some spending, we should remember that households have accumulated more than $2 trillion in excess savings during the pandemic. So, inflation may be more lasting than many policymakers and pundits believe. If inflation doesn’t turn out to be merely transitory, gold could gain some fuel for the upward march.

Higher inflation implies weakened purchasing power of the dollar. If we add America’s growing public debt problem to constantly rising prices, the downward trend in the greenback could continue, supporting the price of gold.

Of course, only time will tell whether or not current inflation worries are justified. However, please note that the economy didn’t collapse last year due to a lack of liquidity but due to the Great Lockdown. The implication is that the Fed has increased money supply well above demand, injecting a lot of liquidity into the system. The expansion in the Fed’s balance sheet and commercial banks’ credit (after all, this time not only the monetary base has jumped, but the broad money supply as well), combined with the Great Unlocking, generated a great inflationary wave that lifted all asset classes: from commodities, through equities, to cryptocurrencies, including crypto-memes like Dogecoin.

And it might be just a coincidence, but the Fed introduced a new monetary regime that is prone to higher inflation also during the last year. A cynical interpretation could be that the Fed knew very well that its last year’s monetary expansion could result in higher inflation.

Hence, inflationary expectations didn’t have to peak, and they could increase later this year supporting gold prices. Having said that, if inflation really turns out to be only transitory, the current situation wouldn’t be much different from 2011-2013, when gold prices struggled amid expectations of monetary policy tightening. Of course, the Fed is even more dovish now under Powell than under Bernanke or Yellen, but higher inflation would be an additional argument for a bull market in gold.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Biden Proposes $6 Trillion Budget. Will Money Flow Into Gold?

June 1, 2021, 9:33 AMBiden proposes $6 trillion of government spending in the 2022 fiscal year. This continuation of ultra-loose fiscal policy could support gold in the long run.

On Friday (May 28), the White House presented the President’s budget for the 2022 fiscal year that starts on October 1, 2021. Biden trumped Trump and proposed $6 trillion, over one trillion more than Trump in his last year’s proposal for $4.8 trillion. Furthermore, POTUS wants to raise government outlays to up to $8.2 trillion by 2031.

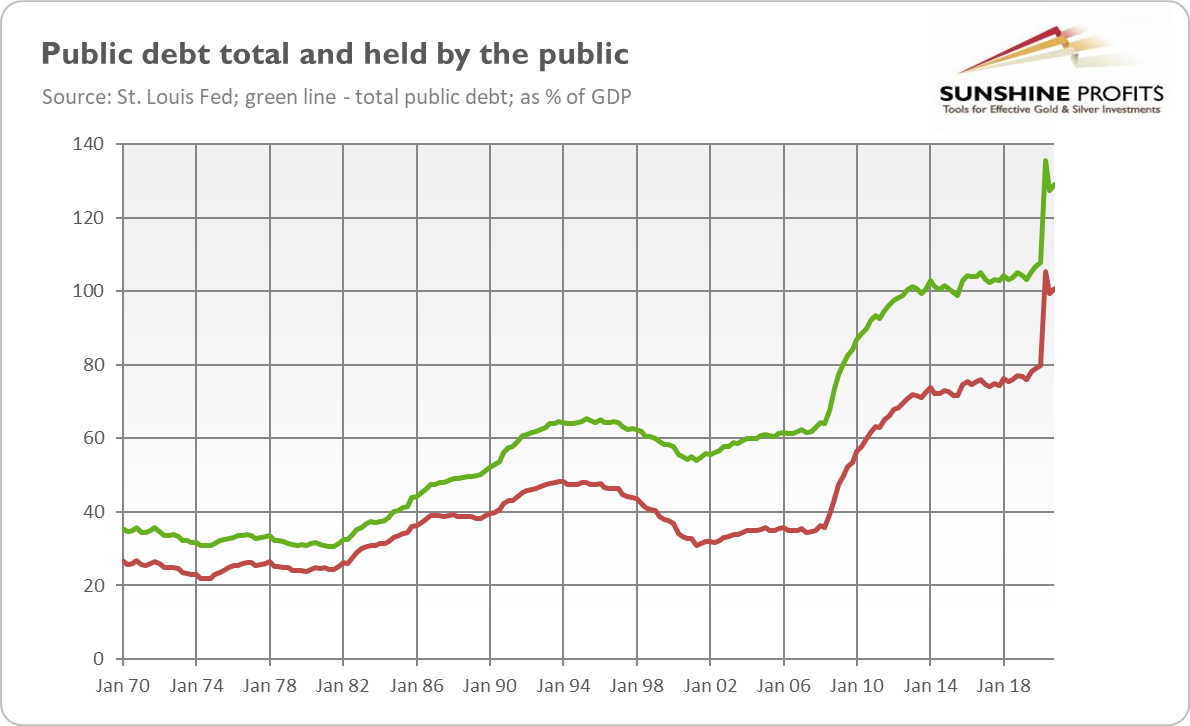

According to the White House, the proposed fiscal agenda will further increase the total federal debt-to-GDP ratio, from the current 129.1% to 136.9% by 2031. Meanwhile, the federal debt held by the public is estimated to rise from the current 100.7% to 108.5% of the GDP. The current level of the US public debt compared to the size of the economy is presented in the chart below.

Despite the increase, Janet Yellen, Treasury Secretary, said that “it is a fiscally responsible program”. Yeah, right. Of course, it’s true that real interest rates are very low, and therefore the debt service costs are bearable; but the interest rates could go up one day. And even when the bond yields are low, there is still the crowding out effect and other negative consequences, as higher government expenditures imply higher taxes and fewer resources for the private sector. Last but not least, the GDP has practically returned to the pre-pandemic level, so such big fiscal programs are clearly excessive and could add to inflationary pressure.

Implications for Gold

What does the budget for the next fiscal year mean for gold prices? Well, although Trump was trumped in the last elections, trumpism is still doing well. Here I’m referring to the fact that Trump started to balloon the government spending and fiscal deficits well before the pandemic. Then the coronavirus hit and the fiscal policy became even looser. And now President Biden raises the stake, widening the budget deficit and public debt despite the recovery from the economic crisis.

In the short term, it doesn’t have to be good news for gold. This is because big deficits and federal debt could exert upward pressure on the Treasury yields, resulting in higher interest rates, which would suppress the price of gold.

Also of importance is the fact that the 2021 fiscal year was a period with an unprecedented size of the fiscal stimulus. So, although Trump proposed ‘only’ $4.8 trillion of government spending and almost $1 trillion of deficit, the actual numbers were much bigger: $7.2 and $3.7 trillion, respectively. In contrast, Biden’s proposal sees the budget deficit worth ‘only’ $1.8 trillion. In relative terms, the fiscal deficit is projected to decline from the current 16.7% to 7.8%.

Of course, the actual numbers will probably be bigger than the White House’s projections. But still, when compared to the previous year, the fiscal policy will become tighter – on a relative basis. However, the fiscal policy will remain ultra-loose; the fiscal deficits are never assumed to decline below $1.3 trillion or 4.2 percent of the GDP, and the public debt is projected to reach a level not seen since World War II.

However, the Fed is ready to intervene if the interest rates increase too much. And, at some point, the current ‘debt elephant’ will become too big to pretend it’s not present in the room. The current policy mix of ultra-loose monetary policy and ultra-loose fiscal policy (despite the economic recovery) is unprecedented and raises the risk of a debt crisis in the more distant future. It seems that some policymakers are starting to notice that, as they switched their narrative from “debt is no problem” to “we have to pay for it through raising corporate taxes”. We can see that even in the White House’s document, as it factors in an increase in the corporate tax rate from 21% to 28%.

Hence, the continuation of the US’s irresponsible fiscal policy could add to the positive momentum in the gold space, especially while taking into consideration that all these new social and infrastructure programs arrive during a period of economic expansion and inflationary pressure. So, the era of big government (with bigger government expenditures and fiscal deficits) and higher inflation is back. It could be, thus, an era of shining gold.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Gold Surpasses $1,900. What’s Next?

May 27, 2021, 10:19 AMGold surpassed $1,900 most recently – and it’s likely that the rally will continue for a while.

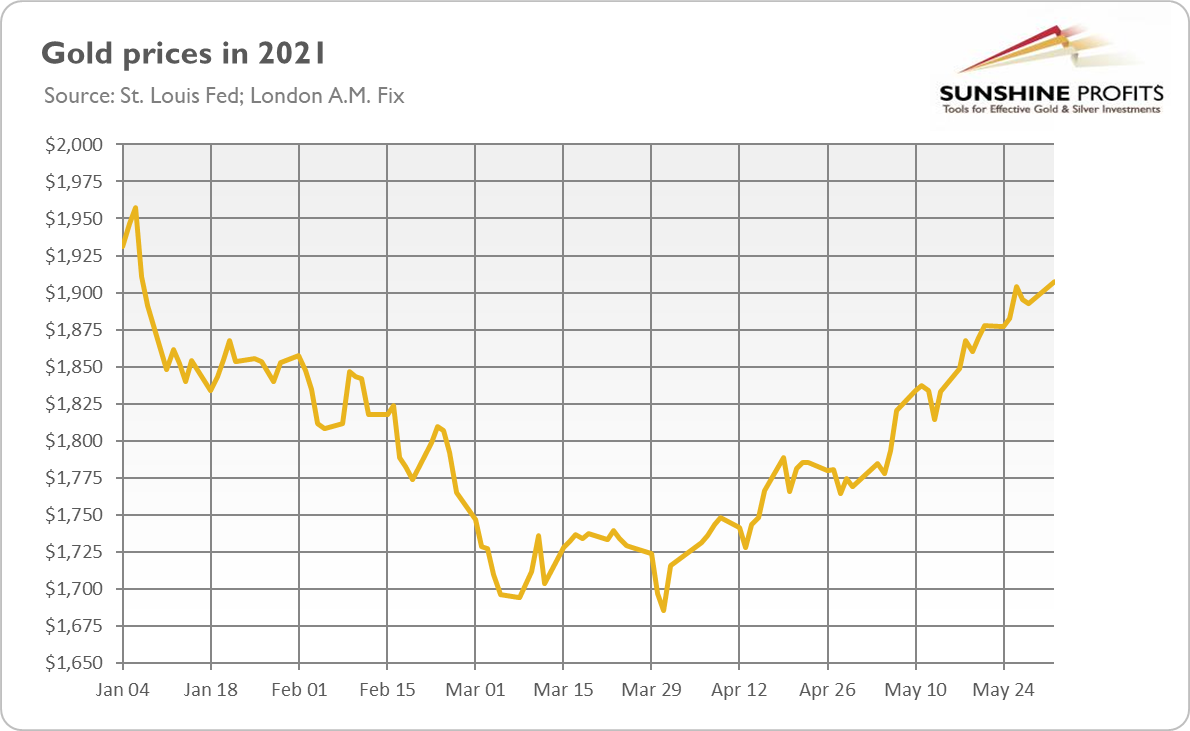

Gold bulls have an opportunity to celebrate. As the chart below shows, the price of gold has been rising recently. And yesterday (May 26) it finally jumped above $1,900, which is an important psychological level.

The question we should ask now is “what’s next?” Well, as the jokes go on, the price of gold will either go up or down. But in earnest, there are significant downside risks for the yellow metal. First of all, the Fed could overreact to rising inflation and increase real interest rates.

However, these worries seem to be overblown. The Fed’s monetary policy is always asymmetrical, i.e., it eases its stance in response to recession more than it tightens it in response to inflation. The federal funds rate gets lower and stays at these low levels for longer, partially because of all the enormous indebtedness of the contemporary economy.

The tapering is surely the risk that looms on the horizon. But the Fed will maintain its quantitative easing and zero-interest-rate policy for at least the rest of 2021. So, there is still room for gold to move further north, especially after the recent turmoil in the cryptocurrency market resulting in renewed confidence in gold as an attractive inflation hedge.

After all, the US monetary policy is loose, and real interest rates are still in negative territory. The fiscal policy remains very easy, and the public debt is high. Inflation is huge and rising. And there is also an issue of depreciation of the greenback. The Fed’s easy stance, low interest rates and high inflation weaken the US dollar, supporting gold prices.

Last but not least, the level of risk appetite/confidence in the Fed and the economy has already reached its peak, as the GDP has recovered with an unprecedentedly high pace of growth. In other words, the post-pandemic euphoria is behind us – now the harsh, inflationary reality sets in. Maybe we won’t repeat the 1970s stagflation, but inflation is probably more deeply embedded than the Fed thinks. And it seems that the markets are finally getting this idea, pushing some investors into gold’s warm and shiny embrace.

Implications for Gold

What does it all mean for gold prices? Well, recently two broad trends have dominated the markets: rising inflation expectations and rising economic confidence. In other words, market participants expected reflation. However, economic confidence has peaked, and now investors focus more on inflation. So, we are moving slowly from the reflation phase to the inflationary phase, which is beneficial for gold – if this trend continues, the yellow metal could continue its upward march.

Every investor should remember one great historical pattern, basically as old as the Roman Empire. The money supply is first aggressively boosted with the excuse that “there is no inflation”. When upward pressure on prices becomes clear, that excuse transforms into “inflation is transitory” or into “the rise in inflation is caused by idiosyncratic factors”. Have you heard about Arthur Burns, the Fed Chair in the 1970s and the predecessor of Paul Volcker? As Stephen Roach notes on him:

Over the next few years, he [Burns] periodically uncovered similar idiosyncratic developments affecting the prices of mobile homes, used cars, children’s toys, even women’s jewelry (gold mania, he dubbed it); he also raised questions about homeownership costs, which accounted for another 16% of the CPI. Take them all out, he insisted!

Finally, the officials admit that there is inflation, but they blame it on speculators and other external, unfavorable or even hostile factors. To be clear, I’m not predicting hyperinflation or even double-digit inflation in the US, but recent economic reports suggest that upward price pressure could be more lasting than the Fed and the pundits believe.

So, inflation could remain elevated for a while, especially given that the description of Burns downplaying it is worryingly similar to the current Fed’s stance under Powell. As Stephen Roach points out, the current size of fiscal and monetary stimuli is unprecedented, especially taking into account the pace of the recovery:

Today, the federal funds rate is currently more than 2.5 percentage points below the inflation rate. Now, add open-ended quantitative easing – some $120 billion per month injected into frothy financial markets – and the largest fiscal stimulus in post-World War II history. All of this is occurring precisely when a post-pandemic boom is absorbing slack capacity at an unprecedented rate. This policy gambit is in a league of its own.

Indeed, but gold loves chess, gambits included. After all, chess is a royal game, while gold is a royal metal!

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

-

Rising Cost Pressure - What Will Mr. Powell and Mr. Gold Do?

May 25, 2021, 9:27 AMThe latest IHS Markit Flash U.S. Composite PMI signals very fast economic expansion – but also strong inflationary pressure. Good news for gold, overall.

On Friday, the recent IHS Markit Flash U.S. Composite PMI has been published. There are two pieces of news for gold - one good and one bad. Let’s start with the negative information. The report signals an unprecedentedly fast expansion in business activity in May. Indeed, the composite index surge from 63.5 in April to 68.1 this month established a new record.

More importantly, both manufacturing and services sectors’ markets have shown strong growth. The former index rose from 60.5 in April to 61.5 in May (also a new record), while the PMI for services soared from 64.7 to 70.1, marking the sharpest jump since data collection for the series began in October 2009. Such an unprecedentedly fast acceleration of growth in the PMI signals strong economic growth, which is clearly bad news for the safe-havens such as gold (however, strong economic growth is something everyone expected, so it might be already priced in as well).

The good information is, however, that at least part of this growth is inflationary, as soaring demand greatly improved the firm’s pricing power. And the input costs have surged, leading to the sharpest rise in output charges since the end of the Great Recession when the data collection started:

Increasing cost burdens continued to be keenly felt, as the rate of input price inflation soared to a new survey record high, often linked to a further marked worsening of supplier performance. Commonly noted were increases in PPE, fuel, metals and freight costs amid significant supplier delays.

The steep rise in costs fed through to the sharpest increase in output charges since data collection began in October 2009, with record rates of inflation registered for both goods and services as soaring demand boosted firms’ pricing power.

What’s more, wage inflation is also coming, as the report says that entrepreneurs couldn’t find people to fill the vacancies. It seems that generous benefits introduced in a response to the recession discouraged people from searching for work, and slack in the labor market is greatly exaggerated.

Although a solid expansion in staffing levels eased some pressure on backlogs in the service sector, manufacturers registered the fastest rise in work-in-hand on record amid raw material shortages. While job creation was again seen in the goods-producing sector, the rise was the slowest for five months, linked in part to difficulties filling vacancies.

In other words, the post-pandemic natural employment will be simply lower because of the institutional changes, not because of weak aggregate demand. How would you explain otherwise the fact that entrepreneurs cannot find workers amid employment lower by 8 million when compared to the pre-pandemic level?

But this is good news for gold. The subdued employment would be a great excuse for the Fed to say that there is slack in the labor market, the aggregate demand is weak, and the economy remains fragile and below the Fed’s targets, so it still needs easy monetary conditions. Hence, Powell would stay passive and would even avoid starting to think about tapering the quantitative easing and hiking interest rates. Dovish Fed and rising prices would support gold prices.

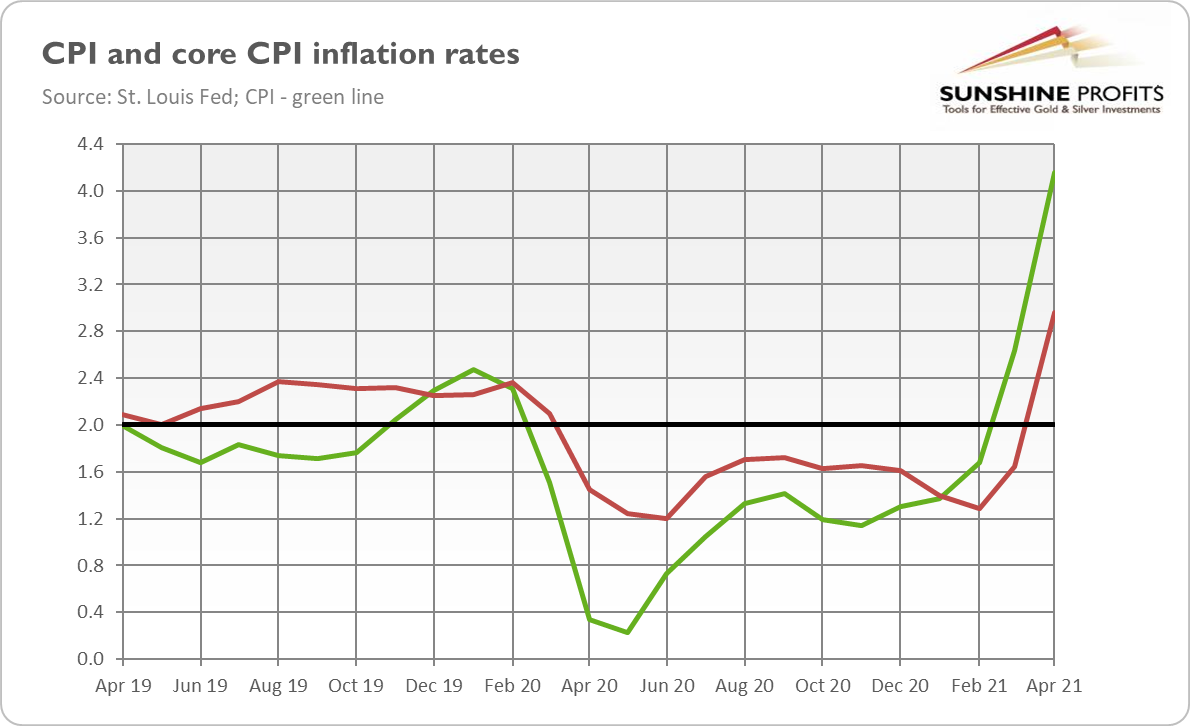

So, high inflation (see the chart below) should remain with us for a while. Indeed, manufacturers worry that raw material shortages “could extend through 2021” and producer price inflation translates into consumer price inflation with a certain lag. Anyway, high inflation won’t disappear in one or two months, but it could last for at least a few or even several months if the Fed remains ultra-dovish and people lose confidence in the central bank’s ability to maintain price stability.

If this scenario happens, inflation expectations could cease to be “well-anchored” and inflation could get out of control, just as it did during stagflation in the 1970s. Chris Williamson, Chief Business Economist at IHS Markit, seems to agree with me in his comment on the report:

The May survey also brings further concerns in relation to inflation, however, as the growth surge continued to result in ever-higher prices. Average selling prices for goods and services are both rising at unprecedented rates, which will feed through to higher consumer inflation in coming months.

Implications for Gold

What does the recent IHS Markit Flash U.S. Composite PMI imply for gold? Well, strong economic activity is bad for gold, given that it usually shines during bad times. However, the yellow metal doesn’t like genuine, real growth, but it performs pretty well during inflationary periods. Of course, part of the growth comes from the reopening of the economies, but there is no doubt that this expansion is accompanied by high inflation.

I’ve been warning readers since the very early part of the pandemic that the following expansion will be more inflationary than the previous one. This is excellent news for gold, which entered a bear market in 2011-2013 (i.e., when the former expansion settled down). What’s important here is that the economic environment is more inflationary (we have easier monetary and fiscal policies) while at the same time the Fed is highly tolerant of high inflation – this is a truly dangerous cocktail, but it could be quite tasty for gold.

If you enjoyed today’s free gold report, we invite you to check out our premium services. We provide much more detailed fundamental analyses of the gold market in our monthly Gold Market Overview reports, and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. To enjoy our gold analyses in their full scope, we invite you to subscribe today. If you’re not ready to subscribe yet, and you are not on our gold mailing list yet, we urge you to sign up there as well for daily yellow metal updates. Sign up now!

Arkadiusz Sieron, PhD

Sunshine Profits: Analysis. Care. Profits.-----

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our Gold & Silver Trading Alerts.

Gold Reports

Free Limited Version

Sign up to our daily gold mailing list and get bonus

7 days of premium Gold Alerts!

Gold Alerts

More-

Status

New 2024 Lows in Miners, New Highs in The USD Index

January 17, 2024, 12:19 PM -

Status

Soaring USD is SO Unsurprising – And SO Full of Implications

January 16, 2024, 8:40 AM -

Status

Rare Opportunity in Rare Earth Minerals?

January 15, 2024, 2:06 PM